|

시장보고서

상품코드

2062093

무방향성 전기강판 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Non Grain Electric Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

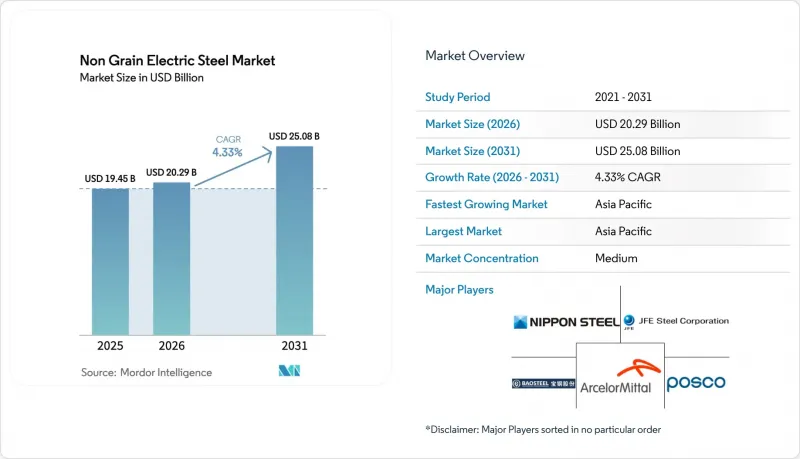

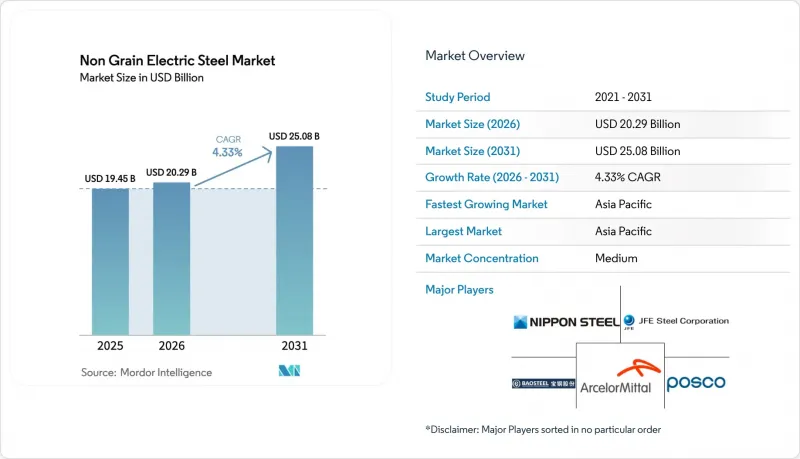

Mordor Intelligence에 의하면, 무방향성 전기강판 시장 규모는 2025년 194억 5,000만 달러로 평가되었습니다. 2026년 202억 9,000만 달러에서 2031년까지 250억 8,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR은 4.33%를 나타낼 것으로 예측됩니다.

본 보고서는 유형별(완제품 및 반제품), 용도별(모터, 변압기, 인덕터 및 리액터, 기타), 최종 사용자 산업별(에너지 및 유틸리티, 자동차·e-모빌리티, 산업 제조, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 무방향성 전기강판 시장 동향 및 분석

전기차 생산 확대

2025년 상반기, BYD의 배터리 전기자동차(BEV)와 플러그인 하이브리드 전기자동차(PHEV) 판매 대수는 214만 6,000대를 넘어섰으며, 이는 구동용 모터에 대한 수요가 얼마나 급속히 확대되고 있는지를 보여줍니다. 인도에서는 2024년에 208만 대의 전기차가 판매되었으며, 2030년까지 30%의 보급률을 목표로 하고 있어 다수의 충전소, 변전소, 배전용 변압기가 필요하지만, 이 모든 시설에 NGOES(비곡물계 전기강판) 코어가 사용되고 있습니다. 2025년 4월 중국이 시행한 희토류 광물 수출 규제로 인해 네오디뮴공급이 제한되면서, 자동차 제조업체들은 영구 자석 대신 추가적인 전기강판 적층을 활용한 전기 자석식 동기 모터로 전환해야 하는 상황에 직면해 있습니다. 포스코가 2030년까지 연간 750만 개의 모터 코어 생산을 목표로 하고 있다는 사실은 각 OEM 업체들이 코일 공급을 확보하기 위해 수직 통합을 추진하고 있음을 보여줍니다. 800V 고속 구동 모터는 1,000Hz 이상에서 작동하지만, 이 주파수 대역에서는 코어 손실이 주파수의 제곱에 비례하여 증가하기 때문에 두께 0.20-0.27mm의 강판은 단순한 선택 사항이 아니라 필수 사항이 됩니다.

재생에너지와 풍력 터빈의 확대

2024년 전 세계 풍력 발전 설비의 신규 설치량은 114.3기가와트에 달했습니다. 이는 전체의 69.4%를 차지하는 중국 단독의 79.4기가와트 규모 건설에 힘입은 결과입니다. 2024년에는 해상 풍력 터빈의 정격 출력이 평균 10메가와트에 근접했고, 16-26메가와트급 플랫폼이 상업 입찰에 참여했으며, 이들 플랫폼은 각각 수 톤 규모의 발전기 코어와 변압기 뱅크를 사용했습니다. 전기강판 공급 부족으로 인해 변압기 가격은 2018년 대비 75% 상승했습니다. 이는 제철소의 생산 능력이 현재 전 세계적으로 1,650기가와트를 넘는 재생에너지의 계통 연계 대기 수요를 따라잡지 못하고 있기 때문입니다. 희토류 자석을 사용하지 않는 전기 자석식 발전기는 터빈 1기당 NGOES(비정질 강판) 사용량을 최대 20% 증가시켜, 소형 변압기에서 비정질 코어의 점유율 하락을 완화하고 있습니다. EU와 아시아·태평양 지역의 정책 지원에 힘입어, 필연적으로 고품질의 NGOES 등급이 필요한 해상 풍력 발전 클러스터로 자본이 계속해서 유입되고 있습니다.

비정질과 나노결정 합금 간의 경쟁

히타치 금속은 2026년 6월, 사우스캐롤라이나주 콘웨이에서 2605HB1M 비정질 리본의 상업 생산을 시작하여, 무부하 시 변압기 손실을 방향성 강판의 불과 3분의 1 수준으로 줄였습니다. HB1M-LL 등급은 1.42 테슬라, 60Hz 조건에서 손실을 0.19 W/kg까지 줄여, 기존 비정질 제품에 비해 20-40%의 성능 향상을 실현했습니다. 히타치는 2024년 8억 6,500만 달러 규모의 비정질 코어 시장에서 이미 57%의 점유율을 차지했으며, 2032년까지 연평균 성장률(CAGR) 6.9%를 목표로 하고 있습니다. 리본 소재는 취성과 낮은 포화 자속 한계로 인해 5MVA 이하의 권선 코어로만 사용되지만, 더욱 엄격한 미국 에너지부(DOE)의 효율 기준을 추구하는 전력 회사들은 이에 맞추어 배전용 변압기의 사양을 변경하고 있습니다. NGOES 제조업체 입장에서는 회전 기계 수요가 견조한 추세를 보이고 있지만, 이로 인해 소출력 유닛 시장 점유율이 잠식되고 있습니다.

부문별 분석

2025년, 완전 가공 등급은 비결정질 전기강판 시장 점유율의 56.11%를 차지했으며, 각 OEM 업체들이 추가 어닐링 공정이 필요 없이 펀칭 가공이 가능한 상태로 납품되는 코일을 선호함에 따라, 2031년까지 연평균 성장률(CAGR) 5.36%를 나타낼 것으로 전망됩니다. BYD의 자체 라미네이트 프레스 가공 및 POSCO Mobility Solution의 750만 코어 목표 등, 자동차 제조업체의 수직 통합 추세를 반영하여 완전 가공품인 비결정질 전기강판 시장 규모는 확대되고 있습니다.

자동차용 트랙션 모터, IE4/IE5 산업용 드라이브, 자동차 충전기 분야에서는 인증된 코어 손실을 갖춘 최대 0.10mm 두께의 초박판에 대한 수요가 증가하고 있습니다. 총 2,130억 엔 규모의 투자를 통해 신일철주금의 히로하타 및 세토우치 노선이 가동을 시작했으며, 2027년까지 한신 및 야하타 노선이 추가될 예정인 가운데, 경쟁 우위를 유지하기 위해 필요한 설비 투자 경쟁이 펼쳐지고 있습니다. 반가공 등급은 설치 현장에서 응력 제거 처리가 이루어지는 대형 동기 발전기에서 여전히 일반적으로 사용되고 있습니다.

지역별 분석

아시아태평양은 2025년에 매출의 47.11%를 차지하며 비결정질 전기강판 시장을 주도했으며, 2031년까지 연평균 성장률(CAGR) 5.49%를 나타낼 것으로 전망됩니다. 2024년 중국에서 79.4GW 규모의 신규 풍력 발전 설비와 인도의 확대되는 전기차(EV) 생태계가 이 지역 수요를 뒷받침하고 있습니다. 히로하타, 세토우치, 포스코의 포항 모빌리티 라인에서 생산 능력을 확충함에 따라, 도요타, 현대, BYD의 각 프로그램에 대한 현지 공급이 확보되었습니다.

북미에서는 섹션 48C 세액 공제 및 ‘바이 아메리카’ 조항에 따라 수요가 클리블랜드 클리프스, 뉴코어, 아르셀로미탈의 제철소로 이동하고 있는 반면, 히타치 금속의 콘웨이 리본 공장은 해당 지역을 비정질 코어 거점으로 삼고 있습니다.

유럽 수요는 에코디자인 IE4 규제와 REPowerEU 조달 규정에 의해 주도되고 있습니다. 티센크루프의 ‘블루민트’와 포에스트알피네의 ‘그린테크’ 강재는 해당 지역의 저탄소 야금 노력을 강화하고 있는 반면, 헨트와 링우드는 폭스바겐과 스텔란티스의 구동계 프로그램에 부품을 공급하고 있습니다.

남미, 중동 및 아프리카에서는 국내 압연 라인 부족, 환율 변동, 수입 의존도가 걸림돌이 되고 있습니다. 그럼에도 불구하고, 브라질 산업의 전기화와 사우디아라비아의 NEOM 메가 프로젝트는 ESG 인증을 취득할 수 있는 수출업체들에게 제한적인 기회를 제공합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the non grain electric steel market size is projected to expand from USD 19.45 billion in 2025 and USD 20.29 billion in 2026 to USD 25.08 billion by 2031, registering a CAGR of 4.33% between 2026 to 2031.

This report is Segmented by Type (Fully-Processed and Semi-Processed), Application (Motors, Transformers, Inductors and Reactors, and More), End-User Industry (Energy and Utilities, Automotive and E-Mobility, Industrial Manufacturing, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Non Grain Electric Steel Market Trends and Insights

Electric Vehicle Production Expansion

Battery-electric and plug-in hybrid sales surpassed 2.146 million units at BYD in the first half of 2025, illustrating how rapidly traction-motor demand is compounding. India's 2.08 million EV sales in 2024 and a 30% penetration goal by 2030 will require large numbers of charging stations, substations, and distribution transformers, all of which use NGOES cores. China's April 2025 export controls on rare-earth minerals restrict neodymium supplies and push automakers toward electrically excited synchronous motors that replace permanent magnets with extra electrical-steel laminations. POSCO's target of 7.5 million motor cores a year by 2030 showcases vertical integration as OEMs safeguard coil supply. High-speed 800-volt traction motors operate above 1,000 hertz, where core loss scales with frequency squared, making 0.20-0.27 millimeter gauges a necessity rather than an option.

Renewable and Wind-Turbine Build-Out

Global wind additions reached 114.3 gigawatts in 2024, driven by China's 79.4 gigawatt build that alone accounted for 69.4% of the total. Offshore turbine ratings climbed toward 10 megawatts on average in 2024, with 16-26 megawatt platforms entering commercial tenders, each using multi-ton generator cores and transformer banks. Electrical-steel shortages lifted transformer prices 75% over 2018 levels as mill capacity lags renewable interconnection queues that now top 1,650 gigawatts worldwide. Electrically excited generators that sidestep rare-earth magnets boost NGOES content per turbine by up to 20%, cushioning the loss of share to amorphous cores in small transformers. Policy support in the EU and APAC continues to funnel capital toward offshore wind clusters that are, by necessity, hungry for premium NGOES grades.

Competition from Amorphous and Nano-Crystalline Alloys

Hitachi Metals started commercial output of 2605HB1M amorphous ribbons at Conway, South Carolina in June 2026, delivering no-load transformer losses barely one-third of grain-oriented silicon steel. The HB1M-LL grade pushes loss down to 0.19 W/kg at 1.42 Tesla and 60 Hz, a 20-40% improvement on earlier amorphous products. Hitachi already controlled 57% of the amorphous-core segment worth USD 865 million in 2024 and aims for 6.9% CAGR through 2032. Although brittleness and low saturation flux limit ribbons to wound cores under 5 MVA, utilities chasing tighter DOE efficiency standards are shifting distribution-transformer specifications accordingly. For NGOES producers this erodes share in small-power units even as rotating-machine demand stays intact.

Other drivers and restraints analyzed in the detailed report include:

- Thin-Gauge NGOES for High-Speed Motors

- Domestic-Content Rules for Transformer Cores

- ESG-Driven Shift to "Green" Steel Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fully processed grades held 56.11% of non grain electric steel market share in 2025 and are projected to grow at 5.36% CAGR to 2031 as OEMs favor coils that arrive ready for punching without extra annealing. The non-grain electric steel market size for fully processed, reflecting automaker vertical-integration moves such as BYD's in-house lamination stamping and POSCO Mobility Solution's 7.5 million-core goal.

Automotive traction motors, IE4/IE5 industrial drives, and on-board chargers increasingly demand ultra-thin gauges down to 0.10 mm with certified core loss. Investments totaling JPY 213 billion brought Nippon Steel's Hirohata and Setouchi lines online and will add Hanshin and Yawata by 2027, showing the capex race needed to stay relevant. Semi-processed grades remain common in large synchronous generators that undergo site-specific stress relief.

Geography Analysis

Asia-Pacific dominated the non grain electric steel market with 47.11% revenue in 2025 and will log a 5.49% CAGR to 2031. China's 79.4 GW of new wind in 2024 and India's expanding EV ecosystem underpin the region's appetite. Capacity additions at Hirohata, Setouchi, and POSCO's Pohang mobility line ensure local supply for Toyota, Hyundai, and BYD programs.

In North America, Section 48C credits and Buy America clauses redirect demand to Cleveland-Cliffs, Nucor, and ArcelorMittal mills, while Hitachi Metals' Conway ribbon plant positions the region as an amorphous-core hub.

Europe's demand is by Ecodesign IE4 mandates and REPowerEU sourcing rules. Thyssenkrupp's Bluemint and Voestalpine's Greentec steel reinforce the bloc's push toward low-carbon metallurgy, while Gent and Ringwood supply Volkswagen and Stellantis traction programs.

South America, and Middle-East and Africa are hampered by scarce domestic rolling lines, currency swings, and import dependence. Nevertheless, Brazil's industrial electrification and Saudi Arabia's NEOM megaproject offer selective upside for exporters able to certify ESG credentials.

- Ansteel Group Corporation Limited

- ArcelorMittal

- Baoshan Iron & Steel Co. Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- JFE Steel Corporation

- JSW

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- NLMK

- POSCO

- Shandong Iron and Steel Group Co., Ltd.

- Shougang Group

- Tata Steel

- thyssenkrupp AG

- United States Steel Corporation

- voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electric Vehicle production expansion

- 4.2.2 Renewable and wind-turbine build-out

- 4.2.3 Thin-gauge NGOES for high-speed motors

- 4.2.4 Domestic-content rules for transformer cores

- 4.2.5 Digital-twin-driven grade upgrades

- 4.3 Market Restraints

- 4.3.1 Competition from amorphous and nano-crystalline alloys

- 4.3.2 ESG-driven shift to "green" steel alternatives

- 4.3.3 Hydrogen-embrittlement risk in next-gen drives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Fully-processed

- 5.1.2 Semi-processed

- 5.2 By Application

- 5.2.1 Motors

- 5.2.1.1 Traction (EV/rail)

- 5.2.1.2 Industrial (IE4/IE5, HVAC)

- 5.2.2 Transformers

- 5.2.2.1 Power

- 5.2.2.2 Distribution and EV on-board

- 5.2.3 Generators

- 5.2.4 Inductors and Reactors

- 5.2.5 Sensors and Miscellaneous

- 5.2.1 Motors

- 5.3 By End-user Industry

- 5.3.1 Energy and Utilities

- 5.3.2 Automotive and E-mobility

- 5.3.3 Industrial Manufacturing

- 5.3.4 Consumer Appliances

- 5.3.5 Aerospace and eVTOL

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Ansteel Group Corporation Limited

- 6.4.2 ArcelorMittal

- 6.4.3 Baoshan Iron & Steel Co. Ltd.

- 6.4.4 Cleveland-Cliffs Inc.

- 6.4.5 Gerdau S/A

- 6.4.6 JFE Steel Corporation

- 6.4.7 JSW

- 6.4.8 LIBERTY Steel Group

- 6.4.9 NIPPON STEEL CORPORATION

- 6.4.10 NLMK

- 6.4.11 POSCO

- 6.4.12 Shandong Iron and Steel Group Co., Ltd.

- 6.4.13 Shougang Group

- 6.4.14 Tata Steel

- 6.4.15 thyssenkrupp AG

- 6.4.16 United States Steel Corporation

- 6.4.17 voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment