|

시장보고서

상품코드

2062116

코발트 합금 분말 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cobalt Alloy Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

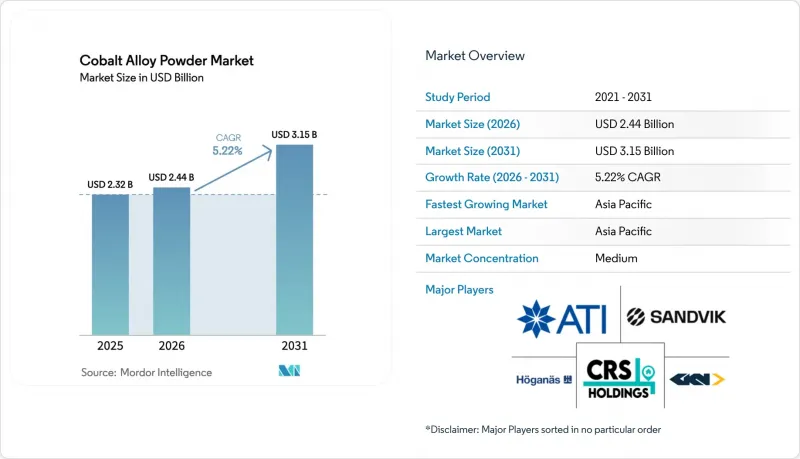

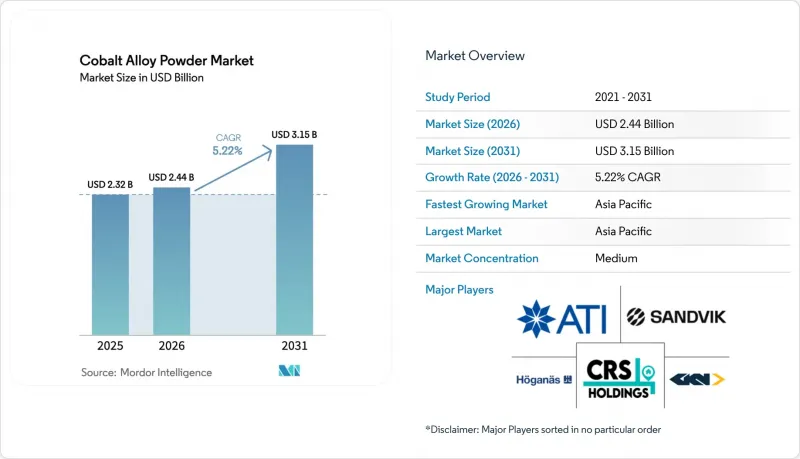

Mordor Intelligence에 의하면, 코발트 합금 분말 시장 규모는 2025년에 23억 2,000만 달러로 평가되었고 2026년 24억 4,000만 달러에서 2031년까지 31억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.22%를 나타낼 전망입니다.

본 보고서는 합금 유형(코발트-크롬, 코발트-니켈, 코발트-철 등), 제조 방법(분무법, 화학적 환원법, 전해법, 기계적 합금화법), 용도(적층 가공, 항공우주, 의료, 공구, 용사, 에너지, 기타), 최종 사용자 산업(의료, 기타), 지역(아시아태평양, 기타)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준입니다.

세계 코발트 합금 분말 시장 동향 및 분석

항공우주 및 의료 분야의 고성능 수요

차세대 민간용 엔진의 경우, 터빈 입구 온도가 1,650°C를 초과하게 되었습니다. 이러한 급격한 상승으로 인해, 특히 니켈계 소재가 한계에 도달하는 상황에서 내산화성으로 정평이 나 있는 코발트·크롬 분말에 대한 수요가 증가하고 있습니다. 이러한 성장세를 뒷받침하는 움직임으로, ATI는 2025년에 대규모 적층 가공 시설을 개소했습니다. 이 시설에서는 미 해군 원자로용으로 특별히 설계된, 높이 최대 1.5m의 코발트 초합금 부품을 3D 프린팅하고 있습니다. 의료기기 분야에서는 ASTM F75 규격에 부합하는 CoCrMo가 여전히 인공 고관절 스템의 주류를 이루고 있지만, EU 의료기기 규정에 따라 코발트는 최근 CMR(발암성, 변이원성, 생식독성) 물질로 지정되었습니다. 이 규정에 따라 특정 기준치를 초과하는 코발트 함유량에는 경고 라벨 부착이 의무화되었으며, 티타늄 단독으로 제작된 접합부에 대한 시험이 활성화되고 있습니다. ECRI의 검토 결과에 따르면, 코발트-크롬 스텐트와 기타 스텐트 간에 표적 병변의 재관류에 유의미한 차이는 나타나지 않았으며, 대체품의 필요성은 낮은 것으로 나타났습니다. 이러한 규제상의 장벽에 대응하기 위해 카펜터 테크놀로지사는 ‘BioDur 108’을 도입했습니다. 니켈과 코발트를 모두 포함하지 않는 이 혁신적인 등급은 우수한 인장 강도를 지닌 오스테나이트계 스테인리스 스틸으로, MDR 표시 의무를 교묘히 회피하고 있습니다. 그러나 2024년 소비 데이터에 따르면, 초합금이 전 세계 코발트 사용량의 상당 부분을 차지하고 있으며, 항공우주 산업과 임플란트 산업 양쪽 모두에서 꾸준한 수요가 있음을 보여주고 있습니다.

내마모성·내식성 공구재 수요

스텔라이트(Stellite) 및 트리발로이(Tribaloy) 시리즈는 현재 절삭 공구, 석유 및 가스용 밸브, 열간 성형 금형 등, 기존에는 초경합금이 충분한 성능을 발휘하지 못했던 분야에서 사용되고 있습니다. 600°C에서 실시된 시험에서 서스펜션 플라즈마 분사로 형성된 코발트 산화물 코팅이 가장 낮은 마모율을 나타냈습니다. 이러한 뛰어난 성능은 윤활성을 지닌 유약층을 형성하는 CoO에서 Co₃O₄로의 상변화에 기인합니다. 케나메탈의 인프라 부문은 네바다주, 노스캐롤라이나주, 독일, 중국에 분말 공장을 운영하고 있으며, 이러한 첨단 응용 분야에 코발트 결합 초경합금을 공급하고 있습니다. 최근 일본은 금속 분말 생산량을 늘리고 있으며, 밸브나 금형 개조에 필수적인 구상 CoCrMo 원료 수요가 급증하고 있습니다. 또한, 고속 산소 연료 및 공기 연료 제트 가공에서는 디지털 분말 패스포트가 도입되어 추적성이 향상되었으며, 공구 공급망에서의 폐기물이 감소하고 있습니다.

환경 및 윤리적 채굴 문제

2025년, 콩고 민주 공화국(DRC)은 코발트 시장에서 지배적인 위치를 유지하며 전 세계 코발트 채굴량의 대부분을 차지했습니다. 그러나 추적성 향상을 위한 노력에도 불구하고, DRC의 소규모 채굴 사업에서는 여전히 아동 노동 의혹이 제기되고 있습니다. 2026년 콩고민주공화국에서 4개월간 수출이 중단되면서 코발트 가격이 급등했습니다. 이러한 가격 급등으로 인해 아토마이저의 이익률이 압박받게 되자, 인도네시아산 HPAL 침전물로 전환하는 움직임이 가속화되었습니다. 동시에, RMAP 준수 여부에 대한 제련소 감사 결과 ESG 프리미엄의 중요성이 부각되었으나, 가격에 민감한 많은 금형 부문에서는 그 도입에 소극적인 태도를 보였습니다.

부문별 분석

2025년, 터빈 블레이드 및 정형외과용 임플란트 수요에 힘입어 코발트-크롬 합금은 코발트 합금 분말 시장의 47.11%를 차지했습니다. 2026년부터 2031년까지 연평균 성장률(CAGR) 5.76%를 나타낼 것으로 예측되는 이 분말들은 800℃가 넘는 고온에서의 산화를 견디며, 관절면의 마모를 방지합니다. 그러나 EU의 MDR(의료기기 규정)에 따른 CMR(발암성, 변이원성, 생식독성) 표기로 인해, 일부 임플란트는 티타늄이나 스테인리스 스틸 대체재로 전환될 가능성이 있습니다. 한편, 코발트·니켈 등의 2세대 합금은 연소기 라이너에 사용되며, 코발트·철 합금은 연자성 부품에 사용됩니다. Tribaloy나 CoCrAlY 본딩 코팅과 같은 특수 등급은 틈새 시장의 마모 방지 및 코팅 용도로 활용되고 있습니다.

적층 가공(애디티브 매뉴팩처링)는 코발트-크롬의 중요성을 부각시키고 있으며, 복잡한 냉각 통로나 환자별로 맞춤화된 형상의 구현을 가능하게 하고 있습니다. FOMAS 그룹의 MIMETE N 75 분말은 그 범용성을 입증하고 있으며, 산업용 가스터빈에 적용되고 있습니다. 한편, 항복 강도가 755 MPa를 초과하는 고엔탈피 합금(HEA)의 시제품은 2030년대 중반에는 시장에서 잠재적인 위협이 될 가능성이 있습니다. 그러나 항공우주 분야의 10년에 달하는 승인 절차와 원자재 비용의 급등으로 인해, 당분간은 코발트-크롬 합금이 계속해서 주목을 받을 것으로 보입니다.

2025년까지 코발트 합금 분말 생산에서 아토마이징 공법이 73.22%의 점유율을 차지하며 주류로 자리 잡았습니다. LPBF용 원료의 경우, 가스 및 진공 유도 용해 가스 분무법(VIGA)이 첫 번째 선택지로 떠올랐습니다. 한편, 수분 분무법은 그 독특한 형태가 유동성을 방해하지 않는 프레스·소결 부품 분야에서 독자적인 틈새 시장을 개척했습니다. 분무법은 성장 궤도에 올라 있으며, 2026년부터 2031년까지의 예측 기간 동안 연평균 성장률(CAGR) 6.03%로 확대되고 있습니다. 이러한 급속한 성장은 주로 초음파 분무법을 통해 이루어졌으며, 스크랩을 95% 구형 분말로 재활용하고, ISO/ASTM 52907 규격을 충족하기 위해 산소 함량을 500ppm 미만으로 유지하고 있습니다.

2025년 시범 프로젝트에서 FeCoNi의 재활용이 입증됨에 따라 신규 원료의 필요성이 사라졌습니다. 마찬가지로, Powder2Powder 시스템은 니어 넷 제로(Near Net Zero) 공급망을 실현하기 위해 개발되었습니다. 기계적 합금화는 오염 우려로 인해 주로 연구 분야에 국한되어 있지만, 전해법은 초고순도 니치 등급에 대한 수요를 효과적으로 충족시키고 있습니다. 게다가 디지털화된 파우더 패스포트나 AI를 활용한 인라인 센서와 같은 혁신 기술들이 업계의 모습을 완전히 바꿔놓고 있습니다. 이러한 발전 덕분에 입자 분포를 실시간으로 모니터링할 수 있게 되었으며, VIGA 및 플라즈마 생산 라인 모두에서 배치 불량률이 현저히 감소하고 있습니다.

지역별 분석

2025년, 중국의 정제 분야에서의 우위와 2024년 분말 야금 생산량 증가에 힘입어 아시아태평양은 전 세계 매출의 36.67%를 차지했으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.03%라는 견실한 성장세를 보였습니다. 한국의 항공우주 분야 지출 확대는 CoCr 터빈 디스크의 국내 수요를 촉진했습니다. 한편, 싱가포르에서의 플라즈마 재활용 실증 시험과 인도에서 부상하고 있는 AM 클러스터가 호재가 되었음에도 불구하고, 두 지역 모두 여전히 수입 분말에 대한 의존도가 높습니다.

북미도 이에 발맞추어 주요 주에 걸쳐 있는 적층 가공 허브와 분말 공장을 활용하며, 모두 인플레이션 감축법(IRA)의 세액 공제 혜택을 받고 있습니다. 캐나다의 MRO 생태계와 멕시코의 1차 자동차 부품 공급업체들이 수요를 견인했으나, 두 국가 모두 콩고민주공화국(DRC)에서 비롯된 공급 차질에 직면할 가능성이 있습니다.

유럽에서는 항공우주 및 의료 분야 수요가 견조했으나, 해당 대륙의 엄격한 규제에 대응하는 데 어려움을 겪었습니다. 주요 공급업체들은 독일, 영국, 프랑스에 거점을 마련했습니다. 그러나 여전히 과제가 남아 있습니다. MDR(의료기기 규정)의 CMR(중요 원자재) 표기 요건은 코발트 임플란트공급량을 위협하고 있으며, ‘중요 원자재법’은 대륙 내 정제 시설 구축을 시급한 과제로 삼고 있습니다. 그렇긴 하지만, 북유럽의 수소 프로젝트와 해상 풍력 발전 사업이 탄력을 받고 있는 만큼, 이러한 움직임이 정형외과 분야의 잠재적인 위축을 상쇄할 가능성이 있습니다.

남미 및 중동 및 아프리카(MEA) 지역의 기여도는 미미했습니다. 브라질은 기존 파이프라인망을 활용했고, 사우디아라비아는 ‘비전 2030’ 자금을 투입해 가스터빈 기술 강화를 도모했습니다. 2025년 말에 해제된 콩고민주공화국(DRC)에 대한 수출 중단 조치는 아프리카가 원자재 공급 면에서 아시아에 의존하고 있는 현실을 여실히 드러냈습니다. 이러한 인식이 인도네시아 내 HPAL(고압 산 처리) 설비의 급속한 확장을 뒷받침했으며, 전략적 제휴를 통해 현재는 상당한 생산 규모를 달성했습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the cobalt alloy powder market size was valued at USD 2.32 billion in 2025 and is estimated to grow from USD 2.44 billion in 2026 to reach USD 3.15 billion by 2031, at a CAGR of 5.22% during the forecast period (2026-2031).

This report is Segmented by Alloy Type (Cobalt-Chromium, Cobalt-Nickel, Cobalt-Iron, and More), Production Method (Atomization, Chemical Reduction, Electrolytic, and Mechanical Alloying), Application (Additive Manufacturing, Aerospace, Medical, Tooling, Thermal Spray, Energy, and Others), End-User Industry (Healthcare, and More), and Geography (Asia-Pacific, and More). Market Forecasts in Value (USD).

Global Cobalt Alloy Powder Market Trends and Insights

Aerospace/Medical High-Performance Needs

Next-gen commercial engines are now pushing turbine inlet temperatures beyond 1,650 °C. This surge is driving up the demand for cobalt-chromium powders, celebrated for their oxidation resistance, especially in scenarios where nickel systems falter. In a move that underscores its scaling momentum, ATI inaugurated a large additive facility in 2025. At this facility, they print cobalt superalloy parts with heights of up to 1.5 m, tailored specifically for U.S. naval reactors. In the medical device arena, while ASTM F75-compliant CoCrMo remains the preferred choice for hip stems, the EU Medical Device Regulation has recently flagged cobalt as a CMR. This designation mandates warning labels for cobalt content surpassing a specific threshold and has spurred trials for titanium-only junctions. ECRI reviews highlighted no significant difference in target-lesion revascularization between cobalt-chromium stents and their counterparts, reducing the urgency for alternatives. In response to these regulatory hurdles, Carpenter Technology introduced BioDur 108. This innovative grade, free from both nickel and cobalt, is an austenitic stainless steel with impressive tensile strength, cleverly avoiding MDR labels. However, consumption data from 2024 reveals that superalloys accounted for a significant share of global cobalt usage, spotlighting the unwavering demand from both aerospace and implant industries.

Wear and Corrosion-Resistant Tooling Demand

Stellite and Tribaloy families are now used in applications such as cutting tools, oil-and-gas valves, and hot-forming dies, where carbides previously underperformed. In tests conducted at 600 °C, thermal-sprayed cobalt-oxide coatings, applied through a suspension plasma spray, exhibited the lowest wear rates. This superior performance is attributed to CoO-to-Co3O4 phase transitions, which form lubricious glaze layers. Kennametal's Infrastructure division operates powder plants in Nevada, North Carolina, Germany, and China, supplying cobalt-bonded carbides for these advanced applications. Japan has increased its metal powder production in recent years, driving a surge in demand for spherical CoCrMo feedstock, which is crucial for refurbishing valves and dies. Additionally, high-velocity oxy-fuel and air-fuel jets have adopted digital powder passports, improving traceability and reducing scrap in the tooling supply chain.

Environmental and Ethical Mining Issues

In 2025, the Democratic Republic of Congo (DRC) maintained its position as the dominant player in the cobalt market, accounting for the majority of the world's mined cobalt. However, despite efforts to enhance traceability, artisanal operations in the DRC continued to face allegations of child labor. A four-month export freeze in the DRC during 2026 caused a significant increase in cobalt prices. This price surge tightened margins for atomizers, prompting a shift toward Indonesian HPAL precipitate. At the same time, audits of smelters for RMAP compliance highlighted the growing importance of ESG premiums, which many price-sensitive tooling segments have been reluctant to adopt.

Other drivers and restraints analyzed in the detailed report include:

- Hydrogen-Turbine Material Requirements

- Cold-Spray Repair Adoption in MRO

- EU Critical-Materials Limits in Implants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, cobalt-chromium alloys, driven by demand for turbine blades and orthopedic implants, accounted for 47.11% of the cobalt alloy powder market. These powders, forecasted to grow at a 5.76% CAGR during the 2026-2031 period, resist oxidation at temperatures exceeding 800 degrees Celsius and protect against wear on articulating surfaces. However, the EU's MDR CMR labeling could steer some implants toward titanium and stainless steel alternatives. Meanwhile, second-tier systems such as cobalt-nickel are used in combustor liners, while cobalt-iron is directed toward soft-magnetic components. Specialized grades, including Tribaloy and CoCrAlY bond coats, serve niche wear and coating applications.

Additive manufacturing highlights the importance of cobalt-chromium, enabling intricate cooling passages and customized patient geometries. The FOMAS group's MIMETE N 75 powder demonstrates its versatility, finding application in industrial gas turbines. Conversely, HEA prototypes with yields exceeding 755 MPa may pose a potential market threat in the mid-2030s. However, with a decade-long approval process in aerospace and elevated raw material costs, cobalt-chromium continues to dominate the spotlight for the time being.

By 2025, cobalt alloy powder production saw atomization dominate with a 73.22% share. For LPBF feedstocks, gas and vacuum induction melting gas atomization (VIGA) became the top choice. Meanwhile, water atomization found its niche in press-and-sinter parts, where its unique morphology did not hinder flowability. Atomization has been on a growth trajectory, expanding at a 6.03% CAGR during the forecast period of 2026-2031. This surge is largely attributed to ultrasonic variants, which recycle scrap into a 95%-spherical powder, maintaining an oxygen content below 500 ppm to meet ISO/ASTM 52907 standards.

A 2025 pilot showcased the recycling of FeCoNi, eliminating the need for virgin feedstock. In a similar vein, the Powder2Powder system was crafted to approach near-net-zero supply chains. While mechanical alloying is predominantly a research domain due to contamination concerns, electrolytic methods successfully address the ultrahigh-purity niche grade demand. Moreover, innovations like digitized powder passports and AI-enhanced inline sensors are transforming the landscape. These advancements facilitate real-time monitoring of particle distribution, leading to a notable decrease in batch reject rates for both VIGA and plasma production lines.

Geography Analysis

In 2025, the Asia-Pacific region, buoyed by China's refining dominance and a 2024 uptick in powder metallurgy output, commanded 36.67% of global revenues, expanding at a robust 6.03% CAGR (2026-2031). South Korea's heightened aerospace spending spurred domestic demand for CoCr turbine disks. Concurrently, while plasma recycling pilots in Singapore and India's budding AM clusters offered a boost, both regions remained reliant on imported powder.

North America closely followed, leveraging expansive additive hubs and powder plants in pivotal states, both benefiting from the Inflation Reduction Act credits. Canada's MRO ecosystem and Mexico's tier-one automotive suppliers bolstered demand, yet both faced potential supply shocks from the DRC.

Europe enjoyed strong demand from the aerospace and medical sectors but contended with the continent's stringent regulations. Major suppliers established bases in Germany, the U.K., and France. However, challenges persist: the MDR CMR labeling threatens cobalt implant volumes, and the Critical Raw Materials Act emphasizes the urgency for on-continent refining. Yet, with Nordic hydrogen projects and offshore wind initiatives gaining traction, they could counterbalance potential orthopedic setbacks.

South America and the MEA regions contributed modestly. Brazil tapped into platform pipelines, and Saudi Arabia channeled Vision 2030 funds to bolster gas turbine capabilities. An export moratorium from the DRC, lifted in late 2025, underscored Africa's dependency on Asia for feedstock. This insight catalyzed swift expansions in Indonesian HPAL capacities, now achieving notable totals through strategic partnerships.

- AMETEK Inc.

- ATI

- Aubert and Duval

- CRS Holdings, LLC.

- Deloro Wear Solutions GmbH

- GKN Powder Metallurgy

- Hoganas AB

- Kennametal Inc.

- Linde Plc

- Metalysis

- OC Oerlikon Management AG

- Sandvik AB

- Sanyo Special Steel Co., Ltd.

- Shanghai HY Industry Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aerospace/medical high-performance needs

- 4.2.2 Wear and corrosion-resistant tooling demand

- 4.2.3 Hydrogen-turbine material requirements

- 4.2.4 Cold-spray repair adoption in MRO

- 4.2.5 AI-accelerated custom alloy design

- 4.3 Market Restraints

- 4.3.1 Environmental and ethical mining issues

- 4.3.2 EU critical-materials limits in implants

- 4.3.3 Emerging high-entropy alloy substitutes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Alloy Type

- 5.1.1 Cobalt-Chromium Alloys

- 5.1.2 Cobalt-Nickel Alloys

- 5.1.3 Cobalt-Iron Alloys

- 5.1.4 Cobalt-Molybdenum Alloys

- 5.1.5 Other Specialized Cobalt Alloys

- 5.2 By Production Method

- 5.2.1 Atomization (Gas, Water, Plasma)

- 5.2.2 Chemical Reduction

- 5.2.3 Electrolytic Methods

- 5.2.4 Mechanical Alloying

- 5.3 By Application

- 5.3.1 Additive Manufacturing/3D Printing

- 5.3.2 Aerospace Components

- 5.3.3 Medical Implants and Devices

- 5.3.4 Tooling and Wear Parts

- 5.3.5 Thermal Spray Coatings

- 5.3.6 Energy and Power Generation

- 5.3.7 Others (Automotive, Defense, Electronics)

- 5.4 By End-User Industry

- 5.4.1 Aerospace and Defense

- 5.4.2 Healthcare and Medical

- 5.4.3 Automotive and Transportation

- 5.4.4 Energy and Power

- 5.4.5 Manufacturing and Industrial Machinery

- 5.4.6 Electronics and Electricals

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AMETEK Inc.

- 6.4.2 ATI

- 6.4.3 Aubert and Duval

- 6.4.4 CRS Holdings, LLC.

- 6.4.5 Deloro Wear Solutions GmbH

- 6.4.6 GKN Powder Metallurgy

- 6.4.7 Hoganas AB

- 6.4.8 Kennametal Inc.

- 6.4.9 Linde Plc

- 6.4.10 Metalysis

- 6.4.11 OC Oerlikon Management AG

- 6.4.12 Sandvik AB

- 6.4.13 Sanyo Special Steel Co., Ltd.

- 6.4.14 Shanghai HY Industry Co., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment