|

시장보고서

상품코드

2062109

고순도 메탄가스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)High-Purity Methane Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

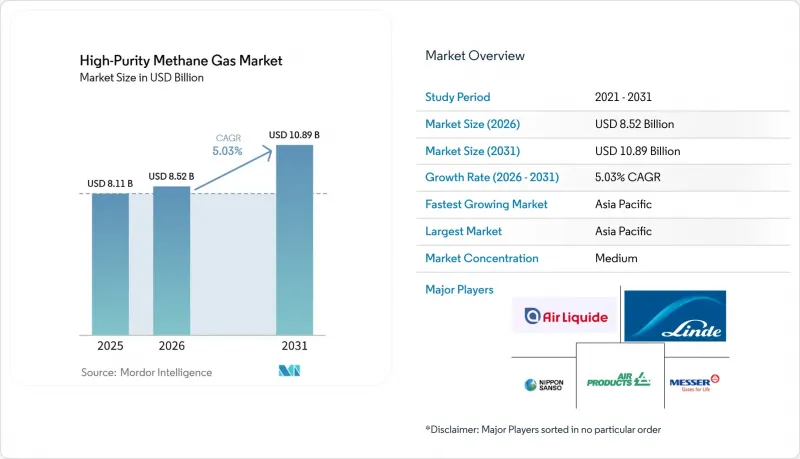

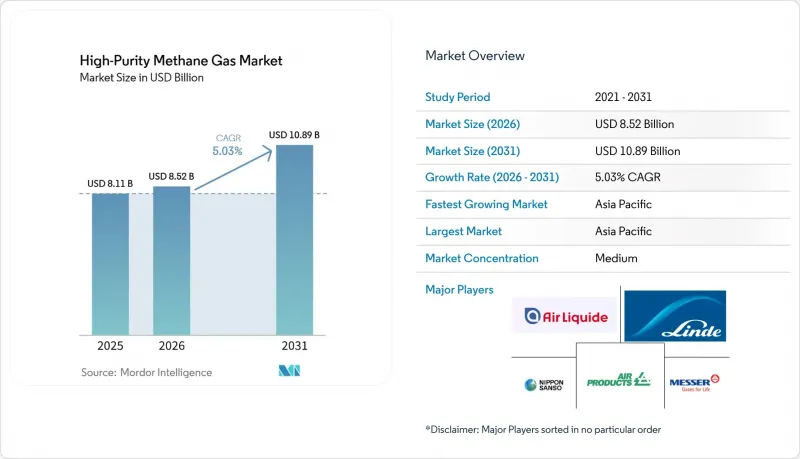

Mordor Intelligence에 의하면, 고순도 메탄가스 시장 규모는 2025년에 81억 1,000만 달러로 평가되었고, 2026년 85억 2,000만 달러로 추정되고, 2031년까지 108억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.03%를 나타낼 전망입니다.

본 보고서는 생산 방식별(천연가스 정제, 바이오메탄 개질, 기타 생산 방식), 용도별(반도체 및 전자기기, 화학제품 및 석유화학제품, 분석 및 교정 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 고순도 메탄 가스 시장 동향 및 분석

반도체 팹의 생산 능력 확충

2025년, 세계 웨이퍼 제조에 대한 투자액은 1,600억 달러에 달했습니다. 새로운 300mm 라인에서는 실리콘 카바이드 에피택시 공정을 위해 산소 및 수분 함량이 10ppb 미만인 메탄이 필요한 등 정밀한 조건이 요구됩니다. 에어 리키드는 애리조나, 싱가포르, 드레스덴에 현장 생산 시설을 설립하기 위해 2억 5,000만 달러 이상을 투자했습니다. 이 플랜트들은 메탄 순도 99.9995%를 달성하고 있으며, 극저온 분리, PSA(압력 변동 흡착) 및 촉매 정제 공정을 통합하고 있습니다. 네바다주에서는 태양일본산업가스와 닛키소가 극저온 공기분리 플랜트의 공동 개발을 추진하고 있습니다. 이 시설은 첨단 패키징 분야의 요구 사항을 충족하도록 설계되었으며, 공정 제어용 가스에 대한 실린더 백업 시스템을 갖추고 있습니다. 2025년, 센트럴 글라스와 후순은 한국에서 전자용 특수 가스의 현지화를 목표로 하는 40억 원 규모의 프로젝트를 시작했습니다. 수출 규제가 강화되고 반도체 제조업체들이 지역화에 주력하는 가운데, 고순도 메탄 가스 시장에서는 각 신흥 팹 클러스터 수요에 맞추어 정제 공정을 조정해 나갈 것으로 예측됩니다.

특수 화학제품 합성 수요의 확대

메탄은 메탄올 생산의 주요 성분이자 암모니아 제조 과정에서 간접적인 수소 공급원으로도 활용되는데, 탈탄소화 목표에 따라 귀금속 촉매를 보호하기 위한 더 깨끗한 분자에 대한 수요가 증가함에 따라 그 중요성이 커지고 있습니다. 중국석유천연가스(페트로차이나)의 다롄 복합단지에서는 퍼지 가스를 재활용하기 위해 각각 12만 Nm3/h의 정격 용량을 가진 PSA 설비를 도입했습니다. 이로 인해 배출량 모니터링의 정확성을 확보하기 위한 교정용 등급의 메탄에 대한 사내 수요가 발생하고 있습니다. 마찬가지로, 중국석유화학(Sinopec)의 타이허(Tahe) 크래커(예산 299억 8,700만 위안)에는 처리 능력 8만 Nm3/h의 수소 회수 루프가 통합되어 있으며, 교정 기준으로 순도 99.995%의 메탄이 사용되고 있습니다. 또한, 아사히카세이, 미쓰이물산, 미쓰비시상사는 2026년 에틸렌 생산의 전기화를 목표로 212억 엔 규모의 제휴를 체결했습니다. 이번 프로젝트에서는 파일럿 규모의 배치 공정에서 촉매 선별을 위해 초고순도 메탄이 사용될 예정입니다. 이러한 동향은 고순도 메탄 가스 시장의 주요 용도에 힘입어, 메탄이 단순한 상품에서 정밀 시약으로 그 역할을 변화시키고 있음을 여실히 보여주고 있습니다.

고순도화 및 분리 비용

단계적 PSA, 극저온 및 촉매 정제 공정을 결합하여 99.995%의 순도를 달성할 경우, 1kg당 비용이 0.50-1.20달러 증가할 수 있습니다. 반면, 막 기술을 활용한 대안은 설비 투자(CAPEX) 절감이라는 선택지를 제공하지만, CO₂와 CH₄의 선택성 간의 상충 관계나, 미처리 바이오가스를 처리할 때 발생하는 오염(fouling) 문제와 같은 과제에 직면해 있습니다. 원자당 97eV의 에너지와 정교한 광학 시스템을 필요로 하는 레이저 동위원소 분리법은 탄소-12 메탄에서 99.9%의 순도를 달성하기 위해 1kg당 10MWh 이상을 소비하는 극저온 증류 캐스케이드 방식과는 대조적입니다. 인도나 동남아시아에서는 독립 기업들이 사전 충전된 가스통을 수입하는 경우가 많은데, 이때 발생하는 운송비 추가 비용이 이익률을 압박하고 있습니다. 새로운 고순도 플랜트를 건설하려면 2,000만-5,000만 달러의 투자가 필요하며, 투자 회수 기간이 5년을 초과하기 때문에 아직 발전 단계에 있는 반도체 수요가 신규 진입의 장벽이 되어, 고순도 메탄 가스 시장의 각 부문별 성장을 제한하고 있습니다.

부문별 분석

2025년, 천연가스 정제 시장은 고순도 메탄 가스 시장 점유율의 62.21%를 차지했습니다. 이는 확립된 극저온 및 PSA 인프라를 활용하며, 전 세계 580곳 이상에서 가동 중인 린데(Linde)사의 플랜트에 의해 뒷받침되고 있습니다. 고순도 메탄 가스 시장 내 천연가스 정제 시장은 애리조나, 드레스덴, 신주의 메가팹에 공급하는 온사이트 시스템에 힘입어 2026년부터 2031년까지 연평균 성장률(CAGR) 5.12%를 나타낼 것으로 예측됩니다. 현재 비교적 작은 비중을 차지하는 바이오메탄 정제 시장은 2031년까지 연평균 성장률(CAGR) 5.68%로 성장할 것으로 전망됩니다. 이러한 성장은 유럽의 재생에너지 지침(RED) 할당량과 중국 및 인도의 고정가격임베디드제도(FIT)에 따른 인센티브에 기인합니다. 막 캐스케이드와 저온 정제를 결합하여 99.995%의 순도를 달성함으로써, 기존에는 화석 연료 파이프라인에 의존하던 반도체 고객사에 정제 가스를 공급할 수 있게 됩니다. 투자 결정은 탄소 크레딧의 프리미엄과 농업 원료와의 근접성에 따라 좌우되며, 프로젝트 파이프라인은 미국 중서부, 프랑스 북부, 그리고 중국 연안 지역으로 이동하고 있습니다. 발전용 전기에 기인한 메탄은 시장의 5% 미만을 차지할 뿐이지만, 재생에너지의 도입 확대에 따라 2020년대 후반에는 그 성장이 가속화되어 고순도 메탄 가스 시장의 비용 구조에 영향을 미칠 가능성이 있습니다.

파이프라인망이 잘 갖춰진 지역에서는 천연가스 정제가 여전히 선호되는 선택지입니다. 예를 들어, 텍사스주, 장쑤성 및 걸프협력회의(GCC) 지역의 통합 석유화학 허브에서는 최소한의 추가 설비 투자만으로 기존 분별탑에 특수 가스용 스키드를 통합할 수 있습니다. 반면, 유럽의 농업 집적지에 위치한 바이오가스 시설에서는 현지 원료와 탄소 가격 제도를 활용하여, 실험실 및 분석 용도로 사용되는 초고순도 분자를 경쟁력 있는 가격에 제공합니다. 플라즈마 촉매 CO₂ 메탄화 등의 합성 기술은 전해조의 가격 하락에 따라 기술 성숙도(TRL)가 향상되고 있으며, 화석 연료 공급 문제에 대처하기 위한 잠재적인 대안으로 부상하고 있습니다. 2026-2031년 고순도 메탄 가스 시장 전반에서 균형 잡힌 사업 전개를 목표로 하는 공급업체들에게 포트폴리오 다각화가 중요한 전략이 될 것으로 보입니다.

지역별 분석

2025년, 아시아태평양은 고순도 메탄 가스 시장의 43.11%라는 큰 점유율을 차지했습니다. 예측에 따르면, 2026-2031년 연평균 성장률(CAGR) 5.78%라는 견실한 성장세를 보일 것으로 전망됩니다. 2024-2026년 중국의 '국가 집적회로 기금 제3기'는 450억 달러 이상을 배정하여 우시와 우한의 신규 팹 건설을 지원했습니다. 이 생산 시설에는 메탄, 질소, 아르곤용 현장 정제 스키드가 설치되어 있습니다. 한편, 한국에서는 첨단 패키징 산업을 위한 29조 원 규모의 야심 찬 경기 부양책을 통해 국내 가스 공급업체에 자금이 투입되고 있습니다. 이 공급업체들은 일본의 라이선스 제공 기업과 제휴하여 가스 캐비닛 및 분석 서비스의 맞춤형 개발을 추진하고 있습니다. 인도에서는 '반도체 미션'을 통해 드레라 및 마이소르 클러스터에 76,000억 루피라는 막대한 자금을 투입하고 있습니다. 동시에, INOX Air Products사는 구자라트주에 거점을 설립할 예정이며, 2027년 초까지 연간 1만 2,000톤의 초고순도 가스를 생산할 것으로 전망됩니다. 현재 전 세계 백엔드 산업의 20% 이상을 차지하는 아세안(ASEAN) 국가들에서 말레이시아와 베트남 정부는 특수 가스 기기에 대한 관세 면제 조치를 합리화하고 있습니다. 이러한 움직임은 Tier 1 OSAT(반도체 수탁 제조업체)를 유치하기 위한 것으로, 고순도 메탄 가스 시장에 대한 지역적 수요를 크게 끌어올릴 것입니다.

북미 시장은 규모 면에서 2위를 차지하고 있습니다. 주요 투자 사례로는 애리조나주에 위치한 에어 리퀴드(Air Liquide)사의 2억 5,000만 달러 규모 사업과 오하이오주에 위치한 에어 프로덕츠(Air Products)사의 확장 계획이 있습니다. 특히 인텔이나 TSMC의 팹에서는 5.0 등급 메탄 공급과 관련하여 철도 차량이나 파이프라인을 통한 중복 백업 체계의 중요성이 강조되고 있습니다. 인플레이션 억제법(Inflation Reduction Act)은 청정 수소에 대한 세액 공제를 제공하며, 비용 곡선이 유리할 경우 가스 공급 구조가 메탄 열분해 방식으로 전환될 가능성을 시사하고 있습니다. 유럽의 관심은 바이오메탄과 수소 회랑으로 옮겨가고 있습니다. 독일의 H2 코어 네트워크는 Linde 및 Messer의 허브와 통합될 예정입니다. 동시에, 네덜란드에서는 권리 제한이 적용되는 바이오메탄 클러스터 실험이 진행 중이며, 전자기기 등급 기준을 충족할 수 있도록 정제 공정이 진행되고 있습니다. 중동 및 아프리카의 점유율은 작지만 증가 추세에 있습니다. 주바이르에서 진행 중인 Linde, Aramco, SLB의 합작 사업은 2027년까지 연간 900만 톤의 CO2 포집을 목표로 하고 있으며, 이로 인해 교정 가스 수요가 증가할 것으로 예측됩니다. 남미에서는 브라질의 바이오가스 자원과 아르헨티나의 셰일 자원이, 일관된 정책 수립을 전제로 정제 프로젝트의 기회를 제공합니다.

지역 간 격차로 인해 공급업체들은 지역에 맞춘 전략을 수립해야 합니다. 아시아태평양에서는 석유화학 단지나 기가팹 내 입지를 통해 업무 효율이 향상되고, 실린더 운송 시간 단축과 수입 절차의 복잡성 완화가 도모됩니다. 유럽에서는 인수합병 활동이 급증하고 있으며, 산업용 가스 대기업들이 바이오가스 개발 기업과 제휴하여 재생 가능 가스 할당 목표를 달성하기 위해 노력하고 있습니다. 북미에는 광범위한 중류 자산이 존재하기 때문에 증기 회수 트레일러나 대용량 튜브 모듈의 활용이 적합하며, 광대한 팹 캠퍼스에 대한 효율적인 서비스 제공이 보장되고 있습니다. 이러한 지역별 복잡한 사정은 자본 배분에 영향을 미칠 뿐만 아니라, 고순도 메탄가스 시장 경쟁 구도를 형성하는 데에도 지극히 중요한 역할을 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the high-Purity methane gas market size was valued at USD 8.11 billion in 2025 and is estimated to grow from USD 8.52 billion in 2026 to reach USD 10.89 billion by 2031, at a CAGR of 5.03% during the forecast period (2026-2031).

This report is Segmented by Production Method (Natural-Gas Purification, Biomethane Upgrading, Other Production Methods), Application (Semiconductors and Electronics, Chemicals and Petrochemicals, Analytical and Calibration, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global High-Purity Methane Gas Market Trends and Insights

Semiconductor Fab Capacity Additions

In 2025, global wafer fabrication investments reached USD 160 billion. New 300 mm lines require precise conditions, specifying methane with oxygen and moisture levels below 10 ppb for silicon-carbide epitaxy. Air Liquide allocated over USD 250 million to establish on-site units in Arizona, Singapore, and Dresden. These units, achieving 99.9995% methane purity, incorporate cryogenic, PSA, and catalytic polishing steps. In Nevada, Taiyo Nippon Sanso and Nikkiso are collaborating on a cryogenic air-separation plant. This facility is designed to support advanced packaging needs, providing a cylinder backup for process-control gases. In 2025, Central Glass and Foosung launched a KRW 4 billion project in South Korea to localize electronic specialty gases. As export controls become stricter, prompting chipmakers to focus on regionalization, the High-Purity Methane Gas market is expected to align purification processes with the needs of each emerging fab cluster.

Growth in Specialty-Chemical Synthesis Demand

Methane, a key component in the production of methanol and an indirect hydrogen vector for ammonia, is increasingly significant as decarbonization targets drive the need for cleaner molecules to protect precious metal catalysts. PetroChina's Dalian complex has installed PSA units, each rated at 120,000 Nm3 h-1, to recycle purge gases. This has created in-house demand for calibration-grade methane, which ensures emissions-monitor accuracy. Similarly, Sinopec's Tahe cracker, with a budget of RMB 29.987 billion, incorporates hydrogen recovery loops with a capacity of 80,000 Nm3 h-1, relying on 99.995% pure methane as a calibration standard. Additionally, Asahi Kasei, Mitsui, and Mitsubishi formed a JPY 21.2 billion alliance in 2026 to electrify ethylene production. This initiative is expected to use ultra-pure methane in pilot-scale batches for catalyst screening. These developments highlight methane's evolving role from a commodity to a precision reagent, driven by its critical applications in the High-Purity Methane Gas market.

High Purification and Isolation Cost

Staged PSA, cryogenic, and catalytic polishing trains can increase costs by USD 0.50-1.20 per kg to achieve 99.995% purity. While membrane alternatives present an option for lower capex, they encounter challenges such as selectivity trade-offs between CO2 and CH4 and fouling issues when processing raw biogas. Laser isotope separation, requiring 97 eV per atom and advanced optics, contrasts with cryogenic distillation cascades, which consume over 10 MWh per kg to reach 99.9% purity in carbon-12 methane. In India and Southeast Asia, independents often import pre-purified cylinders, incurring freight premiums that reduce their margins. Establishing a greenfield high-purity plant involves an investment of USD 20-50 million, and with payback periods exceeding five years, the still-developing semiconductor demand creates barriers for new entrants, limiting growth in segments of the High-Purity Methane Gas market.

Other drivers and restraints analyzed in the detailed report include:

- Clean-Energy and Hydrogen-Economy Expansion

- Uptake of Ultra-High-Purity Gases in Analytical Instrumentation

- Complex Storage and Transport Safety Norms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, natural-gas purification accounted for 62.21% of the High-Purity Methane Gas market share, supported by more than 580 operational Linde plants globally, utilizing established cryogenic and PSA infrastructure. The market for natural-gas purification in High-Purity Methane Gas is expected to grow at a 5.12% CAGR from 2026 to 2031, driven by on-site systems supplying mega-fabs in Arizona, Dresden, and Hsinchu. Biomethane upgrading, which currently represents a smaller segment, is projected to grow at a 5.68% CAGR through 2031. This growth is attributed to Renewable Energy Directive quotas in Europe and feed-in-tariff incentives in China and India. Membrane cascades combined with low-temperature polishing achieve 99.995% purity, enabling upgraded gas to cater to semiconductor clients that previously relied on fossil pipelines. Investment decisions are influenced by carbon-credit premiums and proximity to agricultural feedstock, shifting project pipelines toward the Midwest U.S., Northern France, and coastal China. Although synthetic power-to-methane represents less than 5% of the market, increased renewable-electricity adoption could drive its growth in the latter half of the decade, potentially impacting the cost structure of the High-Purity Methane Gas market.

Natural-gas purification remains a preferred option in regions with strong pipeline networks. For example, integrated petrochemical hubs in Texas, Jiangsu, and the Gulf Cooperation Council can integrate specialty-gas skids into existing fractionation columns with minimal additional capital expenditure. In contrast, biogas facilities in Europe's agricultural clusters utilize local feedstock and carbon pricing to offer competitive pricing on high-purity molecules for laboratory and analytical applications. Synthetic methods, such as plasma-catalytic CO2 methanation, are advancing in technology readiness levels (TRL) as electrolyzer prices decline, providing a potential alternative to address fossil supply challenges. From 2026 to 2031, diversifying portfolios is expected to be a key strategy for suppliers aiming for balanced exposure across the High-Purity Methane Gas market.

Geography Analysis

In 2025, Asia-Pacific commanded a significant 43.11% share of the High-Purity Methane Gas market. Projections indicate a robust growth trajectory, with an anticipated CAGR of 5.78% from 2026 to 2031. Between 2024 and 2026, China's National Integrated Circuit Fund Phase III allocated over USD 45 billion, backing new fabs in Wuxi and Wuhan. These fabs are equipped with on-site purification skids for methane, nitrogen, and argon. Meanwhile, South Korea's ambitious KRW 29 trillion stimulus for advanced packaging is channeling funds towards domestic gas suppliers. These suppliers are collaborating with Japanese licensors to customize gas cabinets and analytical services. In India, the Semiconductor Mission is directing a substantial INR 76,000 crore towards the Dholera and Mysuru clusters. Concurrently, INOX Air Products is set to launch a hub in Gujarat, producing 12,000 tons annually of ultra-clean gases by early 2027. ASEAN nations, now home to over 20% of global back-end operations, see Malaysia and Vietnam's governments streamlining duty exemptions on specialty-gas equipment. This move aims to attract tier-one OSATs, significantly boosting regional demand for the High-Purity Methane Gas market.

North America stands as the second-largest player in the market. Key investments include Air Liquide's USD 250 million venture in Arizona and Air Products' expansion efforts in Ohio. Notably, fabs from Intel and TSMC emphasize the importance of redundant railcar and pipeline back-ups for 5.0-grade methane. The Inflation Reduction Act offers tax credits for clean hydrogen, hinting at a potential shift in the gas balance towards methane pyrolysis, contingent on favorable cost curves. Europe's focus is shifting towards biomethane and hydrogen corridors. Germany's H2 core network is set to integrate with hubs from Linde and Messer. Simultaneously, the Netherlands is experimenting with deed-restricted biomethane clusters, refining streams to meet electronics-grade standards. While the Middle East and Africa hold a smaller share, it's on the rise. A collaborative venture between Linde, Aramco, and SLB in Jubail aims for a 9 Metric tons per year CO2 capture by 2027, bolstering the demand for calibration gas. In South America, Brazil's biogas resources and Argentina's shale assets present opportunities for purification projects, contingent on the establishment of consistent policies.

Regional disparities necessitate localized strategies for suppliers. In Asia-Pacific, positioning within petrochemical parks and gigafabs streamlines operations, reducing both transit times for cylinders and the complexities of import paperwork. Europe witnesses a surge in merger activities, with industrial-gas giants joining forces with biogas developers to align with renewable-gas quotas. North America's extensive midstream assets favor the use of vapor-return trailers and large-volume tube modules, ensuring efficient service to expansive fab campuses. These regional intricacies not only influence capital distribution but also play a pivotal role in shaping competitive dynamics within the High-Purity Methane Gas market.

- Advanced Specialty Gases

- AGTI

- Air Liquide S.A.

- Air Products and Chemicals Inc.

- American Welding and Gas (AWG)

- Asahi Kasei Corporation

- Asahi Kasei Corporation

- Axcel Gases

- Bhoruka Specialty Gases Pvt Ltd

- Chemix Specialty Gases And Equipment.

- Element Solutions Inc

- Linde plc

- Messer Group GmbH

- OSAKA GAS LIQUID Co., Ltd.

- Taiyo Nippon Sanso Corporation

- Yingde Gases Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Semiconductor Fab Capacity Additions

- 4.2.2 Growth in Specialty-Chemical Synthesis Demand

- 4.2.3 Clean-Energy and Hydrogen-Economy Expansion

- 4.2.4 Uptake of Ultra High Purity Gases in Analytical Instrumentation

- 4.2.5 Growing Requirement of Quantum Grade Methane for Diamond-CVD Qubits

- 4.3 Market Restraints

- 4.3.1 High Purification and Isolation cost

- 4.3.2 Complex Storage and Transport Safety Norms

- 4.3.3 Scarce Supply of Isotopically-enriched Methane

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Production Method

- 5.1.1 Natural-gas purification

- 5.1.2 Biomethane upgrading

- 5.1.3 Other Production Methods (Synthetic / Power-to-Methane (PtM), Methane-pyrolysis recycle)

- 5.2 By Application

- 5.2.1 Semiconductors and Electronics

- 5.2.2 Chemicals and Petrochemicals

- 5.2.3 Analytical and Calibration

- 5.2.4 Power Generation / Turbines

- 5.2.5 Research and Development

- 5.2.6 Other Applications (Quantum-technologies, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Advanced Specialty Gases

- 6.4.2 AGTI

- 6.4.3 Air Liquide S.A.

- 6.4.4 Air Products and Chemicals Inc.

- 6.4.5 American Welding and Gas (AWG)

- 6.4.6 Asahi Kasei Corporation

- 6.4.7 Asahi Kasei Corporation

- 6.4.8 Axcel Gases

- 6.4.9 Bhoruka Specialty Gases Pvt Ltd

- 6.4.10 Chemix Specialty Gases And Equipment.

- 6.4.11 Element Solutions Inc

- 6.4.12 Linde plc

- 6.4.13 Messer Group GmbH

- 6.4.14 OSAKA GAS LIQUID Co., Ltd.

- 6.4.15 Taiyo Nippon Sanso Corporation

- 6.4.16 Yingde Gases Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment