|

시장보고서

상품코드

2062310

남미의 BOPP 필름 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South America BOPP Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

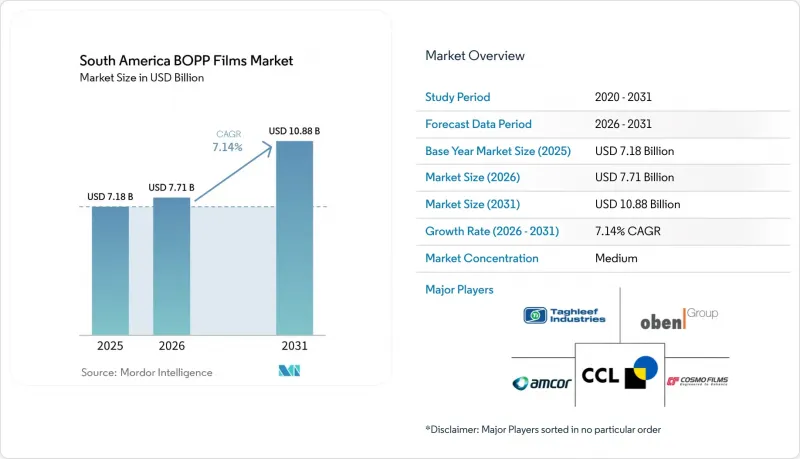

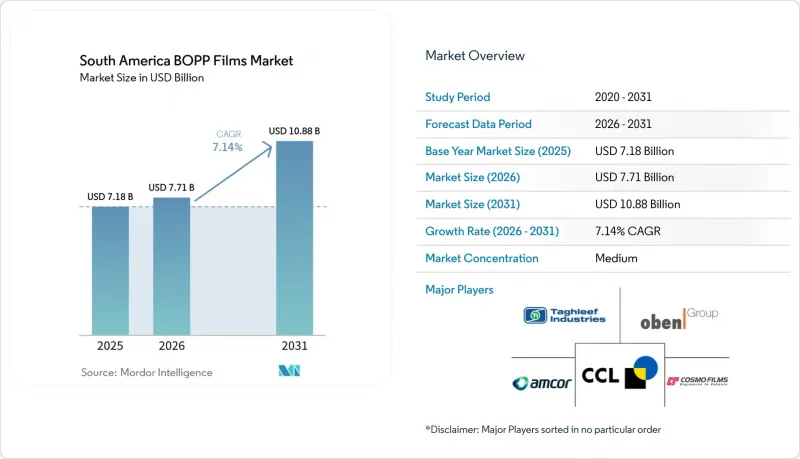

Mordor Intelligence에 의하면, 남미 BOPP 필름 시장 규모는 2025년에 71억 8,000만 달러로 평가되었고 2026년 77억 1,000만 달러에서 2031년까지 108억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.14%를 나타낼 전망입니다.

본 보고서는 필름 유형(투명, 메탈라이즈, 백색/불투명/무광 등), 두께(20마이크론 미만, 20-30마이크론, 31-45마이크론 등), 용도(식품 포장, 담배 포장, 라벨 및 감압 테이프, 기타), 최종 사용자 산업(식품 및 음료, 퍼스널케어 및 화장품, 담배, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

남미 BOPP 필름 시장 동향과 인사이트

식품 소매업의 급성장이 고투명성 연포장재 수요를 끌어올리고 있습니다.

현대적인 슈퍼마켓과 편의점 체인은 브라질의 대도시권과 아르헨티나, 콜롬비아의 지방 도시로 계속 확장되고 있으며, BOPP의 투명성과 광택을 살린 소포장 스낵 제품의 진열 공간이 확대되고 있습니다. 조리된 베이커리 제품이나 과자를 구매하는 소비자들은 신선함을 강조하면서도 습기를 차단하는 투명한 창을 기대하며, 이러한 성능의 균형은 연신 폴리프로필렌(BOPP)을 통해 쉽게 실현될 수 있습니다. 이에 대해 컨버터 제조업체들은 강성을 저하시키지 않으면서도 두께를 얇게 만들 수 있는 개선된 핀닝 및 두께 제어 모듈을 기존 생산 라인에 사후 장착하는 방식으로 대응하고 있습니다. 2024년 하반기에 완료된 브라질 최대 규모의 라인 업그레이드(Votorantim사)를 통해 더욱 고광택의 필름이 생산되기 시작했으며, 현재 고급 쿠키 포장재로 점차 자리 잡고 있습니다. 페루와 콜롬비아 내륙 지역에서는 도시 지역의 콜드체인망이 아직 발전 단계에 있기 때문에 포장의 무결성은 여전히 중요하며, 이는 해당 시장에서 고투명 필름에 대한 수요를 더욱 부추기고 있습니다.

PVC나 셀로판의 대체재로 비용 효율이 뛰어난 BOPP

브라질과 칠레의 규제 당국이 염소 함유 폴리머에 대한 규제를 강화함에 따라, 각 변환업체들은 담배용 오버랩 및 사탕용 트위스트 포장을 PVC에서 BOPP로 전환했습니다. 또한, 현지 메탈라이제이션 능력이 향상되고 비용 격차가 줄어들며 공급 안정성이 높아짐에 따라, BOPP는 고급 과자 분야에서 수입 셀로판의 대체재로 채택되기도 했습니다. 메탈라이즈드 BOPP는 단일 소재로 구성되어 있어 사용 후 분리 수거가 용이하며, 이는 상파울루주에서 시행되는 확대 생산자 책임법에서 요구하는 중요한 요건입니다. 2026년 3월 현재, 이축 연신 필름용 수지의 최근 현물 가격은 톤당 1,453달러에서 1,641달러 사이에서 형성되고 있으며, 이는 특수 셀룰로오스계 소재에 비해 BOPP가 비용 면에서 우위를 점하고 있음을 보여줍니다. 브랜드 소유주들이 재활용 가능성 목표를 공개함에 따라, 모든 형태의 2차 포장재에서 PVC 사용이 더욱 줄어들 것으로 예측됩니다.

변동이 심한 폴리프로필렌 수지 가격

2025년 2분기, 브라질의 PP 현물 가격은 전분기 대비 4% 하락했습니다. 이는 아시아 지역공급 과잉이 현지 판매업체까지 파급되어, 이미 계약된 필름 주문에 대한 가공업체의 이익률을 압박했기 때문입니다. 가격 변동은 안정적인 원자재 비용을 추구하는 식품 브랜드와의 분기별 원가 전가 협상을 복잡하게 만들고 있습니다. 페루의 수입업체에 따르면, 2025년 5월 PP 납품 가격은 16.6% 하락했으나, 추가 운임 및 관세 할증료로 인해 절감된 비용의 일부가 상쇄되었습니다. 아르헨티나의 통화 약세는 불확실성을 더욱 가중시키고 있으며, 일부 제조업체들은 수지 가격을 달러로 헤지하고 재고 수준을 높일 수밖에 없는 상황에 처해 있습니다. 이러한 변동으로 인해 금융기관이 자금을 공급하기 전에 예측 가능한 현금 흐름을 요구함에 따라, 생산 능력 확대가 지연되고 있습니다.

부문별 분석

2025년 남미 BOPP 필름 시장 점유율의 43.63%를 차지하는 투명 등급 제품은 시각적 투명성과 고속 라인 속도가 요구되는 상온 보관이 가능한 스낵 및 제과류 제품의 포장재로 주류를 이루고 있습니다. 메탈라이즈드 등급은 2024년 하반기 국내 생산 능력이 확대됨에 따라, 브랜드 소유주들로부터 동등한 차단 성능을 유지하면서도 호일 라미네이트를 대체할 수 있는 재활용 가능한 대안으로 지지를 얻고 있습니다. 연평균 성장률(CAGR) 7.79%를 나타낼 것으로 예측되는 안개 방지 등급 제품은 습도 변동으로 인해 결로가 발생하기 쉬운 북미 및 아시아 지역으로 페루와 칠레 연안 지역에서 출하되는 농산물용 파우치에 채택이 확대되고 있습니다.

각 제조업체는 유분 침투에 강한 내구성을 갖춘 고부가가치 표면을 구현하는 플라즈마 및 진공 메탈라이저에 투자하고 있습니다. 이는 브라질 미나스제라이스주 클러스터에서 수출되는 분유용 소포장에 있어 최우선 과제입니다. 백색 및 무광 필름은 틈새 시장이지만, 차광성이 필요한 담배 포장지나 고급 과자 분야에서 가격 프리미엄을 확보하고 있습니다. 이러한 차별화된 제품 구성 덕분에 통합형 그룹은 범용 투명 필름의 경기 순환적 수요 감소에 대비할 수 있게 되었으며, 이 전략은 아르헨티나와 콜롬비아 전역의 중견 컨버터들에 의해 점점 더 많이 모방되고 있습니다.

표준적인 20-30μm 제품은 주류 성형·충전·밀봉(FFS) 라인에서 강성과 수율의 균형이 잘 잡혀 있어, 2025년 남미 BOPP 필름 시장 규모의 39.39%를 차지했습니다. 두께가 45µm을 초과하는 두꺼운 기판 시장은 연평균 성장률(CAGR) 8.01%로 증가할 것으로 예상되며, 이는 냉장 운송 중 천공 위험을 견딜 수 있는 아보카도, 포도, 수산물용 진공 봉투 라이너 시장을 뒷받침하고 있습니다. 두께 31-45마이크로미터의 필름은 스낵 포장, 음료 라벨, 담배 오버랩 등 중간 수준의 용도에 적합합니다.

오벤 그룹이 최근 몬테레이에 도입한 폭 12미터의 생산 라인은 분당 700미터의 속도로 가동되며, 페루와 칠레 수출용 포장 공장을 대상으로 한 50m 롤을 효율적으로 생산하고 있습니다. 두께가 20µm 미만인 필름은 전자상거래용 테이프나 랩어라운드 라벨에 사용되며, 재료 절감 효과가 그대로 출하 중량 경감으로 이어집니다. 각 변환기 제조업체들은 더 두꺼운 필름을 저속으로 생산하기 위해 생산 라인을 확장할 때 드는 설비 투자 비용과, 견고한 차단 성능을 요구하는 신선식품 수출업체들 수요 증가로 인한 매출 증대를 저울질하며 검토하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the south america bOPP films market size was valued at USD 7.18 billion in 2025 and estimated to grow from USD 7.71 billion in 2026 to reach USD 10.88 billion by 2031, at a CAGR of 7.14% during the forecast period (2026-2031).

This report is Segmented by Film Type (Transparent, Metallized, White/Opaque/Matt, and More), Thickness (Below 20 Mm, 20-30 Mm, 31-45 Mm, and More), Application (Food Packaging, Tobacco Packaging, Labels and Pressure-Sensitive Tapes, and More), End-User Industry (Food and Beverage, Personal Care and Cosmetics, Tobacco, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America BOPP Films Market Trends and Insights

Food Retail Boom Pushing Demand for High-Clarity Flexible Packs

Modern supermarkets and convenience chains continue to spread across metropolitan Brazil and secondary cities in Argentina and Colombia, widening shelf space for portion-controlled snacks that benefit from BOPP's clarity and gloss. Consumers buying ready-to-eat bakery and confectionery products expect transparent windows that signal freshness while blocking moisture, a performance balance readily delivered by oriented polypropylene. Converters have responded by retrofitting older lines with enhanced pinning and thickness-control modules that allow down-gauging without sacrificing stiffness. Brazil's largest line upgrade at Votorantim, completed in late 2024, produced higher-gloss films that are now making inroads into premium cookie wraps. With urban cold-chain networks still nascent in Peru and interior Colombia, pack integrity remains critical, further lifting demand for high-clarity films in those markets.

Substitution of PVC and Cellophane with Cost-Efficient BOPP

Regulators in Brazil and Chile tightened rules on chlorine-containing polymers, spurring converters to transition tobacco overwraps and candy twists from PVC to BOPP. BOPP also displaced imported cellophane in premium confectionery as local metallization capacity rose, narrowing cost gaps and improving supply security. The mono-material nature of metalized BOPP aids post-consumer sorting, a key requirement under extended producer responsibility laws taking effect in Sao Paulo state. Recent spot resin quotes for bioriented film grades ranged between USD 1,453 and USD 1,641 per metric ton in March 2026, reinforcing BOPP's cost advantage over specialty cellulosics. As brand owners publicize recyclability targets, further PVC withdrawal is expected across secondary packaging formats.

Volatile Polypropylene Resin Pricing

Spot PP prices in Brazil fell 4% quarter over quarter in Q2 2025 as Asian oversupply reached local distributors, eroding converters' margins on previously contracted film orders. Fluctuations complicate quarterly pass-through negotiations with food brands that demand stable input costs. Importers in Peru reported a 16.6% decline in delivered PP values during May 2025, but additional freight and tariff surcharges offset part of the savings. Currency depreciation in Argentina adds another layer of unpredictability, forcing some makers to hedge resin prices in U.S. dollars and hold higher stock levels. These swings delay capacity expansions because financing institutions seek predictable cash flows before releasing capital.

Other drivers and restraints analyzed in the detailed report include:

- Rising E-Commerce Driving Demand for Label and Tape Films

- Brand Owners' Shift Toward Mono-Material Recyclability

- Competition from BOPET in High-Barrier Niches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transparent grades, accounting for 43.63% of the South America BOPP films market share in 2025, dominate shelf-stable snack and bakery wraps that demand aesthetic visibility and rapid line speeds. Metalized variants gained traction after domestic capacity rose in H2 2024, offering brand owners a recyclable alternative to foil laminates at comparable barrier levels. Anti-fog grades, projected to grow at a 7.79% CAGR, are gaining adoption in produce pouches shipped from Peru and Chile's coastal valleys to North America and Asia, where humidity swings can trigger condensation.

Producers invest in plasma and vacuum metallizers that unlock value-added surfaces resistant to grease migration, a priority for dairy powder sachets exported from Brazil's Minas Gerais cluster. White and matt films, although niche, command price premiums in tobacco overwraps and gourmet confectionery that rely on light protection. This differentiated mix allows integrated groups to hedge against cyclical declines in commodity clear films, a strategy increasingly copied by mid-tier converters across Argentina and Colombia.

Standard 20-30 µm products captured 39.39% of the South America BOPP films market size in 2025 because they balance stiffness and yield on mainstream form-fill-seal lines. Thicker substrates above 45 µm, forecast to rise at an 8.01% CAGR, underpin vacuum bag liners for avocados, grapes, and seafood that endure puncture risks during refrigerated transit. Films in the 31-45 micrometer band address mid-range applications, including snack packaging, beverage labels, and tobacco overwraps.

Oben Group's recent 12-meter-wide line in Monterrey runs at 700 m/min, enabling efficient production of 50 µm rolls targeted at export pack houses in Peru and Chile. Below-20 µm gauges are used in e-commerce tapes and wrap-around labels, where material reduction directly translates into lower shipping weight. Converters weigh the capital economics of stretching lines to run thicker films at slower speeds against the volume upside offered by fresh-produce exporters seeking robust barriers.

List of Companies Covered in this Report:

- Vitopel Group

- Oben Holding Group

- Amcor plc

- Taghleef Industries

- Polo Films

- Papion Flexible Films

- Polyplex Corporation Limited

- Braskem S.A.

- Mondi plc

- CCL Industries Inc.

- Jindal Poly Films Limited

- Cosmo Films Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Food Retail Boom Pushing Demand for High-Clarity Flexible Packs

- 4.2.2 Substitution of PVC and Cellophane with Cost-Efficient BOPP

- 4.2.3 Rising E-Commerce Driving Demand for Label and Tape Films

- 4.2.4 Brand Owners' Shift Toward Mono-Material Recyclability

- 4.2.5 Regional Sugar-Tax Policies Spurring Metallized Snack Packs

- 4.2.6 Surge in Agro-Export Vacuum-Bag Liners Using Thick BOPP

- 4.3 Market Restraints

- 4.3.1 Volatile Polypropylene Resin Pricing

- 4.3.2 Competition from BOPET in High-Barrier Niches

- 4.3.3 Limited Tenter-Frame Capacity South of Brazil

- 4.3.4 Extended Truck Strikes Causing Logistics Bottlenecks

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Film Type

- 5.1.1 Transparent Films

- 5.1.2 Metallized Films

- 5.1.3 White / Opaque / Matt Films

- 5.1.4 Anti-Fog and Other Functional Films

- 5.2 By Thickness

- 5.2.1 Below 20 µm

- 5.2.2 20-30 µm

- 5.2.3 31-45 µm

- 5.2.4 Above 45 µm

- 5.3 By Application

- 5.3.1 Food Packaging

- 5.3.1.1 Confectionery

- 5.3.1.2 Snacks

- 5.3.1.3 Bakery

- 5.3.1.4 Fresh Produce

- 5.3.2 Beverage Packaging

- 5.3.3 Tobacco Packaging

- 5.3.4 Labels and Pressure-Sensitive Tapes

- 5.3.5 Industrial and Other Applications

- 5.3.1 Food Packaging

- 5.4 By End-User Industry

- 5.4.1 Food and Beverage

- 5.4.2 Personal Care and Cosmetics

- 5.4.3 Tobacco

- 5.4.4 Industrial and Logistics

- 5.4.5 Other Consumer Goods

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Vitopel Group

- 6.4.2 Oben Holding Group

- 6.4.3 Amcor plc

- 6.4.4 Taghleef Industries

- 6.4.5 Polo Films

- 6.4.6 Papion Flexible Films

- 6.4.7 Polyplex Corporation Limited

- 6.4.8 Braskem S.A.

- 6.4.9 Mondi plc

- 6.4.10 CCL Industries Inc.

- 6.4.11 Jindal Poly Films Limited

- 6.4.12 Cosmo Films Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment