|

시장보고서

상품코드

2062322

E Commerce 자동차 애프터마켓 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)E-Commerce Automotive Aftermarket - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

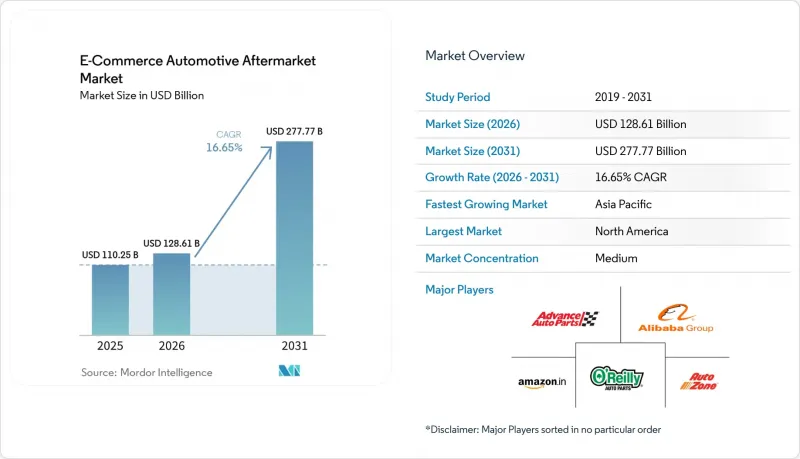

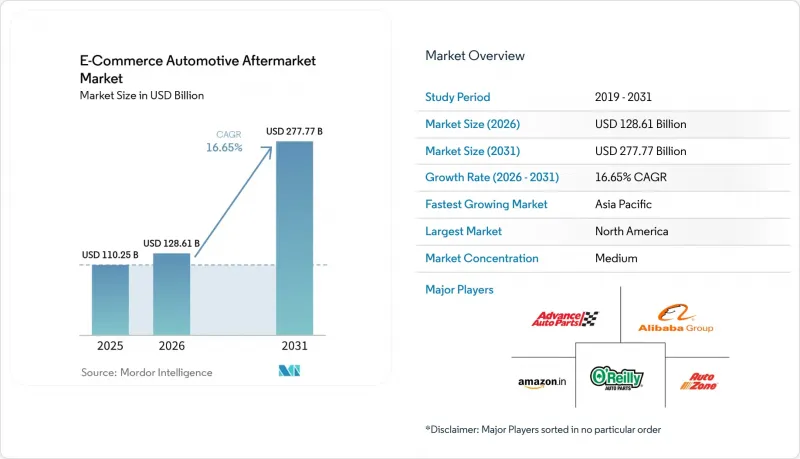

Mordor Intelligence에 의하면, E Commerce 자동차 애프터마켓 시장 규모는 2025년 1,102억 5,000만 달러로 평가되었고, 2026년에는 1,286억 1,000만 달러로 추정되고, 2031년까지 2,777억 7,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 16.65%를 나타낼 것으로 예측됩니다.

본 보고서는 교체 부품별(엔진 부품, 변속기 및 조향 장치, 브레이크 시스템 등), 판매 채널별(기업 간 거래(B2B) 및 기업 대 소비자 거래(B2C)), 차종별(승용차 등), 구동 방식별(내연기관(ICE) 차량 등), 지역별(북미, 남미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

세계의 자동차 애프터마켓 전자상거래 시장 동향 및 인사이트

차량의 평균 사용 연수가 늘어나면서 교체 부품 수요가 증가하고 있습니다.

2025년, 미국의 차량 평균 보유 연수는 12.8년에 달했으며, 차량의 85%가 4년 이상 경과한 상태이며, 이러한 경향은 선진국 시장 전반에서 나타납니다. 이러한 구조적 노후화로 인해 유지보수 빈도가 증가하고, 고액의 수리가 필요한 사례도 늘어나면서, 풍부한 상품 라인업과 투명한 가격 정책을 제공하는 디지털 소매업체로 새로운 수요가 쏠리고 있습니다. 온라인 검색 알고리즘은 복잡한 부품의 조달을 용이하게 하여, 오프라인 매장에 비해 전자상거래에 결정적인 우위를 제공합니다. 신차를 구매하는 대신 차량을 오랫동안 보유하려는 경제적 압력은 전자상거래 자동차 애프터마켓 시장에 대한 이러한 장기적인 호재를 더욱 강화하고 있습니다.

스마트폰과 인터넷의 급속한 보급이 온라인 구매를 가속화했습니다.

남미에서는 브라질의 Pix와 같은 실시간 결제 시스템에 힘입어 인터넷 보급률이 크게 향상되었으며, 전자상거래 사용자 기반도 확대되고 있습니다. 인도에서는 전기차 등록 대수가 크게 증가하고 있으며, 현지 언어를 지원하는 모바일 우선 플랫폼이 첫 구매자들의 절차를 간소화하고 있습니다. WhatsApp과 WeChat의 소셜 커머스 기능은 단체 구매를 촉진하고 있습니다. 또한, DIY 애호가들은 설치 가이드로 동영상 튜토리얼을 점점 더 많이 활용하고 있습니다. 이러한 행동의 변화로 인해 자동차 부품 수요는 기존 오프라인 매장에서 온라인 자동차 애프터마켓으로 이동하고 있습니다.

위조 부품에 대한 우려가 소비자의 신뢰를 훼손합니다.

EU의 조사에 따르면, 압수된 위조 부품의 대부분이 중국산인 것으로 밝혀졌으며, 에어백, 브레이크 패드, 오일 필터 등 주요 부품에 대한 잠재적인 안전 위험이 부각되고 있습니다. 이에 대응하기 위해 마켓플레이스는 머신러닝 도구를 활용하여 의심스러운 판매자를 파악하고 경고를 발령하고 있습니다. 동시에, 브랜드 소유자는 최종 사용자의 검증이 가능하도록 QR 코드나 블록체인 ID를 통합하고 있습니다. 그러나 적발률은 상승하고 있지만, 불법 업자들은 신속하게 판매 거점을 옮기고 있습니다. 또한, 가격에 민감한 지역에서는 소비자들이 여전히 비용을 우선시하고 있기 때문에 전자상거래 자동차 애프터마켓에서 이러한 보호 조치의 효과는 떨어지고 있습니다.

부문별 분석

서스펜션 관련 제품은 2025년 전자상거래 자동차 애프터마켓 시장의 매출액 중 26.64%를 차지했으며, 자주 교체해야 하는 소모품으로서의 입지를 확고히 하고 있습니다. 전기 부품 시장은 운전 보조 시스템 및 전동화 플랫폼에서 센서, 제어 장치, 고전압 하네스가 보급됨에 따라 연평균 성장률(CAGR) 17.66%로 확대되고 있습니다. 조명은 할로겐에서 LED 어레이로 전환되고 있으며, 이는 프리미엄 업그레이드에 대한 수요를 불러일으키고 있습니다. 한편, 와이퍼나 필터는 이익률은 낮지만 재구매를 촉진하고 있습니다.

전기 부품의 SKU에 대한 수요는 1,000달러를 초과하기도 하는 제어 장치의 가격 상승도 반영하고 있으며, 이러한 부품들은 대개 소프트웨어를 통해 고유한 VIN과 연동되어 있습니다. 서스펜션 부품은 여전히 범용화되어 있지만, 안정적인 판매량의 기반이 되고 있으며, OEM 동급 제품, 고성능 제품, 저가 제품이 보증 내용과 가격 면에서 경쟁하고 있습니다. 서스펜션 시장의 성숙도로 인해 매출 총이익률은 다소 낮은 편이지만, 수주 예측 가능성이 전자상거래 자동차 애프터마켓 전체에 걸쳐 효율적인 주문 처리 네트워크를 뒷받침하고 있습니다.

2025년에는 DIY(직접 제작)를 선호하는 주택 소유주들의 자택 배송 수요가 증가하면서, B2C(소비자 대상) 주문이 총 매출의 66.59%를 차지했습니다. 한편, API를 활용한 조달 방식이 차량 운영 업체, 정비소, 딜러 사이에서 점차 확산되고 있으며, 이는 B2B(기업 간 거래) 거래의 급증에 박차를 가하고 있습니다. B2B 시장은 2026-2031년 연평균 성장률(CAGR) 22.70%를 기록하며 견조한 성장세를 보일 것으로 전망됩니다. B2C와 B2B 두 부문 모두를 지원하는 이 플랫폼은 공통의 중앙 재고를 최적화하는 동시에, 서로 다른 가격표, 신용 조건, 전담 고객 성공 팀을 전략적으로 활용하고 있습니다.

차량 운영 업체들 사이에서는 오일, 브레이크, 필터 주문을 효율화해 주는 텔레매틱스 기반 알림을 계기로, 구독형 보충 모델을 도입하는 움직임이 가속화되고 있습니다. 차량 1대당월15-75달러로 책정된 이러한 모델들은 자동차 애프터마켓 전자상거래 분야에서 안정적인 수익원을 구축해 나가고 있습니다. 소매 소비자 대상 수요는 가처분 소득이나 계절적 정비 동향에 따라 변동하지만, 차량 대여 수요는 가동률 지표와 서비스 수준 계약(SLA)에 힘입어 안정적입니다.

지역별 분석

북미는 높은 자동차 보유율, 옴니채널 전문 기업, 그리고 REPAIR법에 기반한 데이터 접근에 대한 우호적인 규제 추진에 힘입어, 2025년 전자상거래 자동차 애프터마켓 시장 매출의 38.45%를 차지했습니다. 캐나다 수요는 미국의 동향과 비슷하지만, 배터리, 서스펜션 시스템, 난방 시스템의 고장이 빈번하게 발생하는 겨울철에는 급증합니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2031년까지 24.70%의 성장이 예상됩니다. 인도는 전기차 보유 대수가 매우 많은 반면, 중국은 판매 대수에서 1위를 차지하고 있습니다. 중국 알리바바 산하의 ‘Tmall Auto’와 같은 플랫폼은 결제와 창고를 통합함으로써 업무 효율을 높이고 마찰을 최소화하고 있습니다. 아세안 시장에서는 경차 판매가 증가하고 있으며, 그중 상당 부분이 전기차로 전환되고 있습니다. 이러한 급증세가 부품 주문을 견인하고 있으며, 스마트폰 앱이나 캐시리스 지갑을 통한 주문이 점점 더 늘어나고 있습니다.

유럽에서는 예비 부품의 장기적인 공급을 의무화하는 ‘수리권’ 규제를 계기로, 온라인을 통한 부품 조달로 빠르게 전환하고 있습니다. 독일, 영국, 프랑스, 이탈리아 등의 국가들이 그 최전선에 서서 수익 면에서 혜택을 누리고 있습니다. 한편, 유럽 단일 시장 내 효율적인 국경 간 물류를 통해 경쟁력 있는 배송 시간이 확보되고 있습니다. 라틴아메리카의 자동차 산업은 아직 발전 단계에 있지만, Pix와 같은 실시간 결제 시스템의 혜택을 누리고 있습니다. 반면, 중동 및 아프리카에서는 규제와 인프라의 단편화로 인해 여러 과제에 직면해 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the e-commerce automotive aftermarket market size is expected to increase from USD 110.25 billion in 2025 to USD 128.61 billion in 2026 to USD 277.77 billion by 2031, growing at a CAGR of 16.65% over 2026-2031.

This report is Segmented by Replacement Part (Engine Parts, Transmission and Steering, Brake System, and More), Sales Channel (Business-To-Business (B2B) and Business-To-Consumer (B2C)), Vehicle Type (Passenger Cars and More), Propulsion (Internal Combustion Engine (ICE) Vehicles and More), and Geography (North America, South America, and More). Market Forecasts are Provided in Value (USD).

Global E-Commerce Automotive Aftermarket Market Trends and Insights

Rising Average Vehicle Age Boosts Replacement Part Demand

The average United States vehicle age reached 12.8 years in 2025, with 85% of cars older than four years, a pattern replicated across developed markets. This structural aging drives more frequent maintenance cycles and higher-ticket repairs, channeling incremental demand toward digital retailers that offer deep catalogs and transparent pricing. Online search algorithms ease sourcing for complex components, giving e-commerce a decisive edge over brick-and-mortar stores. Economic pressure to keep vehicles longer instead of purchasing new models further magnifies this long-run tailwind for the e-commerce automotive aftermarket market.

Rapid Smartphone and Internet Penetration Accelerates Online Purchases

South America has achieved significant internet penetration and a large base of e-commerce users, supported by instant-payment systems such as Brazil's Pix. In India, electric vehicle registrations have grown substantially, and mobile-first platforms with local-language support are simplifying the process for first-time buyers. Social-commerce features on WhatsApp and WeChat are fostering group buying. Additionally, DIY enthusiasts are increasingly relying on video tutorials for installation guidance. These behavioral changes are driving parts traffic away from traditional storefronts and toward the e-commerce automotive aftermarket.

Counterfeit Parts Concerns Erode Consumer Trust

An EU study found that the majority of counterfeit parts seized originated in China, underscoring potential safety hazards to critical components such as airbags, brake pads, and oil filters. To combat this, marketplaces are leveraging machine-learning tools to identify and flag dubious sellers. Concurrently, brand owners are embedding QR codes and blockchain IDs to enable end-user verification. Yet, despite rising authentication rates, illicit operators swiftly rotate their storefronts. Moreover, in price-sensitive regions, consumers continue to prioritize cost, which diminishes the effectiveness of these protective measures in the E-commerce automotive aftermarket.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Last-Mile Logistics and Same-Day Delivery Networks

- OEMs Launching Official E-commerce Channels

- Complex Cross-Border Hazardous-Part Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Suspension items accounted for 26.64% of 2025 revenue in the E-commerce automotive aftermarket market, confirming their status as high-frequency wear components. Electrical parts are expanding at a 17.66% CAGR as sensors, control units, and high-voltage harnesses proliferate in driver-assistance and electrified platforms. Lighting is migrating from halogen to LED arrays, unlocking premium upgrades, while wipers and filters drive repeat traffic despite slim margins.

Demand for electrical SKUs also reflects rising control-unit prices that can exceed USD 1,000, often software-locked to a unique VIN. Suspension parts remain commoditized yet stable volume anchors, with OEM-equivalent, performance, and budget tiers competing on warranty and price. The maturity of the suspension market keeps gross margins modest, but order predictability supports efficient fulfillment networks across the E-commerce automotive aftermarket.

In 2025, DIY owners' preference for doorstep delivery propelled business-to-consumer orders to account for 66.59% of total revenue. Meanwhile, API-based procurement is gaining traction among fleet operators, workshops, and dealers, fueling a surge in business-to-business (B2B) transactions. B2B is projected to expand at a robust 22.70% CAGR from 2026 to 2031. Platforms serving both B2C and B2B segments strategically leverage distinct price lists, credit terms, and dedicated customer success teams, while optimizing a shared central inventory.

Fleets are increasingly adopting subscription replenishment models, spurred by telematics alerts that streamline orders for oil, brakes, and filters. With pricing set at USD 15-75 per vehicle per month, these models are establishing consistent revenue streams in the E-commerce automotive aftermarket. While retail-consumer demand fluctuates with discretionary income and seasonal maintenance trends, fleet demand remains anchored to uptime metrics and service-level agreements.

Geography Analysis

North America held 38.45% of 2025 revenue in the E-commerce automotive aftermarket market, supported by high vehicle ownership, omnichannel pure-plays, and a favorable regulatory push for data access under the REPAIR Act. Canadian demand mirrors United States trends but spikes in winter, when batteries, suspension systems, and heating systems fail more often.

Asia-Pacific is the fastest-growing region, with 24.70% growth through 2031. India has a significant electric vehicle parc, while China leads in sales. Platforms like Alibaba's Tmall Auto in China are streamlining operations by integrating payments and warehouses to minimize friction. ASEAN markets have seen growth in light-vehicle sales, with a notable percentage being electrified. This surge is propelling parts orders, increasingly driven by smartphone apps and cashless wallets.

Europe is swiftly pivoting to online parts sourcing, spurred by right-to-repair regulations mandating long-term availability of spare parts. Countries like Germany, the United Kingdom, France, and Italy are at the forefront, reaping the revenue benefits. Meanwhile, efficient cross-border logistics within Europe's single market ensure competitive shipping times. Latin America's automotive scene is still in its infancy, yet it's reaping rewards from instant-payment systems like Pix. In contrast, the Middle East and Africa grapple with challenges, hindered by fragmented regulations and infrastructure.

- Advance Auto Parts

- Alibaba Group Holding

- Amazon.com, Inc.

- AutoZone

- CARiD

- eBay

- Flipkart

- National Automotive Parts Association (NAPA)

- O'Reilly Auto Parts

- RockAuto

- U.S. Auto Parts Network

- Walmart

- Bosch Auto-Parts Online

- Mister-Auto (Stellantis)

- PartsTech

- LKQ Corporation

- Dana Aftermarket eStore

- DENSO Auto-Parts Hub

- Continental Aftermarket E-shop

- Tenneco (DRiV) Online

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Average Vehicle Age Boosts Replacement Part Demand

- 4.2.2 Rapid Smartphone and Internet Penetration Accelerates Online Purchases

- 4.2.3 Expansion Of Last-Mile Logistics and Same-Day Delivery Networks

- 4.2.4 OEMs Launching Official E-Commerce Channels

- 4.2.5 AI-Powered Parts-Fitment Engines Reduce Return Rates

- 4.2.6 Subscription-Based Replenishment Models for Fleets

- 4.3 Market Restraints

- 4.3.1 Counterfeit Parts Concerns Erode Consumer Trust

- 4.3.2 Complex Cross-Border Hazardous-Part Regulations

- 4.3.3 Right-To-Repair Laws Squeezing Retailer Margins

- 4.3.4 Semiconductor Shortages Limiting Electronic Components Supply

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Replacement Part

- 5.1.1 Engine Parts

- 5.1.2 Transmission and Steering

- 5.1.3 Brake System

- 5.1.4 Lighting

- 5.1.5 Electrical Parts

- 5.1.6 Suspension System

- 5.1.7 Wipers

- 5.1.8 Others

- 5.2 By Sales Channel

- 5.2.1 Business-to-Business (B2B)

- 5.2.2 Business-to-Consumer (B2C)

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles (LCVs)

- 5.3.3 Medium and Heavy Commercial Vehicles (MHCVs)

- 5.4 By Propulsion

- 5.4.1 Internal Combustion Engine (ICE) Vehicles

- 5.4.2 Electric Vehicles (EVs)

- 5.4.3 Hybrid Vehicles

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Netherlands

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Advance Auto Parts

- 6.4.2 Alibaba Group Holding

- 6.4.3 Amazon.com, Inc.

- 6.4.4 AutoZone

- 6.4.5 CARiD

- 6.4.6 eBay

- 6.4.7 Flipkart

- 6.4.8 National Automotive Parts Association (NAPA)

- 6.4.9 O'Reilly Auto Parts

- 6.4.10 RockAuto

- 6.4.11 U.S. Auto Parts Network

- 6.4.12 Walmart

- 6.4.13 Bosch Auto-Parts Online

- 6.4.14 Mister-Auto (Stellantis)

- 6.4.15 PartsTech

- 6.4.16 LKQ Corporation

- 6.4.17 Dana Aftermarket eStore

- 6.4.18 DENSO Auto-Parts Hub

- 6.4.19 Continental Aftermarket E-shop

- 6.4.20 Tenneco (DRiV) Online

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment