|

시장보고서

상품코드

2062262

기업 소셜 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Enterprise Social Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

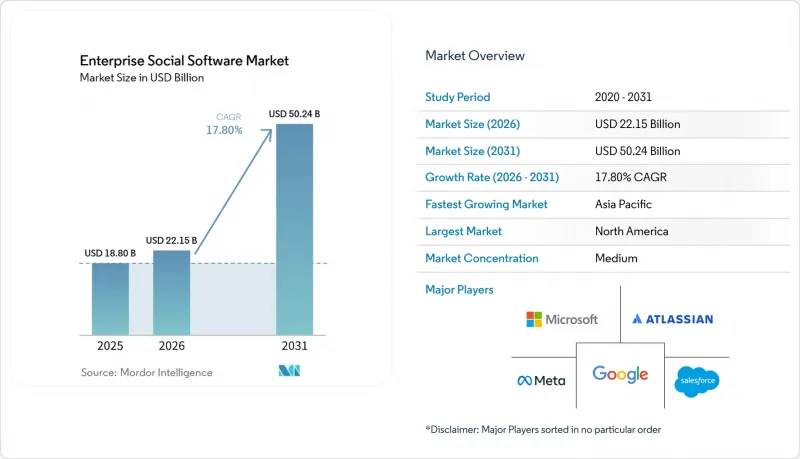

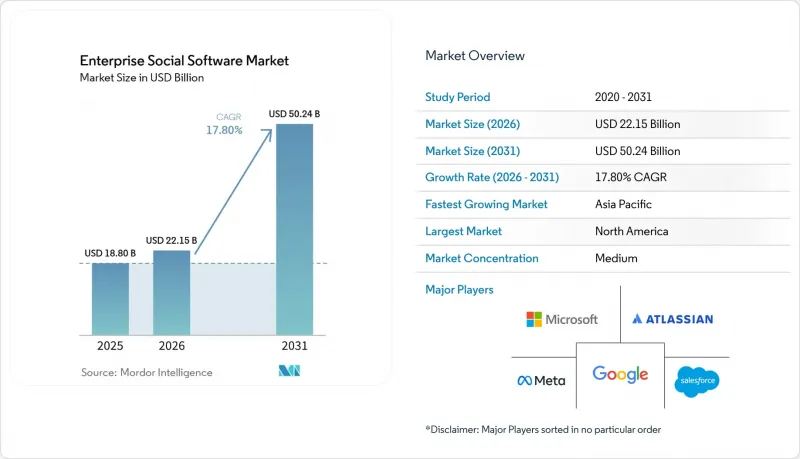

Mordor Intelligence에 의하면, 기업 소셜 소프트웨어 시장 규모는 2025년에 188억 달러, 2026년에 221억 5,000만 달러가 되어, 2031년까지 502억 4,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 17.8%로 성장할 것으로 전망됩니다.

본 보고서는 기능 모듈(사내 커뮤니케이션, 직원 평가 및 웰니스, 기타), 조직 규모(중소기업, 대기업), 제공 채널(모바일 우선, 웹 브라우저, 기타), 업종(헬스케어, IT 및 통신, 소매 및 전자상거래, 기타), 지역(북미, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 기업 소셜 소프트웨어 시장 동향과 인사이트

지속적인 하이브리드 근무 문화

하이브리드 근무 체제는 표준 운영 모델이 되었으며, 4곳 중 3곳의 기업이 공식적인 거점 분산 정책을 유지하고 있습니다. 이러한 추세가 자리 잡으면서 이메일과 회의 중심의 협업 방식의 한계가 드러났고, 2024년부터 2025년까지 비동기형 도구에 대한 예산이 91% 증가했습니다. IT 및 통신과 같은 지식 집약적 분야에서는 사고 대응이나 코드 검토를 위해 영구적으로 보관되고 검색이 가능한 토론 스레드가 필요하기 때문에 도입이 가속화되었습니다. 마이크로소프트공급업체가 2026년에 Viva Engage 커뮤니티를 Teams 내에 직접 통합하기로 결정한 것은 컨텍스트 전환이 사용자 참여를 저해한다는 회사의 인식을 여실히 보여주고 있습니다. 채팅, 컨텐츠, 업무를 하나의 AI 기반 허브로 통합하지 못하는 조직은 직원들이 업무 관련 업무에 시간의 60%를 소비하게 될 위험을 감수하게 됩니다. 이것이 2031년까지 플랫폼 통합이 더욱 가속화될 것으로 예상되는 이유입니다.

TCO 절감을 위한 SaaS 도입 확대

클라우드 전환은 당초 설비 투자 부담을 줄여줄 것으로 기대되었으나, AI 애드온의 높은 가격 책정으로 인해 운영 예산이 급증하고 있습니다. 현재 Salesforce와 Microsoft는 생성형 AI 기능에 대해 사용자당월30-60달러를 청구하고 있으며, 재무 부서는 구독의 총 소유 비용을 재검토해야 하는 상황에 직면해 있습니다. Zoho와 같은 벤더들은 AI를 기본 요금제에 포함시키고, 중소기업에 매력적이고 예측 가능한 가격 정책을 제공함으로써 비용에 민감한 고객들을 확보하고 있습니다. On-Premise 환경을 한 번도 도입한 적이 없는 기업이 많은 아시아태평양의 기업들은 SaaS로 직접 전환하며, 소비자 경험을 반영한 모바일 우선 제품군을 선호하고 있습니다. 그럼에도 불구하고, 토큰 소비량에 연동된 종량제 요금제는 예측의 변동성을 초래하고 있으므로, 회계 담당자는 2027년 및 2028년 예산에 이를 반영해야 합니다.

데이터 주권과 개인정보 보호 위험

GDPR(EU 개인정보보호규정) 및 이와 유사한 법률은 엄격한 데이터 소재지 규정을 의무화하고 있어, 세계 사업 확장을 복잡하게 만들고 있습니다. 국경을 넘는 데이터 전송에 따른 규제 문제를 피하기 위해 유럽 기업들의 주권 클라우드 영역에 대한 투자 비중이 증가함에 따라, 호스팅 비용이 상승하고 조달 주기가 길어지고 있습니다. 다국적 기업은 관할 구역별로 사용자 트래픽을 세분화해야 하며, 이로 인해 아키텍처가 복잡해져 도입이 지연될 수 있습니다. 플랫폼 공급업체들은 지역 내 데이터센터와 세분화된 암호화 키를 활용해 이 문제에 대응하고 있지만, 일부 구매자들은 규정 준수 여부가 확인될 때까지 구매를 보류하고 있습니다. 이러한 추세로 인해, 개인정보 보호에 민감한 분야의 기업 소셜 소프트웨어 시장 성장세가 둔화되고 있습니다.

부문별 분석

지식 탐색 분야의 생성형 AI는 연평균 성장률(CAGR) 21.20%라는 놀라운 성장세를 보이고 있습니다. 이 성장률은 기업 소셜 소프트웨어 시장 전체를 상회하며, 그 중요성이 커지고 있음을 여실히 보여주고 있습니다. 2025년까지 사내 커뮤니케이션이 기업 소셜 소프트웨어 시장 점유율의 40.70%를 차지할 것으로 예측됩니다. 그러나 조직이 예산을 고도화된 모듈로 전환함에 따라, 그 우위는 약화될 것으로 예측됩니다. 이 모듈들은 전문 지식을 자동으로 추출하거나 방대한 문서 저장소를 요약하는 데 중점을 두고 있어, 지식 관리 분야의 효율성 향상에 대한 증가하는 수요에 부응하고 있습니다. 이러한 변화는 기업들이 생산성을 높이고 중요한 정보에 대한 접근을 효율화하는 도구를 우선시하는 보다 광범위한 추세를 반영하고 있습니다.

현재, 체계화되지 않은 조직의 기록은 직원 1인당 하루 평균 1.8시간의 검색 시간이 소요되어 비효율성을 초래하고 있습니다. 기업들은 이 잃어버린 시간을 실질적인 인사이트으로 전환하여, 생산성을 높이는 솔루션에 적극적으로 투자하고 있습니다. 또한, 환경·사회·지배구조(ESG)의 우선순위와 부합한다는 점에서 시상 및 웰니스 관련 모듈이 주목을 받고 있습니다. 한편, 아이디어 창출 허브는 여전히 연구개발(R&D) 집약형 분야에서 주로 활용되고 있습니다. 게다가 프로젝트 협업 및 파일 공유 기능이 생산성 제품군에 통합되는 추세가 강해지면서, 독립형 벤더들은 차별화를 꾀할 수밖에 없는 상황에 처해 있습니다. 이러한 벤더들은 급변하는 시장 환경에서 경쟁력을 유지하기 위해 업계 고유의 워크플로우와 AI의 설명 가능성 향상에 주력하고 있습니다.

2025년 매출 점유율의 56.60%를 대기업이 차지했으나, 중소기업(SME)은 연평균 성장률(CAGR) 18.60%로 성장하고 있어 이용 격차는 점차 줄어들고 있습니다. 중소기업 기업 소셜 소프트웨어 시장 규모는 소규모 기업들이 On-Premise 레거시 시스템을 피하고 모바일 관리 기능을 갖춘 클라우드 제품군을 도입함에 따라 가속화될 것으로 예측됩니다. 이러한 추세는 업무의 민첩성에 부합하는 현대적이고 유연한 솔루션에 대한 중소기업의 선호도가 높아지고 있음을 보여줍니다. 이러한 변화의 주된 요인은 중소기업의 역동적이고 끊임없이 변화하는 요구 사항에 적응할 수 있는 비용 효율적이고 확장성이 뛰어난 기술에 대한 수요입니다. 또한, 기능이 강화된 클라우드 기반 도구를 더 쉽게 이용할 수 있게 된 점도 중소기업이 기존 시스템에서 전환하는 데 박차를 가하고 있습니다. 이러한 변화는 기업 소셜 소프트웨어 시장 경쟁 구도에 큰 영향을 미칠 것으로 예측됩니다.

중소기업들은 도입의 복잡성을 줄여주는 예측 가능한 사용자 단위 요금 체계와 간소화된 온보딩 절차에 점점 더 매력을 느끼고 있습니다. 이러한 가격 모델과 합리화된 프로세스를 통해 중소기업은 고액의 초기 비용이나 기술적 문제에 시달리지 않고 기업 소셜 소프트웨어를 도입할 수 있게 됩니다. Zoho나 MangoApps와 같은 벤더들은 중소기업을 위해 맞춤화된 업종별 템플릿을 패키지 형태로 제공함으로써, 이러한 구체적인 요구 사항에 부응하고 신속한 도입과 사용 편의성을 보장하고 있습니다. 한편, 대기업들은 AI, 보안, 분석 기능을 묶은 엔터프라이즈 계약을 체결하고, 하이퍼스케일러의 생태계를 활용한 종합적인 서비스를 이용하고 있습니다. 공급업체의 이러한 두 가지 접근 방식은 중소기업과 대기업의 다양한 요구를 반영하고 있습니다. Atlassian의 모듈형 가격 전략은 이러한 유연성을 잘 보여주고 있으며, 플랫폼을 전환할 필요 없이 소규모 팀의 도입부터 전 세계적인 확장에 이르기까지 원활하게 규모를 확장할 수 있게 해줍니다.

지역별 분석

북미는 2025년 매출의 37.70%를 차지하며, AI를 접목한 협업 분야의 선도적인 시장으로 자리매김하고 있습니다. 미국 기업들은 생산성 향상과 업무 흐름의 효율화를 목표로 지식 통합 에이전트의 전 세계 시범 도입을 주도하고 있습니다. 메타가 Workplace에서 철수한 것을 계기로, 벤더 간 통합이 가속화되고 있으며, 통합형 생산성 클라우드의 중요성이 부각되고 있습니다. 또한, ESG 프레임워크에 기반한 직원 참여 지표 공개를 요구하는 규제적 압력 또한 플랫폼 업데이트를 촉진하고 있습니다. 이 지역의 견고한 기술 인프라와 첨단 솔루션의 조기 도입은 기업 소셜 소프트웨어 시장에서 혁신과 도입의 핵심 거점으로서의 위상을 더욱 공고히 하고 있습니다.

아시아태평양은 2025년에 디지털 워크플레이스 성숙도가 66.35%에 달하고 연평균 성장률(CAGR) 18.70%를 기록하는 등 가장 빠르게 성장하고 있는 지역입니다. 인도, 일본, 호주 등 주요 시장이 기업 소셜 소프트웨어에 대한 투자를 주도하고 있는 반면, 중국의 현지화 규제로 인해 텐센트나 알리바바의 인프라를 우선시하는 국내 개별 도입이 진행되고 있습니다. 이 지역의 중소기업들은 클라우드 제품군을 빠르게 도입하고 있어 사용자 수 증가에 크게 기여하고 있지만, 사용자 1인당 평균 수익은 북미의 벤치마크와 비교했을 때 여전히 낮은 수준에 머물러 있습니다. 이 지역의 성장은 디지털 전환(DX) 노력의 확대, 클라우드 도입을 촉진하는 정부 정책, 그리고 중소기업의 확장 가능하고 비용 효율적인 솔루션에 대한 수요 증가에 힘입어 더욱 가속화되고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)의 복잡성과 거시경제의 불확실성으로 인해 보급 속도가 둔화되고 있지만, 여전히 기업 소셜 소프트웨어를 위한 전략적 시장입니다. 유럽에서 검증된 데이터 주권 기능은 다른 지역에서도 기본적인 요건으로 자리 잡고 있으며, 규정 준수를 주도하는 혁신의 시험대가 되고 있습니다. 독일, 영국, 프랑스에서는 ESG와 관련된 참여 지표에 중점을 두고 있으며, 이는 플랫폼의 개발 및 도입에 영향을 미치고 있습니다. 한편, 남미와 중동 및 아프리카에서는 모바일 중심의 신규 시장 개척 기회가 생겨나고 있습니다. 그러나 이러한 지역들은 환율 변동, 미비한 인프라, 디지털 전환의 지연과 같은 과제에 직면해 있어, 시장 확대의 가능성은 있으나 이러한 요인들이 성장을 저해할 수 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the enterprise social software market size is expected to be USD 18.8 billion in 2025, USD 22.15 billion in 2026, and reach USD 50.24 billion by 2031, growing at a CAGR of 17.8% from 2026 to 2031.

This report is Segmented by Feature Module (Internal Communications, Employee Recognition and Wellness, and More), Organization Size (SMEs, and Large Enterprises), Delivery Channel (Mobile-First, Web Browser, and More), Industry Vertical (Healthcare, IT and Telecom, Retail and ECommerce, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise Social Software Market Trends and Insights

Permanent Hybrid-Work Culture

Hybrid arrangements have become the default operating model, with three out of four enterprises retaining formal split-location policies. This permanence has exposed the limits of email and meeting-centric collaboration, prompting a 91% increase in asynchronous tool budgets between 2024 and 2025. Knowledge-intensive sectors such as IT and telecom accelerated adoption because incident response and code reviews demand persistent, searchable discussion threads. Microsoft's 2026 decision to surface Viva Engage communities directly inside Teams highlights the vendor's recognition that context switching suppresses engagement. Organizations that fail to converge chat, content, and tasks into a single AI-powered hub risk locking 60% of employee time into "work about work," which is why platform consolidation is expected to intensify through 2031.

Rising SaaS Adoption for Lower TCO

Cloud migration originally promised capital-expense relief, yet premium pricing for AI add-ons is inflating operating budgets. Salesforce and Microsoft now charge USD 30-USD 60 per user each month for generative functionality, pushing finance teams to reassess lifetime subscription costs. Vendors such as Zoho are winning cost-sensitive customers by embedding AI in base tiers, delivering predictable pricing that appeals to small businesses. Asia-Pacific enterprises, many of which never owned on-premises stacks, are leapfrogging directly to SaaS and favoring mobile-first suites that mirror consumer experiences. Even so, usage-based billing tied to token consumption is introducing forecast volatility that controllers must model into 2027 and 2028 budgets.

Data-Sovereignty and Privacy Risks

GDPR and similar statutes mandate strict residency rules that complicate global roll-outs. A growing share of European enterprises invest in sovereign-cloud zones to avoid cross-border transfer triggers, which raises hosting costs and lengthens procurement cycles. Multinationals must segment user traffic by jurisdiction, adding architectural complexity that can slow adoption. Platform vendors address the issue with in-region data centres and granular encryption keys, yet some buyers still delay purchases until compliance evidence matures. These dynamics temper the growth curve of the enterprise social software market in privacy-sensitive sectors.

Other drivers and restraints analyzed in the detailed report include:

- Productivity-Suite Integrations

- ESG-Linked Employee-Engagement Needs

- Cultural Resistance to Open Sharing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Generative AI in knowledge discovery is experiencing significant growth, with a compound annual growth rate (CAGR) of 21.20%. This growth rate surpasses that of the broader enterprise social software market, highlighting its increasing importance. By 2025, internal communications are projected to account for 40.70% of the enterprise social software market share. However, its dominance is expected to decline as organizations shift their budgets toward advanced modules. These modules focus on automatically surfacing expertise and summarizing extensive document repositories, addressing the growing need for efficiency in knowledge management. The shift reflects a broader trend of enterprises prioritizing tools that enhance productivity and streamline access to critical information.

Unstructured institutional memory currently leads to an average of 1.8 hours of daily search time per employee, creating inefficiencies. Enterprises are actively investing in solutions to transform this lost time into actionable insights, driving productivity. Recognition and wellness modules are gaining traction due to their alignment with environmental, social, and governance (ESG) priorities. Meanwhile, ideation hubs remain predominantly utilized in research and development (R&D)-intensive sectors. Additionally, project collaboration and file-sharing functionalities are increasingly integrated into productivity suites, compelling standalone vendors to differentiate themselves. These vendors are focusing on vertical-specific workflows or enhancing AI explainability to remain competitive in a rapidly evolving market landscape.

Large enterprises commanded 56.60% of the 2025 revenue pool, yet SMEs are advancing at an 18.60% CAGR, narrowing the usage divide. The enterprise social software market size for SME deployments is projected to accelerate as smaller firms bypass on-premises legacies and adopt cloud suites with mobile administration. This trend highlights the growing preference among SMEs for modern, flexible solutions that align with their operational agility. The shift is primarily driven by the need for cost-effective and scalable technologies that can adapt to the dynamic and evolving requirements of smaller businesses. Additionally, the increasing availability of cloud-based tools with enhanced features is further encouraging SMEs to transition away from traditional systems. This evolution is expected to significantly impact the competitive landscape of the enterprise social software market.

SMEs are increasingly drawn to predictable per-user fees and simplified onboarding processes, which reduce implementation complexities. These pricing models and streamlined processes enable smaller businesses to adopt enterprise social software without the burden of high upfront costs or technical challenges. Vendors like Zoho and MangoApps are addressing these specific needs by offering packaged industry templates tailored for SMEs, ensuring faster deployment and usability. Meanwhile, large organizations negotiate enterprise agreements that bundle AI, security, and analytics, leveraging hyperscaler ecosystems for their comprehensive offerings. This dual approach by vendors reflects the diverse needs of SMEs and large enterprises. Atlassian's modular pricing strategy exemplifies this adaptability, allowing businesses to scale from small team deployments to global rollouts seamlessly, without requiring platform migration.

Geography Analysis

North America held 37.70% of 2025 revenue and remains the reference market for AI-infused collaboration. U.S. enterprises are leading global pilots of knowledge-synthesis agents, which are designed to enhance productivity and streamline workflows. Vendor consolidation has intensified following Meta's exit from Workplace, highlighting the growing importance of integrated productivity clouds. Additionally, regulatory pressures to disclose employee-engagement metrics under ESG frameworks are driving platform renewals. The region's strong technological infrastructure and early adoption of advanced solutions further solidify its position as a critical hub for innovation and adoption in the enterprise social software market.

Asia-Pacific is the fastest-growing region, with an 18.70% CAGR, as digital workplace maturity reached 66.35% in 2025. Key markets such as India, Japan, and Australia are anchoring investments in enterprise social software, while China's localization rules are fostering separate domestic deployments, favoring Tencent and Alibaba infrastructure. SMEs across the region are rapidly adopting cloud suites, significantly contributing to user-count growth, even though the average revenue per user remains lower compared to North American benchmarks. The region's growth is further supported by increasing digital transformation initiatives, government policies promoting cloud adoption, and the rising demand for scalable and cost-effective solutions among smaller businesses.

Europe faces slower uptake due to GDPR complexities and macroeconomic uncertainties, yet it remains a strategic market for enterprise social software. Data-sovereignty capabilities proven in Europe are becoming baseline expectations in other regions, making it a testing ground for compliance-driven innovations. Germany, the United Kingdom, and France are focusing on ESG-linked engagement metrics, which are influencing platform development and adoption. Meanwhile, South America and the Middle East and Africa present mobile-led greenfield opportunities. However, these regions face challenges such as currency volatility, limited infrastructure, and slower digital transformation, which could temper growth despite their potential for market expansion.

- Microsoft Corporation

- Salesforce Inc

- Google LLC

- Atlassian Corporation

- International Business Machines Corporation

- Meta Platforms Inc

- SAP SE

- Oracle Corporation

- Zoho Corporation Pvt Ltd

- Aurea Inc Jive Software

- LumApps SAS

- MangoApps Inc

- Igloo Software Inc

- Limeade Inc incl Sitrion

- Axero Solutions LLC

- Simpplr Inc

- Happeo Oy

- Staffbase GmbH

- Firstup Inc

- Unily Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Permanent Hybrid-Work Culture

- 4.2.2 Rising SaaS Adoption for Lower TCO

- 4.2.3 Productivity-Suite Integrations

- 4.2.4 ESG-Linked Employee-Engagement Needs

- 4.2.5 Gen-AI Powered Knowledge Discovery

- 4.2.6 Verticalised Intranet Templates

- 4.3 Market Restraints

- 4.3.1 Data-Sovereignty and Privacy Risks

- 4.3.2 Cultural Resistance to Open Sharing

- 4.3.3 Collaboration-Tool Fatigue

- 4.3.4 LLM-Integration Lock-In Concerns

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS VALUE

- 5.1 By Feature Module

- 5.1.1 Internal Communications

- 5.1.2 Knowledge Management

- 5.1.3 Employee Recognition and Wellness

- 5.1.4 Ideation Innovation Hubs

- 5.1.5 Others Feature Module

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises SMEs

- 5.2.2 Large Enterprises

- 5.3 By Delivery Channel

- 5.3.1 Mobile First

- 5.3.2 Web Browser

- 5.3.3 Desktop Client

- 5.4 By Industry Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare

- 5.4.3 IT and Telecom

- 5.4.4 Retail and eCommerce

- 5.4.5 Government and Public Sector

- 5.4.6 Manufacturing

- 5.4.7 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Microsoft Corporation

- 6.4.2 Salesforce Inc

- 6.4.3 Google LLC

- 6.4.4 Atlassian Corporation

- 6.4.5 International Business Machines Corporation

- 6.4.6 Meta Platforms Inc

- 6.4.7 SAP SE

- 6.4.8 Oracle Corporation

- 6.4.9 Zoho Corporation Pvt Ltd

- 6.4.10 Aurea Inc Jive Software

- 6.4.11 LumApps SAS

- 6.4.12 MangoApps Inc

- 6.4.13 Igloo Software Inc

- 6.4.14 Limeade Inc incl Sitrion

- 6.4.15 Axero Solutions LLC

- 6.4.16 Simpplr Inc

- 6.4.17 Happeo Oy

- 6.4.18 Staffbase GmbH

- 6.4.19 Firstup Inc

- 6.4.20 Unily Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White Space and Unmet Need Assessment