|

시장보고서

상품코드

2062351

슬라이드웨이 오일 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Slideway Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

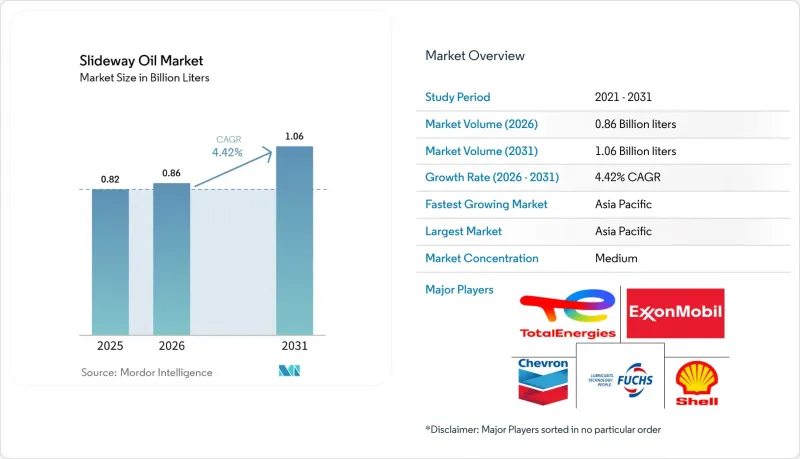

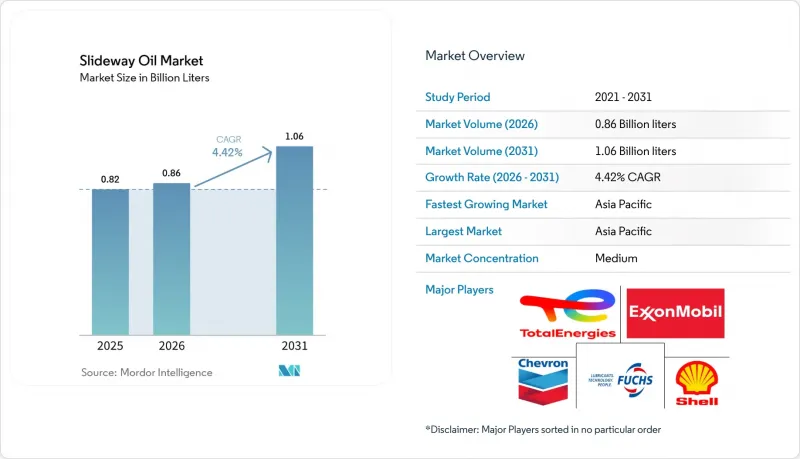

슬라이드웨이 오일 시장 규모는 2025년에 8억 2,000만 리터로 평가되었습니다. 2026년 8억 6,000만 리터에서 2031년까지 10억 6,000만 리터에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 4.42%를 나타낼 전망입니다.

본 보고서는 기유(광물유계, 합성유계, 바이오계), 용도(CNC 공작기계, 수평 슬라이드웨이, 수직 슬라이드웨이 등), 최종 사용자 산업(금속 가공용 중장비 및 기계 가공, 자동차 및 자동차 부품 등), 지역(아시아태평양, 북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 수량(리터) 기준으로 제시되어 있습니다.

세계의 슬라이드웨이 오일 시장 동향 및 분석

정밀 가공의 확대와 CNC의 보급

중국은 2024년에 70만 대의 공작기계를 출하했으며, 새로운 5축 가공 센터에는 저이동성 슬라이딩 표면 오일이 필요하기 때문에 향후 윤활유 수요량의 기준을 확립했습니다. 파낙(FANUC)의 12억 달러 규모 충칭 확장 계획과 트럼프프(Trumpf)의 코네티컷주 스마트 팩토리는 북미의 유사한 성장 추세를 여실히 보여주고 있으며, 자동 팔레트 체인저와 호환되는 폐쇄형 윤활 시스템을 갖춘 고정밀 베드에 대한 전 세계적인 수요를 반영하고 있습니다. 베트남과 인도네시아에서 소형 CNC 선반의 채택이 확대됨에 따라 도입 대수가 더욱 늘어나고, 교체 수요가 증가하면서 공급업체들은 오일 교환 주기를 30-40% 연장하는 합성 에스테르 블렌드의 도입을 촉진하고 있습니다.

신흥국에서의 금속 가공 생산 가속화

인도의 1,000억 루피 규모의 공작기계 생산과 멕시코의 360억 달러 규모의 니어쇼어링을 통한 자금 유입으로 인해, 고온 다습한 환경에서도 확실한 윤활막 형성을 보장하는 슬라이드웨이 오일 수요가 증가하고 있습니다. 동시에, 30조 8,000억 위안 규모의 중국 기계 산업에서는 공용 오일 탱크 방식의 CNC 셀에서 오일 탱크 오염을 방지하기 위한 유화 방지 처방에 여전히 의존하고 있습니다. 제품 판매에 더해 오일 분석 서비스를 제공하는 공급업체는 다년 유지보수 계약을 체결하여 현물 가격 경쟁의 영향을 받지 않고 있습니다.

원유 가격에 연동되는 기초유가의 변동

2025년 4분기, 미국의 윤활유 생산자물가지수는 2021년 이후 최저 수준을 기록했습니다. 그러나 그 후 중동에서 발생한 예기치 못한 가동 중단으로 인해 공급이 부족해지고 현물 가격이 상승하면서, 헤지 프로그램을 갖추지 않은 사료 제조업체들의 이익률이 압박을 받았습니다. 브렌트 원유 가격이 10% 변동하면, 기초유 비용은 6-8% 변동하게 됩니다. 이에 따라 시노펙은 프리미엄 제품 공급에 있어 원유 가격에 대한 의존도를 낮추기 위해, 연간 3만 톤 규모의 메탈로센계 PAO 플랜트에 대한 투자를 결정했습니다.

부문별 분석

2025년 기준으로, 슬라이드웨이 오일 시장 점유율의 55.89%를 광물유계가 차지했으며, 합성 PAO 및 에스테르 블렌드는 고온 용도에 사용되었습니다. 바이오 부문은 2031년까지 연평균 성장률(CAGR) 5.16%를 기록하며, 다른 모든 기초유 범주를 상회할 것으로 예측됩니다. Shell PANOLIN 및 TotalEnergies BIOHYDRAN과 같은 제품은 인증된 생분해성 오일이 극압 성능을 유지하면서도 수명 주기 전반에 걸친 CO2 배출량을 최대 84%까지 줄일 수 있음을 보여줍니다.

그러나 원자재 비용의 급등과 ISO VG 320을 초과하는 HEES 인증 유체공급 부족으로 인해 대형 수직 슬라이드웨이에 이를 도입하는 데 차질이 생기고 있습니다. 에폭시화 대두유 및 톨오일 에스테르의 생산 확대에 힘입어, 2029년까지 그룹 II 광물유와의 가격 차이를 해소할 수 있을 것으로 보입니다.

지역별 분석

아시아태평양은 2025년에 슬라이드웨이 오일 시장 점유율의 47.57%를 차지했으며, 중국의 공작기계 생산 대수 70만 대와 인도의 성장하는 수출용 기계 가공 클러스터에 힘입어 2031년까지 연평균 성장률(CAGR) 5.23%를 나타낼 것으로 전망됩니다. 북미는 2,390억 달러 규모의 미국 제조업 건설의 혜택을 누리고 있으며, EPA(미국 환경보호청)의 위험 관리 계획 개정에 따라 바이오 제품의 도입이 촉진되고 있습니다. 유럽은 공작기계 수주량이 들쑥날쑥한 반면, 규제 측면의 발전을 주도하며 PFAS 프리 혁신의 거점으로서의 입지를 확고히 하고 있습니다. 중동 및 아프리카는 규모는 작지만, 고온 환경에 적합한 블렌드를 현지화하는 퀘이커 호튼 페트로루브와 같은 파트너십을 통해, 수요에 맞춘 솔루션이 주목받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the slideway oil market size was valued at 0.82 Billion liters in 2025 and is estimated to grow from 0.86 Billion liters in 2026 to reach 1.06 Billion liters by 2031, at a CAGR of 4.42% during the forecast period (2026-2031).

This report is Segmented by Base Oil (Mineral Oil-Based, Synthetic Oil-Based, and Bio-Based), Application (CNC Machines, Horizontal Slideways, Vertical Slideways, and More), End-User Industry (Metalworking Heavy Equipment and Machining, Automotive and Auto Components, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Liters).

Global Slideway Oil Market Trends and Insights

Expanding Precision Machining and CNC Penetration

China shipped 700,000 machine-tool units in 2024, setting a benchmark for future lubricant volumes as each new five-axis center requires low-migration slideway oil. FANUC's USD 1.2 billion Chongqing expansion and TRUMPF's Connecticut smart factory highlight similar growth trends in North America, reflecting the global demand for high-accuracy beds with closed-loop lubrication systems compatible with automated pallet changers. The increasing adoption of compact CNC lathes in Vietnam and Indonesia is further expanding the installed base, boosting replacement consumption, and encouraging suppliers to introduce synthetic-ester blends that extend drain intervals by 30-40%.

Accelerating Metal-Working Output in Emerging Economies

India's INR 100 billion machine-tool production and Mexico's USD 36 billion in nearshoring inflows are driving demand for slideway oils that ensure reliable film formation in humid, high-temperature environments. At the same time, China's CNY 30.8 trillion machinery industry continues to rely on demulsifying formulations that prevent sump contamination in shared-fluid CNC cells. Suppliers offering oil-analysis services alongside product sales are securing multi-year maintenance contracts, insulating themselves from spot-price competition.

Crude-Linked Volatility in Base-Oil Prices

In the fourth quarter of 2025, the U.S. Producer Price Index for lubricants reached its lowest level since 2021. However, unplanned outages in the Middle-East subsequently tightened supply and drove up spot prices, squeezing margins for formulators without hedging programs. A 10% fluctuation in Brent crude prices translates to a 6-8% shift in base-oil costs, prompting Sinopec to invest in a 30,000 tpa metallocene PAO plant to reduce reliance on crude benchmarks for premium supply.

Other drivers and restraints analyzed in the detailed report include:

- Industry 4.0 Investments in Automated Tool Rooms

- Tightening VOC-Emission Rules Favoring Bio-Based Slideway Fluids

- Chemical Incompatibility with Water-Miscible Metalworking Fluids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral oil-based represented 55.89% of the slideway oil market share in 2025, with synthetic PAO and ester blends serving high-temperature applications. The bio-based segment is anticipated to grow at a CAGR of 5.16% through 2031, surpassing all other base oil categories. Products such as Shell PANOLIN and TotalEnergies BIOHYDRAN illustrate that certified biodegradable oils can maintain extreme-pressure performance while reducing CO2 life-cycle emissions by up to 84%.

Nevertheless, high feedstock costs and the limited availability of HEES-certified fluids above ISO VG 320 hinder adoption in heavy-duty vertical slideways. Expanding the production of epoxidized-soybean and tall-oil esters could help bridge the price gap with Group II mineral oils by 2029.

Geography Analysis

Asia-Pacific accounted for 47.57% of the slideway oil market share in 2025 and is projected to grow at a CAGR of 5.23% through 2031, supported by China's machine-tool production of 700,000 units and India's growing export machining clusters. North America benefits from USD 239 billion in U.S. manufacturing construction, with EPA Risk Management Plan revisions encouraging the adoption of bio-based products. Europe, while facing mixed machine-tool order volumes, leads in regulatory advancements, positioning it as a hub for PFAS-free innovations. The Middle-East and Africa, though starting from a smaller base, are attracting tailored solutions through partnerships like Quaker Houghton-Petrolube, which localizes blending for high-temperature environments.

- Blaser Swisslube AG

- BP p.l.c.

- Chem Arrow Corporation

- Chevron Corporation

- ENEOS Corporation

- Exxon Mobil Corporation

- FUCHS

- Kluber Lubrication SE

- LUKOIL

- MotulTech (Motul SA)

- Petro-Canada Lubricants Inc.

- PETRONAS Lubricants International

- PT Idemitsu Lube Techno Indonesia

- Quaker Houghton

- Shell plc

- Sinopec Lubricants Co.

- TotalEnergies

- Valvoline Global Operations

- Yushiro Chemical Industry Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding precision machining and CNC penetration

- 4.2.2 Accelerating metal-working output in emerging economies

- 4.2.3 Industry 4.0 investments in automated tool rooms

- 4.2.4 Surge in retrofit/maintenance of ageing slideway beds

- 4.2.5 Tightening VOC-emission rules favouring bio-based slideway fluids

- 4.2.6 IIoT-enabled "smart-lubrication" demand for condition-based dosing

- 4.3 Market Restraints

- 4.3.1 Crude-linked volatility in base-oil prices

- 4.3.2 Chemical incompatibility with water-miscible metal-working fluids

- 4.3.3 Stringent disposal and REACH/EPA compliance costs

- 4.3.4 Adoption of dry/self-lubricating linear-motion polymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Base Oil

- 5.1.1 Mineral oil-based

- 5.1.2 Synthetic oil-based

- 5.1.3 Bio-based

- 5.2 By Application

- 5.2.1 CNC Machines

- 5.2.2 Horizontal Slideways

- 5.2.3 Vertical Slideways

- 5.2.4 Grinders

- 5.2.5 Lathes

- 5.2.6 Other Applications (clean-room tools, etc.)

- 5.3 By End-user Industry

- 5.3.1 Metalworking, Heavy Equipment and Machining

- 5.3.2 Automotive and Auto Components

- 5.3.3 Aerospace and Defense

- 5.3.4 Marine and Rail

- 5.3.5 Other Industries (Electronics, Energy and Power)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Blaser Swisslube AG

- 6.4.2 BP p.l.c.

- 6.4.3 Chem Arrow Corporation

- 6.4.4 Chevron Corporation

- 6.4.5 ENEOS Corporation

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 FUCHS

- 6.4.8 Kluber Lubrication SE

- 6.4.9 LUKOIL

- 6.4.10 MotulTech (Motul SA)

- 6.4.11 Petro-Canada Lubricants Inc.

- 6.4.12 PETRONAS Lubricants International

- 6.4.13 PT Idemitsu Lube Techno Indonesia

- 6.4.14 Quaker Houghton

- 6.4.15 Shell plc

- 6.4.16 Sinopec Lubricants Co.

- 6.4.17 TotalEnergies

- 6.4.18 Valvoline Global Operations

- 6.4.19 Yushiro Chemical Industry Co.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment