|

시장보고서

상품코드

2073095

탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Predictive Carbon Forecasting and Scenario Modeling Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

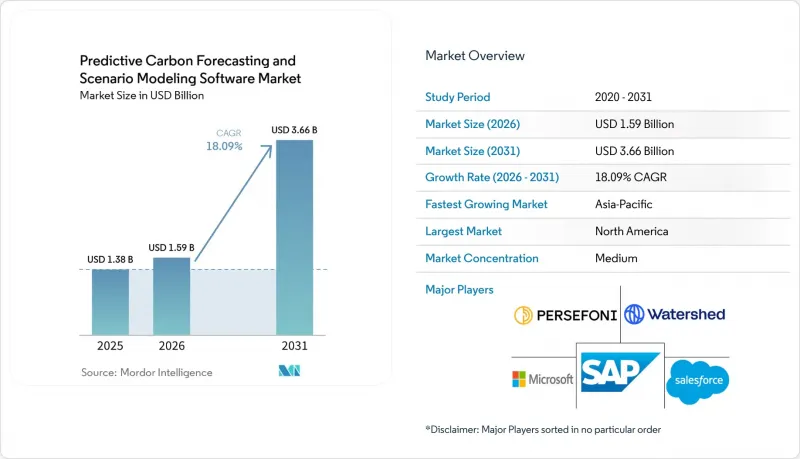

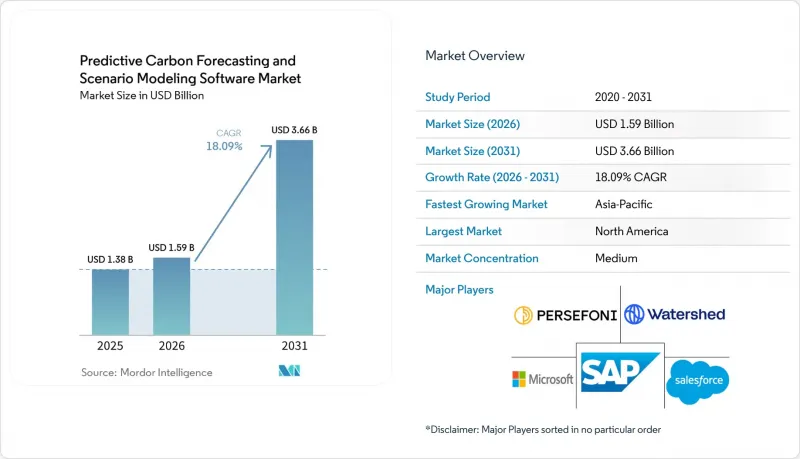

Mordor Intelligence에 의하면, 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장 규모는 2025년 13억 8,000만 달러, 2026년 15억 9,000만 달러에서 2031년까지 36억 6,000만 달러로 확대되어 2026-2031년까지 CAGR 18.09%를 나타낼 것으로 예측됩니다.

본 보고서는 제공 형태(소프트웨어 및 서비스), 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 용도(배출량 예측, 기타), 기업 규모(대기업 및 중소기업), 최종 사용자 산업(에너지 및 유틸리티, 은행, 금융서비스 및 보험(BFSI), 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장 동향과 인사이트

기후 변화 정보 공개 및 탄소중립 계획에 대한 규제 압력

공시 규정에 따라 기업들은 단순한 회계연도 말 보고에 그치지 않고, 계획 수립, 검증, 시나리오 검증을 지원하기 위해 탄소 데이터를 체계화해야 할 필요가 생겼기 때문에 규제상의 압력은 여전히 소프트웨어 수요를 촉진하는 가장 시급한 요인으로 남아 있습니다. IFRS 재단은 의사결정에 유용한 보고를 유지하면서 도입의 복잡성을 줄이기 위해, 2025년 12월에 IFRS S2에 따른 온실가스 공시 요건을 개정했습니다. 이로 인해 시장 전반에서 보고서에 대한 기대감이 변화하는 상황 속에서도 기업 수요가 지속되는 데 일조하고 있습니다. 미국에서는 2026년 5월 SEC가 기후 변화 공시 규정의 철회를 제안하면서 불확실성이 발생했으나, 많은 기업이 여전히 여러 보고 제도 하에서 사업을 영위하며 투자자의 기대에 부응해야 하기 때문에 의사결정에 직접적으로 기여하는 도구에 대한 광범위한 수요는 사라지지 않았습니다. 이는 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 시나리오 분석은 단순한 지속가능성 관련 규정 준수 업무로서뿐만 아니라, 재무 거버넌스의 일부로 다루어지고 있기 때문입니다. 따라서, 자사의 도구를 “계획 수립 인프라”로 자리매김하는 벤더는 주로 규정 준수 체크리스트에 의존하는 벤더보다 유리한 입장에 있습니다. 그 결과, 개별 규정이 개정되거나 연기되거나 이의 제기를 받는 경우에도 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장은 계속해서 규제의 혜택을 누리게 될 것입니다.

배출량 예측 및 감축 경로 최적화에 활용된 AI의 통합

AI는 카본 소프트웨어의 활용 방식을 혁신하고 있습니다. 이는 구매자들이 단일 워크플로우 내에서 더 신속한 데이터 정제, 더 빠른 시뮬레이션, 그리고 결과에 대한 보다 상호작용적인 해석을 기대하게 되었기 때문입니다. SAP는 2026년 5월, 자사의 ‘Footprint Optimization Agent”를 통해 시나리오 시뮬레이션 시간을 약 1일에서 20분으로 단축했다고 발표했습니다. 이는 소프트웨어 경쟁이 더 빠른 응답 시간과 더 높은 운영 편의성을 향해 나아가고 있음을 보여줍니다. 2026년 4월에 발표된 동료 심사를 거친 연구에서도, 에너지 집약형 산업의 탄소 배출량 예측에 있어 협업형 딥러닝 아키텍처가 기존 기준 기법보다 우수한 성능을 보인 것으로 밝혀졌으며, 이는 AI 기반 예측 모델로의 광범위한 전환을 뒷받침하고 있습니다. 이러한 변화에 따라, 해당 도구의 역할은 정적인 배출량 보고에서 능동적인 감축 경로 선정, 거래 수준 분석, 보다 신속한 의사결정 지원으로 확대되고 있습니다. 또한, 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장에서 제품 설계의 난이도도 높아지고 있습니다. 왜냐하면 구매자는 모델의 포괄성뿐만 아니라, 실용적인 해답에 도달하기까지 걸리는 시간도 비교하게 되기 때문입니다. AI를 기본적으로 통합하는 플랫폼이 늘어남에 따라, 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장에서는 기술적 깊이를 갖춘 벤더와 표면적인 보고 업무 자동화에 그치는 벤더 간에 더욱 뚜렷한 양극화가 진행될 것으로 보입니다.

스코프 3 및 공급업체 활동 데이터의 품질과 입수 가능성의 한계

공급업체 데이터의 품질은 여전히 가장 큰 운영상의 제약 요인으로 남아 있습니다. 이는 가장 중요한 배출 범주일수록 표준화가 미흡하고, 복잡한 밸류체인 전반에 걸쳐 검증하기가 가장 어려운 경우가 많기 때문입니다. 2025년 4월에 실시된 한 조사에 따르면, 79%의 조직이 공급업체 데이터의 가용성을 가장 큰 과제로 꼽았고, 62%는 내부 데이터의 품질을 주요 장애 요인으로 지적했는데, 이는 보고 체계의 성숙도 향상만으로는 입력 관련 문제가 해결되지 않았음을 보여줍니다. 한 조사에 따르면, 스코프 3 배출량이 기업 총 배출량의 75% 이상을 차지하는 경우가 많으며, 정확한 정량화를 가로막는 주요 장애 요인은 여전히 공급업체 데이터의 부족에 있다는 점이 지적되고 있습니다. 이러한 약점은 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장에 직접적인 영향을 미칩니다. 왜냐하면 모델의 신뢰성은 훈련, 매핑, 테스트에 사용되는 데이터의 신뢰성에 좌우되기 때문입니다. 기업은 여전히 지출 기반의 대체 지표나 추정 논리를 활용할 수 있지만, 투자자, 감사인 또는 조달 팀이 더 높은 정확도를 요구할 경우 이러한 방법의 신뢰성은 떨어지게 됩니다. 공급업체의 참여가 광범위하게 개선될 때까지, 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장은 중요한 의사결정 과정에서 모델의 산출 결과를 어느 정도까지 신뢰할 수 있는지에 대한 측면에서 계속해서 실질적인 한계에 직면할 것으로 보입니다.

부문별 분석

2025년 매출액 중 소프트웨어가 76.12%를 차지했으며, 이는 예측형 탄소 배출량 예측 및 시나리오 모델링 시장에서 라이선스 기반 플랫폼이 여전히 기업 지출의 중심을 이루고 있음을 보여줍니다. 구매자들은 프로젝트 주도형 자문 업무에만 의존하기보다는 보고, 계획, 위험 검토의 각 주기에서 반복적으로 활용할 수 있는 도구를 점점 더 선호하게 되었습니다. 이러한 추세는 많은 조직이 초기 범위 설정 단계를 이미 넘어, 탄소 분석을 일상적인 업무 프로세스에 통합하기 시작하고 있음을 보여줍니다. 이러한 상황에서 플랫폼 소유자가 중요한 이유는 지속적인 접근을 통해 업데이트를 신속하게 처리하고, 사내에서 폭넓게 활용하며, 가정 및 감사 증거에 대해 보다 일관된 거버넌스를 구현할 수 있기 때문입니다. 또한, 구독 수익을 모델링의 심도, AI 기능, 워크플로우 설계에 재투자할 수 있으므로, 벤더 입장에서는 제품 개선을 위한 보다 견고한 기반이 됩니다.

서비스 부문은 여전히 급속히 성장하고 있으며, 2031년까지 연평균 성장률(CAGR)은 21.54%를 나타낼 것으로 전망됩니다. 이는 소프트웨어만으로는 도입 지원, 시나리오 설계, 결과 해석과 같은 요구 사항을 충족시킬 수 없기 때문입니다. 많은 조직이 기본적인 배출량 데이터를 수집할 수는 있지만, 신뢰할 수 있는 배출 감축 경로를 구축하고, 약속에 대한 스트레스 테스트를 수행하며, 투자자나 감사인이 검토할 수 있는 자료를 작성하는 데에는 여전히 외부 지원이 필요합니다. 이는 서비스의 성장이 소프트웨어 도입이 미흡하다는 것을 나타내는 것이 아니라, 오히려 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장이 더욱 복잡한 이용 사례로 전환되고 있음을 의미합니다. 모델링이 전략에서 점점 더 중요해짐에 따라, 구매자들은 모델 설정 및 거버넌스와 관련된 전문가의 지원에 대해 더욱 적극적으로 비용을 지불하고 있습니다. 시간이 지남에 따라 소프트웨어가 기반이 되고, 더 깊은 도입을 배경으로 서비스가 부가적인 층으로 성장하는 상호 연관된 수익 모델이 형성됩니다. 따라서 예측형 탄소 배출 예측 및 시나리오 모델링 소프트웨어 시장은 두 모델 중 하나를 선택하는 방식이 아니라, 성숙한 소프트웨어의 핵심과 확대되는 자문 기능을 특징으로 하고 있습니다.

2025년에는 클라우드 기반 도입이 매출의 65.13%를 차지했습니다. 이는 대량의 데이터를 처리하고, 정기적인 업데이트에 대응하며, 서로 다른 사업 부문에 걸친 시나리오 테스트를 가능하게 하는 유연한 플랫폼에 대한 기업 수요를 반영한 것입니다. 예측적 탄소 예측 및 시나리오 모델링 소프트웨어 시장에서 클라우드 도입은 인프라 관련 마찰을 줄여주고, 전 세계 사업 활동 전반에 걸친 배출량 데이터, 시나리오 라이브러리 및 사용자 접근을 통합할 수 있게 해줍니다. 또한, 규칙, 채널, 공시 요건이 변경되었을 때 제품 업데이트를 신속하게 진행할 수 있도록 지원합니다. 이는 가설의 진화나 기업이 스코프 3의 적용 범위를 확대함에 따라 모델을 업데이트해야 하는 이 범주에서 중요한 점입니다. 또한, 클라우드 아키텍처는 벤더가 더 큰 컴퓨팅 성능과 공유 모델 환경이 필요한 분석 기능을 제공하도록 지원합니다.

클라우드 기반 도입은 2031년까지 연평균 성장률(CAGR) 20.92%로 확대될 것으로 예측되며, 이는 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장에서 가장 큰 모델이 여전히 가장 빠르게 성장하고 있음을 보여줍니다. 2026년 5월, 한 벤더는 데이터 수집 부담을 줄이면서도 몇 주 이내에 감사에 대응할 수 있는 기준을 제공하도록 설계된 클라우드 네이티브 플랫폼을 발표했습니다. 이는 구매자들이 클라우드 모델을 설정 시간 단축 및 운영 부담 경감과 연관 짓는 이유를 뒷받침해 줍니다. 엄격한 관리가 필요한 기관의 경우, On-Premise 환경은 여전히 중요하며, 데이터 보관 장소나 계약상 기밀성이 우려되는 상황에서는 하이브리드 모델이 계속해서 유용하게 활용되고 있습니다. 신속한 도입, 공유 액세스, 손쉬운 확장성 등의 장점은 On-Premise 환경에서는 좀처럼 실현하기 어렵기 때문에 신규 도입 시에는 여전히 클라우드가 선호되고 있습니다. 이러한 추세에 따라 클라우드 공급업체들은 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장 내에서 사업 영역을 확대할 여지가 더욱 넓어지고 있습니다. 또한, 이는 비정기적인 배치 분석이 아닌, 지속적인 데이터 수집과 빈번한 시나리오 반복을 전제로 한 제품 설계를 촉진하는 결과로 이어지고 있습니다.

지역별 분석

2025년, 북미는 매출의 35.12%를 차지하며, 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장에서 가장 규모가 큰 지역적 기여 요인이 되었습니다. 이 지역은 상장 기업이 밀집해 있는 기반, 성숙한 소프트웨어 조달 관행, 엔터프라이즈 플랫폼 공급업체의 집중이라는 강점을 갖추고 있습니다. 또한, 투자자 생태계가 잘 갖춰져 있어, 성숙도가 낮은 기업 소프트웨어 시장에 비해 기후 변화 관련 보고 및 계획에 대한 논의가 이사회나 재무 부서에서 더 조기에 이루어지는 경향이 있습니다. 미국은 많은 대기업들이 이미 공시 절차와 내부 통제를 갖추고 있으며, 이를 탄소 계획의 업무 흐름에 확대 적용할 수 있기 때문에 계속해서 주요 수요 거점으로 자리매김했습니다. 이로 인해 연방 정부의 정책 환경의 일관성이 떨어졌음에도 불구하고, 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장은 북미에서 견고한 사업 기반을 구축할 수 있었습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 22.91%를 나타낼 것으로 예측되며, 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장에서 가장 빠르게 성장하는 지역 부문이 될 전망입니다. 공식적인 기후 정보 공개 요건으로의 광범위한 전환, 탈탄소화 투자 증가, 수출 지향적 생산 네트워크 전반에 걸친 공급업체 수준의 탄소 가시화에 대한 수요 증가가 이 지역의 성장을 뒷받침하고 있습니다. 2026년 4월, 중국과학원이 “Panshi Yuheng”탄소 회계 대규모 모델 v1.0을 공개한 것은 중요한 기술적 신호가 되었습니다. 이는 국내 탄소 모델링 인프라가 활발하게 개발되고 있음을 보여줍니다(NEA.GOV.CN). 이 점이 중요한 이유는 지역 내 도입이 단순히 수입된 규정 준수 체계에 의해서만 추진되는 것이 아니라, 현지 역량 강화 및 산업 정책의 목표에 의해서도 추진되기 때문입니다. 따라서 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장은 다국적 기업 수요와 현지 플랫폼 개발이라는 두 가지 측면을 통해 아시아태평양에서 성장할 여지가 있습니다.

유럽은 기후 거버넌스가 이미 많은 기업의 보고 및 리스크 관리 프로세스에 통합되어 있기 때문에 탄소 배출량 예측 및 시나리오 모델링 소프트웨어 시장에 있어 계속해서 견고한 기반을 제공합니다. 보고 절차가 간소화되어 규정 준수 부담이 일부 완화되더라도, 시나리오 분석은 기업이 중요한 기후 리스크를 어떻게 평가하고 장기 계획을 수립하는지와 밀접한 관련이 있습니다. 남미 시장 규모는 여전히 작지만, 수출 지향적인 부문과 금융 기관들이 보다 체계적인 탄소 계획 도구에 대한 선택적 수요를 창출하고 있습니다. 중동 및 아프리카는 여전히 초기 단계 시장이지만, 국영 에너지 기업, 국부 펀드, 상장 기업들이 보다 체계적인 기후 변화 전환 로드맵을 수립하고 있어 이에 대한 관심이 높아지고 있습니다. 이 지역 전체에서 예측형 탄소 배출 예측 및 시나리오 모델링 소프트웨어 시장은 구매자가 소프트웨어를 단순한 보고용 구매 품목으로만 취급하지 않고, 규정 준수 요구 사항과 실질적인 계획 수립의 가치를 연결할 수 있는 지역에서 가장 높은 성장 잠재력을 보일 것으로 예측됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.07According to Mordor Intelligence, the predictive carbon forecasting and scenario modeling software market size is projected to expand from USD 1.38 billion in 2025 and USD 1.59 billion in 2026 to USD 3.66 billion by 2031, registering a CAGR of 18.09% between 2026 and 2031.

This report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Emissions Forecasting, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Energy and Utilities, BFSI, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Predictive Carbon Forecasting and Scenario Modeling Software Market Trends and Insights

Regulatory Pressure on Climate Disclosures and Net-Zero Planning

Regulatory pressure remains the most immediate driver of software demand, as disclosure rules now require companies to organize carbon data to support planning, verification, and scenario testing rather than simple year-end reporting. The IFRS Foundation updated greenhouse gas disclosure requirements under IFRS S2 in December 2025 to reduce implementation complexity while preserving decision-useful reporting, helping sustain enterprise demand as reporting expectations evolved across market. The United States introduced uncertainty when the SEC proposed rescinding its climate disclosure rules in May 2026, but that did not remove the broader demand for decision-ready tools, as many companies still operate across multiple reporting regimes and face investor expectations. This matters for the predictive carbon forecasting and scenario modeling software market because scenario analysis is increasingly treated as part of financial governance, not only as a sustainability compliance task. Vendors that frame their tools as planning infrastructure are therefore better positioned than vendors that depend mainly on compliance checklists. The effect is that the predictive carbon forecasting and scenario modeling software market continues to benefit from regulation even when individual rules are revised, delayed, or challenged.

Integration of AI for Emissions Forecasting and Abatement Pathway Optimization

AI is reshaping how carbon software is used because buyers now expect faster data cleaning, quicker simulations, and more interactive interpretation of results within a single workflow. SAP stated in May 2026 that its Footprint Optimization Agent reduced scenario simulation time from around 1 day to 20 minutes, demonstrating how software competition is moving toward faster response times and greater operational usability. A peer-reviewed study published in April 2026 also found that coordinated deep-learning architectures outperformed traditional baseline methods for predicting carbon emissions in energy-intensive industries, supporting the broader move toward AI-driven forecasting models. That shift expands the role of these tools from static emissions reporting into active pathway selection, transaction-level analysis, and faster decision support. It also raises the bar for product design in the predictive carbon forecasting and scenario modeling software market, because buyers will compare not only model breadth but also the time needed to reach a usable answer. As more platforms embed AI natively, the predictive carbon forecasting and scenario modeling software market is likely to further separate between vendors with strong technical depth and those that only automate surface-level reporting tasks.

Limited Quality and Availability of Scope 3 and Supplier Activity Data

Supplier data quality remains the largest operating constraint, because the most material emissions categories are often the least standardized and the hardest to verify across complex value chains. In April 2025, one survey found that 79% of organizations identified supplier data availability as their top challenge, while 62% pointed to internal data quality as a major barrier, which shows that reporting maturity has not solved the input problem. Another study noted that Scope 3 emissions often account for more than 75% of a company's total emissions and that supplier data gaps remain the main obstacle to accurate quantification. That weakness directly affects the predictive carbon forecasting and scenario modeling software market because models can only be as credible as the data used to train, map, and test them. Companies can still use spend-based proxies and estimation logic, but those methods weaken confidence when investors, auditors, or procurement teams need greater precision. Until supplier participation improves at scale, the predictive carbon forecasting and scenario modeling software market will continue to face a practical ceiling on how far model outputs can be trusted in high-stakes decisions.

Other drivers and restraints analyzed in the detailed report include:

- Rising Enterprise Demand for Forward-Looking Carbon Scenario Planning

- Expansion of ESG-Linked Capital Allocation and Board-Level Climate Governance

- High Integration Complexity With ERP, EHS, and Data-Lake Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 76.12% of revenue in 2025, indicating that licensed platforms remained the center of enterprise spending in the predictive carbon forecasting and scenario modeling market. Buyers increasingly favored tools they could use repeatedly across reporting, planning, and risk review cycles rather than relying solely on project-led advisory work. This pattern also indicates that many organizations had already moved past early scoping exercises and started embedding carbon analysis into routine operating processes. In that setting, platform ownership matters because recurring access enables faster updates, broader internal use, and more consistent governance of assumptions and audit trails. It also gives vendors a stronger basis for product improvement because subscription revenue can be reinvested in modeling depth, AI functionality, and workflow design.

Services are still expanding faster, with a projected CAGR of 21.54% through 2031, because software alone does not remove the need for implementation support, scenario design, and interpretation of results. Many organizations can collect basic emissions data, but they still need external help to build credible abatement pathways, stress-test commitments, and prepare outputs for investor or auditor review. This means service growth is not a sign of weak software adoption, but rather that the predictive carbon forecasting and scenario modeling software market is moving into more complex use cases. As modeling becomes more material to strategy, buyers are more willing to pay for expert support around model setup and governance. Over time, this creates a linked revenue pattern in which software remains the anchor and services grow as an attached layer around deeper adoption. The predictive carbon forecasting and scenario modeling software market, therefore, shows a mature software core with a growing advisory edge, rather than a choice between the 2 models.

Cloud-based deployment accounted for 65.13% of revenue in 2025, reflecting enterprise demand for flexible platforms that can handle large data volumes, support regular updates, and enable scenario testing across different business units. In the predictive carbon forecasting and scenario modeling software market, cloud deployment reduces infrastructure friction and enables centralization of emissions data, scenario libraries, and user access across global operations. It also supports faster product updates when rules, pathways, and disclosure requirements change. That is important in a category where models must be refreshed as assumptions evolve and as companies widen their Scope 3 coverage. Cloud architecture further helps vendors deliver analytics features that require greater computing capacity and shared model environments.

Cloud-based deployment is projected to expand at a 20.92% CAGR through 2031, indicating that the largest model remains the fastest-growing in the predictive carbon forecasting and scenario modeling software market. In May 2026, one vendor introduced a cloud-native platform designed to deliver an audit-ready baseline within weeks while reducing data-collection effort, underscoring why buyers associate cloud models with faster setup and lower operating drag. On-premise environments still matter for institutions with strict control needs, and hybrid models remain useful where data residency or contractual sensitivity is a concern. Even so, new deployments continue to favor the cloud because the value of faster onboarding, shared access, and easier scaling is hard to match through local infrastructure. This dynamic gives cloud vendors more room to widen their reach inside the predictive carbon forecasting and scenario modeling software market. It also encourages product design that assumes continuous data ingestion and frequent scenario iteration rather than infrequent batch analysis.

Complete Report Scope:

- By offering

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

- By Application

- Emissions Forecasting

- Climate Scenario and Pathway Modeling

- Climate and Transition Risk Assessment

- Decarbonization Planning and Abatement Optimization

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End User Industry

- BFSI

- Energy and Utilities

- Oil and Gas

- Manufacturing and Industrial

- Transportation and Logistics

- Technology and Telecommunications

- Retail and Consumer Goods

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America accounted for 35.12% of revenue in 2025, making it the largest regional contributor to the predictive carbon forecasting and scenario modeling software market. The region benefits from a dense base of listed companies, mature software procurement practices, and a strong concentration of enterprise platform vendors. It also has a deep investor ecosystem that tends to push climate reporting and planning issues into board and finance discussions sooner than in less mature enterprise software markets. The United States remained the main demand center because many large companies already had disclosure processes and internal controls that could be extended into carbon planning workflows. This gave the predictive carbon forecasting and scenario modeling software market a strong commercial base in North America, even as the federal policy environment became less consistent.

Asia-Pacific is projected to expand at a 22.91% CAGR through 2031, which makes it the fastest-growing regional segment in the predictive carbon forecasting and scenario modeling software market. A broader shift toward formal climate disclosure requirements, rising decarbonization investment, and the growing need for supplier-level carbon visibility across export-oriented production networks support growth in the region. China added an important technology signal in April 2026 when the Chinese Academy of Sciences released the Panshi Yuheng carbon accounting large model v1.0, showing active development of domestic carbon modeling infrastructure NEA.GOV.CN. That matters because regional adoption is not driven solely by imported compliance frameworks, but also by local capability-building and industrial policy goals. The predictive carbon forecasting and scenario modeling software market, therefore, has room to grow in Asia-Pacific through both multinational demand and local platform development.

Europe continues to provide a strong base for the predictive carbon forecasting and scenario modeling software market because climate governance is already embedded in many corporate reporting and risk management processes. Even where reporting simplification has reduced some compliance burden, scenario analysis remains closely tied to how enterprises frame material climate exposure and long-term planning. South America is still smaller, but export-oriented sectors and financial institutions are creating selective demand for more structured carbon planning tools. The Middle East and Africa remain early-stage markets, yet interest is rising as state energy companies, sovereign investors, and listed firms are building more formal climate transition roadmaps. Across these regions, the predictive carbon forecasting and scenario modeling software market is most likely to grow where buyers can connect compliance needs with practical planning value rather than treat software as a reporting-only purchase.

- Microsoft Corporation

- Salesforce, Inc.

- SAP SE

- IBM Corporation

- Oracle Corporation

- Persefoni AI, Inc.

- Watershed Technology, Inc.

- Sweep SAS

- Plan A Earth GmbH

- Greenly SAS

- Normative AB

- Sinai Technologies, Inc.

- Emitwise Ltd.

- Position Green AB

- Gaia Carbon Accounting Ltd.

- Sphera Solutions, Inc.

- Enablon North America Corp.

- Evercomm Singapore Pte. Ltd.

- Workiva Inc.

- Terrascope Pte. Ltd.

- VelocityEHS Holdings, Inc.

- ClimateView AB

- Intelex Technologies ULC

- CarbonChain Ltd.

- Accacia AI Solutions Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Pressure on Climate Disclosures and Net-Zero Planning

- 4.2.2 Rising Enterprise Demand for Forward-Looking Carbon Scenario Planning

- 4.2.3 Expansion of ESG-Linked Capital Allocation and Board-Level Climate Governance

- 4.2.4 Growing Adoption of Cloud-Based Sustainability Platforms in Large Enterprises

- 4.2.5 Integration of AI for Emissions Forecasting and Abatement Pathway Optimization

- 4.2.6 Need to Quantify Transition Risk Across Supplier, Asset, and Portfolio Decisions

- 4.3 Market Restraints

- 4.3.1 Limited Quality and Availability of Scope 3 and Supplier Activity Data

- 4.3.2 High Integration Complexity With ERP, EHS, and Data-Lake Environments

- 4.3.3 Budget Scrutiny and Slow ROI Realization for Mid-Market Buyers

- 4.3.4 Model Credibility Concerns From Assumption Sensitivity and Audit Scrutiny

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Emissions Forecasting

- 5.3.2 Climate Scenario and Pathway Modeling

- 5.3.3 Climate and Transition Risk Assessment

- 5.3.4 Decarbonization Planning and Abatement Optimization

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Energy and Utilities

- 5.5.3 Oil and Gas

- 5.5.4 Manufacturing and Industrial

- 5.5.5 Transportation and Logistics

- 5.5.6 Technology and Telecommunications

- 5.5.7 Retail and Consumer Goods

- 5.5.8 Other Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Salesforce, Inc.

- 6.4.3 SAP SE

- 6.4.4 IBM Corporation

- 6.4.5 Oracle Corporation

- 6.4.6 Persefoni AI, Inc.

- 6.4.7 Watershed Technology, Inc.

- 6.4.8 Sweep SAS

- 6.4.9 Plan A Earth GmbH

- 6.4.10 Greenly SAS

- 6.4.11 Normative AB

- 6.4.12 Sinai Technologies, Inc.

- 6.4.13 Emitwise Ltd.

- 6.4.14 Position Green AB

- 6.4.15 Gaia Carbon Accounting Ltd.

- 6.4.16 Sphera Solutions, Inc.

- 6.4.17 Enablon North America Corp.

- 6.4.18 Evercomm Singapore Pte. Ltd.

- 6.4.19 Workiva Inc.

- 6.4.20 Terrascope Pte. Ltd.

- 6.4.21 VelocityEHS Holdings, Inc.

- 6.4.22 ClimateView AB

- 6.4.23 Intelex Technologies ULC

- 6.4.24 CarbonChain Ltd.

- 6.4.25 Accacia AI Solutions Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment