|

시장보고서

상품코드

2062170

항공기 밴드 클램프 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Aircraft Band Clamp - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

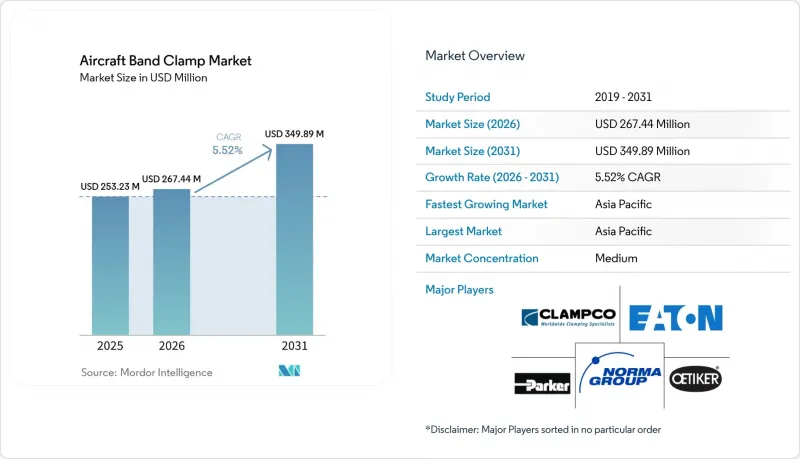

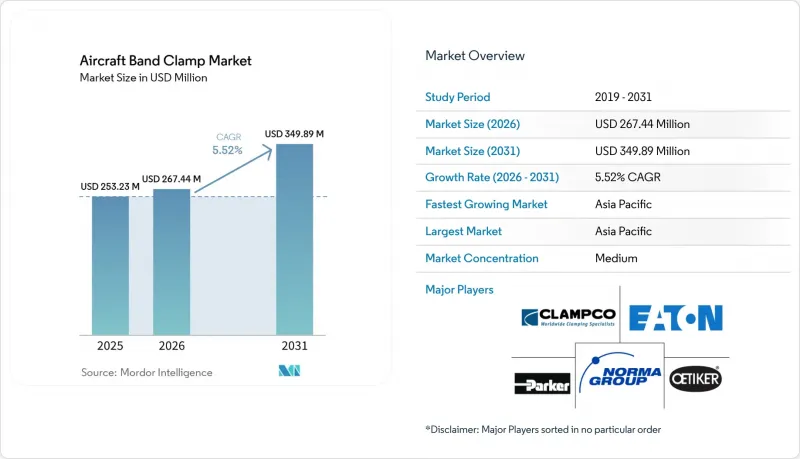

Mordor Intelligence에 의하면, 항공기 밴드 클램프 시장은 2025년에 2억 5,323만 달러 규모가 되어, 2026년 2억 6,744만 달러에서 2031년까지 3억 4,989만 달러로 성장하여 2026년부터 2031년까지 CAGR 5.52%로 확대될 것으로 예측됩니다.

본 보고서는 클램프의 유형(V-밴드 클램프, T-볼트 밴드 클램프 등), 재질(스테인리스 스틸, 티타늄 등), 항공기 유형(고정익기, 회전익기 등), 용도(기체 조립 등), 최종 사용자(OEM 및 애프터마켓), 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 항공기 밴드 클램프 시장 동향 및 분석

증가하는 항공기 생산 주문 잔고가 OEM용 부품 수요를 뒷받침하고 있습니다.

항공기 밴드 클램프 시장은 항공기 생산 속도와 밀접한 관련이 있습니다. 이는 모든 신규 기체 세트의 경우, 초기 조립 시 OEM 인증을 받은 클램프가 필요하기 때문입니다. 2026년 3월 기준으로 에어버스는 9,037대의 민간 항공기 수주 잔고를 보유하고 있으며, 2026년에는 에어버스와 보잉의 합계 수주 잔고가 15,000대를 넘어선 상태로 유지되었습니다. 이를 통해 공급업체는 향후 생산 수요를 명확히 파악할 수 있게 되었습니다. 또한 에어버스는 2025년에 793대의 민간 항공기를 인도할 예정이며, 이는 수주 파이프라인이 이미 진행 중인 프로그램의 탑재 부품 수량에 반영되기 시작했음을 보여줍니다. 이 수주 잔고는 항공기 밴드 클램프 시장 전체에 걸친 자재, 인증 역량 및 장기 공급 계약에 대한 사전 계획을 뒷받침하는 것입니다. 동시에, 2025년에는 공급망 병목 현상으로 인해 항공사에 110억 달러 이상의 손실이 발생할 것으로 예상되며, 그 결과 구형 항공기의 운용 기간이 연장됨에 따라 신규 생산 수요에 더해 교체 수요도 증가하고 있습니다. 그 결과, 신규 생산과 기체 운용 기간 연장이라는 두 가지 요인으로 인해 클램프 수요량이 높은 수준을 유지하는 지속적인 수요 패턴이 형성되고 있습니다.

배출가스 및 연비 기준의 강화가 경량화를 가속화

항공기 밴드 클램프 시장은 경량화와 보다 효율적인 시스템 설계를 중시하는 더욱 엄격해진 환경 규제로 인해 재편되고 있습니다. ICAO는 2026년 3월, 2031년 이후의 신형 항공기 설계에 대해 10% 더 엄격해진 CO2 기준을 채택했습니다. 이로 인해 구조물 및 시스템 전체의 무게를 줄이도록 제조업체에 가해지는 압박이 커지고 있습니다. CORSIA의 1단계(2024년부터 2026년)에서는 이미 690개 항공 운항 사업자에 대해 2019년 수준의 85%를 초과하는 배출량의 모니터링 및 상쇄가 의무화되어 있으며, 항공사 및 공급업체의 최우선 과제로서 연료 소비량 감축이 계속해서 중요하게 여겨지고 있습니다. 이러한 정책적 틀 덕분에, 오랫동안 스테인리스 스틸이 표준적인 선택지였던 용도에서 티타늄이나 알루미늄 합금 클램프를 채택하는 이점이 커지고 있습니다. 또한, 부품 수를 줄이고, 장착을 간소화하며, 주변 어셈블리의 무게 부담을 줄이는 다기능 클램프 설계도 이를 뒷받침하고 있습니다. 중기적으로는 설령 경량 소재의 단가가 기존 대안보다 높은 수준을 유지하더라도, 이러한 규제들로 인해 경량 소재에 대한 투자 비중이 더욱 확대될 가능성이 높다고 볼 수 있습니다.

금속 가격 변동이 이익률의 예측 가능성을 저해하고 있습니다.

경량화 프로그램이 본격화됨에 따라 티타늄 및 특수 합금의 중요성이 커지고 있어, 원자재 가격 변동은 여전히 항공기 밴드 클램프 시장에 걸림돌이 되고 있습니다. 클램프 공급업체는 고정 가격 계약이나 장기 계약으로 업무를 수행하는 경우가 많기 때문에 투입 비용의 급격한 변동이 반드시 신속하게 고객에게 전가되는 것은 아닙니다. 이러한 압박은 이미 체결된 항공우주 계약 하에서 수익성을 유지하면서 티타늄 제품 공급 규모를 확대하려는 제조업체에서 가장 두드러지게 나타납니다. 이 문제는 단순한 가격 책정에 그치지 않고, 공급의 집중이나 지정학적 혼란 또한 공급 상황, 리드타임, 재고 전략에 영향을 미칠 수 있습니다. 조달망이 탄탄하고 구매 관리 체제가 우수한 공급업체는 소규모 경쟁사보다 이러한 변동을 더 잘 흡수할 수 있는 입장에 있습니다. 하지만 합금 시장의 경제 상황이 불안정한 시기에 구매자들이 신중한 태도로 돌아서면, 항공기 밴드 클램프 시장에서는 소재 대체가 더디게 진행될 가능성이 있습니다.

부문별 분석

2025년 기준으로 V형 밴드 클램프는 매출의 35.21%를 차지하며, 항공기 밴드 클램프 시장의 주요 제품 카테고리로 자리 잡고 있습니다. 이러한 우위는 확실한 밀봉 성능과 반복 사용이 가능한 신뢰성이 필수적인 제트 엔진의 배기 덕트, 블리드 에어 시스템 및 APU 연결부에서 폭넓게 사용되고 있다는 점에 기인합니다. 이러한 설치 위치는 격렬한 열 사이클, 진동 및 빈번한 유지보수 작업에 노출되므로, 작업자는 반복적인 유지보수 작업 중에도 고정력을 유지할 수 있는 형태를 선호합니다. 이러한 요건 덕분에 V-BAND 설계는 많은 민간 협폭기 및 가혹한 열 환경에서 운용되는 군용기에서 확고한 입지를 다지고 있습니다. T-볼트 클램프는 고압 연료 및 유압 배관에서 널리 사용되고 있으며, 웜 드라이브 방식은 저압 덕트나 공기 분배 용도에서 여전히 중요한 역할을 하고 있습니다.

크래들 지지 래치 클램프 시장은 2031년까지 연평균 성장률(CAGR) 6.83%를 나타낼 것으로 예측되며, 항공기 밴드 클램프 시장의 이 부문은 구조적 지지 기능과 밀봉 기능을 단일 유닛으로 통합한 설계에 힘입어 성장하고 있습니다. 항공기 제조업체들은 부품 수를 줄이고, 설치 시간을 단축하며, 조립 주변의 패키징을 더욱 간소화해야 하는 압박을 받고 있어, 이러한 통합형 제품이 유리해지고 있습니다. 이러한 매력은 생산 효율성이 설계 결정 과정에서 더욱 중시되는 차세대 협폭기 프로그램에서 가장 두드러지게 나타납니다. 에어버스는 2026년 A350 화물칸 도어 주변부에 적용되는 와이어 방전 가공 티타늄 부품의 양산 통합을 시작하며, 생산 설계가 얼마나 통합적이고 기하학적으로 효율적인 부품으로 전환되고 있는지를 입증했습니다. 이러한 설계 방향성은 단순히 접합부를 고정하는 것 이상의 기능을 수행하는 클램프 형식을 뒷받침하고 있으며, 이것이 항공기 밴드 클램프 시장 전체에서 성장이 다기능형으로 전환되고 있는 이유입니다.

2025년에는 스테인리스 스틸이 매출의 46.65%를 차지하며 소재 수요를 주도했습니다. 이는 폭넓은 인증 실적, 균형 잡힌 비용 구조, 그리고 항공우주 분야의 다양한 용도에 대한 적합성을 반영한 것입니다. 스테인리스 스틸은 내식성, 신뢰할 수 있는 내구성, 그리고 예측 가능한 제조 비용을 제공하기 때문에 극한의 온도 환경을 제외한 많은 용도에서 여전히 가장 먼저 고려되는 선택지입니다. 주요 협폭기 기종의 대량 생산 또한 이러한 입지를 더욱 공고히 하고 있습니다. 비용 관리가 이루어지는 상업적 생산은 여전히 검증된 스테인리스 솔루션에 크게 의존하고 있기 때문입니다. 따라서 항공기 설계자들이 특정 조립 부품에 대해 더 가벼운 대안을 모색하고 있음에도 불구하고, 스테인리스 스틸은 여전히 대량 생산 프로그램의 핵심 소재로 자리 잡고 있습니다. 알루미늄 합금은 무게를 고려해야 하는 경우나 열에 노출되는 정도가 그리 심하지 않은 하중이 적은 기체 구조부에 설치될 때 여전히 중요한 역할을 하고 있습니다.

티타늄 시장은 2031년까지 연평균 성장률(CAGR) 7.22%를 나타낼 것으로 예측되며, 경량화에 대한 요구와 첨단 제조 기술의 결합에 힘입어 항공기 밴드 클램프 시장 규모는 확대되고 있습니다. ICAO의 더욱 엄격해진 환경 기준으로 인해 부품 차원에서의 경량화에 대한 압박이 커지고 있으며, 이는 성능상의 이점이 높은 단가를 정당화하는 티타늄의 경우, 채택 근거를 더욱 공고히 하고 있습니다. 또한, 에어버스사가 2026년에 적층 가공된 티타늄 구조 부재를 양산 기체에 도입할 예정이라는 점도, 복잡한 티타늄 부품의 항공우주 규격 적합성 확보 과정이 양산 규모에서 점차 현실화되고 있음을 시사합니다. Norsk Titanium사는 비행에 필수적인 구조물에 대한 PA-DED 티타늄 인증을 통해 기계 가공된 단조품에 비해 20%에서 35%의 비용 절감을 실현했다고 밝혔으며, 이로 인해 형상이 복잡한 티타늄 부품의 경제적 이점이 더욱 강화되었습니다. 그 결과, 티타늄은 항공기 밴드 클램프 업계의 가치 구조를 가장 뚜렷하게 변화시키고 있는 소재가 되고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 34.45%를 차지해, 2031년까지 연평균 성장률(CAGR) 7.16%로 성장할 것으로 전망되어, 항공기 밴드 클램프 시장에서 가장 큰 점유율과 가장 빠른 성장률을 동시에 기록하는 지역이 될 것입니다. 중국, 인도, 일본, 한국은 각각 항공기 보유 대수 증가, 국산 항공우주 프로그램, 공급업체 육성, MRO(정비·수리·오버홀) 사업의 확대와 같은 독자적인 요인을 통해 수요를 뒷받침하고 있습니다. 일본은 B787 프로그램의 항공기 구조 부품 분야에서 담당하는 역할을 통해 산업의 깊이를 더하고 있는 반면, 한국은 국산 항공기 플랫폼을 통해 군사 수요를 주도하고 있습니다. 인도에서는 항공사의 성장과 국내 정비 거점의 확대로 인해 해당 지역으로의 인증 부품 조달이 증가하고 있으며, 그 중요성이 커지고 있습니다. OEM 공급처가 점차 동쪽으로 이동함에 따라, 아시아태평양은 예측 기간 동안 항공기 밴드 클램프 시장에서 선두 위치를 더욱 공고히 할 가능성이 높습니다.

북미는 보잉사의 생산 체계와 미국의 방위 항공 산업 기반의 규모에 힘입어 2025년에는 2위를 차지했습니다. 미국의 2026 회계연도 국방 예산에는 F-35 47대, F-15EX 이글 II 21대, KC-46A 급유기 15대가 포함되어 있으며, 이를 통해 추진 시스템 및 기체 시스템 전반에 걸친 군용 등급 클램프 수요의 견고한 공급망이 유지되고 있습니다. 국내 정책 또한 프로그램 수요가 있는 지역 인근에서의 생산을 우선시하는 철강 관세 및 방위 조달 규정을 장려함으로써 현지 공급을 뒷받침하고 있습니다. 이에 따라 항공기 밴드 클램프 시장 전체에서는 아시아태평양이 더 빠르게 성장하고 있음에도 불구하고, 북미 공급업체들은 승인된 방위 사업 분야에서 우위를 유지하고 있습니다.

유럽은 매출액 기준 3위를 차지했으며, 툴루즈, 함부르크, 브로턴에서의 에어버스 생산과 NATO의 방위비 증액이 이를 뒷받침하고 있습니다. 에어버스는 2026년에 약 870대의 민간 항공기를 인도할 것으로 전망하고 있으며, 2026년 1분기 기준 헬리콥터 수주 잔고가 1,060대에 달하는 것으로 보고되어, 이는 광범위한 지역 수요 기반을 유지하고 있습니다. 남미는 여전히 규모는 작지만, 엠브라엘과 관련된 활동으로 인해 혜택을 보고 있습니다. 한편, 중동 및 아프리카에서는 MRO(정비·수리·오버홀)에 대한 투자와 항공우주 분야의 더 광범위한 야망을 통해 현지 수요가 형성되고 있습니다. 또한 튀르키예에서도 국내 항공기 프로그램으로 인해 현지 인증 부품에 대한 수요가 증가함에 따라 새로운 기회가 생겨나고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the aircraft band clamp market was valued at USD 253.23 million in 2025, and is projected to grow from USD 267.44 million in 2026 to USD 349.89 million by 2031, at a 5.52% CAGR over 2026-2031.

This report is Segmented by Clamp Type (V-Band Clamps, T-Bolt Band Clamps, and More), Material (Stainless Steel, Titanium, and More), Aircraft Type (Fixed-Wing Aircraft, Rotorcraft, and More), Application (Airframe Assemblies, and More), End-User (Original Equipment Manufacturer and Aftermarket), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aircraft Band Clamp Market Trends and Insights

Rising Aircraft Production Backlog Sustaining OEM Component Pull

The aircraft band clamp market remains closely tied to aircraft build rates, as every new shipset requires OEM-qualified clamps during first assembly. Airbus held a commercial aircraft backlog of 9,037 units as of March 2026, and the combined Airbus and Boeing backlog remained above 15,000 aircraft in 2026, providing suppliers with clear visibility into future production demand. Airbus also delivered 793 commercial aircraft in 2025, which shows that the order pipeline is already translating into installed component volume across active programs. This backlog supports forward planning for materials, certification capacity, and long-run supply agreements across the aircraft band clamp market. At the same time, supply chain bottlenecks cost airlines more than USD 11 billion in 2025, keeping older aircraft in service longer and increasing replacement demand alongside new production demand. The result is a durable two-channel demand pattern in which new builds and prolonged fleet service keep clamp volumes elevated.

Stricter Emission And Fuel-Efficiency Norms Accelerating Lightweighting

The aircraft band clamp market is being reshaped by tighter environmental rules that reward lower weight and more efficient system design. ICAO adopted a CO2 standard in March 2026 that is 10% more stringent for new aircraft type designs from 2031, which increases pressure on manufacturers to reduce mass across structures and systems. CORSIA's first phase, from 2024 to 2026, already requires 690 aircraft operators to monitor and offset emissions above 85% of 2019 levels, keeping fuel-burning reduction high on airline and supplier agendas. That policy setting improves the case for titanium and aluminum-alloy clamps in applications where stainless steel has long been the standard choice. It also supports multi-function clamp designs that reduce part count, simplify installation, and lower the weight burden of surrounding assemblies. Over the medium term, these rules are likely to shift more value toward lightweight materials, even if their unit costs remain above those of conventional options.

Metal Price Volatility Compressing Margin Predictability

Raw-material volatility remains a drag on the aircraft band clamp market because titanium and specialty alloys matter more as lightweight programs gain traction. Clamp suppliers often work under fixed-price or long-term agreements, so sudden changes in input costs are not always passed through to customers quickly. This pressure is most visible for manufacturers trying to scale titanium offerings while preserving margins under approved aerospace contracts. The issue is broader than pricing alone, as supply concentration and geopolitical disruption can also affect availability, lead times, and inventory strategy. Suppliers with stronger sourcing depth or better purchasing discipline are better placed to absorb these swings than smaller competitors. Even so, the aircraft band clamp market can see slower material substitution when buyers turn cautious during periods of unstable alloy economics.

Other drivers and restraints analyzed in the detailed report include:

- Expanding MRO Clamp-Replacement Demand From An Aging Global Fleet

- Higher Defense Aircraft Procurements Enlarging Addressable Platform Base

- Lengthy Airworthiness Certification Cycles Slowing New Product Introduction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

V-band clamps accounted for 35.21% of revenue in 2025, making them the leading product category in the aircraft band clamp market. Their lead comes from broad use in jet engine exhaust ducts, bleed-air systems, and APU connections where secure sealing and repeat serviceability are essential. These installations experience heavy thermal cycling, vibration, and frequent maintenance access, so operators favor a format that can maintain holding force during repeated service events. That requirement keeps V-band designs firmly embedded on many commercial narrowbody platforms and on military aircraft operating under demanding thermal conditions. T-bolt clamps followed with strong use in high-pressure fuel and hydraulic routing, while worm-drive variants remained important in lower-pressure ducting and air-distribution applications.

Cradle support latch clamps are forecast to grow at a 6.83% CAGR through 2031, and this segment of the aircraft band clamp market is supported by designs that combine structural support and sealing in a single unit. Aircraft builders are under pressure to reduce part count, shorten installation time, and simplify packaging around tighter assemblies, which favors these integrated products. Their appeal is strongest on next-generation narrowbody programs where production efficiency now carries more weight in design decisions. Airbus began serial integration of wire-directed energy-deposition titanium parts into the A350 cargo door surround in 2026, demonstrating how production design is moving toward consolidation and more geometry-efficient components. That same design direction supports clamp formats that do more than hold a joint, which is why growth is shifting toward multi-function variants across the aircraft band clamp market.

Stainless steel led material demand with 46.65% of revenue in 2025, reflecting its broad qualification base, balanced cost profile, and suitability for a wide range of aerospace uses. It remains the default choice for many non-extreme-temperature applications because it offers corrosion resistance, reliable durability, and predictable manufacturing economics. The high output of major narrowbody families also reinforces this position, since cost-controlled commercial production still depends heavily on proven stainless solutions. That is why stainless steel continues to anchor large-volume programs even as aircraft designers search for lighter options in selected assemblies. Aluminum alloys retain a meaningful role in lower-load airframe installations where weight sensitivity is high and thermal exposure is less severe.

Titanium is projected to grow at a 7.22% CAGR through 2031, and the market size for aircraft band clamps is gaining value as lightweighting pressure and advanced manufacturing capabilities converge. ICAO's tighter environmental standards are increasing pressure to remove weight at the component level, which improves the case for titanium, where performance benefits justify a higher unit price. Airbus's serial use of additively manufactured titanium structures in 2026 also signals that aerospace qualification pathways for complex titanium parts are becoming more practical at the production scale. Norsk Titanium stated that PA-DED titanium qualification for flight-critical structures delivered a 20% to 35% cost reduction compared to machined forgings, strengthening the economic case for geometry-rich titanium components. As a result, titanium is becoming the material that most clearly changes the value mix inside the aircraft band clamp industry.

Geography Analysis

Asia-Pacific accounted for 34.45% of revenue in 2025 and is forecast to grow at a 7.16% CAGR through 2031, making it the region with both the largest share and the fastest growth in the aircraft band clamp market. China, India, Japan, and South Korea each support demand through distinct mixes of fleet growth, indigenous aerospace programs, supplier development, and MRO expansion. Japan adds industrial depth through its role in the aerostructures of the B787 program, while South Korea adds military demand through locally produced aircraft platforms. India is becoming increasingly relevant as airline growth and a rising local maintenance base drive greater certified component sourcing into the region. With OEM sourcing gradually shifting eastward, Asia-Pacific is likely to widen its lead in the aircraft band clamp market over the forecast period.

North America ranked second in 2025, supported by Boeing production and the scale of the US defense aviation base. The US FY2026 defense budget included 47 F-35s, 21 F-15EX Eagle IIs, and 15 KC-46A tankers, which keeps a strong pipeline of military-grade clamp demand across propulsion and airframe systems. Domestic policy also supports local supply by encouraging steel tariffs and defense sourcing rules that favor manufacturing close to program demand, giving North American suppliers an advantage in approved defense work, even as the Asia-Pacific region grows faster in the broader aircraft band clamp market.

Europe ranked third by revenue, anchored by Airbus production in Toulouse, Hamburg, and Broughton, and by rising NATO defense spending. Airbus guided for around 870 commercial aircraft deliveries in 2026 and reported a helicopter order book of 1,060 units in Q1 2026, which sustains a broad regional demand base. South America remains smaller but benefits from Embraer-linked activity, while the Middle East and Africa are building local demand through MRO investment and broader aerospace ambitions. Turkey also adds an emerging opportunity set as domestic aircraft programs raise the need for locally qualified component supply.

- NORMA Group SE

- Clampco Products, Inc.

- Oetiker Group

- Ideal Tridon Group

- Parker-Hannifin Corporation

- Eaton Corporation plc

- Howmet Aerospace Inc.

- Ho-Ho-Kus, Inc.

- Hexadex Limited

- Leggett & Platt, Incorporated

- Murray Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising aircraft production backlog

- 4.2.2 Expanding MRO clamp-replacement demand

- 4.2.3 Higher defense aircraft procurements

- 4.2.4 Stricter emission/fuel-efficiency norms

- 4.2.5 Additive-manufactured titanium clamps

- 4.2.6 Hybrid-electric thermal-cycling needs

- 4.3 Market Restraints

- 4.3.1 Metal price volatility

- 4.3.2 Lengthy airworthiness certification cycles

- 4.3.3 Band-less quick-release couplings adoption

- 4.3.4 Specialty wire-rod supply disruptions

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Clamp Type

- 5.1.1 V-band Clamps

- 5.1.2 T-bolt Band Clamps

- 5.1.3 Worm-Drive Band Clamps

- 5.1.4 Cradle Support Latch Clamp

- 5.1.5 Other Band Clamps

- 5.2 By Material

- 5.2.1 Stainless Steel

- 5.2.2 Titanium

- 5.2.3 Aluminum Alloys

- 5.2.4 Nickel

- 5.2.5 Others

- 5.3 By Aircraft Type

- 5.3.1 Fixed-Wing Aircraft

- 5.3.1.1 Commercial Aviation

- 5.3.1.1.1 Narrowbody

- 5.3.1.1.2 Widebody

- 5.3.1.1.3 Regional Jets

- 5.3.1.2 Military Aviation

- 5.3.1.2.1 Fighter Jets

- 5.3.1.2.2 Transport Aircraft

- 5.3.1.2.3 Special Mission Aircraft

- 5.3.1.3 General Aviation

- 5.3.1.3.1 Business Jet

- 5.3.1.3.2 Piston and Turbofan Aircraft

- 5.3.1.1 Commercial Aviation

- 5.3.2 Rotorcraft

- 5.3.2.1 Civil Helicopters

- 5.3.2.2 Military Helicopters

- 5.3.3 Unmanned Aerial Vehicles (UAVs)

- 5.3.1 Fixed-Wing Aircraft

- 5.4 By Application

- 5.4.1 Airframe Assemblies

- 5.4.2 Engine Components

- 5.4.3 Hydraulic Systems

- 5.4.4 Fuel Systems

- 5.4.5 Electrical Systems

- 5.5 By End-User

- 5.5.1 Original Equipment Manufacturer (OEM)

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Italy

- 5.6.2.5 Russia

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NORMA Group SE

- 6.4.2 Clampco Products, Inc.

- 6.4.3 Oetiker Group

- 6.4.4 Ideal Tridon Group

- 6.4.5 Parker-Hannifin Corporation

- 6.4.6 Eaton Corporation plc

- 6.4.7 Howmet Aerospace Inc.

- 6.4.8 Ho-Ho-Kus, Inc.

- 6.4.9 Hexadex Limited

- 6.4.10 Leggett & Platt, Incorporated

- 6.4.11 Murray Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment