|

시장보고서

상품코드

2062171

음성 사용자 인터페이스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Voice User Interface - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

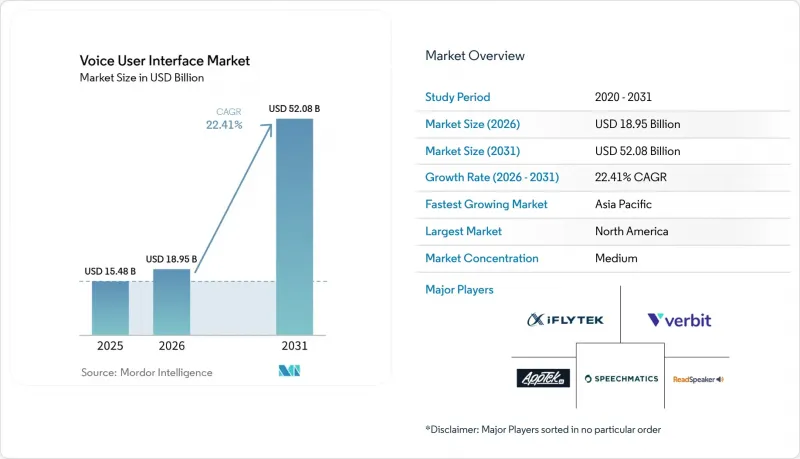

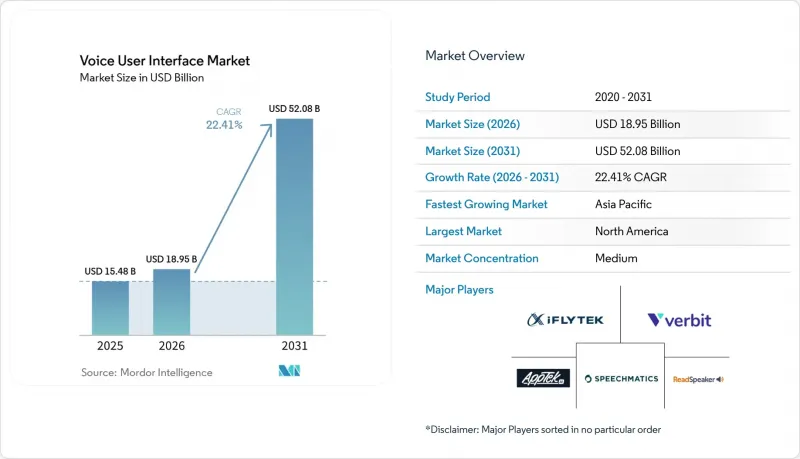

Mordor Intelligence에 의하면, 음성 사용자 인터페이스 시장 규모는 2025년에 154억 8,000만 달러로 평가되었습니다. 2026년 189억 5,000만 달러에서 2031년까지 520억 8,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 22.41%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어, 하드웨어, 서비스), 도입 형태(On-Premise, 클라우드), 용도(가전, 자동차, 헬스케어, 은행, 금융서비스 및 보험(BFSI), 소매 및 전자상거래, 교육, 기타), 기술 스택(엣지 AI 처리, 클라우드 기반 처리, 하이브리드 처리), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 음성 사용자 인터페이스 시장 동향과 인사이트

딥러닝을 통한 음성 인식 정확도 향상

트랜스포머 아키텍처를 통해 2025년에는 생성 시 단어 오류율이 5.42%까지 낮아져, 2023년의 재귀 신경망에 비해 40% 개선되었습니다. 컨텍스트 바이어스 기술 덕분에 음성 인터페이스는 별도의 재훈련 없이도 법률, 의료, 금융 분야의 전문용어를 분석할 수 있게 되었으며, 트레이딩 플로어나 수술실과 같은 고위험 환경에서의 활용이 확대되고 있습니다. 학술적인 REB-former 연구를 통해 중복된 어텐션 헤드가 제거되었고, 엣지 디바이스의 지연 시간이 180밀리초로 단축되어 웨어러블 기기에서 실시간 대화가 가능해졌습니다. 이 장벽을 극복함으로써 기업들은 음성 입력을 보조적인 수단에서 주요 제어 수단으로 격상시켰으며, 과거에는 키보드나 터치스크린에 의존하던 다양한 산업 분야에서의 도입을 가속화하고 있습니다.

오프라인 음성 처리가 가능한 온디바이스 엣지 AI 칩

전용 신경망 처리 장치는 500밀리와트 이하의 전력 소비로 10 TOPS를 달성하여, 10억 개의 매개변수를 가진 모델을 스마트폰이나 차량용 헤드 유닛에 탑재할 수 있게 해줍니다.(3)예를 들어, 메르세데스-벤츠는 로컬 웨이크워드 감지 기능과 중간 수준의 성능을 가진 음성 인식 모델을 결합함으로써 2026년형 E-클래스에서 200밀리초 이하의 실행 시간을 실현했습니다. 오프라인 추론은 성능과 네트워크 품질을 분리합니다. 이는 통신 상태가 불안정한 자동차나 산업 현장에서 결정적인 장점이 됩니다. 대량 생산에 따른 경제적 효과도 따릅니다. ChipIntelli는 2025년에 2.80달러짜리 칩 1,500만 개를 출하함으로써, 배터리 구동식 센서, 잠금 장치, 온도 조절기에 신뢰성 높은 음성 제어 기능을 추가할 수 있게 했습니다.

사생활 보호 및 데이터 보안에 대한 뿌리 깊은 우려

생체 인증인 음성 지문은 일반 데이터 보호 규정(GDPR(EU 개인정보보호규정))의 기밀 데이터 조항의 적용을 받습니다. 또한, 조사 대상 소비자의 68%는 어시스턴트가 녹음 데이터를 어떻게 저장하고 공유하는지에 대해 여전히 확실하게 알지 못하고 있습니다. 미국 연방거래위원회(FTC)가 아마존과 체결한 아동 데이터 관련 합의는 이러한 회의적인 시각을 더욱 강화시켜, 부모들의 구매 의향을 12포인트 하락시켰습니다. 현재 기업들은 기기 내 처리 및 데이터 비보관 방안을 도입하고 있습니다. Nuance의 ‘Dragon Medical One’은 익명화된 텍스트만 보관하며, 프로젝트 예산에 약 120만 달러를 추가했음에도 불구하고 의료보험 상호운용성 및 책임에 관한 법률(HIPAA) 준수를 보장하고 있습니다. 투명한 거버넌스 체계가 확립되기 전까지는 개인정보 보호에 대한 우려가 의료, 은행, 교육 분야에서의 도입을 저해할 것으로 보입니다.

부문별 분석

기업들이 턴키 포장 방식을 넘어선 사업을 확대함에 따라, 서비스는 보조적인 역할에서 성장의 원동력으로 진화했습니다. 2025년에는 소프트웨어가 57.16%의 점유율을 유지했으나, 서비스 부문은 2031년까지 연평균 23.18%의 성장률을 기록하며 소프트웨어와 하드웨어의 성장률을 모두 상회할 것으로 전망됩니다. 2025년 Nuance DAX Copilot의 병원 도입과 같은 대규모 전개에서는 180시간의 통합 작업, 40명의 의사의 어휘에 맞춘 억양 조정, 규정 준수 문서화가 필요했으며, 이로 인해 1개 거점당 34만 달러의 전문 서비스 수익을 창출했습니다. 따라서, 자연어의 진화에 따른 지속적인 재훈련의 필요성에 힘입어, 서비스 부문 내 음성 사용자 인터페이스 시장 규모는 핵심인 라이선싱 시장보다 더 빠르게 확대되고 있습니다.

하드웨어는 여전히 밸류체인에서 필수적인 요소이며, 빔포밍 마이크, 디지털 신호 프로세서, 신경망 처리 장치를 비용 효율적인 칩에 통합하고 있습니다. Anker의 Thus 칩은 6개의 마이크 어레이와 1 TOPS의 추론 기능을 결합하여 원거리 음성 포착 품질을 향상시켰으며, 4.20달러의 가격으로 수백만 개가 출하된 실적을 자랑합니다. 지속적인 학습 계약은 학습 내용을 더욱 공고히 하는 요인이 됩니다. 데이터 세트를 분기마다 업데이트하지 않는 한 정확도는 매년 4-7%씩 떨어지기 때문에 음성 전문 컨설팅 기업에게는 지속적인 수익원이 됩니다. 코드, 실리콘, 서비스 간의 이러한 상호 의존 관계 덕분에, 맞춤화가 가속화되는 상황에서도 균형 잡힌 구성 요소 구성이 유지되고 있습니다.

2025년 매출의 63.22%는 클라우드 배포가 차지했으며, 이는 GPU 풀링을 통해 음성 1분당 추론 비용이 0.005-0.02달러로 낮아져 On-Premise 방식의 경제성을 크게 밑돌게 된 것이 뒷받침하고 있습니다. OpenAI의 GPT-4o 보이스 모드는 입력 토큰 100만 건당 5달러이며, 232-320밀리초의 지연 시간을 실현하고 있습니다. 이러한 지표를 통해 볼 때, 음성 사용자 인터페이스 시장은 복잡한 추론 및 멀티모달 작업 분야에서 클라우드 중심 접근 방식을 유지하고 있습니다. 그럼에도 불구하고, 하이브리드 라우팅 처리가 로컬에서 단어 트리거를 활성화하고 문맥 의존적 쿼리만 전송하는 방식이 표준이 되어, 표준 발화의 70-80%를 기기 내에서 처리함으로써 대역폭 수요를 억제하고 있습니다.

On-Premise 도입은 절대 수치로는 작지만, 생체 인증 데이터의 해외 반출을 금지하는 중국과 인도의 데이터 주권법에 따라 연평균 성장률(CAGR) 18.90%로 성장을 지속하고, 있습니다. iFlytek의 병원용 시스템 도입은 개인정보보호법 요건을 충족하기 위해 모든 데이터가 현지 데이터센터 내에 보관되고 있으며, 이로 인해 사용자당 라이선스 수는 40% 증가했음에도 불구하고 규제 당국의 승인을 확보하고 있습니다. 다국적 벤더들은 현재 퍼블릭 클라우드와 주권형 On-Premise라는 두 가지 제품 라인을 유지해야 하는 상황으로, 이로 인해 엔지니어링의 복잡성은 증가하고 있지만, 법적 장애물 없이 배포할 수 있는 음성 사용자 인터페이스 시장 점유율을 확대되고 있습니다.

지역별 분석

북미는 2025년 매출의 38.23%를 차지하며 1위를 기록했습니다. 3억 대에 달하는 성숙한 스마트 스피커 보급 기반과 연방거래위원회(FTC)의 조기 규제 제정으로 인해 기업들에게 법적 명확성이 확보되었으며, 의료 분야에서의 적극적인 도입이 촉진되었습니다. 해당 지역의 예상 연평균 성장률(CAGR)은 20.80%로 세계 평균보다 낮지만, 이는 현재 소비자 보급률이 가구의 62%에서 정체되어 있기 때문입니다. 미국은 지역 매출의 78%를 차지하고 있으며, 사용자가 Alexa나 Siri 환경에서 벗어나지 못하게 하는 생태계 전환 비용 덕분에 그 입지가 공고해지고 있습니다. 캐나다와 멕시코는 각각 14%와 8%를 차지하고 있으며, 최근 코드 스위칭의 정확도가 향상된 점을 활용하여 이중언어 전략을 가속화하고 있습니다.

아시아태평양은 24.17%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 중국은 전기차 및 스마트 홈 부문에서 월간 83억 건의 검색어를 처리하는 바이두의 DuerOS의 강점을 바탕으로, 해당 지역의 수익 대부분을 차지하고 있습니다. 인도는 지방 도시에서의 보급과 인터넷을 처음 사용하는 사용자들에게 지지를 받고 있는 현지 언어 음성 모델에 힘입어, 상대적으로 작은 시장 점유율을 차지하고 있습니다. 일본과 한국은 2025년 개인정보보호법 개정에 대비하기 위해 기기 내 처리를 중시하고 있습니다. 한편, 동남아시아국가연합(ASEAN) 시장에서는 방언의 다양성이 과제로 대두되고 있으며, 이는 소규모 진출기업에게는 장벽이 되는 반면, 해당 지역을 대표하는 기업에게는 성장의 여지가 되고 있습니다.

유럽은 전 세계 매출의 21.40%를 차지하고 있습니다. 연평균 성장률(CAGR) 22.60%로 예상되는 이러한 성장은 주행 중 운전 부담을 줄이기 위해 음성 기능 탑재를 의무화하는 자동차 산업의 규제에 힘입어 이루어지고 있습니다. 그러나 EU 인공지능법의 Tier-II 공개 요건은 규정 준수 비용을 8-12% 증가시켜 중소 벤더들이 시장에서 철수하거나 제휴를 맺도록 압박하고 있습니다. 남미는 전 세계 매출의 불과 6.20%에 불과하지만, 브라질의 포르투갈어 음성 뱅킹을 배경으로 연평균 성장률(CAGR) 23.40%를 기록하며 성장하고 있습니다. 중동 및 아프리카(5.80%)에서는 아랍어 음성 서비스의 초기 도입이 진행되고 있지만, 방언의 다양성과 공개 코퍼스의 부족으로 인해 정확도 격차가 여전히 크며, 정부나 통신 사업자가 진행하는 시범 사업 이외의 분야에서는 보급이 더딘 양상을 보이고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the voice user interface market size was valued at USD 15.48 billion in 2025 and estimated to grow from USD 18.95 billion in 2026 to reach USD 52.08 billion by 2031, at a CAGR of 22.41% during the forecast period (2026-2031).

This report is Segmented by Component (Software, Hardware, and Services), Deployment Mode (On-Premises, and Cloud), Application Vertical (Consumer Electronics, Automotive, Healthcare, BFSI, Retail and E-Commerce, Education, and More), Technology Stack (Edge AI Processing, Cloud-Based Processing, and Hybrid Processing), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Voice User Interface Market Trends and Insights

Advances in Deep-Learning Speech Recognition Accuracy

Transformer architectures cut production word-error rates to 5.42% in 2025, a 40% lift over 2023 recurrent networks. Contextual-biasing techniques allow voice interfaces to parse legal, medical, and financial jargon without bespoke retraining, expanding use in high-stakes environments such as trading floors and operating rooms. Academic REB-former research prunes redundant attention heads, reducing edge-device latency to 180 milliseconds and making real-time interaction feasible for wearables. With the threshold crossed, enterprises now elevate voice from secondary input to primary control, accelerating deployments across verticals that once relied on keyboards and touchscreens.

On-Device Edge AI Chips Enabling Offline Voice Processing

Specialized neural processing units reach 10 TOPS at sub-500 milliwatt power budgets, placing 1 billion-parameter models inside smartphones and car head units.[3] Mercedes-Benz, for instance, achieves sub-200 millisecond execution in the 2026 E-Class by pairing local wake-word detection with mid-tier transcription models. Offline inference decouples performance from network quality, a decisive benefit in automotive and industrial sites where coverage is spotty. Volume economics follow: ChipIntelli shipped 15 million USD 2.80 chips in 2025, enabling battery-powered sensors, locks, and thermostats to add reliable voice control.

Persistent Privacy and Data-Security Concerns

Biometric voiceprints fall under sensitive-data clauses in the General Data Protection Regulation, and 68% of surveyed consumers remain unsure how assistants store or share recordings. The United States Federal Trade Commission settlement with Amazon over child data amplified skepticism, knocking 12 percentage points off purchase intent among parents. Enterprises now adopt on-device processing and zero-retention policies. Nuance's Dragon Medical One keeps only de-identified text, adding roughly USD 1.2 million to project budgets but securing Health Insurance Portability and Accountability Act compliance. Until transparent governance frameworks solidify, privacy anxiety will mute uptake in healthcare, banking, and education.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Smart Speakers and Voice-First Consumer Devices

- Growing Integration of VUI in Automotive Infotainment

- Acoustic and Accent Variability Reducing Recognition Accuracy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services advanced from a supporting role to a growth engine as enterprises widen deployments beyond turnkey packages. Software retained 57.16% share in 2025, but services are slated to compound at 23.18% annually through 2031, eclipsing both software and hardware expansion. Large rollouts, such as a 2025 hospital implementation of Nuance DAX Copilot, demanded 180 integration hours, accent tuning for 40 physician vocabularies, and compliance documentation, yielding USD 340,000 in professional-services revenue per site. The voice user interface market size for services is therefore scaling faster than the core licensing pool, driven by recurring retraining needs as natural language evolves.

Hardware remains essential in the value chain, bundling beamforming microphones, digital signal processors, and neural processing units on cost-efficient dies. Anker's Thus chip ships in multimillion-unit volumes at USD 4.20, bundling six-microphone arrays with 1 TOPS inference, elevating far-field capture quality. Continuous-learning contracts add another layer of stickiness: accuracy drifts 4-7 percentage points each year unless datasets are refreshed quarterly, creating annuity revenue for speech-specialist consultancies. This interdependence between code, silicon, and services sustains a balanced component mix even as customization accelerates.

Cloud deployments controlled 63.22% of 2025 revenue, propelled by GPU pooling that drops inference cost to USD 0.005-0.02 per audio minute, well below on-premises economics. OpenAI's GPT-4o voice mode hits 232-320 millisecond latency at USD 5 per million input tokens. Such metrics keep the voice user interface market leaning toward the cloud for complex reasoning and multimodal tasks. Nevertheless, hybrid routing processing wakes word triggers locally, then shipping only context-dependent queries has emerged as the operational norm, resolving 70-80% of standard utterances on-device and containing bandwidth demand.

On-premises installations, although smaller in absolute value, post an 18.90% CAGR due to data-sovereignty laws in China and India that forbid biometric prints from leaving national borders. iFlytek's hospital deployments remain entirely inside local data centers to satisfy Personal Information Protection Law rules, lifting per-seat licenses 40% yet securing regulatory clearance. Multinational vendors must now sustain dual product tracks, public cloud and sovereign on-premises, raising engineering complexity but widening the voice user interface market share they can address without legal hindrance.

Geography Analysis

North America led with 38.23% of 2025 revenue. A mature 300 million smart-speaker base and early Federal Trade Commission rule-setting gave enterprises legal clarity, prompting aggressive healthcare implementations. The region's 20.80% forecast CAGR trails the global average because consumer penetration now plateaus at 62% of households. The United States accounts for 78% of regional revenue, locked in by ecosystem switching costs that deter users from leaving Alexa or Siri setups. Canada and Mexico, at 14% and 8% respectively, accelerate bilingual rollouts, leveraging recent improvements in code-switched accuracy.

Asia-Pacific posts the fastest 24.17% CAGR. China owns the majority of regional revenue on the strength of Baidu's DuerOS, which fields 8.3 billion monthly queries across electric vehicles and smart homes. India holds a smaller slice, propelled by tier-2 city adoption and vernacular speech models that resonate with first-time internet users. Japan and South Korea emphasize on-device processing to align with 2025 privacy amendments, and the Association of Southeast Asian Nations markets struggle with dialect fragmentation, raising barriers to smaller entrants but opening room for regional champions.

Europe captures 21.40% of global revenue. Growth, forecast at 22.60% CAGR, is paced by automotive mandates requiring voice to mitigate driver distraction. However, EU Artificial Intelligence Act Tier-II disclosures add 8-12% compliance overhead, nudging smaller vendors to exit or partner. South America, though only 6.20% of worldwide revenue, expands at 23.40% CAGR behind Portuguese-language voice banking in Brazil. Middle East and Africa, at 5.80%, see early Arabic voice deployments, but dialect diversity and limited public corpora keep accuracy gaps wide, slowing uptake outside government and telecom pilots.

- Amazon.com, Inc.

- Google LLC

- Apple Inc.

- Microsoft Corporation

- Baidu Inc.

- iFlytek Co., Ltd.

- Nuance Communications, Inc.

- Sensory, Inc.

- Cerence Inc.

- SoundHound AI, Inc.

- Verbit, Inc.

- AppTek LLC

- Speechmatics Ltd.

- ReadSpeaker Holding B.V.

- Voiceitt Ltd.

- LumenVox LLC

- AISpeech Co., Ltd.

- Deepgram, Inc.

- Picovoice Inc.

- Voxygen S.A.S.

- Uniphore Technologies Inc.

- Grit AI Inc.

- Kore.ai, Inc.

- AssemblyAI, Inc.

- Talkie.ai Sp. z o.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advances in Deep-Learning Speech Recognition Accuracy

- 4.2.2 On-Device Edge AI Chips Enabling Offline Voice Processing

- 4.2.3 Proliferation of Smart Speakers and Voice-First Consumer Devices

- 4.2.4 Growing Integration of VUI in Automotive Infotainment

- 4.2.5 Multimodal Foundation Models Enabling Context-Rich Voice Interactions

- 4.2.6 Open-Source Speech Corpora Lowering Entry Barriers for Niche Language Markets

- 4.3 Market Restraints

- 4.3.1 Persistent Privacy and Data-Security Concerns

- 4.3.2 Acoustic and Accent Variability Reducing Recognition Accuracy

- 4.3.3 Escalating Royalties for Proprietary Wake-Word IP in OEM Devices

- 4.3.4 EU AI Act Tier-II Transparency Mandates Inflating Compliance Overheads

- 4.4 Industry Value and Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By Application Vertical

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive

- 5.3.3 Healthcare

- 5.3.4 BFSI

- 5.3.5 Retail and E-commerce

- 5.3.6 Education

- 5.3.7 Other Application Verticals

- 5.4 By Technology Stack

- 5.4.1 Edge AI Processing

- 5.4.2 Cloud-Based Processing

- 5.4.3 Hybrid Processing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon.com, Inc.

- 6.4.2 Google LLC

- 6.4.3 Apple Inc.

- 6.4.4 Microsoft Corporation

- 6.4.5 Baidu Inc.

- 6.4.6 iFlytek Co., Ltd.

- 6.4.7 Nuance Communications, Inc.

- 6.4.8 Sensory, Inc.

- 6.4.9 Cerence Inc.

- 6.4.10 SoundHound AI, Inc.

- 6.4.11 Verbit, Inc.

- 6.4.12 AppTek LLC

- 6.4.13 Speechmatics Ltd.

- 6.4.14 ReadSpeaker Holding B.V.

- 6.4.15 Voiceitt Ltd.

- 6.4.16 LumenVox LLC

- 6.4.17 AISpeech Co., Ltd.

- 6.4.18 Deepgram, Inc.

- 6.4.19 Picovoice Inc.

- 6.4.20 Voxygen S.A.S.

- 6.4.21 Uniphore Technologies Inc.

- 6.4.22 Grit AI Inc.

- 6.4.23 Kore.ai, Inc.

- 6.4.24 AssemblyAI, Inc.

- 6.4.25 Talkie.ai Sp. z o.o.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment