|

시장보고서

상품코드

2062095

열압성형 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Thermo Compression Forming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

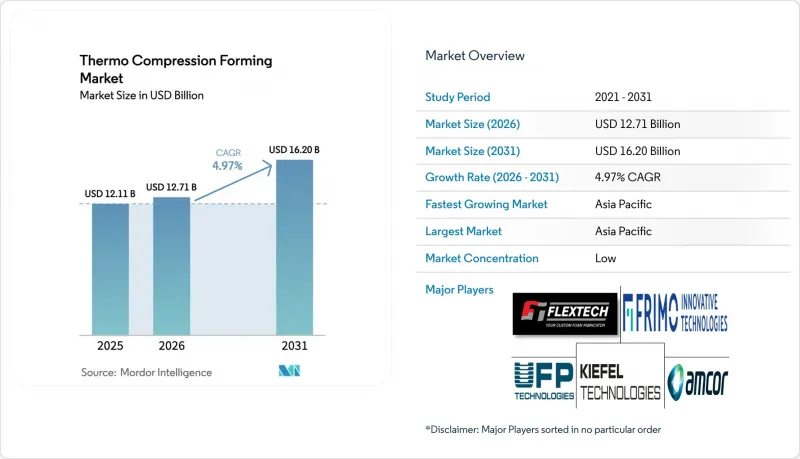

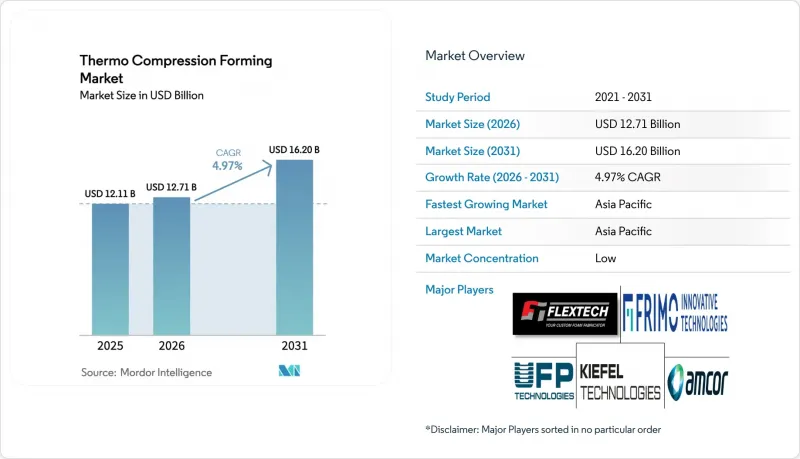

Mordor Intelligence에 의하면, 열압성형 시장 규모는 2025년 121억 1,000만 달러로 평가되었습니다. 2026년 127억 1,000만 달러에서 2031년까지 162억 달러로 확대되어 2026-2031년에 걸쳐 CAGR은 4.97%를 나타낼 것으로 예측됩니다.

본 보고서는 재료 유형(열가소성 수지, 열경화성 수지, 복합재료, 기타 재료 유형), 용도(포장, 자동차 부품, 항공우주 및 방위, 전자기기 및 반도체, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 열압성형 시장 동향 및 인사이트

가볍고 내구성이 뛰어난 포장 솔루션에 대한 수요

현재 소비재 및 제약 브랜드들은 사출 성형 용기와 동등한 차단 성능과 낙하 시험 성능을 갖추면서도 재료 중량을 20-30% 줄인 열성형 트레이를 지정하고 있습니다. 유럽의 포장 및 포장 폐기물 규정에 따르면, 2030년까지 재활용성 또는 퇴비화 가능성을 확보해야 할 의무가 부과되어 있으며, 이에 따라 각 변환 업체들은 천공 손상을 일으키지 않으면서 두께 0.5mm 이하의 성형을 수행해야 하는 상황에 놓여 있습니다. 네팹(Nefab)이 2025년에 테네시주에 개설할 허브에서는 스크랩을 재분쇄 및 재압출 성형하여 새로운 롤 소재로 재생하고, 각 OEM 업체가 ESG 감사에 활용할 수 있는 재활용 소재 함유율 지표를 기록할 수 있도록 할 예정입니다. 또한, 각 푸드서비스 체인 업체들은 산업용 퇴비화기 내에서 90일 만에 분해되는 EN 13432 인증 PLA 재질의 클램쉘 용기로의 전환을 추진하고 있으며, 이는 캘리포니아주와 퀘벡주에서 매립 처리 비용 절감으로 이어지고 있습니다.

전자기기 조립 및 반도체 패키징 분야에서의 활용 확대

이종 통합은 200-400℃에서 형성되며, ±1-2 마이크로미터의 정렬 정밀도를 갖는 구리-구리 하이브리드 접합에 의존합니다. SK하이닉스는 2027년까지 12층 HBM3 스택을 공급할 첨단 패키징 공장 ‘P&T7’에 19조 원(130억 달러)을 투자하기로 결정했습니다. ASE Technology는 2026년에 70억 달러를 투자해 CoWoS급 생산 능력을 월 2만 5,000장으로 3배 확대하는 한편, 120kW AI 랙용 마이크로플루이딕스 채널을 탑재할 예정입니다. TOPPAN의 새로운 플립칩 기판 라인은 SWIR 센서 어레이용으로 5마이크로미터 크기의 인듐 범프를 본딩하고 있으며, 이는 무어의 법칙이 가져다주는 이점이 더 이상 트랜지스터 게이트의 미세화가 아니라 상호 연결의 지연 시간을 최소화하는 데 있다는 점을 입증하고 있습니다.

초박형 적층 기판의 치수 드리프트

1.5 mm 이하의 탄소섬유 적층판은 180°C 이상에서 성형하면 3° 이상 뒤틀립니다. 이는 비대칭적인 프라이의 배향이 열팽창 계수(CTE)의 불일치를 증폭시키기 때문입니다. 레이저 지원 성형에서는 코어를 180°C로 유지하면서 외표면을 250°C까지 가열하지만, 장비 개조에 20만-40만 달러가 소요되기 때문에 항공우주용 스트링거에만 국한된 틈새 용도로만 사용되고 있습니다. 헥셀사의 40분 경화형 프리프레그는 ±0.5mm의 공차를 달성하고 있지만, 설계자는 보강재를 함께 접착해야 하기 때문에 경량화의 이점이 줄어들게 됩니다. 배터리 박스에서는 압력 불균형으로 인해 섬유 체적 분율의 편차가 5포인트 증가하며, 이는 열 사이클 중 잠재적인 층간 박리의 원인이 됩니다.

부문별 분석

열가소성 수지는 사이클 타임 적합성과 폐쇄 루프 방식을 통한 스크랩 재용해 등을 바탕으로, 2025년에는 열압성형 시장에서 39.11%의 점유율을 차지했습니다. 폴리프로필렌, PET, 폴리카보네이트는 식품, 자동차, 전자기기 부문을 주도하고 있는 반면, ABS는 내충격성이 요구되는 케이스 용도로 사용되고 있습니다. 바이오 유래 PLA를 포함한 기타 소재 유형은 일회용 플라스틱에 대한 지자체 차원의 금지 조치와 100℃의 핫필 공정을 견딜 수 있는 새로운 PLA 등급의 등장이라는 호재를 타고, 2031년까지 연평균 성장률(CAGR) 5.51%를 기록하며 성장하고 있습니다.

현재 각 변환 업체들은 재생 PET에 차단재로 EVOH를, 구조재로 PLA를 혼합하여, 산소 흡수 없이 냉장 식품의 유통기한을 7일에서 10일로 연장하는 다층 구조를 형성하고 있습니다. KIEFEL의 ‘NATUREFORMER’는 셀룰로오스를 성형하여 신선식품용 트레이를 제조하며, 이 트레이들은 12주 만에 가정에서 퇴비화할 수 있습니다. 복합 열가소성 플라스틱은 전기차 배터리 트레이에 필요한 강성을 확보하기 위해 탄소섬유나 유리섬유를 첨가하고 있지만, 치수 변동과 재생 섬유의 부족이 보급을 저해하고 있습니다. 열경화성 수지는 틈새 시장 부문이긴 하지만, 150℃에 지속적으로 노출될 때 페놀 수지의 순간 연소 저항성이 요구되는 상황에서는 여전히 대체할 수 없는 존재입니다.

향후 성장세는 PP 시트와 PLA 시트 간에 금형을 신속하게 교체할 수 있고, 인라인 결정도 측정 기능을 통합하며, 포장재의 EPR(확대 생산자 책임) 규정 준수에 활용할 수 있는 수명 주기 데이터를 기록할 수 있는 생산 라인에 유리하게 작용할 것으로 보입니다. 배리어 층의 공압출 성형 및 저장력 시트 공급 기술을 습득한 기업은 다층 바이오 필름으로의 전환 흐름에 동참하게 될 것으로 보입니다.

지역별 분석

아시아태평양은 2025년 매출의 45.24%를 차지했으며, 대만과 한국이 첨단 포장 시장을 확대하고 중국이 전자기기 조립을 지속함에 따라 2031년까지 연평균 성장률(CAGR) 5.84%를 기록할 전망입니다. ASE의 2026년 70억 달러 투자로 페낭에 생산 능력이 추가되어, 대만에 대한 의존에서 벗어나는 동시에 해당 지역의 열압성형기 수요를 뒷받침하게 될 것입니다. 일본의 토판과 닛샤는 40마이크로미터 이하의 구리 필러 본딩이 필요한 플립칩 기판에 투자하고 있는 반면, 중국의 전기차 판매 대수는 800만 대를 넘어 서보 유압 프레스용 배터리 트레이 수주를 뒷받침하고 있습니다.

북미 시장 점유율은 CHIPS법에 따른 보조금 덕분에 회복되고 있습니다. 2027년 가동을 예정하고 있는 암콜의 피오리아 공장에서는 미션 크리티컬한 항공우주용 칩을 위해 열압성형을 실시하여, 지정학적 충격에 대비해 공급망의 안정화를 도모할 예정입니다. 네파브의 테네시 사업장은 자동차 OEM의 재활용 소재 함유율 목표를 충족하고 있으며, 멕시코의 의료기기 산업 클러스터는 미국 OEM과의 근접성과 낮은 인건비를 활용하고 있습니다.

유럽의 포장 폐기물 규제에 따라 각 변환업체들은 퇴비화가 가능한 PLA 및 셀룰로오스 트레이로의 전환을 추진하고 있습니다. 독일, 프랑스, 영국에서는 전기차의 경량화를 목표로 하고 있으며, 주행 거리를 늘리기 위해 탄소섬유 압축 성형 기술을 활용하고 있습니다. 북유럽의 식료품점들은 잘 갖춰진 퇴비화 인프라를 바탕으로 PLA 소재 유제품 용기의 보급을 추진하고 있습니다. 정책과 치솟는 에너지 가격으로 인해, 에너지 회수형 유압 시스템으로의 설비 개조가 진행되고 있습니다. 중동 및 아프리카에서는 첫 번째 의약품 포장 공장이 건설되고 있지만, 재활용량 부족이 순환형 경제 도입을 저해하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the thermo compression forming market size is projected to expand from USD 12.11 billion in 2025 and USD 12.71 billion in 2026 to USD 16.20 billion by 2031, registering a CAGR of 4.97% between 2026 to 2031.

This report is Segmented by Material Type (Thermoplastics, Thermosets, Composites, and Other Material Types), Application (Packaging, Automotive Components, Aerospace and Defense, Electronics and Semiconductors, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Thermo Compression Forming Market Trends and Insights

Demand for Lightweight and Durable Packaging Solutions

Consumer-goods and pharmaceutical brands now specify thermoformed trays that match the barrier and drop-test credentials of injection-molded containers while trimming material mass 20-30%. Europe's Packaging and Packaging Waste Regulation sets a 2030 deadline for recyclability or compostability, prompting converters to run wall sections below 0.5 mm without puncture failures. Nefab's 2025 Tennessee hub re-grinds and re-extrudes scrap into new roll stock, letting OEMs log recycled-content metrics that feed ESG audits. Food-service chains further pull demand by switching to EN 13432-certified PLA clamshells that disintegrate in 90 days inside industrial composters, sparing landfill fees in California and Quebec.

Increased Use in Electronics Assembly and Semiconductor Packaging

Heterogeneous integration relies on copper-to-copper hybrid bonds formed at 200-400 °C with +-1-2 µm alignment. SK Hynix earmarked KRW 19 trillion (USD 13 billion) for its P&T7 advanced-packaging fab to deliver 12-layer HBM3 stacks by 2027. ASE Technology's 2026 USD 7 billion outlay will triple CoWoS-class capacity to 25,000 wafers per month and embed micro-fluidic channels for 120 kW AI racks. TOPPAN's new flip-chip substrate line bonds 5 µm indium bumps for SWIR sensor arrays, confirming that Moore's Law leverage now comes from minimizing interconnect latency rather than shrinking transistor gates.

Dimensional Drift in Ultra-thin Laminate Stacks

Carbon-fiber laminates below 1.5 mm spring back more than 3° when formed above 180 °C because asymmetric ply orientation amplifies CTE mismatch. Laser-assisted forming tempers the outer surface to 250 °C while holding the core at 180 °C, but station retrofits run USD 200,000-400,000 and thus stay niche in aerospace stringers. Hexcel's 40-minute-cure prepregs hit +-0.5 mm tolerances, yet designers must co-bond stiffeners that blunt the weight-saving rationale. In battery boxes, uneven pressure lifts fiber-volume fraction variability 5 points, a latent delamination trigger during thermal cycling.

Other drivers and restraints analyzed in the detailed report include:

- Supply-side Incentives for Reshoring Semiconductor Backend

- In-line AI-Driven Quality Analytics Enabling Zero-defect Forming

- Competition from Low-pressure Thermo-form and Injection-compression

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermoplastics captured 39.11% of the thermo compression forming market share in 2025 on the back of cycle-time compatibility and closed-loop scrap re-melt. Polypropylene, PET, and polycarbonate lead food, automotive, and electronics, while ABS serves housings demanding impact toughness. Other material types, including bio-based PLA, climb at a 5.51% CAGR through 2031, riding municipal bans on single-use plastics and new PLA grades that hold 100 °C hot-fill.

Converters now blend recycled PET with barrier EVOH and structural PLA, forming multilayers that extend chilled-food shelf life from 7 to 10 days without oxygen pick-up. KIEFEL's NATUREFORMER shapes cellulose into fresh-produce trays that home-compost in 12 weeks. Composite thermoplastics add carbon or glass fiber to meet electric-vehicle battery-tray rigidity, yet dimensional-drift and recycled-fiber scarcity temper uptake. Thermosets, while niche, remain irreplaceable where continuous 150 °C exposure demands phenolic flash-burn resistance.

Momentum will favor lines that swap tools quickly between PP and PLA sheets, integrate inline crystallinity measurement, and log life-cycle data to feed packaging EPR compliance. Firms that master barrier-layer co-extrusion and low-tension sheet feeding will ride the mix shift toward multilayer bio-based films.

Geography Analysis

Asia-Pacific held 45.24% of 2025 revenue and will post a 5.84% CAGR to 2031 as Taiwan and South Korea scale advanced packaging and China continues electronics assembly. ASE's USD 7 billion 2026 outlay adds Penang capacity, diversifying away from Taiwan and underpinning regional thermo-compression machine demand. Japan's TOPPAN and Nissha invest in flip-chip substrates that call for sub-40 µm copper-pillar bonding, while China's EV surge exceeds 8 million units, fueling battery-tray orders for servo-hydraulic presses.

North America's share revives under CHIPS Act subsidies. Amkor's Peoria plant, slated for 2027, will run thermo-compression for mission-critical aerospace chips, securing supply chains against geopolitical shocks. Nefab's Tennessee hub meets auto OEM recycled-content targets, and Mexico's medical device corridor leverages proximity to U.S. OEMs and lower labor costs.

Europe's Packaging Waste Regulation steers converters into compostable PLA and cellulose trays. Germany, France, and the U.K. target EV lightweighting, using carbon-fiber compression molding to stretch range. Nordic grocers push PLA dairy cups, supported by robust composting infrastructure. Policy and high energy prices encourage equipment retrofits with energy-recovery hydraulics. The Middle-East and Africa build first-wave pharma-pack plants, yet recycling deficits hinder circular-economy adoption.

- Amcor plc

- Avient Corporation

- Axyal

- Core Molding Technologies

- Engineered Plastic Products Inc.

- FLEXTECH

- Formed Solutions

- FRIMO Innovative Technologies

- Intertech Products, Inc.

- Janjo, Inc

- KIEFEL GmbH

- Nissha Co., Ltd.

- Ray Products Company Inc.

- TOPPAN Packaging Americas Holdings, Inc.

- UFP Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Lightweight and Durable Packaging Solutions

- 4.2.2 Increased Use in Electronics Assembly and Semiconductor Packaging

- 4.2.3 Supply-side Incentives for Reshoring Semiconductor Backend

- 4.2.4 In-line AI-driven Quality Analytics Enabling Zero-defect Forming

- 4.2.5 Ultra-fast-cycle Servo-hydraulic Presses More Than 10 000 kN Cutting Takt Time 40%

- 4.3 Market Restraints

- 4.3.1 Dimensional Drift in Ultra-thin Laminate Stacks

- 4.3.2 Competition from Low-pressure Thermo-form and Injection-compression

- 4.3.3 Scarcity of Heat-resistant Recyclable Composite Feedstock

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Thermoplastics

- 5.1.2 Thermosets

- 5.1.3 Composites

- 5.1.4 Other Material Types (Bio-based PLA, etc.)

- 5.2 By Application

- 5.2.1 Packaging

- 5.2.1.1 Food and Beverage

- 5.2.1.2 Pharmaceutical

- 5.2.1.3 Consumer Goods

- 5.2.2 Automotive Components

- 5.2.3 Aerospace and Defense

- 5.2.4 Electronics and Semiconductors

- 5.2.5 Industrial Equipment

- 5.2.6 Medical Devices

- 5.2.1 Packaging

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Avient Corporation

- 6.4.3 Axyal

- 6.4.4 Core Molding Technologies

- 6.4.5 Engineered Plastic Products Inc.

- 6.4.6 FLEXTECH

- 6.4.7 Formed Solutions

- 6.4.8 FRIMO Innovative Technologies

- 6.4.9 Intertech Products, Inc.

- 6.4.10 Janjo, Inc

- 6.4.11 KIEFEL GmbH

- 6.4.12 Nissha Co., Ltd.

- 6.4.13 Ray Products Company Inc.

- 6.4.14 TOPPAN Packaging Americas Holdings, Inc.

- 6.4.15 UFP Technologies, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment