|

시장보고서

상품코드

2062118

석탄계 활성탄 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Coal Based Activated Carbon - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

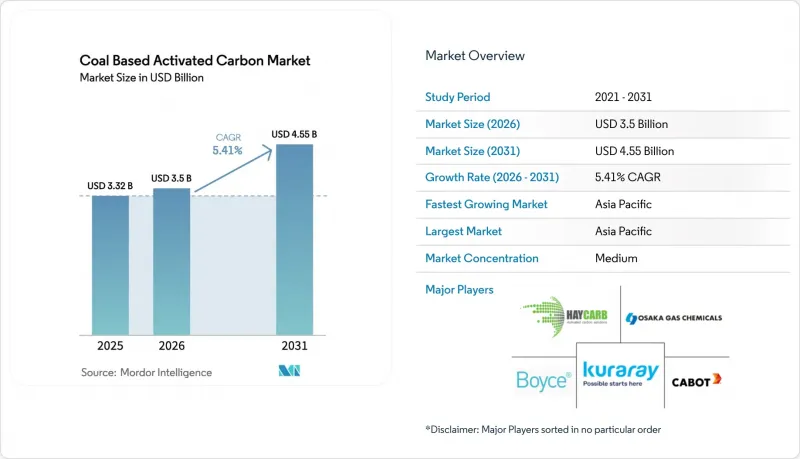

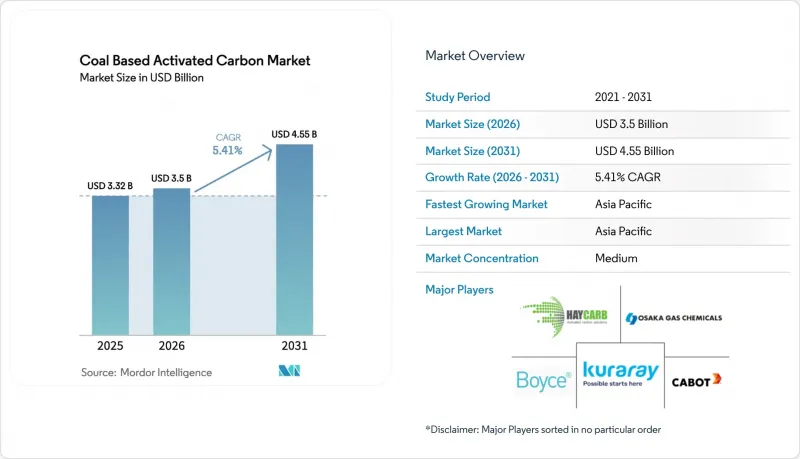

Mordor Intelligence에 의하면, 석탄계 활성탄 시장 규모는 2025년에 33억 2,000만 달러로 평가되었습니다. 2026년에 35억 달러에 달하고, 2031년까지 45억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR은 5.41%를 나타낼 전망입니다.

본 보고서는 제품 유형(분말, 입상, 압출·펠릿상, 비즈 및 펠트), 활성화 공정(증기, 이산화탄소, 인산, 염화아연), 용도(물 및 폐수, 공기·배가스, 식품 및 음료, 의약품, 광업, 기타), 지역(아시아태평양, 북미, 유럽, 기타)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 석탄계 활성탄 시장 동향 및 분석

배기가스 규제 강화가 배기가스 정화를 촉진

2024년, 미국의 MATS 규제와 중국의 초저배출 기준에 따라 발전소 및 시멘트 공장은 요오드수가 높은 분말 활성탄을 주입해야 할 의무가 있습니다. 내몽골과 산서성의 석탄 분지 인근에 위치한 공급업체들은 일반 석탄의 벤치마크 가격에 연동된 공급 계약을 확보하고 있으며, 이러한 움직임은 원자재 가격 변동 속에서도 매출총이익률을 안정시키는 역할을 하고 있습니다. EU에서는 바이오매스 유래 활성탄이 고가에 거래되고 있는 반면, 바이오매스 혼소 플랜트는 2026년 BAT(최적 이용 기술) 기준을 충족하기 위해 서둘러 대응을 추진하고 있으며, 그 결과 파일럿 플랜트용 수주가 급증하고 있습니다. 사업자가 가동 허가를 유지하기 위해 배기가스를 처리해야 하기 때문에 이러한 규제는 석탄 유래 활성탄 시장을 뒷받침하고 있습니다. 유황 혼입을 최소화하고 흡착 속도가 빠른 설비는 부하율이 변동하더라도 큰 이익을 얻을 수 있을 것으로 보입니다.

PFAS 대책에 따른 음용수 사업용 초미량 기준

2024년 4월, 미국 환경보호청(EPA)은 6가지 유형의 PFAS 화합물에 대해 최대 허용 농도(MCL)를 4ppt로 설정했습니다. 또한, 총 PFAS 농도가 100ppt 이하인 물을 처리하기 위한 ‘최적 가용 기술(BAT)’로 석탄 유래 입상 활성탄을 지정했습니다. 이에 따라, 미국 내 수백만 명의 주민에게 상수도를 공급하는 수도 유틸리티자는 사용 후 흡착제의 매립 처리에 따른 책임을 회피하기 위해 ‘테이크 오어 페이(take-or-pay)’ 방식의 재생 계약을 체결했습니다. 쿠라레는 2030년까지 미국 시장이 대폭 확대될 것으로 예측했습니다. 이 기회를 살리기 위해, 이 회사는 신규 생산 능력과 재생 능력을 모두 강화하여 해당 시장에서 큰 시장 점유율을 확보하는 것을 목표로 삼았습니다. 한편, 인도는 EU 기준에 부합하는 PFAS 규제안을 제시하며 남아시아 지역 수요 증가를 시사했습니다. 이러한 동향에 따라 석탄계 활성탄 시장은 서비스 중심의 수익 모델로 전환되고 있으며, 수직 통합형 공급업체에게 유리한 상황이 되고 있습니다.

석탄 원료의 가격 변동과 물류 리스크

2024년, 해상 석탄 가격의 분기별 변동은 기상 조건, 인도네시아의 수출 할당량, 중국의 수입 정책 등의 요인에 의해 영향을 받았습니다. 수입에 크게 의존하고 있는 유럽의 생산자들은 운임 급등으로 인해 석탄의 하역 비용이 대폭 상승하고 있습니다. 단기 조달 계약에 묶여 있는 소규모 생산자들은 원자재 가격의 급등이 계약상의 재가격 책정 폭을 상회함에 따라 이익률 압박에 직면해 있습니다. 반면, 산시성에 자사 광산을 보유한 생산자나 미국 일리노이 분지에서 장기 공급 계약을 체결한 생산자는 현물 가격으로 구매하는 생산자보다 높은 EBITDA 마진을 누리고 있습니다. 한편, 세정 플랜트에서 생산되는 석탄 미분의 품질 향상을 위한 노력 덕분에 요오드수가 제한된 범위 내에 있는 활성탄이 생산되게 되었으나, 이러한 제약으로 인해 그 용도는 부가가치가 낮은 염료 제거 시장으로 한정되어, 석탄계 활성탄 부문의 잠재적 가능성이 훼손되고 있습니다.

부문별 분석

2025년, 시장에서 입상 활성탄이 41.12%라는 압도적인 점유율을 차지했습니다. 그러나 예측에 따르면, 2026-2031년의 예측 기간 동안 압출 성형 및 펠릿 형태의 제품 모두 연평균 성장률(CAGR) 5.89%라는 강력한 성장세를 보이며, 다른 모든 부문을 앞지르는 기세로 확대될 전망입니다. 화학 및 정제 부문에서 에너지 집약적인 VOC 스크러버의 경우 압출 펠릿으로의 전환이 진행되고 있습니다. 이러한 펠릿은 팬의 에너지 소비를 줄일 뿐만 아니라 운영비도 대폭 절감할 수 있기 때문에 사양이 원통형 매체로 전환되는 추세가 나타나고 있습니다.

오사카 가스 케미컬은 새로운 프레스 설비를 가동함으로써 일본의 석탄계 활성탄 시장을 강화했습니다. 이에 더해, BET 비표면적을 향상시키는 바인더 기술의 발전도 맞물려, 압출 성형 제품의 꾸준한 성장이 촉진되고 있습니다. 분말 형태는 비상시 수질 정화나 의약품 정제에서 중요한 역할을 하고 있으며, 비드나 펠트와 같은 파생 제품은 의료기기의 틈새 용도에 대응하고 있습니다. 그러나 1만 톤 규모의 생산 라인에는 막대한 설비 투자가 필요하기 때문에 압출 성형은 재무 기반이 탄탄한 기업으로 한정되어 있으며, 그 결과 석탄계 활성탄 시장의 이 부문에서는 중간 정도의 집중도가 나타납니다.

지역별 분석

2025년, 아시아태평양은 세계 시장을 장악하며 세계 시장의 43.22%라는 상당한 점유율을 차지했을 뿐만 아니라, 2026년부터 2031년까지의 예측 기간 동안 5.96%라는 견실한 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 중국은 주요 생산국인 한편, 수입으로 전환하여 평균 수출 가격을 크게 상회하는 가격으로 고품질 제품을 조달했습니다. 이러한 추세는 석탄계 활성탄 시장에서 특수 등급 제품에 대한 수요와 시장의 견조함을 여실히 보여주었습니다. 인도에서는 생산 수준에 더해, 안드라프라데시 주와 오디샤 주에서 물류 비용이 절감됨에 따라 지역별 자급률 향상의 길이 열렸습니다. 한편, 필리핀은 혼합 원료의 비용 면에서의 이점을 부각시켜 일본과 한국의 바이어들에게 매력적인 선택지가 되었습니다.

북미, 특히 미국은 2025년 수요 동향에서 매우 중요한 역할을 했습니다. 이는 주로 재생 에너지 계약을 촉진하는 엄격한 PFAS 규제와 수은 배출 제한의 영향 때문입니다. 캐나다의 오일샌드 관련 수처리 공정과 멕시코의 호황을 누리고 있는 식품 가공 산업이 지역 동향을 더욱 다채롭게 만들었습니다. 유럽은 큰 시장 점유율을 유지하고 있지만, 석탄 가격 급등과 ESG 관련 자금 조달 압박과 같은 과제에 직면했습니다. 이러한 요인들로 인해 생산자들은 재생 가마로 전환할 수밖에 없게 되었으며, 그 동력원으로 재생에너지의 이용이 확대되었습니다. 남미에서는 페루와 칠레의 금 생산에 힘입어 시장이 꾸준한 성장세를 보였습니다. 중동 및 아프리카는 세계 시장 점유율은 다소 낮지만, 해수 담수화의 전처리 및 서아프리카의 금 프로젝트 분야에서 틈새 시장을 개척했습니다. 이러한 지역별 복잡한 동향이 맞물리면서, 석탄계 활성탄 시장에 있어 균형 잡힌 세계 성장 궤도를 형성했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the coal-Based activated carbon market size is projected to be USD 3.32 billion in 2025, USD 3.5 billion in 2026, and reach USD 4.55 billion by 2031, growing at a CAGR of 5.41% from 2026 to 2031.

This report is Segmented by Product Type (Powdered, Granular, Extruded/Pelletized, and Bead and Felt), Activation Process (Steam, Carbon Dioxide, Phosphoric Acid, and Zinc Chloride), Application (Water/Wastewater, Air/Flue-Gas, Food/Beverage, Pharmaceutical, Mining, and Other), and Geography (Asia-Pacific, North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Coal Based Activated Carbon Market Trends and Insights

Stricter Air-Emission Norms Boosting Flue-Gas Purification

In 2024, the U.S. MATS rule and China's ultra-low-emission standards mandate power and cement plants to inject high-iodine-number powdered activated carbon. Suppliers near the Inner Mongolia and Shanxi coal basins are securing supply contracts tied to the thermal-coal benchmarks, a move that stabilizes gross margins amid feedstock fluctuations. In the EU, while biomass-based carbons command a premium, biomass co-firing plants are racing to meet the 2026 BAT conclusions, resulting in a surge in pilot orders. These regulations bolster the coal-based activated carbon market, as operators treat flue gas to maintain their operational licenses. Facilities that ensure minimal sulfur bleed-through and rapid adsorption kinetics stand to gain significantly, even with fluctuating load factors.

PFAS-Driven Ultra-Trace Standards for Potable-Water Utilities

In April 2024, the EPA set Maximum Contaminant Levels for six PFAS compounds at 4 ppt. They also identified coal-based granular activated carbon as the Best Available Technology for treating waters with total PFAS levels below 100 ppt. In response, utilities serving millions of U.S. residents entered into take-or-pay regeneration contracts, avoiding landfill liabilities for spent sorbent. Kuraray had anticipated the U.S. market opportunity to grow significantly by 2030. To capitalize, the company enhanced both virgin and reactivation capacities, aiming to secure a substantial share of that market. Meanwhile, India proposed a draft PFAS limit in line with EU Standards, signaling increased demand in South-Asia. These developments have driven the coal-based activated carbon market toward a service-oriented revenue model, favoring vertically integrated suppliers.

Price Volatility and Logistics Risk in Coal Feedstock

In 2024, quarterly fluctuations in seaborne coal prices were influenced by factors such as weather conditions, Indonesian export quotas, and Chinese import policies. European producers, who rely heavily on imports, are seeing a significant increase in their landed coal costs due to rising freight charges. Smaller producers, bound by short-term procurement contracts, are experiencing margin compression as spikes in feedstock prices outpace the repricing of their contracts. In contrast, producers with captive mines in Shanxi or long-term offtakes in the U.S. Illinois Basin are enjoying higher EBITDA margins than those buying at spot prices. While efforts to enhance coal fines from wash-plants have led to carbons with iodine numbers in a limited range, this constraint restricts their use to low-value dye-removal markets and diminishes their potential in the coal-based activated carbon sector.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Gold-Ore Cyanidation Recovery Circuits

- Adoption of Carbon-Capture Sorbents for Cement and Steel Kilns

- Competition from Biomass-Based Activated Carbon

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the market saw granulated activated carbon holding a dominant 41.12% share. However, projections indicate that during the forecast period of 2026-2031, both extruded and pelletized forms are poised to expand at a vigorous 5.89% CAGR, outpacing all other categories. Within the chemicals and refining sectors, energy-intensive VOC scrubbers are increasingly leaning towards extruded pellets. These pellets not only reduce fan energy consumption but also lead to substantial savings in operating expenses, prompting a shift in specifications toward cylindrical media.

Osaka Gas Chemicals has bolstered Japan's coal-based activated carbon market by activating new presses. This, combined with binder advancements that enhance BET surface areas, has fueled steady growth for extruded products. While powdered forms play a pivotal role in emergency water remediation and pharmaceutical purification, bead and felt derivatives cater to niche applications in medical devices. However, the high capital investment required for a 10,000-ton line confines extrusion to financially robust players, resulting in a moderate concentration within this segment of the coal-based activated carbon market.

Geography Analysis

In 2025, the Asia-Pacific region dominated the global stage, capturing a notable 43.22% share of the global market and charting a robust projected CAGR of 5.96% for the forecast period 2026-2031. China, while a significant producer, turned to imports, acquiring premium products at prices considerably above the average export rates. This trend highlighted the resilience and demand for specialty grades in the coal-based activated carbon market. In India, production levels, combined with reduced logistics costs in Andhra Pradesh and Odisha, paved the way for enhanced regional self-sufficiency. Meanwhile, the Philippines showcased the cost benefits of blended feedstock, making it an attractive proposition for buyers in Japan and South Korea.

North America, particularly the United States, played a pivotal role in the 2025 demand landscape, largely influenced by stringent PFAS regulations and mercury limits that leaned towards regeneration contracts. Canada's oil-sands water circuits and Mexico's vibrant food processing industry further enriched the regional dynamics. Europe, while holding a significant market share, faced challenges with rising coal prices and ESG capital pressures. These factors nudged producers to pivot towards reactivation kilns, increasingly powered by renewable energy. In South America, buoyed by gold outputs from Peru and Chile, the market witnessed steady growth. The Middle-East and Africa, though modest in their global share, carved out niches in desalination pre-treatment and gold projects in West Africa. These intricate regional dynamics collectively shaped a balanced global growth trajectory for the coal-based activated carbon market.

- Active Char Pvt. Ltd.

- Boyce Carbon Ltd

- Cabot Corporation

- Carbon Activated Corporation

- Carbotech

- Donau Carbon US LLC

- Eurocarb Products Limited

- Haycarb PLC

- Jacobi Carbons Group

- KURARAY CO., LTD.

- KUREHA CORPORATION

- Osaka Gas Chemicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter air-emission norms boosting flue-gas purification

- 4.2.2 PFAS-driven ultra-trace standards for potable-water utilities

- 4.2.3 Surge in gold-ore cyanidation recovery circuits

- 4.2.4 Adoption of carbon-capture sorbents for cement and steel kilns

- 4.2.5 Emergence of "regeneration-as-a-service" business models

- 4.3 Market Restraints

- 4.3.1 Price volatility and logistics risk in coal feedstock

- 4.3.2 Competition from biomass-based activated carbon

- 4.3.3 ESG-driven capital withdrawal from coal supply chains

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Powdered Activated Carbon (PAC)

- 5.1.2 Granular Activated Carbon (GAC)

- 5.1.3 Extruded/Pelletized Carbon Block

- 5.1.4 Bead and Felt Activated Carbon

- 5.2 By Activation Process

- 5.2.1 Steam Activation

- 5.2.2 Carbon Dioxide Activation

- 5.2.3 Phosphoric Acid

- 5.2.4 Zinc Chloride

- 5.3 By Application

- 5.3.1 Water and Wastewater Treatment

- 5.3.2 Air and Flue-Gas Purification

- 5.3.3 Food and Beverage Processing

- 5.3.4 Pharmaceutical and Medical Uses

- 5.3.5 Mining (Gold Recovery)

- 5.3.6 Other Applications (Industrial Solvent Recovery, Biogas and Hydrogen Purification, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Active Char Pvt. Ltd.

- 6.4.2 Boyce Carbon Ltd

- 6.4.3 Cabot Corporation

- 6.4.4 Carbon Activated Corporation

- 6.4.5 Carbotech

- 6.4.6 Donau Carbon US LLC

- 6.4.7 Eurocarb Products Limited

- 6.4.8 Haycarb PLC

- 6.4.9 Jacobi Carbons Group

- 6.4.10 KURARAY CO., LTD.

- 6.4.11 KUREHA CORPORATION

- 6.4.12 Osaka Gas Chemicals

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment