|

시장보고서

상품코드

2062247

고강도 알루미늄 합금 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)High Strength Aluminum Alloys - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

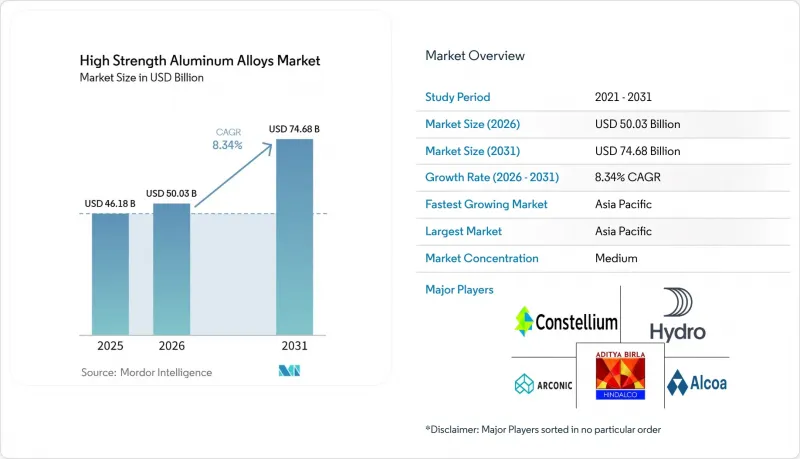

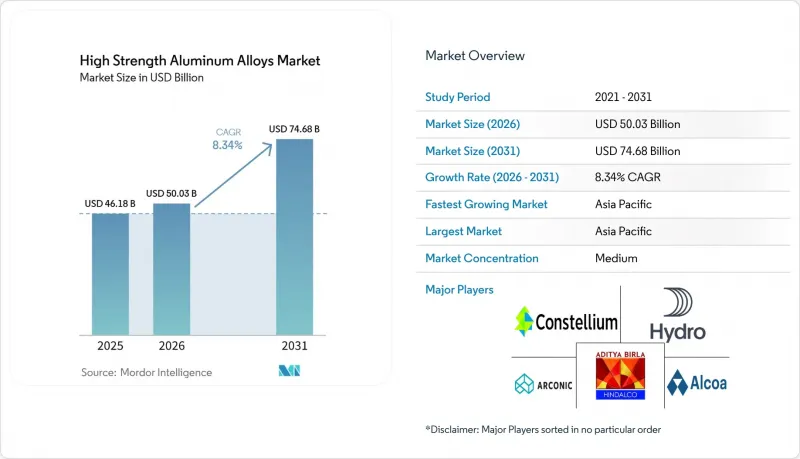

Mordor Intelligence에 의하면, 고강도 알루미늄 합금 시장 규모는 2025년 461억 8,000만 달러로 평가되었습니다. 2026년 500억 3,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR은 8.34%를 나타내, 2031년까지 746억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 등급(6xxx 계열, 기타), 제품 형태(플레이트 및 시트, 기타), 가공 기술(열처리, 기타), 최종 사용자 산업(항공우주 및 방위, 자동차 및 운송, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 고강도 알루미늄 합금 시장 동향 및 분석

항공우주 및 방위 부문에서 경량화에 대한 수요가 증가하고 있습니다.

항공기 제조업체들은 엄격한 연료 소비 목표를 달성하기 위해 새로운 플랫폼에 고강도 알루미늄 합금 시장 사양을 도입하고 있습니다. 보잉과 에어버스는 2026년에 단일 통로기 생산 대수를 각각월38대와 75대로 늘렸으며, 각 기체의 동체 외판에는 800kg 이상의 7xxx계 및 2xxx계 강판이 사용되고 있습니다. 해군 프로그램에서는 미국 해군의 DDG-51 Flight III형 구축함이 상부 구조물의 무게를 12% 줄이기 위해 5xxx계 선박용 판재의 사용을 의무화하고 있으며, 이를 통해 안정성을 저해하지 않으면서도 더 무거운 레이더 시스템을 탑재할 수 있게 되었습니다. 스페이스X(SpaceX) 등 로켓 제조업체들은 재사용형 단에 Al-Li 스트링거를 채택하여, 반복되는 극저온 사이클을 견딜 수 있도록 하고 있습니다. 유럽 항공안전청(EASA)과 연방항공청(FAA) 등 규제 당국은 AMS 4999 및 AMS 7003 규정을 철저히 준수하고 있으며, 이에 따라 제철사들은 공정 관리를 강화해야 하는 상황에 놓여 있습니다. 이러한 누적된 영향으로 인해 수년에 걸친 수요 전망을 예측하기가 쉬워졌으며, 통합 제조업체들은 최종 조립 라인 인근에서 단조 및 열처리 능력을 확대하도록 장려받고 있습니다.

전기차용 배터리 케이스 및 플랫폼에서의 적용 확대

자동차 설계자들은 배터리의 무게를 상쇄하기 위해 알루미늄을 많이 사용한 언더바디로 전환하고 있습니다. 노벨리스는 2025년에 50만 톤 이상의 6xxx 계열 자동차용 시트를 출하했는데, 그중 절반은 IIHS 충돌 테스트 프로토콜에서 강판을 능가하는 성능을 발휘하는 배터리 인클로저용이었습니다. 일체형 압출 트레이는 최대 40개의 패스너 사용을 없애고, 조립 시간을 15% 단축할 뿐만 아니라, 침수로 인한 보증 청구 건수도 줄여줍니다. 중국 공업정보화부(MIIT)는 100km당 12kWh 이하의 전기차에 보조금을 지급하고 있으며, 이를 통해 각 OEM 업체들이 BYD Seal과 같이 알루미늄을 많이 사용한 플랫폼으로 전환하도록 장려하고 있습니다. 프레스 경화강에 비해 두꺼운 판재가 필요하지만, 차량 총중량을 80-100kg 줄일 수 있으므로, 차량 1대당 150-200달러의 재료비 증가는 정당화됩니다. 각 공급업체는 설계 반복 기간을 단축하기 위해 OEM 공장 근처에 압출 성형, 프레스 가공, 마찰 교반 접합 생산 라인을 집약하고 있습니다.

높은 가공 비용과 중요한 합금 원소

최대 530°C에서 진행되는 용체화 열처리 및 인위적 시효 처리에는 1톤당 1,500kWh의 전력을 소비하기 때문에 유럽의 제련소는 2024년에 전력 가격을 40%나 끌어올린 에너지 위기의 영향을 받기 쉬운 상황입니다. 스칸듐 마스터 합금은 1kg당 약 4,000달러에 거래되고 있으며, 이는 알루미늄 가격의 200배에 달하기 때문에 그 경제적 타당성은 항공우주용 격벽이나 극저온 탱크로 한정되어 있습니다. 리튬 가격도 톤당 1만 2,000-1만 5,000달러로 높은 수준을 유지하고 있어, 원가 구조에 부담을 주고 있습니다. 게다가, 지정학적 공급 집중이 위험을 높이고 있습니다. 카이저 알루미늄은 감당하기 어려운 전기 요금을 이유로 스포캔의 열처리 라인을 폐쇄했습니다. 이는 재생에너지를 운영하는 통합 생산자만이 톤당 1,800달러 이하의 현금 원가를 달성할 수 있는 양극화된 시장의 실태를 여실히 보여주고 있습니다.

부문별 분석

6xxx 시리즈는 여전히 수량 기준 1위를 차지하고 있으며, 전기차용 배터리 케이스 계약 및 철도 차량용 압출재 수요를 바탕으로 2025년에는 39.65%의 시장 점유율을 확보했습니다. 비용 효율이 높은 스칸듐을 미량 첨가함으로써 충돌 안전성을 저해하지 않으면서 6xxx 시리즈의 단면 두께를 얇게 만들 수 있으므로, 고강도 알루미늄 합금 시장 점유율 우위는 축소될 것으로 예측됩니다. 한편, 2xxx 계열과 5xxx 계열은 각각 기존 와이드 바디 항공기 및 극저온 탱크와 같은 틈새 시장에서 우위를 유지하고 있으며, 연구 개발비의 대부분은 차세대 재사용형 로켓용 알루미늄-리튬 하이브리드 소재 개발에 투입되고 있습니다.

7xxx 시리즈는 2031년까지 연평균 성장률(CAGR) 9.22%를 나타낼 것으로 전망됩니다. 높은 아연 함량 덕분에 570 MPa를 초과하는 극한 인장 강도를 얻을 수 있으며, 이는 기체 프레임이나 해군용 레이더 마스트에 필수적입니다. 보잉과 에어버스의 생산량 급증으로 인해 2030년까지의 선임베디드 계약이 확고해졌으며, 제련소의 가동률이 안정적으로 유지될 것이 보장되고 있습니다. 또한, 적층 가공(AM)의 보급으로 인해 7xxx 시리즈에 대한 수요는 더욱 증가하고 있습니다. 이는 LPBF(레이저 분말 소결법)가 HIP(열간 압밀) 처리 후의 밀도에서 단조판의 밀도와 0.5% 이내의 차이를 보이도록 실현했기 때문입니다.

2025년에는 항공기 외판, 철도 차량 지붕, 전기차 차체 패널용으로 공급된 판재 및 시트가 매출의 41.02%를 차지했습니다. 그러나 분말, 박막, 선재는 적층 가공 및 고체 전지 수요 증가를 배경으로 연평균 성장률(CAGR) 9.57%를 기록하며 이들보다 높은 성장세를 보일 것으로 전망됩니다. 고체 전지 개발 기업들이 10-20마이크론 두께의 집전막을 지정하고 있는 만큼, 2026년부터 2031년에 걸쳐 초초박형 전지용 박판 전용 고강도 알루미늄 합금 시장 규모는 대폭 확대될 것으로 전망됩니다.

압출 성형품은 중량 대비 강성 면에서 경제성이 뛰어나고 용접 기술도 성숙되어 있어, 자동차 및 건축 부문을 지속적으로 뒷받침하고 있습니다. 한편, 단조품은 결정립의 배향이나 피로 수명이 비용보다 더 중요하게 여겨지는 초고신뢰성이 요구되는 틈새 시장인 착륙 장치 및 선박용 샤프트 부문에서 확고한 입지를 다지고 있습니다. 그럼에도 불구하고, 경량화 요구에 따라 자본은 분말 분무 및 초박판 압연 기술로 이동하고 있으며, 이는 반가공 제조업체 간의 수익성 순위에 재편을 가져오고 있습니다.

지역별 분석

아시아태평양은 2025년 수요의 44.69%를 차지했으며, 중국의 철도망 확충과 일본의 항공우주용 단조품 수출 프로그램에 힘입어 2031년까지 연평균 성장률(CAGR) 9.56%를 나타낼 전망입니다. 인도 구자라트주와 마하라슈트라주에 위치한 압출 성형 거점은 물류 비용을 상쇄하기 위해 인건비 경쟁력을 활용하여 유럽의 1차 공급업체에 제품을 공급하고 있습니다. OEM 업체들이 중국에 대한 의존도를 낮추는 가운데, 동남아시아 국가들은 대체 공급처로 나설 기회를 모색하고 있습니다.

북미에서는 리쇼어링 요구에 따라 생산 능력을 확대되고 있습니다. 알코어의 생 시프리앙 공장의 재건과 노벨리스의 베이 미넷 공장을 통해 2027년까지 연간 총 67만 5,000톤 규모의 시트 및 단조품 생산 능력이 추가될 예정입니다. 방위 예산 덕분에 7xxx계 강재의 수주 실적이 견조한 추세를 보이고 있는 반면, 미국 인프라법에는 6xxx계 압출재를 대량으로 소비하는 철도 현대화 사업이 배정되어 있습니다.

유럽에서는 적극적인 탄소 감축 정책과 자동차 경량화가 양립하고 있습니다. 노르스크 하이드로의 수력 발전 제련소는 CBAM 감면 조치의 대상이 되는 고품질의 저탄소 빌렛을 공급하고 있습니다. 철도 회랑에 대한 투자와 OEM을 통한 다종 소재 차체 채택으로 인해, 제철소는 두꺼운 강판, 압출재, 박판 등의 특수 제품을 균형 있게 생산해야 합니다. 남미와 중동은 규모는 작지만, LNG 운반선 및 해상 풍력 발전 지원선용 5xxx계 두꺼운 강판 수요를 끌어모으고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the high strength aluminum alloys market size is expected to grow from USD 46.18 billion in 2025 to USD 50.03 billion in 2026 and is forecast to reach USD 74.68 billion by 2031 at 8.34% CAGR over 2026-2031.

This report is Segmented by Grade (6xxx Series, and More), Product Form (Plates and Sheets, and More), Processing Technique (Heat-Treated, and More), End-User Industry (Aerospace and Defense, Automotive and Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global High Strength Aluminum Alloys Market Trends and Insights

Growing Demand from Aerospace and Defense for Lightweighting

Airframe manufacturers are embedding high strength aluminum alloys market specifications into new platforms to hit stringent fuel-burn targets. Boeing and Airbus increased single-aisle build rates to 38 and 75 units per month, respectively, in 2026, each fuselage skin containing more than 800 kg of 7xxx and 2xxx plate. In naval programs, the U.S. Navy's DDG-51 Flight III destroyer mandates 5xxx-series marine plate to cut topside weight by 12%, permitting heavier radar systems without compromising stability. Rocket manufacturers such as SpaceX employ Al-Li stringers in reusable stages to survive repeated cryogenic cycles. Regulators at the European Union Aviation Safety Agency (EASA) and the Federal Aviation Administration (FAA) enforce AMS 4999 and AMS 7003 compliance, driving mills to tighten process control. The cumulative effect lifts multi-year demand visibility, incentivizing integrated producers to expand forging and heat-treat capacity adjacent to final-assembly lines.

Increasing Adoption in EV Battery Enclosures and Platforms

Automotive architects are converging on aluminum-intensive underbodies to offset battery mass. Novelis shipped more than 500,000 tons of 6xxx automotive sheet in 2025, half earmarked for battery enclosures that outperform steel in IIHS crash protocols. One-piece extrusion trays eliminate up to 40 fasteners, cutting assembly time 15% and reducing warranty claims tied to water ingress. China's MIIT awards subsidies to EVs under 12 kWh/100 km, nudging OEMs toward aluminum-rich platforms like BYD Seal. While thicker gauges are needed versus press-hardened steel, total curb-weight savings of 80-100 kg justify a USD 150-200 per vehicle material premium. Suppliers co-locate extrusion, stamping, and friction-stir welding cells near OEM plants to shorten design iterations.

High Cost of Processing and Critical Alloying Elements

Solution heat treatment at up to 530°C and artificial aging regimes consume 1,500 kWh per ton, exposing European mills to energy shocks that pushed electricity prices 40% higher in 2024. Scandium master alloy trades around USD 4,000/kg, 200 times base aluminum, restricting economic viability to aerospace bulkheads or cryogenic tanks. Lithium at USD 12,000-15,000/ton also stresses cost structures, and geopolitical concentration heightens risk. Kaiser Aluminum shuttered its Spokane heat-treat line, citing unsustainable power tariffs, underscoring a two-tier market where only integrated producers running renewable power can achieve sub-USD 1,800/ton cash costs.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of High-Speed Rail and Urban Transit Projects

- Lightweighting Push in Construction and Industrial Equipment

- Weldability and Stress-Corrosion Sensitivities in Some Grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 6xxx series remains the volume leader, securing 39.65% market share in 2025 on the back of EV battery-enclosure contracts and rail-car extrusions. The high-strength aluminum alloys market share advantage is expected to narrow as cost-effective scandium micro-additions enable thinner 6xxx profiles without sacrificing crashworthiness. Meanwhile, 2xxx and 5xxx series maintain niche defensibility in legacy wide-body aircraft and cryogenic tanks, respectively, with research and development dollars mostly channeling toward aluminum-lithium hybrids for next-generation reusable launchers.

The 7xxx series is projected to expand at 9.22% CAGR to 2031. High zinc content delivers ultimate tensile strength above 570 MPa, indispensable for fuselage frames and naval radar masts. Boeing's and Airbus's production surges anchor forward-purchase agreements through 2030, ensuring consistent mill utilization. Additive manufacturing further lifts 7xxx demand as LPBF achieves density within 0.5% of wrought plate after HIP consolidation.

Plates and sheets delivered 41.02% revenue share in 2025 by serving aircraft skins, rail roofs, and EV body panels. However, powders, foils, and wires are forecast to outpace with a 9.57% CAGR, riding on additive manufacturing and solid-state battery opportunities. The high-strength aluminum alloys market size for ultra-thin battery foil alone is projected to increase significantly between 2026 and 2031 as solid-state developers specify 10-20 micron collectors.

Extrusions continue to underpin automotive and building segments thanks to favorable weight-to-stiffness economics and mature welding methods. Forgings secure ultra-high reliability niches, landing gear, and naval shafts, where grain-flow orientation and fatigue life trump cost. Mass-reduction imperatives nonetheless steer capital toward powder atomization and ultra-thin rolling capabilities, reshuffling the profitability hierarchy among semi-fabricators.

Geography Analysis

Asia-Pacific held 44.69% of 2025 demand and will compound at 9.56% CAGR through 2031, fueled by China's rail build-out and Japan's aerospace forgings export program. India's extrusion hubs in Gujarat and Maharashtra supply European tier-1s, leveraging labor advantages to offset logistics costs. Southeast Asian nations chase substitution opportunities as OEMs de-risk China exposure.

North America scales capacity under reshoring mandates: Alcoa's San Ciprian rebuild, and Novelis's Bay Minette mill inject a combined 675,000 tons of annual sheet and forging output by 2027. Defense budgets channel steady 7xxx orders, while the U.S. Infrastructure Act allocates rail modernizations that consume 6xxx extrusions.

Europe balances aggressive carbon policy with automotive lightweighting. Norsk Hydro's hydropower smelters supply premium low-carbon billet, qualifying for CBAM relief. Rail corridor investments and OEM multi-material bodies force mills to juggle plate, extrusion, and foil specialties. South America and the Middle East stay sub-scale but attract 5xxx plate demand for LNG carriers and offshore wind-support vessels.

- Akshay Aluminium Alloys

- Alcoa Corporation

- Aluminum Corporation of China (Chalco)

- AMAG Austria Metall AG

- Arconic

- Belmont Metals

- Constellium SE

- ElvalHalcor

- Emirates Global Aluminium PJSC

- Fischer Group

- GARMCO

- Granges

- Hindalco Industries Ltd.

- Kaiser Aluminum Corp.

- KOBE STEEL, LTD.

- Norsk Hydro ASA

- Rio Tinto

- UACJ Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from aerospace and defence for lightweighting

- 4.2.2 Increasing adoption in EV battery enclosures and platforms

- 4.2.3 Expansion of high-speed rail and urban transit projects

- 4.2.4 Light-weighting push in construction and industrial equipment

- 4.2.5 Uptake in cryogenic hydrogen-storage vessels (H2 economy)

- 4.2.6 Demand from satellite constellations and re-usable launchers

- 4.3 Market Restraints

- 4.3.1 High cost of processing and critical alloying elements

- 4.3.2 Weldability and stress-corrosion sensitivities in some grades

- 4.3.3 Competition from advanced steels and carbon-composite hybrids

- 4.3.4 Supply-risk of scandium/lithium for ultra-high-strength series

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 6xxx Series (Al-Mg-Si)

- 5.1.2 2xxx Series (Al-Cu)

- 5.1.3 5xxx Series (Al-Mg)

- 5.1.4 7xxx Series (Al-Zn)

- 5.1.5 Other High-Strength Grades (Sc, Li-Al, and More)

- 5.2 By Product Form

- 5.2.1 Plates and Sheets

- 5.2.2 Extrusions

- 5.2.3 Forgings

- 5.2.4 Castings

- 5.2.5 Bars, Rods and Tubes

- 5.2.6 Other Forms (Powders, Foils, and Wires)

- 5.3 By Processing Technique

- 5.3.1 Heat-Treated

- 5.3.2 Non-Heat-Treated

- 5.3.3 Cold-Worked

- 5.3.4 Powder Metallurgy and Additive Manufacturing

- 5.4 By End-user Industry

- 5.4.1 Aerospace and Defence

- 5.4.2 Automotive and Transportation

- 5.4.3 Marine and Shipbuilding

- 5.4.4 Construction and Infrastructure

- 5.4.5 Electronics and Electrical

- 5.4.6 Industrial Equipment

- 5.4.7 Other End-users (Energy and Packaging)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.5.4 Rest of MEA

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)}

- 6.4.1 Akshay Aluminium Alloys

- 6.4.2 Alcoa Corporation

- 6.4.3 Aluminum Corporation of China (Chalco)

- 6.4.4 AMAG Austria Metall AG

- 6.4.5 Arconic

- 6.4.6 Belmont Metals

- 6.4.7 Constellium SE

- 6.4.8 ElvalHalcor

- 6.4.9 Emirates Global Aluminium PJSC

- 6.4.10 Fischer Group

- 6.4.11 GARMCO

- 6.4.12 Granges

- 6.4.13 Hindalco Industries Ltd.

- 6.4.14 Kaiser Aluminum Corp.

- 6.4.15 KOBE STEEL, LTD.

- 6.4.16 Norsk Hydro ASA

- 6.4.17 Rio Tinto

- 6.4.18 UACJ Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Next-gen alloy development for aerospace electrification and EV batteries