|

시장보고서

상품코드

2062163

디지털 교육 출판 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Digital Education Publishing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

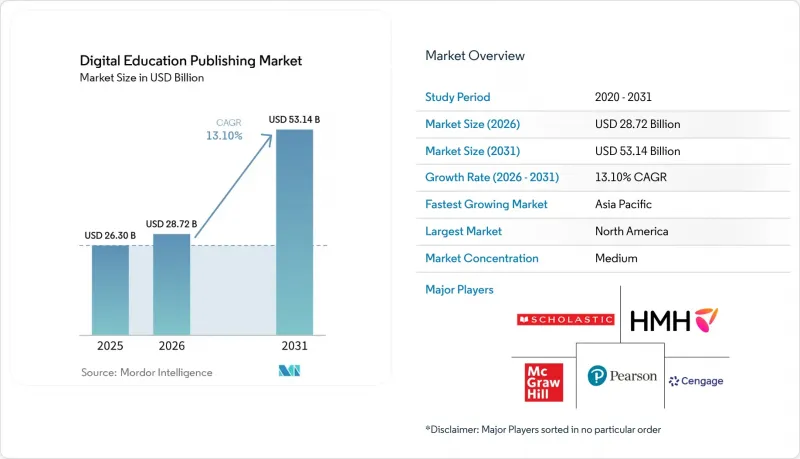

Mordor Intelligence에 의하면, 디지털 교육 출판 시장 규모는 2025년에 263억 달러로 평가되었고 2026년 287억 2,000만 달러에서 2031년까지 531억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 13.10%를 나타낼 전망입니다.

본 보고서는 컨텐츠 유형(디지털 교과서, 인터랙티브 코스웨어 등), 최종 사용자(K-12 교육 기관, 고등 교육 기관 등), 학습 형태(자기 주도형 학습, 강사 주도형 학습, 블렌디드/하이브리드형 학습 등) 등으로 분류되어 있습니다. 시장 전망은 입수 가능한 데이터를 바탕으로 금액(달러) 단위로 제시되어 있습니다.

세계 디지털 교육 출판 시장 동향과 인사이트

제도화된 하이브리드 학습의 조달 주기가 수년까지 수익원을 확보합니다.

학군 및 교육 시스템 차원에서 하이브리드 학습이 의무화됨에 따라, 지출은 3-5년 계약의 라이선스로 전환되고 있으며, 일회성 거래는 LMS 통합, 컨텐츠 접근성, 그리고 공급업체의 인증 획득 진행 상황에 연동된 갱신 계약으로 변화하고 있습니다. 미국 19개 주 및 워싱턴 D.C.에서 교과서 채택이 중앙 집중화되어 있는 지역에서는 공식적인 RFP(제안 요청서)를 통해 LTI 1.3, WCAG 2.2 및 섹션 508 준수가 ‘있으면 바람직한’ 속성에서 주 차원 승인 시 필수 요건으로 격상되었으며, 다년간의 채택 주기 동안 준수 업체에 보상을 제공함으로써 디지털 교육 출판 시장을 안정화하고 있습니다. 정부 플랫폼은 디지털 우선 컨텐츠를 더욱 중시하고 있으며, 전국 규모의 컨텐츠 배포를 지원하는 인도의 PM e-VIDYA와 DIKSHA가 그 대표적인 사례입니다. 정부 부처가 저장소 및 컨텐츠 메타데이터를 표준화하면, 출판사는 공공 워크플로우와 다국어 요구 사항에 맞추어 제품 로드맵을 조정합니다. 중국의 ‘AI+교육’ 행동 계획은 초등교육부터 고등교육까지를 아우르며, 2030년까지 모든 교육 과정에 AI를 통합하는 것을 목표로 하고 있습니다. 이에 따라, 성(省) 차원의 플랫폼과 연동 가능한 디지털 교재나 AI를 지원하는 현지화 컨텐츠에 대한 수요가 증가하고 있습니다. 유럽에서는 ‘디지털 교육 행동 계획’이 상호 운용성과 교원 역량 개발을 핵심 틀로 삼고 있으며, 컨텐츠 제공업체에 대해 표준화 참여 및 설계 단계부터 접근성을 고려한 제작 프로세스를 추진하고 있습니다. 이를 통해 국경을 초월한 프로그램에서 입지를 유지할 수 있게 되었으며, 디지털 교육 출판 시장 전체를 혁신할 가능성이 계속해서 열려 있습니다. 조달 과정에서 개별 타이틀보다 지속적인 통합이 더욱 중요시됨에 따라, 디지털 교육 출판 시장에서는 전환 비용이 증가하여 학군의 업무 흐름과 데이터 시스템에 깊이 뿌리내린 공급업체가 유리한 입지를 점하고 있습니다.

교육 과정에 따른 디지털 평가 의무화가 컨텐츠 개발의 경제 구조를 재편하고 있습니다.

형성 평가와 학습 진도 모니터링의 의무화로 인해, 출판사는 단순한 컨텐츠 제공업체에서 수업 계획 및 교실 차원의 지도 개입에 필요한 정보를 제공하는 지속적인 진단·분석 파트너로 그 역할을 전환하고 있습니다. 이 프레임워크의 효과는 교육부가 명확한 디지털 역량 목표를 제시할 때 가장 두드러집니다. EU의 정책 방향에서 볼 수 있듯이, 컴퓨터 및 정보 활용 능력 향상을 도모하는 동시에, 학교 간에 평가 결과를 호스팅하고 공유할 수 있는 상호 운용 가능한 플랫폼에 대한 투자를 유도함으로써 디지털 교육 출판 시장 수요 구조를 재편하고 있습니다. 중국의 ‘AI+교육’이라는 방향성은 다국어·다문자 체계에 걸친 컨텐츠 현지화 및 AI 지원형 평가에 대한 수요를 창출하고 있으며, 각 성의 스마트 플랫폼은 내장된 진단 기능을 활용해 학습 지연을 해소할 수 있는 대규모 사용자 기반에 서비스를 제공합니다. AI가 문제 작성을 가속화하고 있기는 하지만, 인간의 개입이 필요한 워크플로는 여전히 필수적입니다. 이는 AI를 활용한 시험 문제 생성에 관한 동료 심사 연구에 의해 입증되었으며, 해당 연구에서는 품질과 공정성을 확보하기 위한 전문가의 검토가 여전히 필요함에도 불구하고 확장성 또한 입증되었습니다. 그 결과, 컨텐츠, 평가, 분석은 개별 교과서 주기가 아닌 교육 기관의 라이선스에 연계된 지속적인 서비스로 통합되어, 디지털 교육 출판 시장의 지속적인 수익 창출을 강화하게 될 것입니다.

해적판과 취약한 DRM이 신흥 시장에서의 수익 확보를 저해하고 있습니다.

인터넷 연결이 불안정한 지역에서는 배포 방식 선택에 영향을 미칠 뿐만 아니라, 교재를 장기간 오프라인에서 이용할 수 있도록 해야 하는 경우 무단 재배포의 위험이 높아질 수 있습니다. 모바일 및 유선 광대역 요금이 합리적인 수준을 넘어선 시장에서는 사용자들이 캐시된 컨텐츠나 사이드로드된 컨텐츠에 의존하는 경향이 강해져 정보 유출 위험이 높아짐에 따라, 디지털 교육 출판 시장에서 프리미엄 타이틀의 투자 수익률(ROI) 산정이 복잡해지고 있습니다. 학교 네트워크 도입이 아직 초기 단계에 있는 지역에서는 지속적인 본인 확인이나 라이선스 검증이 제대로 이루어지지 않는 경우가 많으며, 이로 인해 클라우드 기반 DRM 검증 워크플로의 효율성이 떨어지게 되어 컨텐츠 제공업체는 간헐적인 연결 환경에 적합한 대체 관리 방안을 모색할 수밖에 없게 됩니다. 국가 플랫폼이 기초 교재에 대해 오픈 액세스를 기본 설정으로 채택할 경우, 출판사는 가치를 보호하기 위해 적응 기능이나 분석 기능과 같은 프리미엄 기능을 세분화하여 대응하게 되며, 이는 디지털 교육 출판 시장 전체의 제품 전략을 형성하게 됩니다. 이러한 환경에서는 지역별 연결 상황이나 학교의 단말기 정책에 맞춘 패키징 모델 및 배포 보호 조치에 대한 지속적인 수요가 유지될 것이며, 이는 DRM 아키텍처의 설계 철학을 변화시킬 가능성이 있습니다.

부문별 분석

2025년, 디지털 교과서는 디지털 교육 출판 시장 점유율의 44.36%를 차지했습니다. 이는 주별 도입 주기의 연속성과, 공식적인 조달 과정에서 핵심 교육 과정이 확고히 자리 잡은 역할을 반영한 것입니다. 교육 기관과 고용주들이 임상, 공학, 안전이 극히 중요한 환경을 모방한 체험형 학습을 요구함에 따라, 몰입형 및 시뮬레이션 기반 형식은 2031년까지 연평균 성장률(CAGR) 21.87%로 가장 빠르게 성장할 것으로 예상되며, 이는 디지털 교육 출판 시장의 범위를 확대되고 있습니다. 유럽의 국가 디지털 플랫폼 및 학교 네트워크에 대한 투자는 멀티미디어 중심의 교육 방식을 뒷받침하고 있습니다. 이로 인해 교과서만으로는 충족할 수 없는 컨텐츠 패키징 및 접근성에 대한 기준이 높아지면서, 출판사의 정적 컨텐츠와 인터랙티브 컨텐츠 포트폴리오의 균형에 영향을 미치고 있습니다. 디지털 교육 출판 업계에서는 역량 추적이나 포용적 접근과 같은 정책 목표에 부합할 수 있는 분석 지원형 자산도 우선시되고 있습니다. 이에 따라 맞춤형 컨텐츠와 평가 연계형 컨텐츠가 정규 교육의 혁신 전략의 핵심으로 자리 잡고 있습니다. 국가 저장소가 기초 교재를 제공하는 한편, 출판사들은 맞춤형 피드백, 진행 상황 대시보드, 안전한 시험 감독과 같은 프리미엄 기능에 주력하여 오픈 컨텐츠를 뛰어넘는 독자적인 강점을 구축하고, 디지털 교육 출판 시장 전반에서 교육 기관과의 계약을 유지하고 있습니다.

AI 기반 제작 도구가 개발 기간을 단축함에 따라, 상호작용형 학습 자료와 평가 자료의 도입은 계속해서 확대되고 있습니다. 동시에, 전문가의 감독 하에 진행된 AI 생성 시험 문제에 대한 동료 심사 연구에서 입증된 바와 같이, 인간의 검증은 심리측정적 품질을 유지하고 있습니다. 광대역 및 기기의 보급으로 인해 더욱 풍부한 형식이 가능해진 분야에서는 멀티미디어 컨텐츠의 도입이 확대되고 있습니다. 또한, 데이터 통합 파트너십을 통해 평가와 교육 과정을 연계하여, 교실 및 학군 차원의 학습 순서를 개별화하고 있습니다. 몰입형 및 시뮬레이션 컨텐츠의 디지털 교육 출판 시장은 2031년까지 연평균 성장률(CAGR) 21.87%로 확대될 것으로 전망됩니다. 이는 교육 기관들이 임베디드 과제와 분석을 통해 측정 가능한 시나리오 기반 학습을 도입하고 있기 때문입니다. 참고 자료 및 보충 컨텐츠 분야에서는 OER(개방형 교육 자원)과의 경쟁이 치열해지고 있으며, 이에 따라 공공 부문의 기대에 부응하는 유연성, 접근성, 그리고 학습 효과 입증과 같은 차별화된 요소가 요구되고 있습니다. 이러한 변화들이 맞물리면서, 디지털 교육 출판 시장 전반에서 포트폴리오가 정적인 PDF에서 새로운 기준과 정책 목표에 부합하는 평가 기능을 갖춘 동적인 모듈로 전환되고 있습니다.

2025년에는 K-12 및 고등교육 기관이 총 37.75%의 점유율을 차지했으나, 기업 및 전문직 학습자층은 조직이 목표로 삼은 역량 강화 및 인사 시스템 전반에서 추적 가능하고 검증 가능한 자격증에 자금을 투입함에 따라, 2031년까지 연평균 성장률(CAGR) 19.39%로 성장할 전망입니다. 기업 수요는 역량 진단, 지속적인 평가, 그리고 직원의 생산성을 높이는 역할 기반 컨텐츠 경로에 집중되어 있으며, 이는 디지털 교육 출판 시장의 더 큰 점유율을 구독형 배포 및 분석 기능과의 통합으로 이끌고 있습니다. 대학 관련 플랫폼 및 출판사들은 AI를 활용한 검색, 컨텐츠 발견 및 검증 기능을 교육 기관의 업무 흐름에 통합하기 위해 기술 제휴를 맺고 있으며, 이를 통해 디지털 교육 출판 시장 내에서 인증된 이용 및 인용에 대한 프리미엄 가격 책정이 유지되고 있습니다. 또한, 교육 기관의 구매자들이 데이터 보호 규정을 준수하면서 LMS 카탈로그에 통합 가능한 ‘설계 단계부터 접근성을 고려한’ 구성 요소를 요구함에 따라, 디지털 교육 출판 업계도 그 혜택을 누리고 있습니다. 이를 통해 사회의 기대에 부응하는 플랫폼의 신뢰성과 고객 지원에 대한 투자가 촉진될 것입니다. 시간이 지남에 따라 고용주들이 검증된 역량을 취업 준비도와 동등하게 여기게 됨에 따라, 성과 연계형 컨텐츠 및 자격증 네트워크가 경쟁 우위로 부상하고, 디지털 교육 출판 시장 전반에서 내재형 평가의 가치가 높아질 것입니다.

기술 및 직업 훈련 제공업체들은 실험실 접근성 확대, 네트워크 연결 강화, 교원 양성 확대라는 국가적 목표의 혜택을 누리고 있으며, 그 결과 디지털 교육 출판 시장에서 지역별 고용 경로에 부합하는 모듈식 및 축적 가능한 컨텐츠의 도입이 증가하고 있습니다. 기업용 프로그램의 경우, EU 및 기타 지역의 진화하는 표준화 동향을 반영하고, 해당 지역의 데이터에 대한 기대치를 저해하지 않으면서 사내 시스템과 통합되며, 역할 기반 분석을 지원하는 컨텐츠가 요구되고 있습니다. 한편, K-12 및 고등교육 부문에서는 일관된 평가, 교원 지도, 접근성 요건 준수가 여전히 최우선 과제로 꼽히고 있으며, 이로 인해 학군이나 캠퍼스 차원의 예산 변동이 있더라도 계약 갱신이 안정적으로 이루어지고 있습니다. 이러한 추세는 디지털 교육 출판 시장에서 역량 향상을 검증하고 다양한 사용자 유형에 걸친 규정 준수를 지원하는 풍부한 분석 기능을 갖춘 컨텐츠에 대한 지속적인 수요 기반을 보여주고 있습니다.

지역별 분석

북미는 2025년에 31.74%의 점유율을 차지했습니다. 이는 LMS 제공 및 분석 기능과 연계된 종합적 접근 라이선스를 중시하는 재정적 여유가 있는 K-12 학군 및 대학 프로그램의 지원을 바탕으로 한 것입니다. 미국 19개 주와 워싱턴 D.C.에서 교과서를 일원화하여 채택하는 것은 LTI 1.3, WCAG 2.2 및 섹션 508 준수의 중요성을 부각시키고 있습니다. 이것들은 디지털 교육 출판 시장 전체에서 제품 설계 및 입찰 자격의 기준이 되고 있습니다. 또한 교육 기관들은 여전히 접근성 도구 및 ID 관리와 연동되는 브라우저 기반 접근 방식을 선호하고 있으며, 이것이 웹 우선 포트폴리오를 뒷받침하고 있습니다. 동시에, 모바일 앱은 특정 이용 사례나 그동안 충분히 다루어지지 않았던 상황에 대응하고 있습니다. 이 지역에서 진단 및 분석 기능을 통합한 교육 과정으로의 전환은 디지털 교육 출판 시장 전반에서 학습 효과와 정책과의 부합성을 입증할 수 있는 업체들에게 지속적인 수익 모델을 강화해 줄 것입니다. 시간이 지남에 따라 이러한 기능들은 전환 비용을 높이며, 지도 및 평가 전반에 걸친 학군 데이터 흐름과의 통합 및 호환성이 입증된 공급업체에게 유리하게 작용합니다.

아시아태평양은 연결성, 기기, 스마트 교육 플랫폼에 대한 대규모 공공 투자의 뒷받침을 받아 2031년까지 연평균 성장률(CAGR) 15.99%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 지역입니다. 인도의 최근 예산 배분은 학교용 디지털 자원 및 인프라에 대한 지원을 지속하고 있으며, 그 결과 PM e-VIDYA나 DIKSHA와 같은 국가 차원의 이니셔티브에 부합하는 정부 시스템 내 플랫폼의 활용도와 교사들의 도입률이 증가하고 있습니다. 이를 통해 디지털 교육 출판 시장 전반에서 대규모 컨텐츠의 발굴과 유통이 촉진되고 있습니다. 중국의 ‘AI+교육’ 행동 계획은 2030년까지 AI 과정 보급에 관한 목표를 제시하고 있으며, 대규모 수강생을 수용할 수 있는 성(省) 차원의 플랫폼을 활용하여 디지털 교육 출판 시장에서 지역 특화 컨텐츠 및 평가 기능 개발을 가속화하고 있습니다. 아세안 시장에서는 인터넷 접속 환경과 통신 속도에 큰 편차가 나타납니다. 따라서 출판사는 대역폭의 현실에 맞추어 SKU를 조정하는 동시에, 각국의 프로그램이 디지털 경제로의 도약을 추진하는 가운데 성장에 대비해야 합니다. 국가 클라우드 및 데이터 소재지 관련 규제가 발전함에 따라, 공급업체들은 지역별 특성에 맞춘 호스팅 및 개인정보 보호 관행을 도입하고 있으며, 이를 통해 디지털 교육 출판 시장에서 공공 조달 및 교육 기관과의 장기적인 파트너십이 가능해졌습니다.

유럽에서는 EU 차원의 프로그램이 상호 운용 가능한 솔루션과 기술 성과에 대한 방향을 제시하는 한편, 회원국들이 조달 및 공동 자금 조달을 관리하고 있어 꾸준한 성장이 나타나고 있습니다. ‘디지털 교육 행동 계획 2021-2027’은 교사의 역량, 플랫폼 간 상호 운용성, 그리고 학생들의 디지털 기술 향상을 측정 가능한 목표로 삼고 있으며, 이를 통해 디지털 교육 출판 시장 전반에 걸쳐 접근성, 표준화, 분석과 관련된 공급업체들의 우선순위를 형성하고 있습니다. 독일의 ‘Digitalpakt 2.0’은 2026년부터 2030년까지 Wi-Fi, 단말기 및 교육에 자금을 배정하고 있습니다. 이를 통해 지방 자치단체의 매칭 자금이 확보되는 대로, 리치 미디어 및 하이브리드형 지도 역량이 대폭 확대될 것입니다. EU의 데이터 보호에 대한 기대는 개인정보를 침해하지 않으면서 교육 기관에서의 활용을 지원하는 호스팅 및 분석 모델을 이끌어내고 있으며, 이를 통해 디지털 교육 출판 시장에서 컨텐츠 패키징 및 평가 설계가 공공 부문의 요구 사항과 더욱 부합하게 되었습니다. 중동 및 아프리카 및 라틴아메리카의 일부 시장에서는 각국의 디지털 마스터 플랜에 따라 접속 환경과 학교 네트워크 확충이 진행되고 있으며, 이에 따라 학교와 직장에서 디지털 퍼스트 컨텐츠의 대상 사용자층이 점차 확대될 전망입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the digital education publishing market size was valued at USD 26.30 billion in 2025 and is estimated to grow from USD 28.72 billion in 2026 to reach USD 53.14 billion by 2031, at a CAGR of 13.10% during the forecast period (2026-2031).

This report is Segmented by Content Type (Digital Textbooks, Interactive Courseware, and More), End User (K-12 Educational Institutions, Higher Education Institutions, and More), Learning Format (Self-Paced Learning, Instructor-Led Learning, Blended/Hybrid Learning, and More), and More. The Market Forecasts are Provided in Terms of Value (USD), Based On Availability.

Global Digital Education Publishing Market Trends and Insights

Institutionalized Hybrid Learning Procurement Cycles Lock Multi-Year Revenue Streams

District- and system-level hybrid learning mandates channel spending into three-to-five-year licenses, turning one-off transactions into renewals anchored to LMS integration, content accessibility, and vendor certification trajectories. Where textbook adoption is centralized across 19 U.S. states plus Washington, D.C., formal RFPs elevate LTI 1.3, WCAG 2.2, and Section 508 compliance from nice-to-have attributes to eligibility gates for state-level approvals, stabilizing the digital education publishing market by rewarding compliant vendors during multi-year adoption cycles . Government platforms place greater weight on digital-first content, as illustrated by India's PM e-VIDYA and DIKSHA, which support national-scale distribution; when ministries standardize repositories and content metadata, publishers adapt product roadmaps to align with public workflows and multilingual needs. China's "AI + Education" action plan spans primary through higher education, with a 2030 horizon for full AI course integration, reinforcing demand for digital courseware and localized AI-aligned content that can connect to provincial platforms. In Europe, the Digital Education Action Plan frames interoperability and teacher capacity-building, pushing content providers toward standards participation and accessible-by-design production processes to remain relevant in cross-border programs, which sustains renewal potential across the digital education publishing market. As procurement focuses on durable integrations rather than discrete titles, the digital education publishing market faces higher switching costs, favoring vendors entrenched in district workflows and data systems.

Curriculum-Aligned Digital Assessment Mandates Restructure Content Development Economics

Mandated formative assessment and progress monitoring shift publishers from content shipments to ongoing diagnostic and analytics partners that feed lesson planning and intervention at the classroom scale. The framework effect is clearest where ministries outline explicit digital skills targets, as seen in the EU's policy track to raise computer and information literacy while directing investment into interoperable platforms that can host and share assessment outcomes across schools, thereby reshaping demand in the digital education publishing market . China's "AI + Education" direction produces content localization and AI-supported assessment needs across languages and scripts, with provincial smart platforms serving large installed bases that can use embedded diagnostics to close learning gaps. Human-in-the-loop workflows remain essential even as AI accelerates item creation, as evidenced by peer-reviewed research on AI-assisted test generation that documents scalability alongside the persistent need for expert review to ensure quality and fairness. The net effect is that content, assessment, and analytics converge into continuous services tied to institutional licenses rather than discrete textbook cycles, which reinforces recurring revenue for the digital education publishing market.

Piracy and Weak DRM Erode Revenue Capture in Emerging Markets

Low-connectivity environments influence delivery choices and can raise exposure to unauthorized redistribution when materials need to be accessible offline for extended periods. In markets where mobile and fixed broadband affordability exceeds benchmark targets, user reliance on cached or sideloaded content increases the risk surface for leakage, complicating ROI on premium titles in the digital education publishing market. Regions with school networks still in early deployment phases often lack persistent identity and license checks, which reduces the effectiveness of cloud-based DRM verification workflows and forces content providers to consider alternative controls suited to intermittent connectivity. When national platforms set open-access defaults for baseline materials, publishers respond by segmenting premium features such as adaptivity and analytics to defend value, which shapes product strategy across the digital education publishing market. This environment sustains a continuous need for packaging models and distribution safeguards aligned with local connectivity profiles and school device policies, which can change the calculus of DRM architectures.

Other drivers and restraints analyzed in the detailed report include:

- LMS-Native Content Bundles Compress Publisher Margins Through Platform Revenue Shares

- Mobile-First Access Expands Addressable Markets in Connectivity-Constrained Geographies

- Uneven Broadband and Device Access Fragments Addressable TAM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital Textbooks commanded 44.36% of the digital education publishing market share in 2025, reflecting the persistence of state adoption cycles and the embedded role of core curricula in formal procurement. Immersive and simulation-based formats are projected to grow fastest at a 21.87% CAGR through 2031 as institutions and employers seek experiential learning that mimics clinical, engineering, and safety-critical environments, broadening the scope of the digital education publishing market. Europe's investment in national digital platforms and school networks supports multimedia-first pedagogy. It raises the bar for content packaging and accessibility that textbooks alone cannot meet, thereby influencing publishers' portfolio balance between static and interactive assets. The digital education publishing industry is also prioritizing analytics-ready assets that can align with policy objectives such as skill tracking and inclusive access, putting adaptive and assessment-ready content at the center of renewal strategies in formal education. Where national repositories provide baseline materials, publishers focus on premium layers like adaptive feedback, progress dashboards, and secure proctoring to create a moat beyond open content and retain institutional contracts across the digital education publishing market.

Interactive Courseware and Assessment Materials continue to gain adoption as AI-assisted authoring compresses development timelines. At the same time, human validation maintains psychometric quality, as documented in peer-reviewed research on AI-generated test items with expert oversight. Multimedia Content adoption rises where broadband and device availability enable richer formats, with data integration partnerships that connect assessments and curricula to personalize sequencing in classrooms and districts. The digital education publishing market for immersive and simulation content is projected to expand at a 21.87% CAGR through 2031, as institutions procure scenario-based learning that can be measured through embedded tasks and analytics. Reference and supplemental content see more OER competition, which pushes differentiation toward adaptivity, accessibility, and evidence of learning impact that meets public-sector expectations. Together, these shifts move portfolios from static PDFs toward dynamic modules with assessment hooks that align with emerging standards and policy goals across the digital education publishing market.

K-12 and Higher Education Institutions collectively held 37.75% share in 2025, while Corporate and Professional Learners are set to grow at a 19.39% CAGR through 2031 as organizations fund targeted upskilling and verifiable credentials that can be tracked across HR systems. Enterprise demand focuses on skill diagnostics, continuous assessment, and role-based content paths that drive workforce productivity, steering a larger share of the digital education publishing market toward subscription delivery and analytics integrations. University-linked platforms and publishers are forming technology partnerships to bring AI-supported search, content discovery, and verification into institutional workflows, which sustains premium pricing for authenticated usage and citation inside the digital education publishing market. The digital education publishing industry also benefits when institutional buyers require accessible-by-design components that integrate into LMS catalogs in line with data protection rules, which encourages investment in platform reliability and customer support aligned with public expectations. Over time, outcome-linked content and credential networks become competitive moats as employers equate verified competencies with job readiness, which elevates the value of embedded assessment across the digital education publishing market.

Technical and vocational training providers benefit from national goals that expand access to labs, connectivity, and teacher development, thereby increasing the adoption of modular, stackable content aligned with local employment paths in the digital education publishing market. Corporate programs seek content that integrates with internal systems and supports role-based analytics without breaching regional data expectations, aligning with evolving standards agendas across the EU and other regions. Meanwhile, the K-12 and higher education segments continue to prioritize aligned assessments, teacher guidance, and compliance with accessibility mandates, which help stabilize renewals even as budgets fluctuate at the district and campus levels. These patterns point to a durable demand base for analytics-rich content that verifies skill gains and supports compliance across diverse user types inside the digital education publishing market.

Geography Analysis

North America secured 31.74% share in 2025, supported by well-funded K-12 districts and campus programs that favor inclusive-access licenses tied to LMS provisioning and analytics. Centralized textbook adoption across 19 states of the United States and Washington, D.C. underscores the importance of LTI 1.3, WCAG 2.2, and Section 508 compliance, which guide product design and bidding eligibility across the digital education publishing market. Institutions also maintain a preference for browser-based access that aligns with accessibility tooling and identity management, which sustains web-first portfolios. At the same time, mobile apps fill specific use cases and underserved contexts. The region's shift toward diagnostic and analytics-infused curricula strengthens recurring revenue models for vendors that can evidence learning impact and policy alignment across the digital education publishing market. Over time, these features add to switching costs and favor vendors with proven integrations and compatibility with district data flows that span instruction and assessment.

Asia-Pacific is the fastest-growing region with a projected 15.99% CAGR to 2031, supported by large-scale public investments in connectivity, devices, and smart education platforms. India's recent budgetary allocations continue to support digital resources and infrastructure for schools, thereby increasing platform usage and teacher adoption in government systems aligned with national initiatives like PM e-VIDYA and DIKSHA, which boost discovery and distribution at scale across the digital education publishing market. China's "AI + Education" action plan sets expectations for AI course coverage through 2030 and leverages provincial platforms that support massive enrollments, accelerating the development of localized content and assessment features in the digital education publishing market. ASEAN markets show wide variation in internet access and speeds, which pushes publishers to tailor SKUs to bandwidth realities while preparing for growth as national programs advance digital-economy ambitions. As national clouds and data-residency rules evolve, vendors adopt region-specific hosting and privacy practices that enable public procurement and long-term institution partnerships in the digital education publishing market.

Europe posts steady gains as EU-level programs set direction for interoperable solutions and skills outcomes while member states manage procurement and co-funding. The Digital Education Action Plan 2021-2027 prioritizes teacher capacity, platform interoperability, and measurable progress in student digital skills, thereby shaping vendor priorities in accessibility, standards, and analytics across the digital education publishing market. Germany's Digitalpakt 2.0 allocates funding from 2026 through 2030 for WLAN, devices, and training, which will expand capacity for rich media and hybrid instruction at scale once local match funding is arranged. EU data protection expectations guide hosting and analytics models that support institutional use without compromising privacy, which further aligns content packaging and assessment design with public-sector requirements in the digital education publishing market. Select markets in the Middle East and Africa and in Latin America continue to expand connectivity and school networks under national digital masterplans, which will progressively widen the addressable user base for digital-first content delivery at school and in the workplace.

- Pearson

- McGraw Hill

- Cengage Learning

- John Wiley & Sons

- Houghton Mifflin Harcourt

- Oxford University Press

- Cambridge University Press

- Scholastic Corporation

- Elsevier (Health Education)

- Springer Nature

- Savvas Learning Company

- Discovery Education

- Hachette Livre (Hodder Education)

- Georg von Holtzbrinck (Macmillan Education)

- SAGE Publishing

- Sanoma Learning

- Santillana

- Nelson (Canada)

- Hodder Education

- Vibal Group

- Diwa Learning Systems

- VitalSource Technologies (distribution/content partnerships)

- Chegg

- IXL Learning

- Coursera

- Udemy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Institutionalized hybrid learning procurement cycles

- 4.2.2 Curriculum-aligned digital assessment mandates

- 4.2.3 LMS-native content bundles scaling adoption

- 4.2.4 Mobile-first access expands consumption

- 4.2.5 Interoperability certifications increasingly drive purchasing

- 4.2.6 GenAI item banks speed test-prep

- 4.3 Market Restraints

- 4.3.1 Piracy and weak DRM leakage

- 4.3.2 Uneven broadband and device access

- 4.3.3 LMS revenue share compresses margins

- 4.3.4 Accessibility retrofits inflate production costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Educator Enablement & Implementation Services

- 4.8 Content Authoring & Lifecycle Economics (item banks, metadata, updates)

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Competitive Rivalry

- 4.9.2 Threat of New Entrants

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Bargaining Power of Buyers

- 4.9.5 Threat of Substitutes

5 Market Size & Growth Forecasts

- 5.1 By Content Type

- 5.1.1 Digital Textbooks

- 5.1.2 Interactive Courseware

- 5.1.3 Assessment & Test-Prep Materials

- 5.1.4 Reference & Supplemental Materials

- 5.1.5 Multimedia Content

- 5.1.6 Immersive & Simulation-Based Content

- 5.2 By End User

- 5.2.1 K-12 Educational Institutions

- 5.2.2 Higher Education Institutions

- 5.2.3 Corporate & Professional Learners

- 5.2.4 Technical & Vocational Training Providers

- 5.2.5 Independent Learners

- 5.3 By Learning Format

- 5.3.1 Self-Paced Learning

- 5.3.2 Instructor-Led Learning

- 5.3.3 Blended / Hybrid Learning

- 5.3.4 Synchronous Virtual Classrooms

- 5.4 By Delivery Channel

- 5.4.1 Web-Based Platforms & Portals

- 5.4.2 Mobile Learning Applications

- 5.4.3 Learning Management Systems (LMS)

- 5.4.4 Others

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Colombia

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Benelux (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, Product Launches)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Pearson

- 6.4.2 McGraw Hill

- 6.4.3 Cengage Learning

- 6.4.4 John Wiley & Sons

- 6.4.5 Houghton Mifflin Harcourt

- 6.4.6 Oxford University Press

- 6.4.7 Cambridge University Press

- 6.4.8 Scholastic Corporation

- 6.4.9 Elsevier (Health Education)

- 6.4.10 Springer Nature

- 6.4.11 Savvas Learning Company

- 6.4.12 Discovery Education

- 6.4.13 Hachette Livre (Hodder Education)

- 6.4.14 Georg von Holtzbrinck (Macmillan Education)

- 6.4.15 SAGE Publishing

- 6.4.16 Sanoma Learning

- 6.4.17 Santillana

- 6.4.18 Nelson (Canada)

- 6.4.19 Hodder Education

- 6.4.20 Vibal Group

- 6.4.21 Diwa Learning Systems

- 6.4.22 VitalSource Technologies (distribution/content partnerships)

- 6.4.23 Chegg

- 6.4.24 IXL Learning

- 6.4.25 Coursera

- 6.4.26 Udemy

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment