|

시장보고서

상품코드

2062155

화학 인디케이터 잉크 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Chemical Indicator Inks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

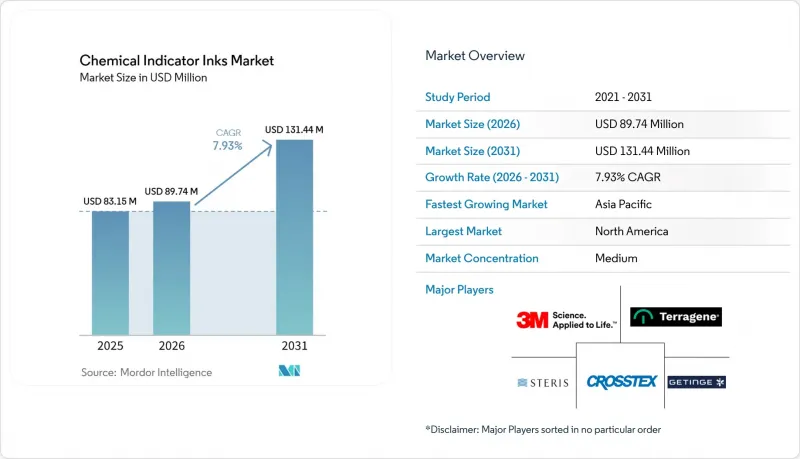

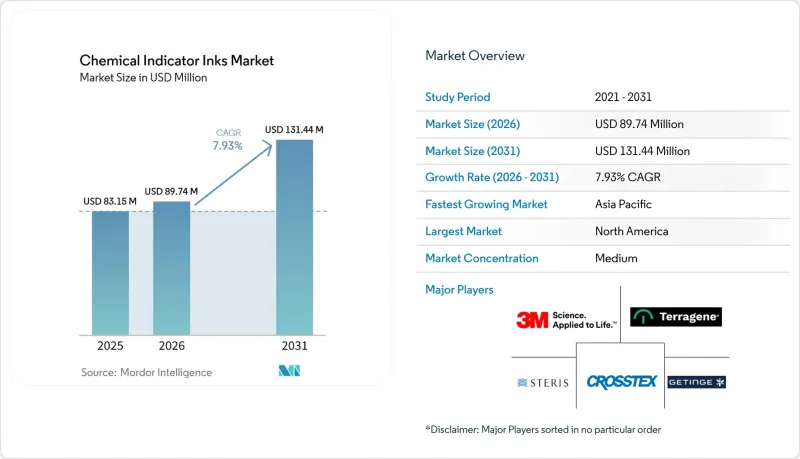

Mordor Intelligence에 의하면, 화학 인디케이터 잉크 시장 규모는 2025년에 8,315만 달러로 평가되었습니다. 2026년 8,974만 달러에서 2031년까지 1억 3,144만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.93%를 나타낼 전망입니다.

본 보고서는 유형별(수성 지시약 잉크, 기타), 공정별(증기 멸균 지시약, 기타), 용도별(포장, 라벨·태그, 기타), 최종 사용자 산업별(병원 및 클리닉, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 화학 인디케이터 잉크 시장 동향 및 분석

감염 관리 규제에 대한 인식 제고

규제 당국은 현재 규정 준수 문제를 해결하기 위해 단일 매개변수 스트립 대신 다중 매개변수 유형 4 지시약의 사용을 권장하고 있습니다. 2025년 3월, 미국 식품의약국(FDA)이 ANSI/AAMI ST58 : 2024를 승인함에 따라, 미국의 병원들은 시간, 온도, 멸균제 농도를 검증할 수 있는 추적 가능한 화학 지시약을 사용하여 각 멸균 주기를 기록해야 할 의무가 부과되었습니다. 2024년 7월과 2025년 7월에 실시된 조인트 커미션(Joint Commission)의 갱신 심사에서는 이러한 요건들이 인증 감사에 반영되어 제품 업그레이드가 요구되었습니다. 캐나다의 GUI-0074와 유럽의 EN 556-1 : 2024는 지역 규정을 ISO 11140에 부합하도록 조정하여, 해당 규정을 준수하는 시설의 수를 확대되고 있습니다. 이러한 규제 변경으로 인해 고성능 발색 시스템이 필수적인 사업 투자가 됨에 따라, 화학 인디케이터 잉크 시장의 성장이 촉진되고 있습니다.

외과 수술 및 외래 시술 건수 증가

외래 수술과 로봇 보조 수술은 입원 수술보다 훨씬 빠르게 증가하고 있으며, 이로 인해 증기 지시계에만 의존할 수 없는 저온 멸균기에 대한 수요가 늘어나고 있습니다. 2025년, 인튜이티브 서지컬은 다빈치 수술 건수가 약 315만 건에 달했다고 보고했으며, 이는 전년 대비 18% 증가한 수치로, 2026년에는 두 자릿수 성장이 예상됩니다. 미국 메디케어·메디케이드 서비스 센터(CMS)는 2026년에 573건의 새로운 외래 진료 코드를 도입했습니다. 이로 인해 집중적인 멸균 처리 부서를 갖추지 않은 경우가 많은 다수의 소규모 시설에 멸균 업무의 부담이 분산되게 됩니다. 각 신규 시설은 검증된 지시약을 상시 비치해야 할 의무가 있으며, 이를 통해 공급업체에 대한 안정적인 수요가 확보될 뿐만 아니라 화학 인디케이터 잉크 시장의 잠재력도 높아지고 있습니다.

저소득 지역에서의 낮은 시장 인지도

사하라 이남 아프리카의 수술 부위 감염률은 11.8%로, 고소득 국가의 1.9%에 비해 높은 수준입니다. 이 지역 내 많은 의료 기관들은 재정적 제약으로 인해 다중 지표 대신 단일 변수만을 모니터링하는 기본적인 클래스 1 스트립에 의존하고 있습니다. 기증 프로그램은 멸균 장치에 자금을 지원하는 경우가 많지만, 소모품은 지원 대상에서 제외되기 때문에 기술자들은 멸균 사이클 검증에 필요한 도구를 확보하지 못하는 상황에 처해 있습니다. 게다가 상당수의 직원이 국제표준화기구(ISO) 기준에 따른 지표 해석에 관한 정식 교육을 받지 않았습니다. 다자간 기구의 조달 지침에 화학 지표에 대한 자금 지원이 포함되지 않는 한, 이러한 지표의 도입은 여전히 고르지 못한 상태로 남아 있을 것으로 예측됩니다. 이러한 불균형은 해당 지역의 화학 인디케이터 잉크 시장 성장 잠재력에 영향을 미칠 수 있습니다.

부문별 분석

2025년, 수성은 유형별 부문의 47.12%를 차지했습니다. 이는 현대식 인쇄기와의 호환성 및 중국의 제14차 5개년 계획에서 정한 휘발성 유기 화합물(VOC) 제한 기준에 부합함을 반영한 것입니다. 병원과 의료기기 제조업체들이 자사의 탄소중립 목표에 맞추어 조달 방침을 조정하는 움직임이 가속화됨에 따라, 수성 화학 인디케이터 잉크 시장은 꾸준히 성장할 것으로 예측됩니다. 후지필름의 ‘AQUAFUZE’ 하이브리드 수성 자외선(UV) 잉크 시리즈나 선케미컬의 바이오 재생 가능 잉크 ‘SunCure Advance ECO’ 등공급업체들은 탄소 발자국을 줄이면서 성능을 향상시키고 있습니다.

제품 유형별로는 UV 경화형 시스템이 연평균 성장률(CAGR) 8.36%를 기록하며 시장에서 가장 높은 성장세를 보이고 있습니다. 이러한 성장은 에너지 비용을 최대 60% 절감하고, 대량의 라벨을 처리하는 위탁 멸균 업체의 처리 능력을 향상시키는 순간 경화 기술에 힘입어 이루어지고 있습니다. 산업계에서는 채용이 확대되고 있으며, 미마키와 같은 기업이 화학물질의 등록, 평가, 허가 및 제한(REACH) 규정을 준수한 ELH 잉크를 도입하고, 스타컬러가 저이동성 플렉소 인쇄용 잉크 세트를 제공하는 등, 모두 의약품 포장 부문에서 호평을 얻고 있습니다. 또한, 멸균 증명과 콜드체인의 시간·온도 반응을 결합한 듀얼 인디케이터 화학물질 개발에 뛰어난 공급업체는 프리미엄 시장 부문에 진출하여 화학 인디케이터 잉크 시장의 성장을 뒷받침할 수 있습니다.

2025년에는 공정형 인디케이터 매출액 중 증기 인디케이터가 36.98%를 차지했습니다. 이는 주로 전 세계 병원에서 오토클레이브가 광범위하게 사용되고 있기 때문입니다. 개정된 ANSI(미국국가표준협회)/AAMI(의료기기진보협회) ST58 : 2024 표준에서는 유형 4 내부 모니터의 사용이 의무화되었으며, 이로 인해 교체 수요가 증가하여 증기 인디케이터 시장 점유율을 뒷받침하고 있습니다.

플라즈마 및 기화 과산화수소 지시약 시장은 연평균 성장률(CAGR) 8.14%를 나타낼 것으로 전망됩니다. 이러한 성장은 로봇 기술의 발전, 열감응성 임플란트의 도입, 그리고 검증 절차를 간소화한 FDA(미국 식품의약국)의 2024년 카테고리 A 재분류에 기인한 것입니다. 게팅게(Getinge)사의 ‘Poladus 150’ 번들 및 메사 랩(Mesa Lab)사의 ‘ExpoSure’ 키트는 독자적인 잉크를 통해 고객을 유지하도록 설계된 장비 및 소모품 생태계를 보여주는 것으로, 주요 기술 공급업체들이 보유한 화학 인디케이터 잉크 시장 점유율 확대에 기여하고 있습니다.

지역별 분석

2025년, 북미는 매출의 37.88%를 차지했습니다. 미국 병원에서 ANSI/AAMI ST58 : 2024(미국국가표준협회/의료기기발전협회)를 도입한 데 더해, 제약 업계의 막대한 설비 투자가 수요를 뒷받침했습니다. 또한, 메디케어·메디케이드 서비스 센터(CMS)가 외래 시술에 대한 보상 범위를 확대함에 따라 고객 기반이 확대되었습니다. RFID(무선 주파수 식별) 검사 시스템의 도입은 대학병원에서 주요 통합 의료 네트워크(IDN)로 확대되면서, 화학 인디케이터 잉크 시장 입지를 강화하고 있습니다.

유럽에서는 EU MDR(유럽 연합 의료기기 규정) 감사, EN 556 : 2024 표준과의 조화, 수성 및 UV(자외선) 세트를 뒷받침하는 12%의 탄소 국경 조정 관세 도입이 호재로 작용하고 있습니다. 이산화티타늄(TiO2)에 대한 관세로 인해 안료 비용이 상승함에 따라, 각 컨버터 업체들은 장기 공급 계약 체결이나 후방 통합을 모색하고 있으며, 이에 따라 경쟁 구도가 재편되고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 2031년의 연평균 성장률(CAGR)은 8.32%로 예측됩니다. 인도가 2030년까지 200만 병상을 증설할 계획이며, 중국이 휘발성 유기화합물(VOC)을 30% 감축하도록 의무화하고 있는 점이, 수량 증가와 기술 전환을 모두 주도하고 있습니다. 아시아의 위탁 개발·제조 기관(CDMO) 및 병원에 대한 사모펀드 투자를 통해 검증된 지표에 대한 수요가 더욱 높아지면서, 화학 지표 잉크 시장의 성장이 가속화되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the chemical indicator inks market size was valued at USD 83.15 million in 2025 and is estimated to grow from USD 89.74 million in 2026 to reach USD 131.44 million by 2031, at a CAGR of 7.93% during the forecast period (2026-2031).

This report is Segmented by Type (Water-Based Indicator Inks and More), Process Type (Steam Sterilization Indicators and More), Application (Packaging, Labels and Tags, and More), End-User Industry (Hospitals and Clinics and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Chemical Indicator Inks Market Trends and Insights

Increased Awareness About Infection-Control Regulations

Regulators now recommend the use of multi-parameter Type 4 indicators instead of single-parameter strips, addressing a compliance gap. In March 2025, the U.S. Food and Drug Administration (FDA) recognition of ANSI/AAMI ST58:2024 requires U.S. hospitals to document each sterilization cycle with a traceable chemical indicator that verifies time, temperature, and sterilant concentration. Updates from the Joint Commission in July 2024 and July 2025 incorporate these requirements into accreditation audits, necessitating product upgrades. Canada's GUI-0074 and Europe's EN 556-1:2024 align regional regulations with ISO 11140, expanding the number of compliant facilities. These regulatory changes drive the growth of the chemical indicator inks market by making advanced chromogenic systems a necessary business investment.

Rising Surgical and Outpatient Procedure Volumes

Ambulatory and robotic-assisted surgeries are growing faster than inpatient procedures, driving the need for low-temperature sterilizers that cannot rely solely on steam indicators. In 2025, Intuitive Surgical reported approximately 3.15 million da Vinci procedures, reflecting an 18% year-over-year increase, with expectations of double-digit growth in 2026. The United States Centers for Medicare and Medicaid Services (CMS) introduced 573 new outpatient codes for 2026, distributing sterilization workloads across numerous smaller centers that often lack centralized sterile-processing departments. Each new site is required to stock validated indicators, ensuring consistent demand for suppliers and increasing the market potential for chemical indicator inks.

Limited Market Awareness in Low-Income Regions

Surgical-site infection rates in sub-Saharan Africa are 11.8%, compared to 1.9% in high-income countries. Many medical facilities in these regions, constrained by financial limitations, rely on basic Class 1 strips that monitor only a single variable instead of using multi-parameter indicators. Donor programs often fund sterilizers but exclude consumables, leaving technicians without the necessary tools to validate sterilization cycles. Additionally, a significant portion of staff lacks formal training in interpreting International Organization for Standardization (ISO)-compliant indicators. Without the inclusion of chemical-indicator funding in procurement guidelines by multilateral agencies, the adoption of these indicators is expected to remain inconsistent. This inconsistency could impact the growth potential of the chemical indicator inks market in these regions.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Validation Norms in Pharma and Med-Device Manufacturing

- RFID-Integrated Smart Indicator Labels for Asset Tracking

- Volatile Supply of Specialty Chromogenic Pigments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, water-based formulations accounted for 47.12% of the type segment, reflecting their compatibility with modern presses and compliance with volatile organic compound (VOC) limits outlined in China's 14th Five-Year Plan. As hospitals and medical device companies increasingly align their purchases with corporate net-zero objectives, the market for water-based chemical indicator inks is expected to grow steadily. Suppliers such as Fujifilm, with its AQUAFUZE hybrid water-based ultraviolet (UV) line, and Sun Chemical, with its bio-renewable SunCure Advance ECO, are improving performance while reducing carbon footprints.

Among the type segments, UV-curable systems are growing at a compound annual growth rate (CAGR) of 8.36%, the fastest in the market. This growth is driven by instant curing technology, which reduces energy costs by up to 60% and increases throughput for contract sterilizers handling high-volume labels. The industry is seeing increased adoption, with companies like Mimaki introducing Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH)-compliant ELH inks and StarColor offering low-migration flexographic (flexo) sets, both gaining traction in pharmaceutical packaging. Additionally, suppliers proficient in developing dual-indicator chemistries, combining sterilization proof with cold-chain time-temperature response, can access premium market segments and support the growth of the chemical indicator inks market.

In 2025, steam indicators accounted for 36.98% of the process-type revenue, primarily driven by the extensive use of hospital autoclaves worldwide. The updated ANSI (American National Standards Institute)/AAMI (Association for the Advancement of Medical Instrumentation) ST58:2024 standard requires Type 4 internal monitors, leading to increased replacement sales and supporting steam's market share.

Plasma and vaporized hydrogen peroxide indicators are projected to grow at a CAGR (Compound Annual Growth Rate) of 8.14%. This growth is attributed to advancements in robotics, the adoption of heat-sensitive implants, and the FDA's (Food and Drug Administration) 2024 Category A reclassification, which simplified validation processes. Getinge's Poladus 150 bundle and Mesa Labs' ExpoSure kits illustrate equipment-consumable ecosystems designed to retain customers through proprietary inks, contributing to the chemical indicator inks market share held by leading technology providers.

Geography Analysis

In 2025, North America accounted for 37.88% of the revenue. The adoption of ANSI/AAMI ST58:2024 (American National Standards Institute/Association for the Advancement of Medical Instrumentation) by hospitals in the United States, along with significant capital expenditures in the pharmaceutical industry, supported demand. Additionally, the Centers for Medicare & Medicaid Services (CMS) expanded reimbursement for outpatient procedures, increasing the customer base. RFID (Radio-Frequency Identification) trials are progressing from university hospitals to major Integrated Delivery Networks (IDNs), enhancing the market presence of chemical indicator inks.

Europe follows, driven by EU MDR (European Union Medical Device Regulation) audits, the harmonization of EN 556:2024, and the implementation of a 12% Carbon Border Adjustment tariff, which supports water-based and UV (ultraviolet) sets. Rising pigment costs due to duties on titanium dioxide (TiO2) are prompting converters to pursue long-term supply agreements or backward integration, reshaping the competitive landscape.

Asia-Pacific is the fastest-growing region, with an 8.32% CAGR (Compound Annual Growth Rate) projected through 2031. India's plan to add 2 million hospital beds by 2030 and China's 30% reduction mandate on volatile organic compounds (VOCs) are driving both volume growth and technology shifts. Private-equity investments in Asian Contract Development and Manufacturing Organizations (CDMOs) and hospitals are further increasing demand for validated indicators, accelerating the market expansion for chemical indicator inks.

- 3M

- Andersen Sterilizers

- Anpro

- Crosstex International, Inc.

- Ecolab

- Getinge AB

- GKE

- Inkmaker SRL

- LA-CO Industries

- McKesson Medical-Surgical Inc.

- Mesa Labs, Inc.

- NiGK Corporation

- PMS Healthcare Technologies

- Propper Manufacturing

- Raven Biological Laboratories

- STERIS

- Terragene

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased awareness about infection-control regulations

- 4.2.2 Rising surgical and outpatient procedure volumes

- 4.2.3 Stricter validation norms in pharma and med-device manufacturing

- 4.2.4 RFID-integrated smart indicator labels for asset tracking

- 4.2.5 Rapid adoption of on-pack smart inks for cold-chain biologics

- 4.3 Market Restraints

- 4.3.1 Limited market awareness in low-income regions

- 4.3.2 Volatile supply of specialty chromogenic pigments

- 4.3.3 Sustainability pressure on solvent-based ink carriers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Water-Based Indicator Inks

- 5.1.2 Solvent-Based Indicator Inks

- 5.1.3 UV-Curable Indicator Inks

- 5.1.4 Hybrid / Dual-Indicator Systems

- 5.2 By Process Type

- 5.2.1 Steam Sterilization Indicators

- 5.2.2 Ethylene Oxide (EO) Sterilization Indicators

- 5.2.3 Dry-Heat Sterilization Indicators

- 5.2.4 Plasma / H2O2 Gas Sterilization Indicators

- 5.2.5 Radiation (Gamma / E-Beam) Indicators

- 5.2.6 Formaldehyde Sterilization Indicators

- 5.3 By Application

- 5.3.1 Packaging (Bags, Wraps, Tapes)

- 5.3.2 Labels and Tags

- 5.3.3 Test Strips and Pouches

- 5.4 By End-user Industry

- 5.4.1 Hospitals and Clinics

- 5.4.2 Pharmaceutical and Medical-Device Firms

- 5.4.3 Diagnostic Laboratories

- 5.4.4 Contract Sterilization Service Providers

- 5.4.5 Research Institutes and Academia

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Andersen Sterilizers

- 6.4.3 Anpro

- 6.4.4 Crosstex International, Inc.

- 6.4.5 Ecolab

- 6.4.6 Getinge AB

- 6.4.7 GKE

- 6.4.8 Inkmaker SRL

- 6.4.9 LA-CO Industries

- 6.4.10 McKesson Medical-Surgical Inc.

- 6.4.11 Mesa Labs, Inc.

- 6.4.12 NiGK Corporation

- 6.4.13 PMS Healthcare Technologies

- 6.4.14 Propper Manufacturing

- 6.4.15 Raven Biological Laboratories

- 6.4.16 STERIS

- 6.4.17 Terragene

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment