|

시장보고서

상품코드

2062091

캐슈넛 껍질액 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cashew Nut Shell Liquid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

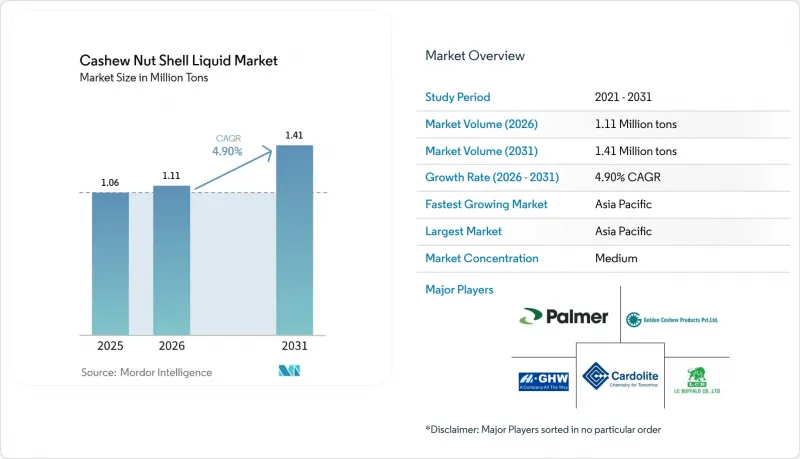

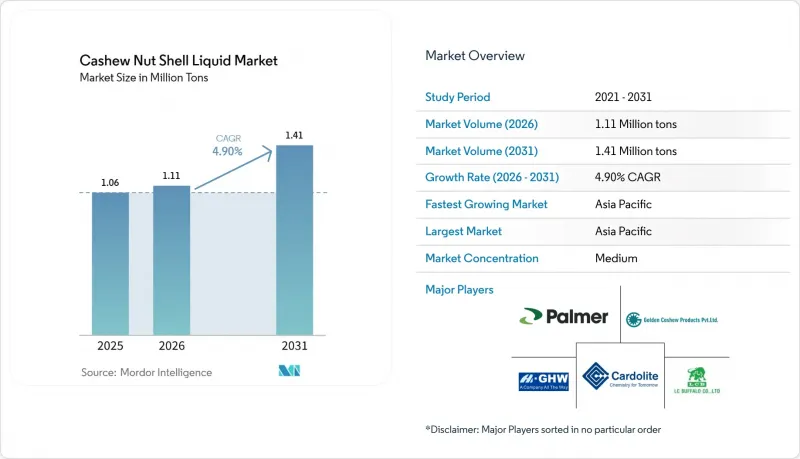

Mordor Intelligence에 의하면, 캐슈넛 껍질액(CNSL) 시장 규모는 2025년에 106만 톤으로 평가되어 2026년 111만 톤에서 2031년까지 141만 톤에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.90%를 나타낼 전망입니다.

본 보고서는 제품 유형(칼도르 및 기타), 등급(테크니컬 등급 및 기타), 추출 방법(기계적 압착 및 기타), 용도(마찰재 및 기타 용도), 최종 사용자 산업(석유 및 가스 및 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제공됩니다.

전 세계 캐슈넛 껍질액(CNSL) 시장 동향 및 인사이트

고성능 마찰 라이닝에 대한 OEM 수요 증가

자동차 및 상용차 제조업체들은 더욱 엄격해진 미세먼지 배출 규제 및 구리 함량 규제를 준수하기 위해, 브레이크 패드에 사용되던 기존의 페놀·포름알데히드계 수지를 카르다놀계 페놀 수지로 대체하고 있습니다. 이러한 전환은 유럽연합(EU) 규정 2019/631 및 중국의 국가 VI 기준에 따라 추진되고 있습니다. 또한, 전기자동차 플랫폼에서는 빈도는 낮지만 높은 에너지가 수반되는 제동 상황에 대응할 수 있는 마찰재가 요구되고 있습니다. 수요 증가에 힘입어, 파머 인터내셔널은 북미 트럭 OEM(순정 부품 제조업체)으로부터 바이오 라이닝에 대한 수주가 크게 증가했다는 보고를 받고, 2025년에 텍사스주의 생산 능력을 확대했습니다. 학술지 심사를 거친 연구에 따르면, 캐슈넛 껍질액(CNSL)과 페놀 수지를 결합한 복합재료는 내마모성을 향상시키고 소음·진동·거칠기(NVH)를 저감하는 효과가 있는 것으로 밝혀져, 이 재료의 사용 확대에 박차를 가하고 있습니다. 첸나이와 푸네에 거점을 둔 인도공급업체들은 국내 원자재와 국제표준화기구(ISO) 9001 인증을 활용하여 전 세계 계약을 이행하고 있으며, 이를 통해 아시아태평양 내 해당 시장에서의 입지를 더욱 공고히 하고 있습니다.

바이오·저VOC 산업용도료에 대한 규제 추진

국제해사기구(IMO)의 휘발성 유기화합물(VOC) 규제 상한치 및 각국의 친환경 인증 기준은 저온에서도 효율적으로 경화되고 재생 가능 탄소 함량이 높다는 특징을 바탕으로 페날카민 경화형 에폭시 수지를 권장하고 있습니다. 2025년 5월에 출시된 Cardolite사의 LITE 514HP는 ASTM B117 염수 분무 시험에서 3,000시간의 기준치를 상회하며, 해상 풍력 발전 타워나 선박 선체 등의 용도에 적합합니다. 유럽연합의 화학물질 등록, 평가, 허가 및 제한에 관한 규정(EU REACH)이나 미국 환경보호청(U.S. EPA)의 '세이퍼 초이스(Safer Choice)'와 같은 규제 프로그램으로 인해 노닐페놀 에톡실레이트의 사용이 억제되고 있어, 비용은 비싸지만 카르다놀계 희석제에 대한 수요가 증가하고 있습니다. 유럽의 바이어들은 추적성 문서가 첨부된 증류 캐슈넛 껍질액(CNSL)에 대해 일관되게 15-20%의 프리미엄을 지불하고 있으며, 이로 인해 고순도 공급품의 구조적 최저 가격이 형성되고 있습니다.

캐슈넛 수확량 변동과 생껍질 가격

예측 불가능한 몬순과 해충 발생으로 인해 원료 부족이 발생하고, 껍질 가격이 상승하면서 가공업체의 이익률이 하락하고 있습니다. 2026년 1분기(Q1), 인도에서는 서아프리카의 물류 문제로 인해 생견과류 수입이 현저히 감소했습니다. 이러한 상황으로 인해 소규모 채굴 업체들이 가동을 중단하면서, 정제 등급의 가격은 톤당 975-1,025달러까지 상승했습니다. 서아프리카 국가들은 여전히 껍질의 대부분을 에너지원으로 활용하고 있어, 추출을 통해 얻을 수 있는 잠재적 수익을 놓치고 있을 뿐만 아니라 세계 공급 변동의 한 원인이 되고 있습니다. 농장과 연계된 통합형 기업들은 장기 계약을 확보하고 있지만, 단기 구매자들은 작황이 부진한 시기에 이익률 압박에 직면하고 있습니다.

부문별 분석

산업용 캐슈넛 껍질액(CNSL)은 마찰재 및 범용 산업용도료 분야에서 뛰어난 비용 효율성을 바탕으로, 2025년에는 전체 시장의 46.5%를 차지할 것으로 예측됩니다. 카르다놀은 가드너 색도 1 이하, 칼륨 함량 10ppm 미만, 안정적인 아민가 등의 사양을 요구하는 에폭시 및 페놀아민계 배합 제조업체들 수요에 힘입어 연평균 성장률(CAGR) 5.12%로 성장할 것으로 전망됩니다.

증류 공정을 통해 카르다놀은 순도 78%까지 농축되며, 이를 통해 배합 제조업체는 전기차 브레이크 시스템 및 영하에서 경화되는 선박용 도료에 관한 OEM(Original Equipment Manufacturer) 요건을 충족할 수 있게 됩니다. 원료 쉘 가격 변동에 따른 이익률 압박으로 인해, 인도와 베트남의 가공업체들은 와이프 필름법이나 이온 교환법을 이용한 정제 라인을 확장하여 특수 유도체에서 더 높은 부가가치를 창출하도록 유도되고 있습니다. 또한, 페날카민 수지는 여전히 수익성이 높은 하위 부문으로, 해양용 코팅 분야에서는 톤당 최대 3,500달러에 달하는 가격을 형성하고 있습니다.

증류·정제 등급은 고급 복합재료 시장에서 일관된 화학적 특성과 미량 금속 함유량에 대한 하류 수요에 힘입어, 2031년까지 연평균 성장률(CAGR) 5.23%로 성장할 것으로 전망됩니다. 2025년, 테크니컬 등급은 캐슈넛 껍질액(CNSL) 시장 규모의 42.1%를 차지했으나, 전 세계 OEM(주문자 상표 제조업체)들이 공급업체의 품질 감사를 표준화해 나감에 따라 그 시장 점유율은 감소할 것으로 예측됩니다.

유럽의 수입업체들은 REACH(화학물질 등록·평가·허가·제한) 규정을 준수하는 정제 원료에 대해 최대 20% 더 높은 가격을 지불하고 있으며, 이러한 가격 차이는 아시아태평양의 생산 시설에서 기술 업그레이드를 촉진하고 있습니다. 산 등급의 생산량은 틈새 시장인 목재용 접착제 용도로 계속 공급되고 있지만, 많은 합판 제조업체들은 기존의 페놀·포름알데히드계 바인더에 비해 성능이 향상된 저포름알데히드 카르다놀계 제품으로의 전환을 추진하고 있습니다.

지역별 분석

2025년, 아시아태평양은 캐슈넛 껍질액(CNSL) 시장의 39.1%를 차지하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 5.25%로 성장할 것으로 전망됩니다. 인도는 캐슈 농장과 인접한 지리적 이점을 살려 전 세계 CNSL 공급량의 약 45%를 가공하고 있습니다. 베트남은 유럽 및 북미 시장에서 고가에 거래되는 정제 CNSL 등급의 수출에 주력하고 있습니다. 한편, 중국의 수지 제조업체들은 공급망의 현지화와 수입 의존도 감소를 목표로, 카르다놀·에폭시계 수지에 대한 조사를 진행하고 있습니다. 이는 2025년에 그래핀 강화 카르다놀 매트릭스에 관한 여러 편의 동료 평가 논문이 발표된 사실로도 입증됩니다.

북미는 CNSL 원료의 대부분을 아시아에서 조달하고 있지만, 마찰 바인더나 페날카민계 코팅제 등 고성능 용도에 대한 수요는 여전히 견조합니다. 2025년 파머 인터내셔널의 생산 능력 확대는 특히 바이오 소재가 필요한 전기차 플랫폼의 다운스트림 공정에서 견조한 수주 실적을 반영한 것입니다. 또한, 캐나다 풍력 발전 부문에서는 블레이드 보수용 수지로 카르다놀 에폭시가 채택되어 시장의 잠재적 규모를 더욱 확대되고 있습니다.

유럽은 정제 및 증류 CNSL 등급 제품의 최대 수입 지역으로 자리매김하고 있으며, 화학물질의 등록, 평가, 허가 및 제한(REACH)이나 친환경 라벨 인증 요건을 충족하기 위해 종종 추적성 프리미엄을 지불합니다. 북유럽 국가들은 해상 풍력 발전 프로젝트를 위해 재활용이 가능한 에폭시 시스템을 우선적으로 채택하고 있으며, 이에 대한 연구 개발 노력을 추진하고 있습니다. 이러한 노력은 CNSL 화학의 발전과 부합하는 순환형 경제 지원금을 통해 지원받고 있습니다.

남미는 캐슈넛 원료가 풍부함에도 불구하고, CNSL의 추출량은 제한적입니다. 브라질의 연구진들은 CNSL의 새로운 용도를 개척하고 있지만, 해당 지역의 산업화는 자금 부족으로 인해 차질을 빚고 있습니다. 중동 및 아프리카의 CNSL 수요는 미미한 수준입니다. 그러나 서아프리카의 캐슈넛 원료 과잉 생산은 현지에서 가공할 기회를 제공하고 있으며, 이를 통해 해당 지역은 밸류체인 내에서 더 많은 부가가치를 창출할 수 있을 것으로 보입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the cashew nut shell liquid market size was valued at 1.06 million tons in 2025 and is estimated to grow from 1.11 million tons in 2026 to reach 1.41 million tons by 2031, at a CAGR of 4.90% during the forecast period (2026-2031).

This report is Segmented by Product Type (Cardol and Others), Grade (Technical Grade and Others), Extraction Method (Mechanical Press and Others), Application (Friction Materials and Other Applications), End-User Industry(Oil and Gas and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Global Cashew Nut Shell Liquid Market Trends and Insights

Growing OEM Demand for High-Performance Friction Linings

Automotive and commercial vehicle manufacturers are replacing conventional phenol-formaldehyde with cardanol-based phenolic resins in brake pads to comply with stricter particulate emission and copper content regulations. This shift is driven by European Union (EU) Regulation 2019/631 and China's National VI standards. Additionally, electric vehicle platforms require friction materials capable of handling infrequent but high-energy braking events. In response to rising demand, Palmer International expanded its Texas production capacity in 2025, following reports of significant growth in orders for bio-based linings from North American truck original equipment manufacturers (OEMs). Peer-reviewed studies indicate that cashew nutshell liquid (CNSL)-phenolic composites offer improved wear resistance and reduced noise, vibration, and harshness, supporting their increased usage. Indian suppliers based in Chennai and Pune are utilizing domestic feedstock and International Organization for Standardization (ISO) 9001 certification to fulfill global contracts, further strengthening the Asia-Pacific region's position in this market.

Regulatory Push for Bio-Based, Low-VOC Industrial Coatings

The International Maritime Organization's Volatile Organic Compound (VOC) caps and national ecolabels support phenalkamine-cured epoxies due to their ability to cure efficiently at low temperatures and their high renewable-carbon content. Cardolite's LITE 514HP, introduced in May 2025, exceeds ASTM B117 salt-spray thresholds of 3,000 hours, making it suitable for applications such as offshore wind towers and marine hulls. Regulatory programs like the European Union Registration, Evaluation, Authorization, and Restriction of Chemicals (EU REACH) and the United States Environmental Protection Agency (U.S. EPA) Safer Choice discourage the use of nonylphenol ethoxylates, increasing demand for cardanol-based diluents despite their higher cost. European buyers consistently pay a 15-20% premium for distilled Cashew Nut Shell Liquid (CNSL) accompanied by traceability documentation, establishing a structural price floor for high-purity supply.

Volatile Cashew Crop Yields and Raw-Shell Pricing

Unpredictable monsoons and pest outbreaks have resulted in feedstock shortages, increasing shell prices, and reducing processor margins. In the first quarter (Q1) of 2026, India experienced a notable decline in raw-nut imports due to logistical challenges in West Africa. This situation led to smaller extractors halting operations and raised refined-grade prices to USD 975-1,025 per ton. West African countries continue to utilize most shells for energy, foregoing potential extraction revenue and contributing to global supply fluctuations. Integrated players with plantation connections secure long-term contracts, while spot buyers face margin pressures during periods of crop shortages.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Wind-Energy Blade Manufacturing Composites

- Shift to Phenalkamine Curing Agents in Marine Epoxy Systems

- Availability of Low-Cost Synthetic Alkyl-Phenols

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Technical Cashew Nut Shell Liquid (CNSL) is expected to account for 46.5% of the volume in 2025, reflecting its cost efficiency in friction materials and generic industrial coatings. Cardanol is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.12%, driven by demand from epoxy and phenalkamine formulators requiring specifications such as Gardner color less than or equal to 1, potassium content below 10 parts per million (ppm), and a consistent amine value.

Distillation processes concentrate cardanol to 78% purity, enabling formulators to meet Original Equipment Manufacturer (OEM) requirements for electric vehicle brake systems and marine coatings that cure at sub-zero temperatures. Margin pressures caused by raw-shell price volatility are encouraging Indian and Vietnamese processors to expand wiped-film and ion-exchange purification lines to capture higher value from specialty derivatives. Additionally, phenalkamine resins remain a profitable sub-segment, with prices reaching up to USD 3,500 per ton for offshore coating applications.

Distilled and refined grades are projected to grow at a Compound Annual Growth Rate (CAGR) of 5.23% through 2031, driven by downstream demand for consistent chemical profiles and low trace metal content in high-end composites. In 2025, technical grade accounted for 42.1% of the Cashew Nut Shell Liquid market size; however, its market share is expected to decline as global Original Equipment Manufacturers (OEMs) standardize supplier quality audits.

European importers pay up to 20% more for Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH)-compliant refined materials, creating a price differential that supports technology upgrades in Asia-Pacific production facilities. Acid-grade output continues to cater to niche wood-adhesive applications, although many plywood manufacturers are transitioning to low-formaldehyde cardanol options, which offer improved performance compared to traditional phenol-formaldehyde binders.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 39.1% of the Cashew Nut Shell Liquid (CNSL) market and is projected to grow at a compound annual growth rate (CAGR) of 5.25% from 2026 to 2031. India processes approximately 45% of the global CNSL supply, benefiting from its proximity to cashew farms. Vietnam focuses on exporting refined CNSL grades, which are priced higher in European and North American markets. Meanwhile, China's resin producers are advancing research on cardanol-epoxy systems to localize supply chains and reduce import dependency. This is supported by multiple peer-reviewed studies in 2025 on graphene-reinforced cardanol matrices.

North America sources the majority of its CNSL feedstock from Asia but maintains strong demand for high-performance applications, such as friction binders and phenalkamine coatings. Palmer International's capacity expansion in 2025 reflects robust downstream orders, particularly from electric vehicle platforms that require bio-based materials. Additionally, Canada's wind energy sector is incorporating cardanol epoxies in blade repair resins, further expanding the market's addressable volume.

Europe remains the largest importer of refined and distilled CNSL grades, often paying traceability premiums to meet the requirements of Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) and Ecolabel certifications. Nordic countries are prioritizing recyclable epoxy systems for offshore wind projects, driving research and development efforts. These initiatives are supported by circular-economy grants that align with CNSL chemistry advancements.

South America, despite its abundance of raw cashew nuts, extracts limited volumes of CNSL. Brazilian researchers are pioneering new applications for CNSL, but industrialization in the region is hindered by capital shortages. The Middle East and Africa exhibit modest CNSL offtake. However, West Africa's surplus of raw cashew nuts presents an opportunity for localized extraction, which could enable the region to capture more value within the supply chain.

- Adarsh Industrial Chemicals

- Blueline Foods (India) Pvt Ltd

- C. Ramakrishna Padayatchi

- Cardolite Corporation

- Cashew Chem India

- Cat Loi Cashew Oil Production & Export JSC

- Elementis Plc

- GHW (VIETNAM) CO., LTD

- Golden Cashew Products Pvt. Ltd.

- K2P Chemicals

- Kumaraswamy Industries

- LC BUFFALO CO., LTD

- Muskaan Group

- Olam International

- Palmer International, Inc.

- Senesel

- Shivam Cashew Industry

- Shree Ganesh Agro

- SI Group

- Sri Devi Group

- Vavimex Co., Ltd

- Zhejiang Wansheng Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing OEM demand for high-performance friction linings

- 4.2.2 Regulatory push for bio-based, low-VOC industrial coatings

- 4.2.3 Expansion of wind-energy blade manufacturing composites

- 4.2.4 Shift to phenalkamine curing agents in marine epoxy systems

- 4.2.5 Rapid adoption of CNSL-based bio-pesticides in agro-chemicals*

- 4.3 Market Restraints

- 4.3.1 Volatile cashew crop yields and raw-shell pricing

- 4.3.2 Availability of low-cost synthetic alkyl-phenols

- 4.3.3 Scale-up challenges for super-critical CO2 extraction

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Technical CNSL (TCNSL)

- 5.1.2 Cardanol

- 5.1.3 Cardol

- 5.1.4 Phenalkamine Resins

- 5.1.5 Anacardic Acid and Other Derivatives

- 5.2 By Grade

- 5.2.1 Technical Grade

- 5.2.2 Acid Grade

- 5.2.3 Distilled / Refined Grade

- 5.3 By Extraction Method

- 5.3.1 Mechanical Press

- 5.3.2 Solvent Extraction

- 5.3.3 Distillation and Vacuum Distillation

- 5.3.4 Super-critical CO2 Extraction

- 5.3.5 Thermal Cracking

- 5.4 By Application

- 5.4.1 Friction Materials

- 5.4.2 Paints and Coatings

- 5.4.3 Adhesives and Laminates

- 5.4.4 Surfactants and Plasticizers

- 5.4.5 Polymer and Composites

- 5.4.6 Chemical Intermediates

- 5.4.7 Other Niche Uses (Bio-lubricants, Carbon Materials)

- 5.5 By End-User Industry

- 5.5.1 Automotive and Transportation

- 5.5.2 Building and Construction

- 5.5.3 Industrial Chemicals

- 5.5.4 Personal Care and Cosmetics

- 5.5.5 Oil and Gas

- 5.5.6 Agriculture

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 Japan

- 5.6.1.3 India

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 NORDIC Countries

- 5.6.3.8 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Adarsh Industrial Chemicals

- 6.4.2 Blueline Foods (India) Pvt Ltd

- 6.4.3 C. Ramakrishna Padayatchi

- 6.4.4 Cardolite Corporation

- 6.4.5 Cashew Chem India

- 6.4.6 Cat Loi Cashew Oil Production & Export JSC

- 6.4.7 Elementis Plc

- 6.4.8 GHW (VIETNAM) CO., LTD

- 6.4.9 Golden Cashew Products Pvt. Ltd.

- 6.4.10 K2P Chemicals

- 6.4.11 Kumaraswamy Industries

- 6.4.12 LC BUFFALO CO., LTD

- 6.4.13 Muskaan Group

- 6.4.14 Olam International

- 6.4.15 Palmer International, Inc.

- 6.4.16 Senesel

- 6.4.17 Shivam Cashew Industry

- 6.4.18 Shree Ganesh Agro

- 6.4.19 SI Group

- 6.4.20 Sri Devi Group

- 6.4.21 Vavimex Co., Ltd

- 6.4.22 Zhejiang Wansheng Co., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Increasing Demand for Sustainable, Bio-based Solutions