|

시장보고서

상품코드

2062190

군용 차량 전동화 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Military Vehicle Electrification - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

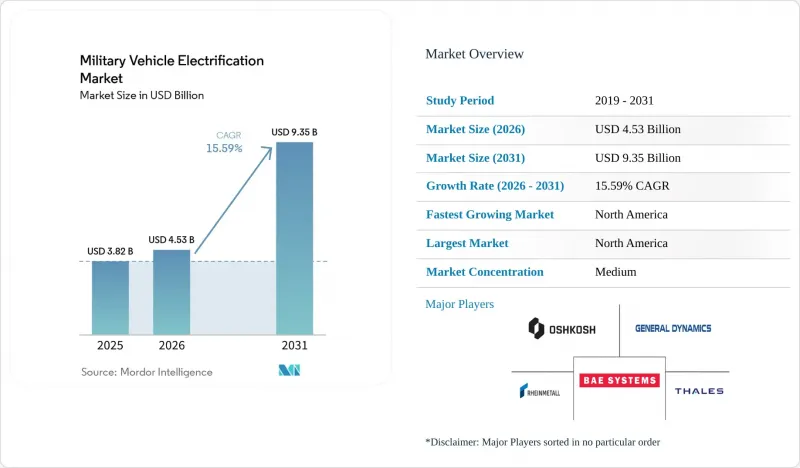

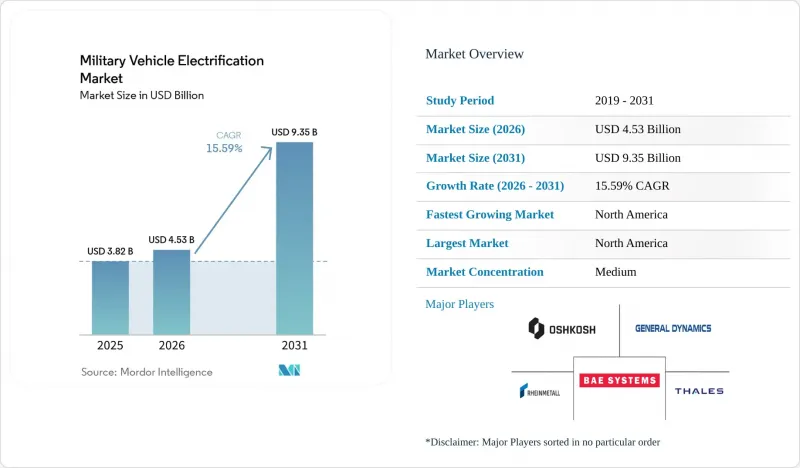

Mordor Intelligence에 의하면, 군용 차량 전동화 시장은 2025년에 38억 2,000만 달러로 평가되었고 2026년 45억 3,000만 달러에서 2031년까지 93억 5,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 15.59%로 성장할 전망입니다.

본 보고서는 추진 방식(하이브리드 전기식 및 완전 전기식), 플랫폼(전투 차량, 지원 차량, 무인 지상 차량), 시스템(발전, 냉각, 에너지 저장, 구동 시스템 등), 전압 등급(저전압, 중전압, 고전압), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 군용 차량 전동화 시장 동향과 인사이트

지상 차량 현대화 프로그램을 위한 국방 예산 증액

예산의 신속한 배분으로 인해 전례 없는 규모의 자금이 전동화에 투입되고 있습니다. 미 육군의 기후 전략은 2027년까지 비전술 차량의 완전한 전동화를 목표로 하고 있으며, GM 디펜스의 울티움(Ultium) 기술을 기반으로 한 첨단 배터리 팩을 통합한 M1E3 에이브럼스 프로그램을 시작으로 전술 플랫폼의 하이브리드화를 추진하고 있습니다. 이와 병행하여 유럽연합(EU)은 ‘ReArm Europe’ 계획의 일환으로 차세대 파워트레인 개발 자금으로 1,500억 유로(1,758억 3,000만 달러)를 확보하고, 전동화를 전력 증강을 위한 ‘전력 배가 요인’으로 규정하고 있습니다. 이러한 자금 풀은 고체 배터리 기술, 냉각 서브시스템, 전력 전자 장치에 대한 공급업체의 투자 위험을 완화하고, 군용 차량의 전동화 시장에서 전 세계적인 보급 속도를 가속화하고 있습니다.

방위 차량에 영향을 미치는 전 세계 배기가스 규제 및 연비 기준

대통령령 제14008호 및 제14057호는 미국 정부 기관에 대해 엄격한 일정에 따라 무공해 차량으로의 전환을 의무화하고 있으며, 이 지침은 국방부(DoD)의 방대한 전술 장비에도 영향을 미치고 있습니다. 나토(NATO) 회원국들은 GDP의 2%라는 국방비 지침에 이와 유사한 지속가능성 지표를 반영하고 있으며, 조달 부문에 하이브리드 차량과 전기차를 우선적으로 도입할 것을 요구하고 있습니다. 이러한 정책들은 은밀성, 열 신호 저감, 유지보수 비용 절감을 부가적인 이점으로 명시하고 있어, 군용 차량의 전동화 시장의 장기적인 성장 궤도를 강화하고 있습니다.

부족한 전술적 전력 공급 및 전장 전력 공급 인프라

미군 기지 내 레벨 3 충전기의 시범 도입은 진전을 보이고 있지만, 원정 부대에는 견고하고 전력망에 의존하지 않는 솔루션이 부족합니다. 태양광 발전과 발전기를 결합한 하이브리드 시스템이나 모듈형 리튬 배터리를 활용한 미국 국방부(DoD)의 마이크로그리드 시험은 실현 가능성을 보여주고 있으나, 대규모 도입을 위해서는 MIL 규격 인증과 교리 통합이 필요한 상황입니다. 휴대용 대용량 충전기가 상용화되기 전까지는 주행 거리에 대한 우려가 군용 차량의 전동화 시장 내 보급률을 저해할 것으로 보입니다.

부문별 분석

하이브리드 전기 시스템은 회생 제동, 주행 중 전력 공급 및 기존 연료 보급 방식과의 호환성을 활용하여 2025년 매출의 76.00%를 차지했습니다. 군용 차량의 전동화 시장에서 이 분야는 근본적인 인프라 개편 없이도 단기간 내에 차량 군을 업그레이드할 수 있게 해줍니다. 현재 규모는 작지만, 완전 전기식 플랫폼은 연평균 성장률(CAGR) 19.88%로 성장을 지속하고, 있으며, 한 번의 충전으로 장갑차가 임무 수행에 필요한 거리를 주행할 수 있게 해주는 배터리 기술의 발전 덕분에 성장세를 보이고 있습니다.

전투 플랫폼 부문은 M1E3 에이브럼스 및 박서(Boxer)의 하이브리드화 같은 주요 프로그램에 힘입어 2025년 수요의 48.97%를 차지했습니다. 새로운 센서 시스템 및 레이저 대응 조치에 필요한 전력 공급 요건은 전동화된 구동계와 자연스럽게 부합하며, 전투 차량은 군용 차량 전동화 시장의 성장 중심에 계속 자리 잡고 있습니다.

지원 및 후방 지원 차량은 2031년까지 연평균 성장률(CAGR)이 17.81%로 가장 빠르게 성장하고 있는 부문입니다. 이들은 모듈식 배터리 포드와 보조 인버터를 점점 더 통합하여, 야전 병원이나 레이더 기지에 전력을 공급할 수 있는 이동식 마이크로그리드를 형성하고 있습니다. 이러한 2차 수요 흐름은 수익 기회를 더욱 다각화시키고, 고가 전투 차량 수주에 따른 주기적인 변동으로부터 공급업체를 보호하는 역할을 하고 있습니다.

지역별 분석

2025년 매출의 51.62%를 차지한 북미 시장은 2031년까지 연평균 성장률(CAGR) 16.30%로 성장할 것으로 전망됩니다. 이러한 성장 추세는 배터리 표준화에서부터 공급망의 국내 복귀에 이르기까지 미국 국방부(DoD)의 투자 동향을 반영하고 있습니다. 차세대 전술 차량(하이브리드)이나 하이브리드화된 에이브럼스 전차와 같은 주목할 만한 프로그램들은 확장 가능한 전동화에 대한 확신을 뒷받침하고 있습니다. 또한, 한랭지 운용과 정숙성을 중시한 캐나다의 현대화 계획은 지역 기후 요인이 군용 차량의 전동화 분야 사양에 어떤 영향을 미치는지를 여실히 보여주고 있습니다.

한국, 일본, 호주에서는 대규모 현대화 노력이 아시아태평양의 성장을 견인하고 있으며, 각국은 에너지 자립을 추구하고 후방 지원으로 인한 환경 부담을 최소화하는 것을 목표로 하고 있습니다. 이 지역은 이러한 노력을 구체화하기 위해 정부 자금을 지원받아 수소 동력 장갑차와 고전압 지원 트럭의 시범 운행을 공개하고 있습니다. 이러한 노력은 군용 차량의 전동화 분야에서 기술적 전망을 다각화할 것으로 예측됩니다.

유럽의 동향은 공동 안보 및 방위 정책(CSDP)에 대한 자금 지원과 강화된 지속가능성 요건에 의해 주도되고 있습니다. 17억 유로(19억 9,000만 달러) 규모로 진행된 이베코 디펜스의 레오나르도 통합은 이탈리아가 유럽 내 지상 시스템 분야의 강자로서의 입지를 공고히 하고, 유럽 대륙 내 전기 구동계(electric drivetrain)의 폐쇄형 공급망을 가속화하고 있습니다. NATO의 철도 운송 규격 및 국경 간 기동성 기준에 기반한 상호운용성 요건은 회원국 간 수요를 더욱 조화시키고, 군용 차량의 전동화 시장에서 유럽 방위 블록의 집단적 협상력을 강화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the military vehicle electrification market was valued at USD 3.82 billion in 2025, and is projected to grow from USD 4.53 billion in 2026 to reach USD 9.35 billion by 2031, at a 15.59% CAGR over 2026-2031.

This report is Segmented by Propulsion Type (Hybrid-Electric and Fully Electric), Platform (Combat Vehicles, Support Vehicles, and Unmanned Ground Vehicles), System (Power Generation, Cooling, Energy Storage, Traction Drive, and More), Voltage Class (Low, Medium, and High), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Military Vehicle Electrification Market Trends and Insights

Increased Defense Funding for Ground Vehicle Modernization Programs

Accelerated appropriations are channeling unprecedented sums into electrification. The US Army's climate strategy pursues an all-electric non-tactical fleet by 2027 and hybridized tactical platforms beginning with the M1E3 Abrams program, which integrates an advanced battery pack derived from GM Defense's Ultium technology. In parallel, the European Union earmarked EUR 150 billion (USD 175.83 billion) within its ReArm Europe framework to seed next-generation powertrains, positioning electrification as a force multiplier for readiness. Such funding pools de-risk supplier investment in solid-state chemistry, cooling subsystems, and power electronics, accelerating the global adoption curve of the military vehicle electrification market.

Global Emissions and Fuel-Efficiency Standards Influencing Defense Fleets

Federal Executive Orders 14008 and 14057 require US government agencies to transition to zero-emission vehicles on aggressive timelines, a mandate that affects the Department of Defense's (DoD's) vast tactical inventory. NATO members embed similar sustainability metrics into the 2% of GDP defense-spending guideline, compelling procurement offices to favor hybrid and electric variants. These policies codify stealth, reduced thermal signature, and lower maintenance overhead as co-benefits, reinforcing the long-run growth trajectory of the military vehicle electrification market.

Insufficient Tactical Charging and Battlefield Refueling Infrastructure

Pilot installations of Level-3 chargers on US bases underscore progress, yet expeditionary forces lack ruggedized, grid-independent solutions. DoD microgrid tests using solar-generator hybrids and modular lithium packs indicate feasibility, but large-scale deployment awaits MIL-spec certification and doctrinal integration. Until portable high-capacity chargers are ready, range anxiety will temper adoption rates in the military vehicle electrification market.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in High-Energy-Density Lithium and Solid-State Batteries

- Operational Savings from Reduced Fuel Logistics and Supply-Chain Dependencies

- High Initial Costs for Procurement and Retrofitting of Electric Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid-electric systems generated 76.00% of 2025 revenue, leveraging regenerative braking, on-the-move power export, and compatibility with existing refueling doctrine. This portion of the military vehicle electrification market supports near-term fleet upgrades without demanding radical infrastructure overhaul. Though smaller today, fully electric platforms are posting an 19.88% CAGR and benefit from advances in cell chemistry that enable armored vehicles to travel mission-relevant distances on a single charge.

Combat platforms accounted for 48.97% of 2025 demand, propelled by marquee programs such as the M1E3 Abrams and the Boxer hybridization effort. The requirement for exportable electrical power to new sensor suites and laser countermeasures aligns naturally with electrified drivelines, keeping combat vehicles central to growth in the military vehicle electrification market.

Support and logistics vehicles are the fastest-growing segment, with a 17.81% CAGR through 2031, as they increasingly integrate modular battery pods and auxiliary inverters, creating rolling microgrids capable of powering field hospitals and radar stations. This secondary demand stream further diversifies revenue opportunities and cushions suppliers against the cyclicality of big-ticket combat vehicle awards.

Geography Analysis

North America, which accounted for 51.62% of 2025 revenue, is projected to grow at a 16.30% CAGR through 2031. This growth trajectory mirrors the DoD's investments, spanning from battery standardization to supply-chain onshoring. Notable programs like the Next-Generation Tactical Vehicle-Hybrid and the hybridized Abrams underscore the confidence in scalable electrification. Furthermore, Canada's modernization initiatives, prioritizing cold-weather and silent mobility, highlight how regional climate factors influence specifications in the military vehicle electrification arena.

In South Korea, Japan, and Australia, large-scale modernization efforts are fueling growth in the Asia-Pacific region, with each nation pursuing energy independence and aiming to minimize logistics footprints. Demonstrating its commitment, the region has showcased government-funded trials of hydrogen-powered armored vehicles and high-voltage support trucks. Such initiatives are set to diversify the technological landscape of the military vehicle electrification sector.

Europe's trajectory is guided by funding for the Common Security and Defence Policy and by tightened sustainability mandates. The EUR 1.7 billion (USD 1.99 billion) integration of Iveco Defence into Leonardo cements Italy's position as a European land-systems powerhouse and accelerates the continent's closed-loop supply of electrified drivetrains. Interoperability requirements under NATO rail-carriage dimensions and cross-country mobility standards further harmonize demand across member states, elevating the collective bargaining power of the European defense bloc within the military vehicle electrification market.

- Oshkosh Corporation

- General Motors Company

- General Dynamics Corporation

- BAE Systems plc

- Leonardo S.p.A.

- Textron Inc.

- Singapore Technologies Engineering Ltd.

- QinetiQ Group plc

- Rheinmetall AG

- Thales Group

- KNDS N.V.

- FNSS Savunma Sistemleri A.S.

- Arquus (John Cockerill Group)

- Patria Group

- Allison Transmission Holdings, Inc.

- Hyundai Rotem Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological advancements in high-energy-density lithium and solid-state batteries

- 4.2.2 Rising onboard power requirements for directed-energy and C4ISR systems

- 4.2.3 Increased defense funding for ground vehicle modernization programs

- 4.2.4 Operational savings from reduced fuel logistics and supply chain dependencies

- 4.2.5 Tactical benefits of silent mobility for ISR and electronic warfare operations

- 4.2.6 Global emissions and fuel efficiency standards influencing defense fleets

- 4.3 Market Restraints

- 4.3.1 Supply chain vulnerabilities in critical minerals under defense procurement policies

- 4.3.2 Insufficient tactical charging and battlefield refueling infrastructure

- 4.3.3 High initial costs for procurement and retrofitting of electric platforms

- 4.3.4 Thermal signature risks associated with large-capacity battery systems

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Propulsion Type

- 5.1.1 Hybrid-Electric

- 5.1.2 Fully Electric

- 5.2 By Platform

- 5.2.1 Combat Vehicles

- 5.2.2 Support Vehicles

- 5.2.3 Unmanned Ground Vehicles (UGVs)

- 5.3 By System

- 5.3.1 Power Generation

- 5.3.2 Cooling

- 5.3.3 Energy Storage

- 5.3.4 Traction Drive

- 5.3.5 Power Conversion

- 5.3.6 Transmission

- 5.4 By Voltage Class

- 5.4.1 Low (Less than 50 V)

- 5.4.2 Medium (50 V to 600 V)

- 5.4.3 High (Greater than 600 V)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Oshkosh Corporation

- 6.4.2 General Motors Company

- 6.4.3 General Dynamics Corporation

- 6.4.4 BAE Systems plc

- 6.4.5 Leonardo S.p.A.

- 6.4.6 Textron Inc.

- 6.4.7 Singapore Technologies Engineering Ltd.

- 6.4.8 QinetiQ Group plc

- 6.4.9 Rheinmetall AG

- 6.4.10 Thales Group

- 6.4.11 KNDS N.V.

- 6.4.12 FNSS Savunma Sistemleri A.S.

- 6.4.13 Arquus (John Cockerill Group)

- 6.4.14 Patria Group

- 6.4.15 Allison Transmission Holdings, Inc.

- 6.4.16 Hyundai Rotem Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment