|

시장보고서

상품코드

2062332

FRP 용기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)FRP Vessels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

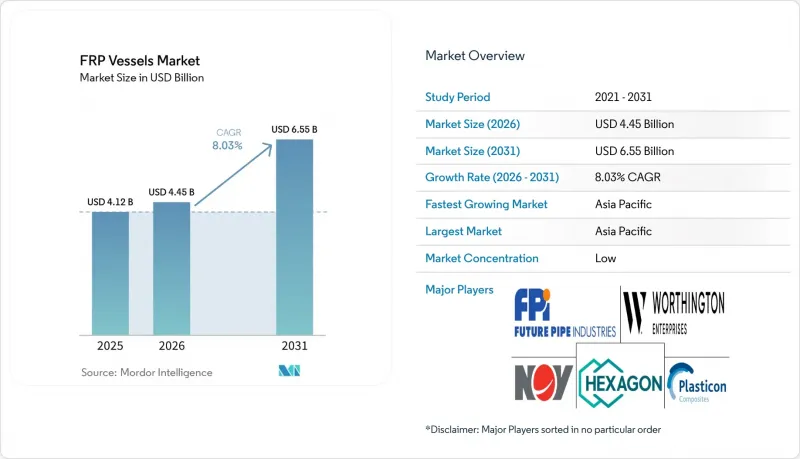

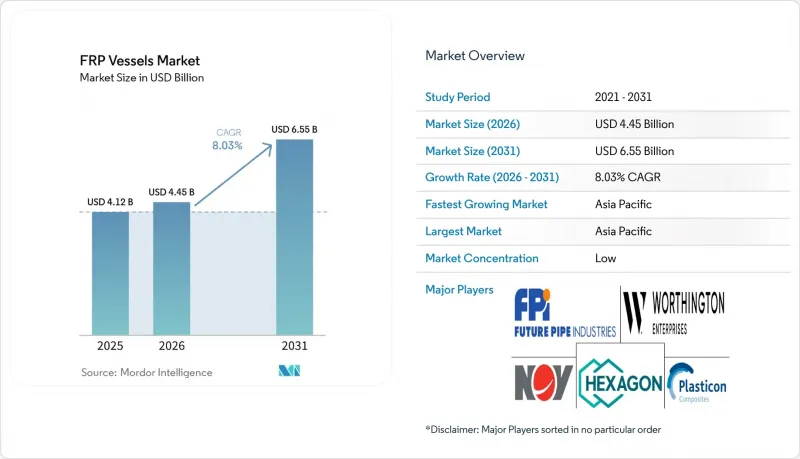

FRP 용기 시장 규모는 2025년에 41억 2,000만 달러로 평가되었습니다. 2026년에 44억 5,000만 달러에 달하고, 2031년까지 65억 5,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 8.03%를 나타낼 전망입니다.

본 보고서는 용기 유형(탱크, 컬럼 등), 압력 분류(저압(10바르 이하) 등), 섬유 유형(유리 섬유, 탄소섬유 등), 용도(상하수도 처리, 전력 및 에너지 등), 최종 사용자 산업(산업·화학 등), 지역(아시아태평양, 북미 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

세계의 FRP 용기 시장 동향 및 분석

경량이며 내식성이 뛰어난 소재의 채택

FRP 용기는 강철에 비해 무게를 약 70% 줄일 수 있으므로, 운송이 용이해지고, 개보수 공사 시 기초에 가해지는 하중도 경감됩니다. 해양 플랫폼이나 해수 담수화 시설에서는 갈바닉 부식을 방지하기 위해 복합재료가 선호되며, 도장 없이도 30년이 넘는 수명을 실현하고 있습니다. 화학 플랜트에서는 산이나 알칼리에 대응하기 위해 이중 적층 구조를 채택하여, 강철에서 흔히 발생하는 라이너 박리 현상을 방지하고 있습니다. 엔코어 아라비아는 2025년에 사우디 워터 컨버전 코퍼레이션에 이러한 탱크를 공급함으로써, 고온의 해수 환경에서 FRP의 유효성을 입증했습니다. 가혹한 가동 환경에서는 높은 초기 비용을 상회하는 수명 주기 비용의 이점이 인정됩니다.

상하수도 유틸리티자 수요 증가

북미의 지자체에서는 부식으로 인한 고장이 발생함에 따라 2024년부터 2025년에 걸쳐 강철 탱크를 FRP 탱크로 교체하는 작업이 가속화되었습니다. 7구역 상수도국과 플로리다주 정부 유틸리티국은 유지관리 비용 절감과 NSF/ANSI 61 규격 준수를 그 이유로 꼽고 있습니다. First Line사가 칭하이성의 리튬 프로젝트를 위해 3,019대를 수주한 것은 공업용수와 광업 분야를 아우르는 수요의 확대를 보여줍니다. 인도의 조립식 하수 처리 시스템에서는 염화물 농도가 높은 폐수에 대응하기 위해 FRP의 채택이 증가하고 있으며, 신속한 설치를 가능하게 하는 모듈식 이동층 생물막 설계가 활용되고 있습니다. 그동안 미뤄져 왔던 미처리 유지보수 건들이 현재 수년에 걸친 조달 붐을 뒷받침하고 있습니다.

높은 초기 설비 투자(CAPEX) 및 설치 비용

복합재 탱크는 강철 탱크에 비해 1.5-2.5배의 비용이 들기 때문에 수명 주기 총비용이 낮은 편임에도 불구하고 예산 제약이 있는 유틸리티자의 도입을 가로막고 있습니다. 대구경 권취기는 50만 달러를 초과하며, 전용 리프팅 장치를 사용하기 때문에 납품 가격에 10-15%가 추가로 가산됩니다. 보수 현장에서는 하중 경로의 변화로 인해 기초 보수가 필요해지는 경우가 있어, 토목 공사 예산이 늘어나게 됩니다. 또한, 부식으로 인한 고장으로 탱크의 수명이 단축된 후에도, 익숙한 제품에 대한 편견 때문에 구매자들은 여전히 강철 제품을 선택하는 경향이 있습니다.

부문별 분석

탱크는 2025년 매출의 41.76%를 차지하며, 수처리 및 화학약품 저장 분야에서 폭넓게 활용됨에 따라 FRP 용기 시장에서 우위를 유지했습니다. 반응기는 공정 산업에서 화학적 및 열적 스트레스에 대한 내성을 바탕으로 한 신뢰성에 힘입어, 2031년까지 연평균 성장률(CAGR) 8.69%를 기록하며 성장할 것으로 전망됩니다. 믹서나 재킷을 통합한 탱크-리액터의 하이브리드 설계는 기존의 범주 개념을 재정의하고 있으며, 식품 및 생명공학 용도의 위생적 발효조가 시장 수요 증가에 기여하고 있습니다.

공정 플랜트에서는 스테인리스 스틸에 수반되는 피칭(점식) 문제를 방지하기 위해 ASME RTP-1 또는 BPE 규격을 준수하는 반응기를 지정하는 사례가 증가하고 있습니다. 제약 회사는 CIP(정지 세척) 작업을 용이하게 하는 매끄러운 내면을 가진 1,000-2만 리터 용량의 필라멘트 와인딩 방식 용기를 채택하고 있습니다. 식품 가공업체들은 간장이나 식초 등의 제품에 FRP 발효조를 활용하고 있는 반면, 수소 모빌리티 분야에서는 차량 기지에 구형 실린더 번들의 도입을 촉진하고 있습니다. FRP 용기 시장에서는 표준화된 솔루션보다 용도에 특화된 엔지니어링이 여전히 중요시되고 있습니다.

중압 용기(10-250바)는 2025년 매출의 46.01%를 차지하며, 산업용 가스 및 도시가스 네트워크 분야에서 FRP 용기 시장을 주도했습니다. 고압 용기(250바르 이상) 시장은 350바르 물류용 및 700바르 모빌리티용 실린더에 대한 수요에 힘입어 2031년까지 연평균 성장률(CAGR) 8.92%를 기록하며 성장할 것으로 예측됩니다.

ASME RTP-1 : 2023 규격은 1바르 미만의 용기를 규정하고 있지만, UN R134, TPED 및 ISO 14692는 고압 수소 용도를 규제하고 있어, 이로 인해 시험 비용이 증가하고 있습니다. 용접연구협의회(WRC)의 2025년판 Bulletin 601은 소유자의 우려 사항에 대응하여, 사용 중 검사에 관한 지침을 제시하고 있습니다. 규격의 조화는 여전히 과제로 남아 있지만, 공동 작업반을 통해 진전이 보이고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 44.89%를 차지했으며, 중국의 일일 600개 RO 용기 생산 시설과 인도의 물 재이용 프로그램에 힘입어 2031년까지 연평균 성장률(CAGR) 9.18%를 나타낼 것으로 전망됩니다. 한국이 2040년까지 620만 대의 수소연료전지차를 도입하겠다는 목표는 고압 실린더에 대한 수요를 뒷받침하고 있는 반면, 아세안(ASEAN) 국가들에서는 팜유 및 양식 시설에 FRP가 채택되고 있습니다. 정부의 보조금과 현지 섬유 공급망이 생산 비용 절감에 기여하고 있어, 이 지역의 경쟁력을 강화하고 있습니다.

북미에서는 철강 기반 시설의 현대화와 셰일가스 관련 수처리 사업이 호재로 작용하고 있습니다. 7구역 및 플로리다주 당국은 2025년에 FRP 재질의 식수 탱크를 설치하여 유지관리 비용을 절감했다고 보고했습니다. 헥사곤 퓨라스사는 메릴랜드주의 생산 능력을 연간 1만 본으로 확대했으며, 한편 캐나다의 오일샌드 사업에서는 광미수 관리에 FRP가 채택되었습니다. 미국의 ‘인플레이션 억제법’에 따른 수소 크레딧은 새로운 고압 용기 공장의 설립을 촉진하고 있습니다.

유럽에서는 엄격한 순환형 경제 규제와 수소 개발 이니셔티브가 결합되고 있습니다. EU 청정 수소 파트너십은 연구개발(R&D)에 자금을 지원하고 있으며, 독일의 시설에서는 연간 4만 개의 실린더가 생산되고 있습니다. 남유럽 및 북아프리카에서는 해수에 의한 부식을 방지하기 위해 해수 담수화 파이프라인에 FRP 재질의 하우징을 사용하고 있습니다. 중동에서는 대규모 해수 담수화 및 석유화학 프로젝트에 복합재료가 활용되고 있으며, 사우디 아람코는 Future Pipe Industries와 제휴하여 공급의 현지화를 추진하고 있습니다. 라틴아메리카에서는 멕시코로부터의 수소 실린더 수주와 브라질 화학 산업의 확대로 인해 초기 성장세를 보이고 있지만, 생산 능력 면에서는 아시아태평양에 뒤처져 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the fRP vessels market size is projected to be USD 4.12 billion in 2025, USD 4.45 billion in 2026, and reach USD 6.55 billion by 2031, growing at a CAGR of 8.03% from 2026 to 2031.

This report is Segmented by Vessel Type (Tanks, Columns, and More), Pressure Classification (Low Pressure (<=10 Bar), and More), Fiber Type (Glass Fiber, Carbon Fiber, and More), Application (Water and Wastewater Treatment, Power and Energy, and More), End-User Industry (Industrial and Chemical, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Value (USD).

Global FRP Vessels Market Trends and Insights

Adoption of Lightweight, Corrosion-Resistant Materials

FRP vessels reduce weight by approximately 70% compared to steel, easing transport and lowering foundation loads in retrofits. Offshore platforms and marine desalination sites prefer composites to eliminate galvanic corrosion, extending service life beyond 30 years without coatings. Chemical plants integrate dual-laminate designs for acids and alkalis, avoiding liner delamination seen in steel. Encore Arabia supplied such tanks to the Saudi Water Conversion Corporation in 2025, reinforcing FRP's viability in high-temperature seawater service. The lifetime-cost advantage outweighs higher upfront prices in harsh operating environments.

Rising Demand from Water and Wastewater Utilities

North American municipalities accelerated steel-to-FRP replacements in 2024-2025 after corrosion failures, with the Zone 7 Water Agency and the Florida Governmental Utility Authority citing lower maintenance and NSF/ANSI 61 compliance. First Line's 3,019-unit order for Qinghai lithium projects shows cross-sector pull between industrial water and mining. India's prefabricated sewage systems increasingly specify FRP for chloride-rich waste streams, leveraging modular moving-bed biofilm designs for rapid installation. Deferred maintenance backlogs now fuel a multiyear procurement wave.

High Initial CAPEX and Installation Costs

Composite vessels cost 1.5-to-2.5X steel alternatives, deterring budget-constrained utilities despite lower lifecycle totals. Large-diameter winders exceed USD 500,000, and specialized lifting gear adds another 10-15% to the delivered price. Retrofit sites may need foundation upgrades due to altered load paths, inflating civil budgets. Familiarity bias also steers buyers toward steel even after corrosion failures shorten tank life.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Chemical and Petrochemical Processing Capacity

- Growth in Renewable Energy and Desalination Projects

- Limited Recyclability and End-of-Life Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tanks accounted for 41.76% of the 2025 revenue, maintaining their dominance in the FRP vessels market due to their extensive use in water treatment and chemical storage. Reactors are projected to grow at a CAGR of 8.69% through 2031, driven by their reliability in handling chemical and thermal stress in process industries. Hybrid tank-reactor designs, incorporating mixers and jackets, are redefining traditional categories, while sanitary fermenters for food and biotech applications contribute to additional market demand.

Process plants increasingly specify ASME RTP-1 or BPE-compliant reactors to avoid pitting issues associated with stainless steel. Pharmaceutical manufacturers are adopting 1,000-20,000 L filament-wound vessels for their smooth inner surfaces, which facilitate CIP operations. Food processors are utilizing FRP fermenters for products like soy sauce and vinegar, while hydrogen mobility is driving the adoption of spherical cylinder bundles in fleet depots. The FRP vessels market continues to emphasize application-specific engineering over standardized solutions.

Medium pressure vessels (10-250 bar) contributed 46.01% of the 2025 revenue, dominating the FRP vessels market across industrial gases and municipal networks. High pressure vessels (>=250 bar) are expected to grow at a CAGR of 8.92% through 2031, driven by demand for 350-bar logistics and 700-bar mobility cylinders.

The ASME RTP-1:2023 standard governs sub-1 bar vessels, while UN R134, TPED, and ISO 14692 regulate high pressure hydrogen applications, leading to increased testing costs. The Welding Research Council's 2025 Bulletin 601 provides guidance for in-service inspections, addressing owner concerns. While code convergence remains a challenge, progress is being made through collaborative working groups.

Geography Analysis

Asia-Pacific captured 44.89% of the 2025 revenue and is projected to grow at a CAGR of 9.18% through 2031, supported by China's 600-unit-per-day RO vessel production facility and India's water renewal programs. South Korea's goal of deploying 6.2 million fuel-cell vehicles by 2040 sustains demand for high pressure cylinders, while ASEAN countries adopt FRP for palm-oil and aquaculture facilities. Government subsidies and local fiber supply chains help maintain low production costs, reinforcing the region's dominance.

North America benefits from steel infrastructure replacements and shale-gas water handling. Zone 7 and Florida authorities installed FRP potable-water tanks in 2025, reporting reduced maintenance costs. Hexagon Purus increased its Maryland production capacity to 10,000 cylinders annually, while Canada's oil sands adopted FRP for tailings water management. The U.S. Inflation Reduction Act's hydrogen credits are supporting the establishment of new high pressure vessel plants.

Europe blends strict circular-economy regulations with hydrogen development initiatives. The EU Clean Hydrogen Partnership funds R&D, and German facilities produce 40,000 cylinders annually. Southern Europe and North Africa are opting for FRP housings in desalination pipelines to prevent seawater corrosion. The Middle-East relies on composites for large-scale desalination and petrochemical projects, with Saudi Aramco partnering with Future Pipe Industries to localize supply. Latin America is showing early momentum with Mexico's hydrogen-cylinder order and Brazil's chemical expansions, though its capacity lags behind Asia-Pacific.

- Aquanomics Systems Limited

- Creative Composites Group

- EPP Composites Pvt Ltd.

- Fiber Tech Composite Pvt. Ltd.

- Fibro Plastichem

- Future Pipe Industries

- Hengshui Jiubo Composites Co., Ltd.

- Hexagon Composites ASA

- International Fiberglass LLC

- Jiangsu Jiuding New Material Co., Ltd.

- Mitsubishi Chemical Infratec Co., Ltd.

- NOV

- Plasticon

- RPS Composites

- Shalin Composites (India) Private Ltd.

- Worthington Enterprises

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of lightweight, corrosion-resistant materials

- 4.2.2 Rising demand from water and wastewater utilities

- 4.2.3 Expansion of chemical and petrochemical processing capacity

- 4.2.4 Growth in renewable-energy and desalination projects

- 4.2.5 Rapid hydrogen storage roll-out for fuel-cell mobility

- 4.2.6 National green-hydrogen mandates unlocking long-run captive demand

- 4.3 Market Restraints

- 4.3.1 High initial CAPEX and installation costs

- 4.3.2 Limited recyclability and end-of-life pathways

- 4.3.3 Skilled-labour shortages in large-diameter filament winding

- 4.3.4 Inconsistent global codes and standards for FRP pressure vessels

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Vessel Type

- 5.1.1 Tanks

- 5.1.2 Columns

- 5.1.3 Pipes

- 5.1.4 Reactors

- 5.1.5 Spherical Bundles (Type-IV H2 storage)

- 5.2 By Pressure Classification

- 5.2.1 Low Pressure (<=10 bar)

- 5.2.2 Medium Pressure (10-250 bar)

- 5.2.3 High Pressure (>=250 bar)

- 5.3 By Fiber Type

- 5.3.1 Glass Fiber

- 5.3.2 Carbon Fiber

- 5.3.3 Aramid Fiber

- 5.3.4 Hybrid Fiber (Glass-Carbon/Glass-Basalt)

- 5.4 By Application

- 5.4.1 Water and Wastewater Treatment

- 5.4.2 Chemical Processing and Storage

- 5.4.3 Oil, Gas and Petrochemical Upstream

- 5.4.4 Food and Beverage Processing

- 5.4.5 Power Generation and Desalination

- 5.4.6 Hydrogen and Alternative-Fuels Storage

- 5.4.7 Pharmaceutical and Biotech Fluids

- 5.5 By End-user Industry

- 5.5.1 Industrial and Chemical

- 5.5.2 Oil, Gas and Petrochemicals

- 5.5.3 Municipal and Private Water Utilities

- 5.5.4 Power and Energy

- 5.5.5 Food and Beverage

- 5.5.6 Other End-user Industries (Pulp and Paper, Mining, Pharma)

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 Japan

- 5.6.1.3 India

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aquanomics Systems Limited

- 6.4.2 Creative Composites Group

- 6.4.3 EPP Composites Pvt Ltd.

- 6.4.4 Fiber Tech Composite Pvt. Ltd.

- 6.4.5 Fibro Plastichem

- 6.4.6 Future Pipe Industries

- 6.4.7 Hengshui Jiubo Composites Co., Ltd.

- 6.4.8 Hexagon Composites ASA

- 6.4.9 International Fiberglass LLC

- 6.4.10 Jiangsu Jiuding New Material Co., Ltd.

- 6.4.11 Mitsubishi Chemical Infratec Co., Ltd.

- 6.4.12 NOV

- 6.4.13 Plasticon

- 6.4.14 RPS Composites

- 6.4.15 Shalin Composites (India) Private Ltd.

- 6.4.16 Worthington Enterprises

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment