|

시장보고서

상품코드

2062342

유전 스케일 억제제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Oilfield Scale Inhibitor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

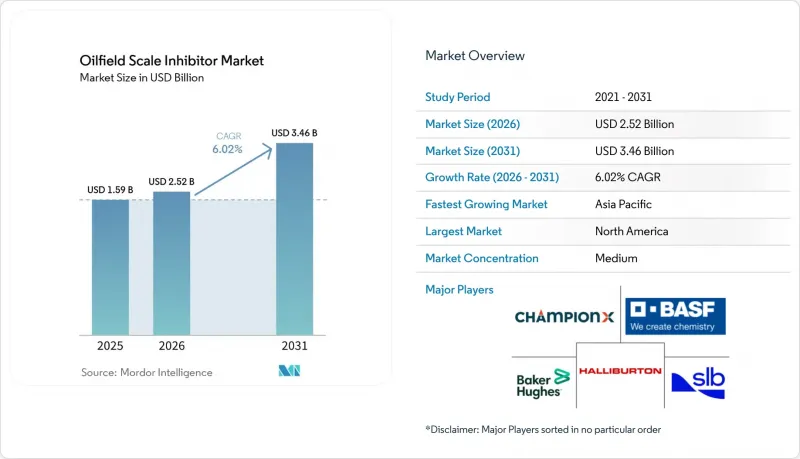

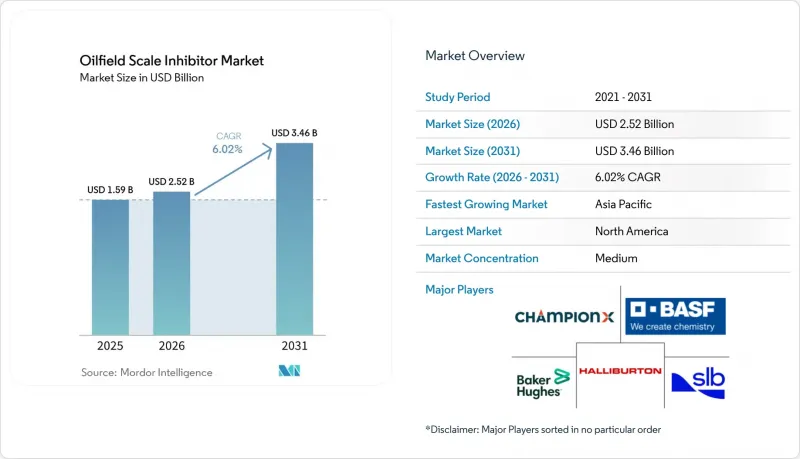

유전 스케일 억제제 시장 규모는 2025년 15억 9,000만 달러로 평가되었습니다. 2026년 25억 2,000만 달러로 확대되어 2031년까지 34억 6,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR은 6.02%를 나타낼 전망입니다.

본 보고서는 유형별(포스폰산염, 카르복실산염/아크릴계, 고분자계, 생분해성, 유기인산염), 용도별(광산 내 방청, 튜브 보호, 표면 처리, 파이프라인 제어, 물 주입, 생산수 재주입), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

세계의 유전 스케일 억제제 시장 동향 및 인사이트

성숙 유전에서 스케일 제어에 대한 수요 증가

세계의 성숙한 유전에서 물 혼합 비율이 증가함에 따라, 운영사들은 스케일 형성 가능성이 높은 염수 증가량을 관리하는 데 있어 점점 더 큰 과제에 직면하고 있습니다. 퍼미안 분지에서는 운영사가 매일 대량의 생산수를 배출하고 있으며, 물 대 원유 비율은 3 : 1에서 12 : 1 사이입니다. 이 물을 재주입하고 재활용하는 과정에서 의도치 않게 탄산 이온이나 황산 이온이 농축되어, 그 결과 고도의 스퀴즈 프로그램에 대한 의존도가 높아지고 있습니다. 아시아태평양은 생산량의 지속적인 감소에 직면하여 개보수 작업과 증산 기술(EOR) 활동이 활발해지고 있는 반면, 노르웨이에서 새로 개발된 북해 유전에서는 18-24개월의 스퀴즈 사이클과 온라인 잔류 분석 장치를 결합하는 이중 접근 방식을 채택하여 부유식 시설의 가동 중단 시간을 줄이고 있습니다. 이러한 동향을 고려할 때, 유전 스케일 억제제 시장은 스케일로 인한 가동 중단으로 발생하는 하루 수백만 달러 규모의 잠재적 손실을 방지하는 비용 대비 효과가 높은 안전 대책으로 부상하고 있습니다.

해양 탐사 및 파이프라인 활동의 확대

2025년까지 브라질의 프레솔트층 생산량은 급증하여 하루 수백만 배럴에 달했습니다. 현재, 신규 FPSO(부유식 생산·저장·하역 설비)에는 18킬로미터에 달하는 타이백을 포괄하는 CO₂가 풍부하게 포함된 유체를 위해 특별히 설계된 스케일 억제제 패키지가 탑재되어 있습니다. CNOOC는 생산량을 확대하여 하루 수백만 배럴의 석유 환산량을 달성했습니다. 이 회사는 해수 주입 방식을 채택했으나, 이러한 전략은 해저 매니폴드에서 황산칼슘 스케일이 발생할 위험을 높입니다. 서아프리카에서도 심해 시스템은 유사한 과제에 직면해 있으며, 체류 시간이 긴 스퀴즈 계열 약제에 의존하고 있습니다. 이에 따라 2026년부터 2031년까지의 예측 기간 동안 유전 스케일 억제제 시장의 매출 증가가 예상됩니다.

원유 가격 변동이 화학약품 예산을 억제

브렌트유 가격은 2026년 2분기에 정점을 찍은 뒤, 이듬해에는 하락할 것으로 전망됩니다. 이러한 급격한 하락은 과거에 재량적인 화학약품 지출 삭감으로 이어져 왔습니다. 이에 대응하여 북미의 독립 기업들은 이미 비긴급 스퀴즈 작업을 연기하고 있으며, 이는 유전 스케일 억제제 시장의 주요 공급업체들에 압박을 가하고 있습니다.

부문별 분석

2025년, 뛰어난 내열성과 1,000 mg/L를 초과하는 내칼슘성을 갖춘 포스폰산염계 제품이 유전 스케일 억제제 시장에서 45.82%라는 압도적인 점유율을 차지했으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.83%를 기록하며 성장했습니다. 2026년까지 중동에서 진행 중인 해수 주입 프로젝트에서 서브 ppm 수준의 처리 농도를 보이는 아미노메틸렌계 혼합물이 점점 더 선호받게 되어, 이러한 성장을 뒷받침할 것으로 보입니다. 카르복실산염이나 아크릴계 제품은 인 배출을 억제하라는 EPA 및 REACH의 규제 압력으로 인해 보급이 확대되고 있지만, 이러한 대체품은 대부분의 경우 두 자릿수 ppm 단위의 투여량이 필요합니다. 이러한 요건으로 인해, 화학 약품의 물류 비용이 총비용에 큰 영향을 미치는 브라질의 심해 지역에서는 도입이 제한적입니다. 스케일 이온 외에도 부유 고형물 관리가 필수적인 생산수 재주입 네트워크에서는 고분자계 및 인을 배합한 하이브리드 제품의 인기가 높아지고 있습니다. 특히 주목할 점은 PETRONAS가 광범위한 파이프라인 네트워크 전반에 걸쳐 다기능 분산제를 채택하고 있다는 점입니다. 생분해성 제제는 틈새 시장에 머물러 있지만, 비율 기준으로 볼 때 가장 높은 성장률을 보이고 있습니다. 호카이(北海)의 운영사는 OSPAR의 ‘옐로우 C’ 등급으로 분류되는 제품에 투자하고 있어, 시장의 환경 중시 태도가 두드러지게 나타나고 있습니다.

황화수소나 철의 동반 생산과 같은 과제에 직면한 유정에서는 기존의 단일 화학 물질을 이용한 방법으로는 효과가 미흡한 경우에도 유기인산염이나 시너지 효과가 있는 혼합물이 해결책이 됩니다. 각 공급업체들은 효율성을 높이기 위해 추적 표지 분자에 대한 시험을 진행하고 있습니다. 광섬유를 통해 감지할 수 있는 이러한 분자 덕분에, 운영자는 광산 내 분포를 정확하게 파악하고 과도한 처리를 줄일 수 있으므로, 이러한 특수 솔루션 시장 점유율 확대로 이어질 가능성이 있습니다. 시장 상황은 복잡합니다. 세계의 주요 기업들이 REACH 등록 서류를 제출하는 반면, 지역 배합 제조업체들은 규제가 완화된 점을 활용하여 기존의 포스폰산염을 적극 추진하고 있습니다. 환경 규제의 강화와 작동 온도의 상승에 따라 다양한 화학 물질에 대한 수요가 증가함에 따라, 2026년부터 2031년까지의 예측 기간 동안 기존 억제제 계열과 신흥 억제제 계열이 모두 수용되는 균형 잡힌 시장이 유지될 것으로 보입니다.

지역별 분석

2025년, 북미는 유전 스케일 억제제 시장의 36.11%를 차지했습니다. 이는 셰일 지역, 멕시코만 연안 및 바카 무엘타에서 활동이 집중된 데 기인합니다. 퍼미안 분지에서는 생산수 처리에 있어 지속적인 약제 주입이 필수적이었습니다. 애팔래치아 셰일 지역의 운영사들은 가격 압박과 유층 압축 구간의 장기화에 직면해 있으며, 지역 전체적으로 다양한 동향이 나타나고 있습니다. 2026년부터 2031년까지의 예측 기간 동안, 북미 유전 스케일 억제제 시장은 꾸준한 성장세를 보였으나, 원유 가격 변동이 단기 예산에 어려움을 초래했습니다. 캐나다에서는 고온의 역청에 대응하는 억제제가 필요한 오일샌드 사업 분야에서 꾸준하지만 완만한 단위 성장이 나타났습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 선두를 달렸으며, 2026년부터 2031년까지의 예측 기간 동안 연평균 성장률(CAGR) 6.79%를 기록했습니다. 중국의 해양 개발 확대, 인도네시아의 폴리머 주입, 말레이시아의 급성장하는 파이프라인망이 화학물질 사용 증가를 촉진했습니다. 아세안 지역의 유전에서는 연간 생산량 감소로 인해 개보수 작업이 필요해지면서, 염수 pH 상승 및 스케일 형성 위험이 높아지고 있지만, 유전 스케일 억제제 시장 전망은 여전히 낙관적입니다. 기준 연도인 2025년에 중국해양석유(CNOOC)의 생산 증가와 보하이만에서의 해수 주입이 수요를 확대시켰습니다. 또한, 인도 KG 분지에서 ONGC와 릴라이언스의 제휴를 통해, 높은 염분 내성을 가진 화학 약품이 필요한 생산량을 확보했습니다. 페트로나스(PETRONAS)의 PM3 프로젝트 20년 연장은 동남아시아에서 화학제품에 대한 지속적인 수요를 입증하는 것이었습니다.

유럽에서는 완만한 성장에 그쳤지만, 소비는 안정적으로 유지되었습니다. 기준 연도인 2025년에는 노르웨이에서 새로 개발된 7개의 유전에서 고성능 스케일 억제제, 특히 전기가 공급되는 해저 시스템에 대응하는 제품에 대한 수요가 증가했습니다. 영국에서는 생산량의 점진적인 감소를 상쇄하는 듯, 폐지 조치에 따른 유정 보존용 화학 약품에 대한 간헐적인 수요가 나타났습니다. 러시아 시장은 규모가 크지만 제재의 영향으로 불확실한 상황이 지속되고 있어, 주로 국내의 포스폰산염 생산에 의존해 왔습니다. 중동은 성장률 면에서는 1위를 차지하지는 못했지만, 절대량 면에서는 가장 큰 폭 증가가 예상되었습니다. 사우디 아람코, ADNOC, 쿠웨이트 석유공사 등 업계 주요 기업들은 주입 및 석유 증산 회수(EOR) 인프라에 막대한 투자를 단행했습니다. 남미에서는 브라질이, 특히 아르헨티나 이외의 지역에서 주목을 받았습니다. 페트로브라스는 기준 연도인 2025년의 생산량을 바탕으로, CO₂가 풍부하게 함유된 프리솔트층의 유체용으로 특별히 설계된 내산성 억제제를 도입했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the oilfield scale inhibitor market size is expected to increase from USD 1.59 billion in 2025 to USD 2.52 billion in 2026 and reach USD 3.46 billion by 2031, growing at a CAGR of 6.02% over 2026-2031.

This report is Segmented by Type (Phosphonates, Carboxylates/Acrylics, Polymeric, Biodegradable, and Organophosphates), Application (Downhole Prevention, Tubing Protection, Surface Treatment, Pipeline Control, Water Injection, and Produced-Water Reinjection), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). Market Forecasts are Provided in Value (USD).

Global Oilfield Scale Inhibitor Market Trends and Insights

Growing Demand for Scale Control in Mature Fields

Operators face increasing challenges in managing the growing volumes of brine, which have a high potential for scaling, as mature reservoirs worldwide experience rising water cuts. In the Permian Basin, operators generate significant volumes of produced water daily, with water-to-oil ratios ranging from 3:1 to 12:1. As they reinject and recycle this water, they inadvertently concentrate carbonate and sulfate ions, leading to a heightened reliance on advanced squeeze programs. While the Asia-Pacific region has grappled with a sustained production decline, intensifying workover and Enhanced Oil Recovery (EOR) activities, Norway's newly tapped North Sea fields have adopted a dual approach - pairing 18-24 month squeeze cycles with online residual analyzers to curtail downtime on floating facilities. Given these dynamics, the oilfield scale inhibitor market has emerged as a cost-effective safeguard, protecting against potential million-dollar daily losses stemming from scale-induced outages.

Expansion of Offshore Exploration and Pipeline Activities

By 2025, Brazil's pre-salt output surged, reaching millions of barrels per day. Each new FPSO now features inhibitor packages specifically designed for CO2-rich fluids, spanning 18-kilometer tiebacks. CNOOC increased its production, achieving millions of barrels of oil equivalent per day. The company adopted seawater injection, a strategy that increases the risk of calcium-sulfate scaling in subsea manifolds. In the West-African region, deepwater systems face similar challenges, relying on long-residence squeeze chemistries that are expected to enhance revenue in the oilfield scale inhibitor market during the forecast period of 2026-2031.

Volatile Crude Prices Curbing Chemical Budgets

Brent prices are projected to peak in Q2 2026 before declining in the following year. This significant drop has historically led to a reduction in discretionary chemical spending. In response, North American independents are already postponing non-critical squeezes, putting pressure on premium suppliers in the oilfield scale inhibitor market.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of EOR Techniques Elevating Chemical Consumption

- Growth in Unconventional Oil Resources

- Tightening Discharge Regulations on Phosphorus and Heavy Metals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, phosphonates, with a robust thermal endurance and a calcium tolerance exceeding 1,000 mg/L, captured a dominant 45.82% share of the oilfield scale inhibitor market, growing at an annual rate of 6.83% CAGR from 2026 to 2031. By 2026, ongoing seawater-injection projects in the Middle-East, increasingly favoring aminomethylene blends at sub-ppm treatment rates, will support this growth. While carboxylates and acrylics are gaining traction - driven by EPA and REACH pressures to curtail phosphorus discharge - these alternatives often require double-digit ppm dosages. This necessity has limited their adoption in deepwater Brazil, where chemical logistics heavily impact total costs. In produced-water reinjection networks, where managing suspended solids alongside scaling ions is vital, polymeric and phosphorus-tagged hybrids are becoming more popular. Notably, PETRONAS utilizes multifunctional dispersants throughout its extensive pipeline network. Although biodegradable formulations occupy a niche segment, they are witnessing the fastest growth rate in percentage terms. Operators in the North Sea are investing in products classified under OSPAR's "Yellow C" designation, highlighting the market's environmental focus.

For wells facing challenges like hydrogen sulfide or iron co-production, organophosphates and synergistic blends provide solutions where traditional single-chemistry methods falter. Suppliers are trialing tracer-tagged molecules to enhance efficiency. Detectable via fiber optics, these molecules allow operators to accurately map downhole distribution and reduce overtreatment, potentially boosting the market share for these specialized solutions. The landscape is intricate: while global giants register REACH dossiers, regional formulators champion classic phosphonates, benefiting from lighter oversight. As environmental regulations tighten and operational temperatures rise, the demand for diverse chemistries ensures a balanced market, accommodating both established and emerging inhibitor families during the forecast period of 2026-2031.

Geography Analysis

In 2025, North America commanded a 36.11% share of the oilfield scale inhibitor market, driven by activities converging in shale regions, the offshore Gulf, and Vaca Muerta. Continuous chemical dosing was essential for the produced-water stream in the Permian Basin. Operators in the Appalachian shale, facing price pressures and extended squeeze intervals, are resulting in mixed dynamics across the region. While North America's oilfield scale inhibitor market was on a steady growth trajectory during the forecast period 2026-2031, fluctuations in crude prices posed challenges to short-term budgets. In Canada, oil sands operations, requiring inhibitors compatible with hot bitumen, experienced consistent but slower unit growth.

Asia-Pacific led as the fastest-growing region, registering a 6.79% CAGR during the forecast period 2026-2031. China's offshore expansions, Indonesia's polymer floods, and Malaysia's burgeoning pipeline network spurred heightened chemical usage. Despite annual declines in ASEAN fields prompting workovers and increased brine pH and scaling risks, the oilfield scale inhibitor market's outlook remained optimistic. CNOOC's production boost in the base year 2025, alongside seawater injections in Bohai Bay, amplified demand. Furthermore, the collaboration between ONGC and Reliance in India's KG basin unlocked volumes necessitating high-salinity-tolerant chemicals. PETRONAS's two-decade extension of the PM3 project underscored the enduring chemical demand in Southeast Asia.

Europe experienced modest growth yet sustained stable consumption. In the base year 2025, Norway's seven newly tapped fields favored high-performance inhibitors, particularly those adept against electrified subsea systems. The United Kingdom's decommissioning activities spurred sporadic demand for well-preservation chemicals, offsetting the nation's gradual production declines. Russia's market, while sizable, remained opaque due to sanctions and leaned predominantly on domestic phosphonate production. The Middle-East, though not leading in percentage growth, was poised for the most substantial absolute volume increase. Industry giants such as Saudi Aramco, ADNOC, and Kuwait Oil Company made significant investments in injection and enhanced oil recovery (EOR) infrastructure. In South America, Brazil emerged as a focal point, particularly in regions outside Argentina. Petrobras, capitalizing on its production in the base year 2025, deployed acid-stable inhibitors specifically designed for CO2-rich pre-salt fluids.

- Afton Chemical

- Arkema

- Ashland

- Baker Hughes Company

- BASF

- ChampionX

- Clariant

- Dow

- Halliburton

- Huntsman

- Innospec

- Italmatch Oil & Gas

- Kemira

- LANXESS

- SLB (Schlumberger)

- SNDB

- SNF

- Solenis

- Solvay

- Stepan Company

- Thermax Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for scale control in mature fields

- 4.2.2 Expansion of offshore exploration and pipeline activities

- 4.2.3 Adoption of EOR techniques elevating chemical consumption

- 4.2.4 Growth in unconventional oil resources

- 4.2.5 Real-time digital inhibitor dosing and monitoring

- 4.2.6 Shift toward produced-water reinjection in water-scarce regions

- 4.3 Market Restraints

- 4.3.1 Volatile crude prices curbing chemical budgets

- 4.3.2 Tightening discharge regulations on phosphorus and heavy metals

- 4.3.3 All-electric subsea systems reducing chemical injection points

- 4.3.4 Persistent supply-chain risk for phosphonate intermediates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Phosphonates

- 5.1.2 Carboxylates/Acrylics

- 5.1.3 Polymeric/Phosphorus-tagged Polymers

- 5.1.4 Biodegradable and Green Inhibitors

- 5.1.5 Organophosphates and Synergistic Blends

- 5.2 By Application

- 5.2.1 Downhole Scale Prevention (Squeeze)

- 5.2.2 Tubing and Casing Protection

- 5.2.3 Surface Facility Treatment

- 5.2.4 Pipeline and Flowline Scale Control

- 5.2.5 Water-Injection Systems

- 5.2.6 Produced-Water Reinjection and Disposal

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Nordic Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 Afton Chemical

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Baker Hughes Company

- 6.4.5 BASF

- 6.4.6 ChampionX

- 6.4.7 Clariant

- 6.4.8 Dow

- 6.4.9 Halliburton

- 6.4.10 Huntsman

- 6.4.11 Innospec

- 6.4.12 Italmatch Oil & Gas

- 6.4.13 Kemira

- 6.4.14 LANXESS

- 6.4.15 SLB (Schlumberger)

- 6.4.16 SNDB

- 6.4.17 SNF

- 6.4.18 Solenis

- 6.4.19 Solvay

- 6.4.20 Stepan Company

- 6.4.21 Thermax Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Smart inhibitors with embedded fibre-optic sensing