|

시장보고서

상품코드

2062048

IoT 마이크로컨트롤러 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)IoT Microcontroller - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

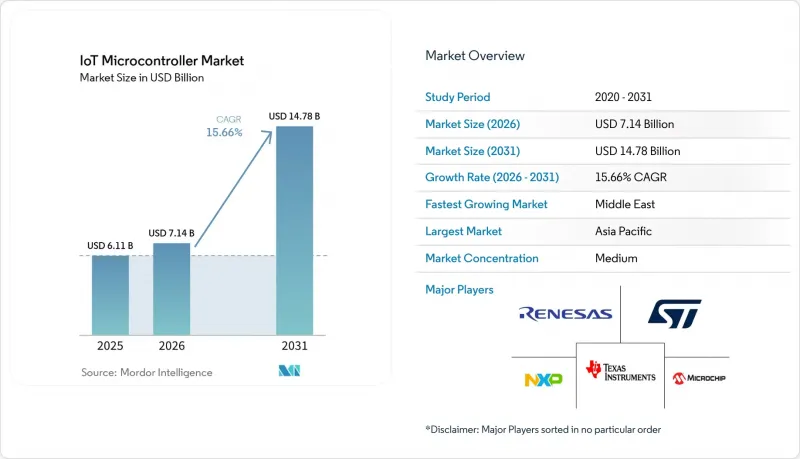

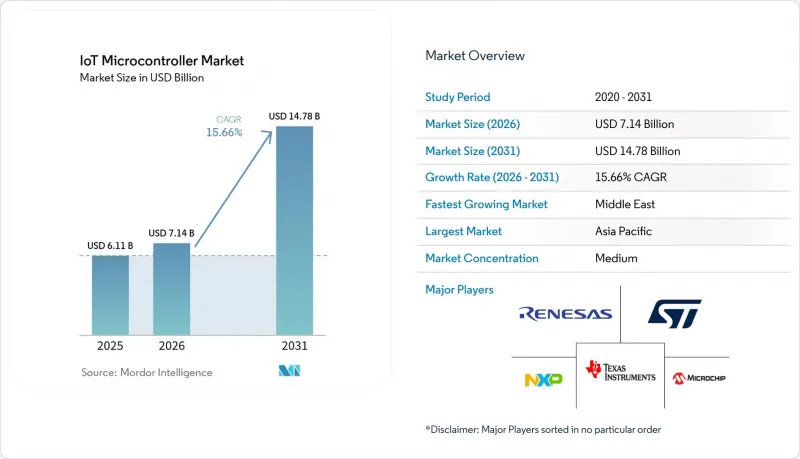

Mordor Intelligence에 의하면, IoT 마이크로컨트롤러 시장 규모는 2025년 61억 1,000만 달러로 평가되었고, 2026년에는 71억 4,000만 달러로 추정되고, 2031년까지 147억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 15.66%로 성장할 전망입니다.

본 보고서는 비트 클래스별(8비트, 16비트, 기타), 연결 유형별(통합 연결 없음, Wi-Fi, Bluetooth/BLE, Zigbee/Thread, 기타), 명령어 세트 아키텍처별(ARM, RISC-V, x86, 기타), 용도별(스마트 홈 및 웨어러블, 산업 자동화 및 IIoT, 자동차 및 운송, 기타), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 IoT 마이크로컨트롤러 시장 동향 및 인사이트

연결형 산업 시스템의 급속한 확대

플랜트 관리자들이 예상치 못한 가동 중단 시간을 줄이려 노력하는 가운데, 공장 디지털화 예산에서는 분산 제어와 분석이 우선순위로 꼽히고 있습니다. 모든 로봇 셀, 컨베이어 모듈, 스마트 툴에는 센서 퓨전과 결정론적 네트워크를 결합해야 하는 컨트롤러가 적어도 하나씩 내장되어 있습니다. 예지 유지보수 적용 사례에서는 온칩 아날로그 프런트엔드 외에도, 클라우드 지연 없이 진동 및 열 추론을 수행할 수 있는 충분한 여유가 필요합니다. 2025년에 출시된 인피니언의 PSoC Edge E8x 제품군은 ARM Cortex-M33 코어와 Ethos-U55 신경망 처리 유닛을 통합함으로써, 클라우드 지연 없이 온칩에서 이상 감지가 가능하도록 하여 이러한 추세를 잘 보여주고 있습니다. 신제품 제품군에는 IEC 62443 요건을 충족하기 위한 하드웨어 루트 오브 트러스트(RoT) 구성 요소가 내장되어 있으며, 부품 명세서(BOM)에서 보안이 신호 무결성과 동등한 수준으로 중요시되고 있습니다.

엣지 AI 디바이스에서 '보안 설계(Secure-by-Design)' MCU에 대한 수요 증가

서비스 로봇이나 자율형 드론 등 지연 시간을 허용할 수 없는 시스템에서는 추론 워크로드를 클라우드에서 보드 측으로 이전하는 추세가 확산되고 있습니다. 이러한 변화로 인해 모델 가중치 추출을 방지하기 위한 하드웨어 분리, 보안 부팅 및 변조 감지에 대한 요구 사항이 높아지고 있습니다. PSA Certified Level 2와 같은 인증 프레임워크는 설계상의 선택을 명확하게 정의된 위협 모델에 대조하여 검토하지만, 그와 동시에 개발 일정을 수개월 연장하게 됩니다. 각 브랜드는 EU 사이버 복원력 법 및 이와 유사한 미국 지침이 보안 조치가 미흡한 연결 기기에 대해 엄격한 책임을 부과하고 있기 때문에 이러한 일정상의 부담을 감수하고 있습니다.

새로운 ISA에서의 소프트웨어 생태계 분열

RISC-V의 오픈 라이선스는 로열티 지출을 줄여주지만, 제한 없는 맞춤형 확장 기능으로 인해 바이너리 호환성이 부족한 도구 체인이 뒤섞여 생겨나고 있습니다. 개발자들은 종종 실리콘의 각 변형마다 별도의 코드베이스를 유지하며, 이로 인해 비반복적 엔지니어링(NRE) 예산이 불어나고 있습니다. RVA 프로파일 등의 통합 작업은 진행 중이지만, 준수는 선택 사항이며, 보급 현황은 여전히 고르지 않습니다. 그로 인해 발생하는 불확실성은 15년간의 소프트웨어 지원을 보장해야 하는 자동차 및 의료기기 설계자들을 주저하게 만들고 있습니다.

부문별 분석

2025년에는 32비트급이 매출의 58.39%를 차지하며, 연산 성능의 한계와 비용 간의 균형이 뛰어나다는 점이 부각되었습니다. 이 등급의 대량 생산형 컨트롤러는 소형 머신러닝 라이브러리와 함께 실시간 OS를 실행하기 때문에 스마트 게이트웨이 및 팩토리 드라이브 시장을 독점하고 있습니다. IoT 마이크로컨트롤러 시장은 벡터 연산 유닛과 온칩 보안 블록을 탑재한 제품으로 계속해서 전환되고 있으며, 이는 암호화 처리량을 저하시키지 않으면서도 결정론적 제어를 가능하게 합니다. 2024년에 출시된 라즈베리 파이(Raspberry Pi)의 RP2350은 ARM Cortex-M33 또는 RISC-V Hazard3 명령어 중 하나를 실행할 수 있는 듀얼 코어 구성을 채택하여, 개발자에게 아키텍처의 유연성과 32비트에서 64비트 워크로드로의 전환 경로를 제공합니다.

고해상도 이미징 및 멀티 센서 융합에는 더 넓은 주소 공간이 필요하기 때문에 64비트 컨트롤러 수요는 연평균 성장률(CAGR) 16.46%로 증가하고 있습니다. 로봇 공학용 모듈이나 첨단 운전자 보조 시스템(ADAS) 보드에서는 이미 4GB를 넘는 메모리가 사용되고 있으며, 구동 전류 증가에도 불구하고 엔지니어들은 더 넓은 데이터 경로를 채택할 수밖에 없는 상황입니다. 컴파일러 지원이 성숙해짐에 따라, 64비트 명령어 세트로의 전환은 하이엔드 설계에 그치지 않고 주류 엣지 분석 분야로도 확대될 것입니다.

Wi-Fi는 2025년에도 출하 점유율 37.73%를 유지했습니다. 이는 대부분의 게이트웨이가 기존 액세스 포인트의 커버리지 범위 내에 있는 건물 내에 설치되어 있기 때문입니다. 스마트 홈 허브, 소매용 휴대용 단말기, 소형 산업용 단말기는 Wi-Fi 인프라의 여유 있는 대역폭과 높은 보급률의 혜택을 누리고 있습니다. 현재 이 모듈은 평균 소비 전류를 25μA 미만으로 억제하는 절전 모드를 지원하여 배터리 수명을 연장하는 동시에, 과거 블루투스로만 제한되었던 Wi-Fi 기능을 휴대용 단말기로까지 확대되고 있습니다.

계량기 제조업체, 물류 사업자, 농업 플랫폼이 자체 백홀을 보유하지 않고도 광범위한 커버리지를 확보하고자 함에 따라, 셀룰러 NB-IoT 및 LTE-M 모듈 시장은 연평균 성장률(CAGR) 16.86%로 성장하고 있습니다. eSIM과 세계 로밍 프로파일의 등장으로, 단일 부품 번호로 다양한 규제 지역에 대응할 수 있게 되어 재고 관리가 간소화되었습니다. 예측 기간 동안 IoT 마이크로컨트롤러 시장에서는 인증된 모뎀 펌웨어와 데이터 요금제 관리 기능을 사전 탑재한 공급업체들이 우위를 점하게 되어, 차량 운영업체의 도입 주기를 단축할 것으로 보입니다.

지역별 분석

2025년, 아시아태평양은 전 세계 매출의 38.14%를 차지했습니다. 이는 중국의 수탁 생산 역량, 일본의 정밀 로봇 기술 기반, 그리고 수입 의존도를 낮추기 위한 인도의 재정적 우대 조치에 힘입은 결과입니다. 중국의 국내 클라우드 제공업체들은 엣지 노드용으로 RISC-V 부품을 권장하는 경향이 강해지고 있으며, 이로 인해 현지 공급망이 강화되고 로열티 지불 위험이 감소하고 있습니다. 인도는 생산 장려 계획에 따라 15,554만 루피(약 16억 4,800만 달러)를 지출하고 있으며, 이를 통해 웨이퍼에서 완제품 모듈에 이르는 리드 타임을 단축하는 여러 범프 및 테스트 기업을 이미 유치했습니다.

북미는 자동차용 전자기기에 대한 견조한 수요와 산업용 자동화 인프라의 지속적인 업그레이드의 혜택을 누리고 있습니다. 'CHIPS and Science Act'는 IoT 마이크로컨트롤러 시장을 겨냥한 기존 생산 시설에 수십억 달러 규모의 보조금을 지원하고 있지만, 신규 팹이 안정적으로 가동되기까지는 2020년대 후반이 될 것으로 보입니다. 한편, OEM 업체들은 할당량 부족으로 인한 공급 충격에 대처하기 위해 다중 조달 전략이나 승인된 대체품에 의존하고 있습니다. 유럽에서는 에너지 가격 급등으로 인해 웨이퍼 제조에 드는 제반 비용이 증가하고 있지만, 안전성이 극히 중요한 컨트롤러 설계 분야에서 이 지역은 여전히 없어서는 안 될 존재입니다. 독일과 프랑스의 1차 공급업체들이 엄격한 ISO 26262 문서화를 추진하고 있으며, 이는 궁극적으로 전 세계적인 모범 사례가 될 것이기 때문에 유럽공급업체들은 출하 점유율 이상의 영향력을 행사하고 있습니다.

중동은 현재 규모는 작지만, 주요 스마트시티 계획에서 사막의 더위와 모래 유입을 견딜 수 있는 센서 네트워크가 요구됨에 따라 연평균 성장률(CAGR) 16.53%라는 다른 지역을 앞지르는 속도로 성장하고 있습니다. 남미와 아프리카는 여전히 새로운 기회가 되고 있습니다. 정밀 관개 및 태양광 마이크로그리드 모니터링 분야의 시범 사업에서는 인프라 격차를 해소하는 장거리 셀룰러 컨트롤러가 주목받고 있습니다. 데이터 통신 요금제와 위성 백홀 요금이 하락함에 따라, 해당 지역에서는 개념 검증(PoC) 단계에서 대규모 도입 단계로 전환될 것이며, 이는 가성비가 뛰어난 32비트 부품에 대한 롱테일 수요를 촉진할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the ioT microcontroller market size is expected to increase from USD 6.11 billion in 2025 to USD 7.14 billion in 2026 and reach USD 14.78 billion by 2031, growing at a CAGR of 15.66% over 2026-2031.

This report is Segmented by Bit Class (8-Bit, 16-Bit, and More), Connectivity Type (No Integrated Connectivity, Wi-Fi, Bluetooth/BLE, Zigbee/Thread, and More), Instruction Set Architecture (ARM, RISC-V, X86, and More), Application (Smart Home and Wearables, Industrial Automation and IIoT, Automotive and Transportation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global IoT Microcontroller Market Trends and Insights

Rapid Expansion of Connected Industrial Systems

Factory digitization budgets now prioritize distributed control and analytics as plant managers seek to cut unplanned downtime. Every robot cell, conveyor module, and smart tool embeds at least one controller that must combine sensor fusion with deterministic networking. Predictive-maintenance use cases demand on-chip analog front ends plus enough headroom to run vibration and thermal inference without cloud latency. Infineon's PSOC Edge E8x family, launched in 2025, exemplifies this trend by embedding an ARM Cortex-M33 core alongside an Ethos-U55 neural processing unit, enabling on-chip anomaly detection without cloud latency. New product families embed hardware root-of-trust components to meet IEC 62443 mandates, meaning security now rides alongside signal integrity in the bill of materials.

Growing Demand for Secure-by-Design MCUs in Edge AI Devices

Latency-intolerant systems, such as service robots and autonomous drones, are moving inference workloads from the cloud to the board. This change increases the requirements for hardware isolation, secure boot, and tamper detection to prevent the extraction of model weights. Certification frameworks like PSA Certified Level 2 map design choices to clearly defined threat models, but they also extend development schedules by several months. Brands accept the timeline penalty because the EU Cyber Resilience Act and similar U.S. directives impose strict liability for insecure connected products.

Software Ecosystem Fragmentation for New ISAs

RISC-V's open license lowers royalty outlays, but unrestricted custom extensions have created a patchwork of toolchains that lack binary compatibility. Developers often maintain separate code bases for each silicon variant, which inflates non-recurring engineering budgets. Consolidation efforts such as the RVA profiles are underway, yet adherence is optional, and uptake remains uneven. The resulting uncertainty deters automotive and medical designers who must guarantee 15-year software support.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Multi-Protocol Wireless MCUs for Smart-Home Ecosystems

- Government-Led Semiconductor Localization Incentives

- Persistent Semiconductor Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 32-bit class delivered 58.39% of revenue in 2025, underscoring its balance between compute ceiling and cost. High-volume controllers in this tier dominate smart gateways and factory drives because they run real-time operating systems alongside compact machine-learning libraries. The IoT microcontroller market continues to pivot toward variants with vector math units and on-chip security blocks, enabling deterministic control without compromising encryption throughput. Raspberry Pi's RP2350, launched in 2024, offers a dual-core configuration that can run either ARM Cortex-M33 or RISC-V Hazard3 instructions, providing developers with architectural flexibility and a migration path from 32-bit to 64-bit workloads.

Demand for 64-bit controllers is climbing at a 16.46% CAGR as high-definition imaging and multi-sensor fusion need wider address spaces. Robotics modules and advanced driver-assistance boards already exceed 4 GB of memory, compelling engineers to adopt wider data paths despite higher active current. As compiler support matures, the jump to 64-bit instruction sets will spread beyond premium designs into mainstream edge analytics.

Wi-Fi maintained a 37.73% shipment share in 2025 because most gateways are located inside buildings with existing access-point coverage. Smart-home hubs, retail handhelds, and small industrial terminals benefit from the bandwidth headroom and ubiquity of Wi-Fi infrastructure. Modules now support power-saving modes that lower average draw to below 25 µA, extending battery life and nudging Wi-Fi into portable devices once locked to Bluetooth.

Cellular NB-IoT and LTE-M modules are expanding at a 16.86% CAGR as meter companies, logistics providers, and agricultural platforms pursue wide-area reach without owning a private backhaul. The rise of eSIM and global roaming profiles means a single part number can address many regulatory domains, simplifying inventory. Over the forecast horizon, the IoT microcontroller market will reward suppliers that preload certified modem firmware and data-plan management hooks, shortening deployment cycles for fleet operators.

Geography Analysis

Asia-Pacific captured 38.14% of global revenue in 2025, anchored by China's contract-manufacturing depth, Japan's precision robotics base, and India's fiscal incentives that reduce import reliance. Domestic cloud providers in China increasingly recommend RISC-V parts for edge nodes, reinforcing local supply chains and lowering royalty exit risk. India's disbursement of INR 15,554 crore (approximately USD 1,648 million) under its production incentive plan has already attracted several bump-and-test houses that shorten the time from wafer to finished module.

North America benefits from strong automotive electronics demand and continuing upgrades to industrial automation infrastructure. The CHIPS and Science Act funnels multi-billion-dollar grants to mature nodes serving the IoT microcontroller market, but new fabs will not reach steady state until the back half of the decade. In the interim, original-equipment manufacturers rely on multi-sourcing strategies and approved alternates to manage allocation shocks. Europe faces higher energy prices that raise wafer fabrication overhead, yet the region remains essential for safety-critical controller design. German and French tier-ones drive stringent ISO 26262 documentation that eventually becomes global best practice, giving European suppliers influence that exceeds their shipment share.

The Middle East, though smaller today, is scaling faster than any peer region at 16.53% CAGR because flagship smart-city programs require sensor networks that survive desert heat and sand ingress. South America and Africa remain emerging opportunities. Pilot programs in precision irrigation and solar-microgrid monitoring highlight long-range cellular controllers that bridge infrastructure gaps. As data plans and satellite-backhaul tariffs decline, these regions will shift from proof of concept to scaled deployments, lifting long-tail unit volumes for value-optimized 32-bit parts.

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Infineon Technologies AG

- Silicon Laboratories Inc.

- Nordic Semiconductor ASA

- GigaDevice Semiconductor Inc.

- Espressif Systems (Shanghai) Co., Ltd.

- Holtek Semiconductor Inc.

- Analog Devices, Inc.

- Maxim Integrated Products, Inc.

- Toshiba Electronic Devices and Storage Corporation

- Nuvoton Technology Corporation

- Qualcomm Incorporated

- Intel Corporation

- Advanced Micro Devices, Inc.

- Samsung Electronics Co., Ltd.

- ROHM Co., Ltd.

- Espressif Systems (Shanghai) Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Connected Industrial Systems

- 4.2.2 Growing Demand for Secure-by-Design MCUs in Edge AI Devices

- 4.2.3 Proliferation of Multi-protocol Wireless MCUs for Smart Home Ecosystems

- 4.2.4 Government-Led Semiconductor Localization Incentives

- 4.2.5 Open-Source RISC-V Adoption Reducing Licensing Costs

- 4.2.6 Increasing Integration of AI Accelerators Inside 32-bit MCUs

- 4.3 Market Restraints

- 4.3.1 Software Ecosystem Fragmentation for New ISAs

- 4.3.2 Persistent Semiconductor Supply-Chain Volatility

- 4.3.3 Rising Cyber-Security Compliance Costs for IoT OEMs

- 4.3.4 Performance-Power Trade-offs Limiting Battery Life Gains

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Bit Class

- 5.1.1 8-bit

- 5.1.2 16-bit

- 5.1.3 32-bit

- 5.1.4 64-bit

- 5.2 By Connectivity Type

- 5.2.1 No Integrated Connectivity

- 5.2.2 Wi-Fi

- 5.2.3 Bluetooth / BLE

- 5.2.4 Zigbee / Thread

- 5.2.5 Cellular NB-IoT / LTE-M

- 5.2.6 Multi-protocol SoC

- 5.3 By Instruction Set Architecture

- 5.3.1 ARM

- 5.3.2 RISC-V

- 5.3.3 x86

- 5.3.4 Proprietary / Other Instruction Set Architectures

- 5.4 By Application

- 5.4.1 Smart Home and Wearables

- 5.4.2 Industrial Automation and IIoT

- 5.4.3 Automotive and Transportation

- 5.4.4 Healthcare and Medical Devices

- 5.4.5 Smart City Infrastructure

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 STMicroelectronics N.V.

- 6.4.2 NXP Semiconductors N.V.

- 6.4.3 Texas Instruments Incorporated

- 6.4.4 Microchip Technology Inc.

- 6.4.5 Renesas Electronics Corporation

- 6.4.6 Infineon Technologies AG

- 6.4.7 Silicon Laboratories Inc.

- 6.4.8 Nordic Semiconductor ASA

- 6.4.9 GigaDevice Semiconductor Inc.

- 6.4.10 Espressif Systems (Shanghai) Co., Ltd.

- 6.4.11 Holtek Semiconductor Inc.

- 6.4.12 Analog Devices, Inc.

- 6.4.13 Maxim Integrated Products, Inc.

- 6.4.14 Toshiba Electronic Devices and Storage Corporation

- 6.4.15 Nuvoton Technology Corporation

- 6.4.16 Qualcomm Incorporated

- 6.4.17 Intel Corporation

- 6.4.18 Advanced Micro Devices, Inc.

- 6.4.19 Samsung Electronics Co., Ltd.

- 6.4.20 ROHM Co., Ltd.

- 6.4.21 Espressif Systems (Shanghai) Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment