|

시장보고서

상품코드

2062138

삼염화인 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Phosphorus Trichloride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

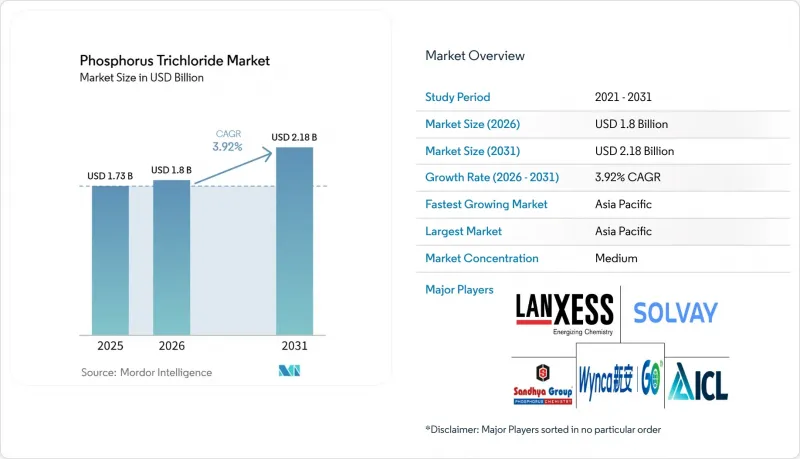

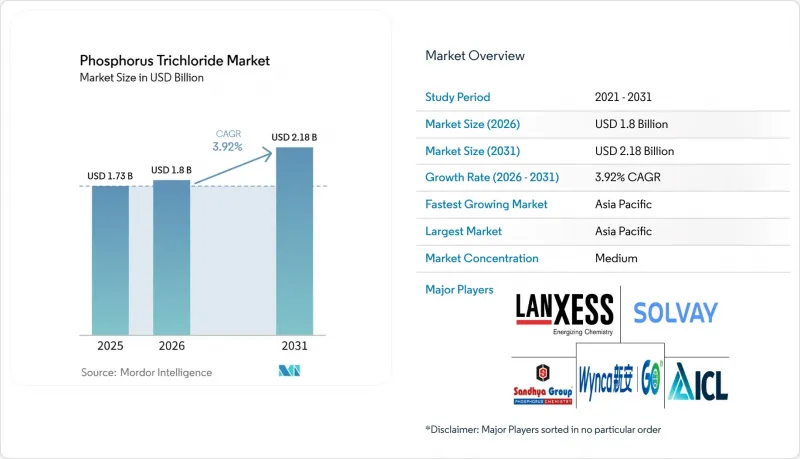

Mordor Intelligence에 의하면, 삼염화인 시장 규모는 2025년 17억 3,000만 달러로 평가되었습니다. 2026년 18억 달러에서 2031년까지 21억 8,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR은 3.92%를 나타낼 것으로 예측됩니다.

본 보고서는 순도/등급(기술 등급, 고순도 등급, 초고순도 전자 등급), 용도(농약, 의약품, 기타), 최종 사용자 산업(제약, 농업, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 삼염화인 시장 동향 및 분석

확대되는 의약품 중간체의 합성

엑셀 인더스트리즈 등 인도의 주요 수탁 제조 기업들은 유럽과 미국의 제약사들이 후기 단계의 API 합성을 비용 효율이 높고 감사를 마친 시설에 외주화함에 따라, 삼염화인 수요 증가에 대응하고 있습니다. 중국의 환경 규제로 인해 수익성이 낮은 생산 업체가 감소함에 따라, GMP(우수 제조 기준)를 준수하는 인도의 공장으로 수주가 이동하고 있습니다. 삼염화인은 온화한 염소화 공정에서 아실클로라이드와 알킬클로라이드를 제조할 때 여전히 선호되는 시약입니다. 엑셀 인더스트리즈의 로테 복합 시설에 신설된 생산 능력을 통해, 이 회사는 2028년까지 다단계 합성을 지원할 수 있는 체제를 구축함으로써, 중국 내 공급 차질 가능성에 직면한 상황에서도 유럽 및 미국 시장으로공급망 안정성을 확보하고 있습니다. 린 염소화가 필요한 저분자 의약품의 탄탄한 파이프라인이 중기적인 성장을 더욱 뒷받침하고 있습니다.

린계 난연제 사용 확대

규제 당국은 전자기기, 자동차, 건축자재에 사용되는 할로겐계 첨가물의 단계적 폐지를 추진하고 있으며, 이에 따라 각 OEM 업체들은 부식성 가스를 발생시키는 대신 탄화되는 인계 난연제의 채택을 강요받고 있습니다. 클라리언트가 2025년에 가동을 시작할 예정인 라산(레샨) 합작 공장에서는 얇은 두께의 배터리 모듈용 UL94 V-0 규격을 충족하는 2세대 Exolit 라인이 도입되었습니다. 마이크로캡슐화된 적린 덕분에 옅은 색상의 엔지니어링 폴리머를 제조할 수 있게 되어, 일본과 독일의 소비재 제조업체들에게 디자인 선택의 폭이 넓어지고 있습니다. 안전성이 높은 화학적 특성과 폭넓은 색조에 대한 적합성이 맞물려 평균 판매 가격이 상승하고 있으며, 연간 대체 성장률은 5%에 육박하고 있습니다. 가장 강력한 성장세는 아시아의 e-모빌리티 및 가전 부문에서 나타나고 있습니다.

중국 내 황인 원료의 불안정한 공급

황린 생산에는 1톤당 1만 4,000kWh의 전력이 필요하기 때문에 구이난성과 쓰촨성의 제련소는 수력 발전량 부족이나 환경 규제의 영향을 받기 쉽습니다. 2025년에는 현물 가격이 38% 변동하여 하류 부문의 이익률을 압박했습니다. 2026년은 4만 5,500톤공급 과잉으로 시작되었지만, 애널리스트들은 일시적인 가동 중단으로 인해 2027년까지 공급 과잉이 해소될 가능성이 있다고 예측했습니다. 중국 정부가 국내 사료 제조업체를 우선시하고 있기 때문에 유럽과 미국의 바이어들은 갑작스러운 수출 규제 위험에 직면해 있습니다. 2026년 2월 미국의 중요 광물 지정은 현지 원료 프로젝트를 장려함으로써 이러한 위험을 완화하는 것을 목적으로 하고 있습니다.

부문별 분석

2025년에는 기술·산업용 등급이 총 취급량의 대부분을 차지하여, 삼염화인 시장 점유율의 66.11%를 차지했습니다. 그러나 중국공급 과잉으로 가격 경쟁이 심화되었고, 부가가치세(VAT) 정책 변경으로 인해 평균 판매 가격이 전년 대비 6% 하락하는 등 이익률에 대한 압박이 뚜렷했습니다. 반면, 틈새 시장인 유기인 화합물 합성에 사용되는 고순도 제품 부문에서는 구매자들이 더 깨끗한 제품 특성에 대해 적정한 프리미엄을 수용함에 따라 가격이 안정세를 유지했습니다.

초고순도 전자 등급 제품은 범용 제품에 비해 300-500% 높은 가격 배율을 기록했습니다. 각 로트별 ppb 이하의 금속 함유량 및 입자 수에 대한 검증과 같은 엄격한 인증 요건이 진입 장벽이 되어, 신규 경쟁사 시장 진입을 가로막고 있습니다. 이 부문은 로직 노드가 3nm에서 2nm로 발전함에 따라 더욱 성장세를 보일 것으로 예측됩니다.

지역별 분석

2025년에는 중국의 원료 생산, 인도의 성장하는 제약 부문, 한국의 반도체 기술 발전에 힘입어 아시아태평양이 56.12%의 점유율로 시장을 독점했습니다. 해당 지역은 반도체 화학제품 생산에 대한 수십억 달러 규모의 인센티브와 지속적인 비료 수요에 힘입어, 2031년까지 연평균 성장률(CAGR) 5.11%를 기록하며 성장할 것으로 예측됩니다. 라슈트리야 케미컬즈나 콜로만델과 같은 인도 기업들은 후방 통합을 강화하고 수입 원료에 대한 의존도를 낮추기 위해 인산 생산 능력을 확대되고 있습니다.

북미에서는 배터리 재료 및 국내 반도체 제조를 촉진하는 정책에 힘입어 완만한 성장세가 나타나고 있습니다. 모자이크 사의 루이지애나주에서의 활동과 같은 프로젝트는 동맹국으로부터의 조달로 향하는 추세를 여실히 보여주고 있지만, 해당 지역에서는 여전히 대규모 황인 제련이 이루어지지 않고 있습니다.

유럽에서는 순환형 화학에 주력하고 있으며, 2029년까지 1만 톤의 회수 백린을 공급할 수 있을 것으로 전망됩니다. 이러한 노력은 엄격한 탄소 공시 요건을 준수하면서 공급의 회복탄력성을 높이는 것을 목표로 하고 있습니다.

남미, 중동 및 아프리카는 공급량과 용도의 다양성 측면에서 여전히 소규모 시장에 머물러 있습니다. 이집트와 요르단에서 진행 중인 메가 프로젝트는 비료 밸류체인을 대상으로 하고 있지만, 고부가가치 염소화 플랫폼과의 연계는 여전히 초기 단계에 머물러 있습니다. 브라질은 제초제 생산을 위해 삼염화인 수입을 계속하고 있으며, 아시아의 원료 공급망에 대한 의존도가 높다는 점이 부각되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the phosphorus trichloride market size is projected to expand from USD 1.73 billion in 2025 and USD 1.8 billion in 2026 to USD 2.18 billion by 2031, registering a CAGR of 3.92% between 2026 to 2031.

This report is Segmented by Purity/Grade (Technical/Industrial Grade, High-Purity Grade, and Ultra-High Purity Electronic Grade), Application (Agrochemicals, Pharmaceuticals, and More), End-User Industry (Pharmaceuticals, Agriculture, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Phosphorus Trichloride Market Trends and Insights

Expanding Pharmaceutical-Intermediate Synthesis

India's contract manufacturing leaders, such as Excel Industries, are addressing the growing demand for phosphorus trichloride as Western pharmaceutical companies outsource late-stage API synthesis to cost-effective, audited facilities. Environmental regulations in China have reduced the number of marginal producers, redirecting orders to Indian plants that comply with Good Manufacturing Practices. Phosphorus trichloride remains a preferred reagent for producing acyl chlorides and alkyl chlorides in mild chlorination processes. Excel's new capacity at its Lote complex positions the company to support multistep syntheses through 2028, ensuring supply chain stability for Western markets amid potential Chinese supply disruptions. A robust pipeline of small-molecule drugs requiring phosphorus chlorination further supports medium-term growth.

Growth in Phosphorus-Based Flame-Retardant Adoption

Regulators are phasing out halogenated additives in electronics, vehicles, and construction materials, prompting OEMs to adopt phosphorus-based flame retardants that char instead of emitting corrosive fumes. Clariant's joint-venture plant in Leshan, scheduled to open in 2025, utilizes second-generation Exolit lines that meet UL94 V-0 standards for thin-wall battery modules. Microencapsulated red phosphorus now enables pale-colored engineering polymers, expanding design options for consumer goods manufacturers in Japan and Germany. The combination of safer chemistry and broader color compatibility is increasing average selling prices, with annual substitution growth nearing 5%. The strongest momentum is observed in Asia's e-mobility and home-appliance sectors.

Volatile Yellow-Phosphorus Feedstock Supply in China

Yellow phosphorus production requires 14,000 kWh per ton, making smelters in Yunnan and Sichuan vulnerable to hydropower shortages and environmental restrictions. Spot prices fluctuated by 38% in 2025, compressing downstream margins. Although 2026 began with a 45,500-ton surplus, analysts predict temporary closures could reverse the surplus by 2027. Western buyers face risks of sudden export restrictions as Beijing prioritizes domestic formulators. The February 2026 U.S. critical-mineral designation aims to mitigate this risk by encouraging local feedstock projects.

Other drivers and restraints analyzed in the detailed report include:

- High-Purity Need for Semiconductor Wet-Etch Chemistries

- On-Site Chlorination and Circular-Chemistry Plants Reducing Logistics Cost

- Rising Adoption of Alternative Chlorinating Agents (SOCl2, POCl3)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Technical/industrial grade accounted for the majority of tonnage in 2025, capturing 66.11% of the phosphorus trichloride market share. However, margin pressures were evident as oversupply from China intensified price competition, leading to a 6% year-on-year decline in average selling prices due to changes in VAT policies. In contrast, the high-purity segment, catering to niche organophosphorus syntheses, maintained stable pricing as buyers accepted modest premiums for cleaner product profiles.

Ultra-high purity electronic grade commanded price multiples of 300-500% over commodity products. Stringent qualification requirements, such as sub-ppb metal and particle count verification for each batch, create significant entry barriers, discouraging new competitors. This segment is expected to gain further traction as logic nodes advance from 3 nm to 2 nm.

Geography Analysis

Asia-Pacific dominated the market in 2025 with a 56.12% share, driven by China's feedstock production, India's expanding pharmaceutical sector, and South Korea's semiconductor advancements. The region is expected to grow at a 5.11% CAGR through 2031, supported by multi-billion-dollar incentives for chip-chemical production and sustained fertilizer demand. Indian companies like Rashtriya Chemicals and Coromandel are expanding phosphoric acid capacity to enhance backward integration and reduce reliance on imported raw materials.

North America is experiencing moderate growth, supported by policies promoting battery materials and domestic chip fabrication. Projects like Mosaic's Louisiana initiative highlight a trend toward sourcing from allied nations, although large-scale yellow-phosphorus smelting remains absent in the region.

Europe is focusing on circular chemistry initiatives, which could supply 10,000 tons of recovered white phosphorus by 2029. These efforts aim to enhance supply resilience while adhering to stringent carbon disclosure requirements.

South America and the Middle-East and Africa remain smaller markets in terms of volume and application diversity. Mega-projects in Egypt and Jordan are targeting fertilizer value chains, but connections to higher-value chlorination platforms are still in early stages. Brazil continues to import phosphorus trichloride for herbicide production, highlighting its dependence on Asian feedstock cycles.

- Aditya Birla Chemicals

- Alpha Chemika

- BASF

- Bayer AG

- DONGYUE GROUP

- Excel Industries

- ICL

- Jinhe Industrial

- LANXESS

- Merck KGaA

- Otsuka Chemical Co. Ltd.

- SANDHYA GROUP

- Solvay

- Syngenta

- Taixing Shenlong Chemical Co., Ltd

- Wynca Group

- Xuzhou JianPing Chemical Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding pharmaceutical-intermediate synthesis

- 4.2.2 Growth in phosphorus-based flame-retardant adoption

- 4.2.3 High-purity need for semiconductor wet-etch chemistries

- 4.2.4 Emerging Li-ion battery electrolyte precursor demand (LiPF6 route)

- 4.2.5 On-site chlorination and circular-chemistry plants reducing logistics cost*

- 4.3 Market Restraints

- 4.3.1 Volatile yellow-phosphorus feedstock supply in China

- 4.3.2 Rising adoption of alternative chlorinating agents (SOCl2, POCl3)

- 4.3.3 Carbon-intensity scrutiny of chlor-phosphorus route*

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Purity/Grade

- 5.1.1 Technical/Industrial Grade (Greater than or equal to 99%)

- 5.1.2 High-Purity Grade (Greater than or equal to 99.9%)

- 5.1.3 Ultra-High Purity Electronic Grade (Greater than or equal to 99.999%)

- 5.2 By Application

- 5.2.1 Agrochemicals (Herbicides, Insecticides, etc.)

- 5.2.2 Pharmaceuticals

- 5.2.3 Plastic Additives and Stabilizers

- 5.2.4 Flame Retardants

- 5.2.5 Surfactants and Detergents

- 5.2.6 Metal and Water Treatment Chemicals

- 5.2.7 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Chemicals and Intermediates

- 5.3.2 Agriculture

- 5.3.3 Pharmaceuticals

- 5.3.4 Plastics and Polymers

- 5.3.5 Electronics and Semiconductors

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aditya Birla Chemicals

- 6.4.2 Alpha Chemika

- 6.4.3 BASF

- 6.4.4 Bayer AG

- 6.4.5 DONGYUE GROUP

- 6.4.6 Excel Industries

- 6.4.7 ICL

- 6.4.8 Jinhe Industrial

- 6.4.9 LANXESS

- 6.4.10 Merck KGaA

- 6.4.11 Otsuka Chemical Co. Ltd.

- 6.4.12 SANDHYA GROUP

- 6.4.13 Solvay

- 6.4.14 Syngenta

- 6.4.15 Taixing Shenlong Chemical Co., Ltd

- 6.4.16 Wynca Group

- 6.4.17 Xuzhou JianPing Chemical Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment