|

시장보고서

상품코드

2062177

노킹 방지제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Antiknock Agents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

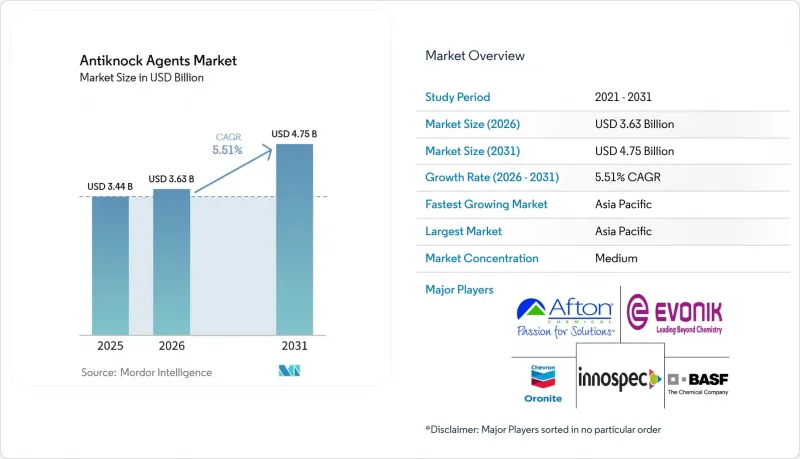

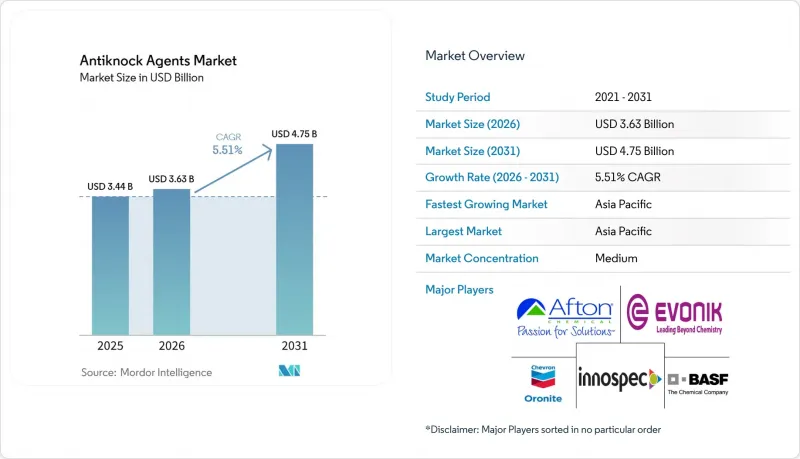

Mordor Intelligence에 의하면, 노킹 방지제 시장 규모는 2025년 34억 4,000만 달러로 평가되었습니다. 2026년 36억 3,000만 달러로 확대되어 2031년까지 47억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR은 5.51%를 나타낼 전망입니다.

본 보고서는 제품 유형(에탄올, 테트라에틸납(TEL), 기타), 형태(액체, 고체, 첨가제 포장/농축액), 유통 채널(OEM 공급, 벌크 터미널 주입, 기타), 용도(자동차, 항공, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 노킹 방지제 시장 동향 및 분석

고옥탄가 연료가 필요한 터보차저가 장착된 다운사이징

압축비가 11 : 1 이상인 1.2-2리터 터보차저 장착 엔진은 91의 조사 옥탄가(RON) 연료의 한계 근처에서 작동합니다. 2025년에는 14개 OEM 업체가 TOP TIER 기준을 채택하고, 인젝터의 침전물 및 저속 주행 시의 예연소를 해결하기 위해 미국 환경보호청(EPA)의 세정제 기준의 5배를 의무화했습니다. 아르곤 국립연구소의 조사에 따르면, 에탄올 함량을 E10에서 E15로 늘리면 미세먼지 배출량을 18% 줄일 수 있는 것으로 나타났습니다. 그러나 E20을 초과하면, 연소 속도에 미치는 충전 냉각의 영향으로 인해 RON의 향상은 한계에 도달하게 됩니다. 그 결과, 프리미엄 연료 혼합 업체들은 E10에 10-12 부피%(vol%)의 에틸-터셔리-부틸-에테르(ETBE)를 배합하여, 7 psi(제곱인치당 파운드)의 리드 증기압 제한을 준수하면서도 95 이상의 RON을 달성하고 있습니다.

동남아시아에서의 급속한 자동차 보급과 완만한 방향족 제한

인도네시아의 유로 4에 상응하는 규제에서는 방향족 45%와 벤젠 1.5%가 허용됩니다. 이러한 규제 체계 덕분에, 펠타미나는 리포메이트 함량이 높은 92 RON 휘발유를 효율적으로 공급할 수 있게 되었습니다. 2025년, 베트남의 휘발유 소비량은 8.2% 증가했습니다. 그러나 해당 국가의 정유시설에는 유동 접촉 분해(FCC) 설비의 업그레이드가 미흡하기 때문에 수입업체들은 한국이나 싱가포르산 방향족 나프타에 의존하고 있습니다. 태국에서는 E20이 도입되었지만, 연비 저하 우려로 인해 소매 판매의 고작 12%만을 차지하고 있습니다. 한편, 고급 하이브리드 차량에는 95 RON 이상의 휘발유가 필요하기 때문에 이로 인해 메틸-터샤리-부틸-에테르(MTBE)와 에탄올의 프리미엄 시장이 형성되고 있습니다.

에탄올 가격 변동과 미국의 혼합 및 월(Wall)에 따른 제약

2025년 1월, 중서부 지역의 가뭄으로 인해 수확량이 14% 감소한 것을 배경으로, 옥수수 유래 에탄올 가격은 갤런당 1.85달러에서 8월까지 2.62달러로 상승했습니다. 환경보호청(EPA)이 3,800곳의 주유소에서 연중 E15 사용을 승인했음에도 불구하고, E10 혼합 및 판매 제한이 여전히 추가 수요를 억제하고 있습니다. 브라질이 에탄올을 국내 수화 용도로 전용함에 따라, 로테르담의 수입 가격은 1m³당 720유로(0.47달러)까지 상승했습니다.

부문별 분석

2025년, 에탄올은 노킹 방지제 시장 점유율의 39.11%를 차지했습니다. 이는 수요를 뒷받침한 브라질의 E27-E30 정책과 미국의 재생 가능 연료 기준(RFS)에 힘입은 결과입니다. 그러나 바이오 유래 산소화제는 2031년까지 연평균 성장률(CAGR) 6.17%를 기록하며, 노킹 방지제 시장에서 가장 빠른 성장세를 보일 것으로 전망됩니다. 이러한 성장은 재생에너지 지침 III(RED III)에 따른 바이오에틸-터샤리부틸에테르(바이오 ETBE)의 이중 산입과, 비용 효율이 높은 이소부틸렌을 공급하는 지속가능 항공연료(SAF)의 부산가스를 통합한 결과입니다.

2025년 기준으로, 액상 제제는 노킹 방지제 시장 점유율의 62.14%를 차지하고 있으며, 연평균 성장률(CAGR) 5.88%를 나타낼 것으로 전망됩니다. 이러한 성장은 파이프라인과의 호환성과 터미널에서의 첨가 공정에서의 편의성에서 기인합니다. 또한, 셰브론의 인라인 분석 장치는 옥탄가 손실을 0.4포인트 줄임으로써 가동 효율 향상에 기여했으며, 그 결과 산소화제 비용에서 320만 달러의 비용 절감을 실현했습니다. 이러한 요인들은 노킹 방지제 시장에서 액상 제제가 차지하는 중요한 역할을 부각시키고 있습니다.

지역별 분석

2025년, 아시아태평양은 노킹 방지제 시장 매출의 46.11%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 6.28%를 나타낼 것으로 전망됩니다. 중국의 3억 대에 달하는 자동차 보유 대수에 더해, 연구용 옥탄가(RON) 95로의 전환이 메틸-터샤리-부틸-에테르(MTBE) 수요를 견인하고 있습니다. 인도에서는 바라트 스테이지 VII의 도입에 따라 유동층 분해(FCC) 촉매의 업그레이드가 진행되고 있으며, BASF의 Fourtiva가 방향족 화합물의 저감에 기여하고 있습니다. 일본에서는 100 RON의 프리미엄을 필요로 하는 하이브리드 차량이, 전체 휘발유 소비량은 감소하고 있음에도 불구하고 고옥탄가 휘발유 판매를 6% 증가시키는 요인이 되고 있습니다.

북미의 노킹 방지제 시장에서는 판매량이 안정적이지만, 옥탄가에 대한 수요 집중도가 높아지고 있습니다. 해당 지역에서 연중 E15를 도입하고, 캐나다의 청정 연료 규제가 에탄올과 바이오 MTBE의 사용을 촉진하고 있습니다. 멕시코에서는 관세 장벽이 낮아짐에 따라 MTBE 수입이 증가하고 있습니다. 전기차의 보급으로 미국의 휘발유 소비량은 연간 1.1% 감소하고 있지만, 터보 하이브리드 차량의 성장에 힘입어 프리미엄 등급 연료에 대한 강한 수요가 유지되고 있습니다.

유럽에서는 재생에너지 의무화 조치에 따라 진전이 나타나고 있습니다. 프랑스는 바이오 MTBE의 사용 비율을 6.8 부피%로 높였으며, 독일은 이산화탄소(CO2) 배출 규제에 대응하기 위해 12-15%의 혼합 비율을 목표로 하고 있습니다. 영국의 E10 기준에서는 여전히 97+RON 프리미엄 휘발유가 허용되고 있으며, 이에 대한 수요는 2025년에 9% 증가했습니다. 배터리 전기자동차(BEV)의 점유율이 92%에 달하는 노르웨이에서는 휘발유 소비량이 11% 감소했으며, 이는 노킹 방지제 시장 수요가 향후 프리미엄 부문으로 이동할 것임을 시사합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the antiknock agents market size is expected to increase from USD 3.44 billion in 2025 to USD 3.63 billion in 2026 and reach USD 4.75 billion by 2031, growing at a CAGR of 5.51% over 2026-2031.

This report is Segmented by Product Type (Ethanol, Tetraethyllead(tel), and More), Form (Liquid, Solid, and Additive Packages/Concentrates), Distribution Channel (OEM Supply, Bulk Terminal Injection, and More), Application (Automotive, Aviation, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Antiknock Agents Market Trends and Insights

Turbocharged Downsizing Requiring Higher Octane Fuels

With compression ratios of 11:1 or higher, 1.2 to 2.0 liter turbocharged engines operate near the limits of 91 Research Octane Number (RON) fuel. In 2025, 14 Original Equipment Manufacturers (OEMs) adopted the TOP TIER standard, mandating five times the Environmental Protection Agency's (EPA) detergent baseline to address injector deposits and low-speed pre-ignition. Research from Argonne National Laboratory indicates that increasing ethanol content from E10 to E15 reduces particulate number emissions by 18%. However, RON improvements plateau beyond E20 due to charge-cooling effects on flame speed. Consequently, premium fuel blenders are incorporating 10-12 volume percent (vol%) Ethyl Tertiary Butyl Ether (ETBE) into E10, achieving 95+ RON while adhering to the 7 pounds per square inch (psi) Reid vapor-pressure limit.

Rapid Motorization in Southeast Asia With Lax Aromatic Limits

Indonesia's Euro 4-equivalent regulations permit 45% aromatics and 1.5% benzene. This regulatory framework enables Pertamina to efficiently supply reformate-rich 92 RON gasoline. In 2025, gasoline consumption in Vietnam increased by 8.2%. However, with its refineries lacking Fluid Catalytic Cracking (FCC) upgrades, importers rely on aromatic naphtha from Korea and Singapore. While E20 has been introduced in Thailand, it accounts for only 12% of retail sales due to concerns about reduced mileage. Conversely, luxury hybrids require 95 RON or higher, creating a premium market for Methyl Tertiary Butyl Ether (MTBE) and ethanol.

Ethanol Price Volatility and US Blend-Wall Constraints

In January 2025, corn-ethanol prices increased from USD 1.85 per gallon to USD 2.62 by August, driven by a 14% yield reduction due to Midwestern droughts. Although the Environmental Protection Agency (EPA) approved year-round E15 at 3,800 stations, the E10 blend wall continues to limit additional demand. Rotterdam import prices rose to EUR 720 (USD 0.47) per m3 as Brazil redirected ethanol to domestic hydrous use.

Other drivers and restraints analyzed in the detailed report include:

- Bio-MTBE and Bio-ETBE Adoption to Meet EU Renewable Targets

- E-Fuel Pilot Projects Creating Drop-In Octane Demand

- Electric Vehicle Penetration Eroding Gasoline Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ethanol accounted for 39.11% of the antiknock agents market share in 2025, driven by Brazil's E27-E30 policy and the United States Renewable Fuel Standard, which supported demand. However, bio-based oxygenates are projected to experience the fastest growth in the antiknock agents market, with a CAGR of 6.17% through 2031. This growth is attributed to the Renewable Energy Directive III (RED III) double-counting of bio-ethyl tertiary-butyl ether (bio-ETBE) and the integration of sustainable aviation fuel (SAF) off-gas, which provides cost-effective isobutylene.

Liquid formulations accounted for 62.14% of the antiknock agents market share in 2025 and are projected to grow at a CAGR of 5.88%. This growth is attributed to their compatibility with pipelines and the convenience they offer in terminal dosing processes. Additionally, Chevron's inline analyzers contributed to operational efficiency by reducing octane giveaway by 0.4 points, which resulted in cost savings of USD 3.2 million in oxygenate expenses. These factors highlight the significant role of liquid formulations in the antiknock agents market.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.11% of the antiknock agents market revenue and is projected to grow at a CAGR of 6.28% through 2031. China's 300 million-vehicle fleet, along with its transition to 95 Research Octane Number (RON), is driving Methyl Tertiary Butyl Ether (MTBE) demand. In India, the implementation of Bharat Stage VII is leading to upgrades in Fluid Catalytic Cracking (FCC) catalysts, with BASF's Fourtiva supporting aromatic control. Japan's hybrid vehicles, requiring a 100 RON premium, have contributed to a 6% increase in high-octane sales, despite a decline in overall gasoline consumption.

North America's antiknock agents market is experiencing stable volumes but an increase in octane intensity. The region's year-round E15 adoption and Canada's Clean Fuel Regulations are supporting the use of ethanol and bio-MTBE. In Mexico, reduced tariff barriers have facilitated higher MTBE imports. While electric vehicle penetration is reducing U.S. gasoline consumption by 1.1% annually, the growth of turbo-hybrids is maintaining strong demand for premium-grade fuels.

Europe is progressing due to renewable mandates. France has increased its bio-MTBE usage to 6.8 vol%, while Germany is targeting a 12-15% blend for carbon dioxide (CO2) compliance. The United Kingdom's E10 baseline still allows for a 97+ RON premium, which grew by 9% in 2025. Norway, with a 92% share of battery electric vehicles (BEVs), has reduced gasoline consumption by 11%, indicating a future shift in antiknock agents market demand toward premium segments.

- Afton Chemical

- Baker Hughes Company

- BASF

- Braskem

- Chevron Oronite Company LLC

- China National Petroleum Corporation

- Evonik Industries AG

- Ifineum International Limited

- Innospec

- LyondellBasell Industries Holdings B.V.

- PetroChina Company Limited

- SABIC

- The Lubrizol Corporation

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Turbocharged downsizing requiring higher octane fuels

- 4.2.2 Rapid motorisation in SE-Asia with lax aromatic limits

- 4.2.3 Bio-MTBE and Bio-ETBE adoption to meet EU renewable targets

- 4.2.4 E-fuel pilot projects creating drop-in octane demand

- 4.2.5 SAF off-gas integration enabling co-produced bio-ethers

- 4.3 Market Restraints

- 4.3.1 Ethanol price volatility and US "blend-wall" constraints

- 4.3.2 Electric Vehicle penetration eroding gasoline demand base

- 4.3.3 Next-gen engine controls reducing octane requirement

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Ethanol

- 5.1.2 Tetraethyllead (TEL)

- 5.1.3 Methyl-Tert-Butyl Ether (MTBE)

- 5.1.4 Ethyl-Tert-Butyl Ether (ETBE)

- 5.1.5 Ethylbenzene and other Aromatics

- 5.1.6 Ferrocene and other metallics

- 5.1.7 Bio-based Oxygenates

- 5.1.8 Others

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid

- 5.2.3 Additive Packages/Concentrates

- 5.3 By Distribution Channel

- 5.3.1 Bulk Terminal Injection

- 5.3.2 OEM Supply

- 5.3.3 Retail Aftermarket

- 5.4 By Application

- 5.4.1 Automotive

- 5.4.2 Aviation

- 5.4.3 Industrial Engines

- 5.4.4 Petro-refining and Blending

- 5.4.5 Other Applications

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Afton Chemical

- 6.4.2 Baker Hughes Company

- 6.4.3 BASF

- 6.4.4 Braskem

- 6.4.5 Chevron Oronite Company LLC

- 6.4.6 China National Petroleum Corporation

- 6.4.7 Evonik Industries AG

- 6.4.8 Ifineum International Limited

- 6.4.9 Innospec

- 6.4.10 LyondellBasell Industries Holdings B.V.

- 6.4.11 PetroChina Company Limited

- 6.4.12 SABIC

- 6.4.13 The Lubrizol Corporation

- 6.4.14 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment