|

시장보고서

상품코드

2062381

공기입 타이어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pneumatic Tire - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

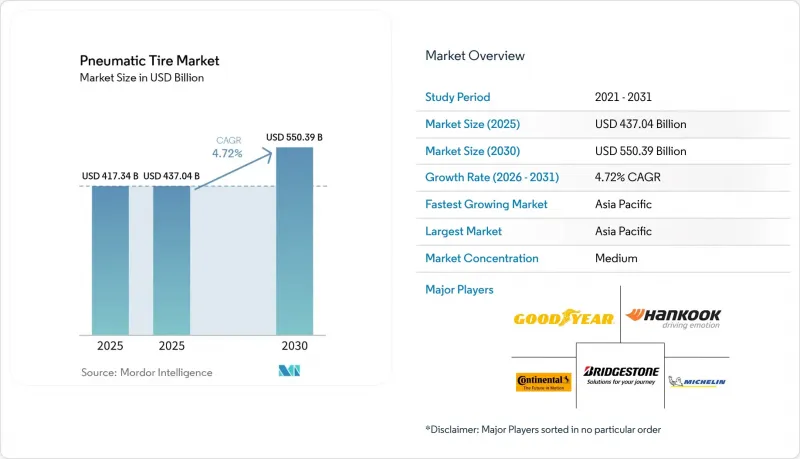

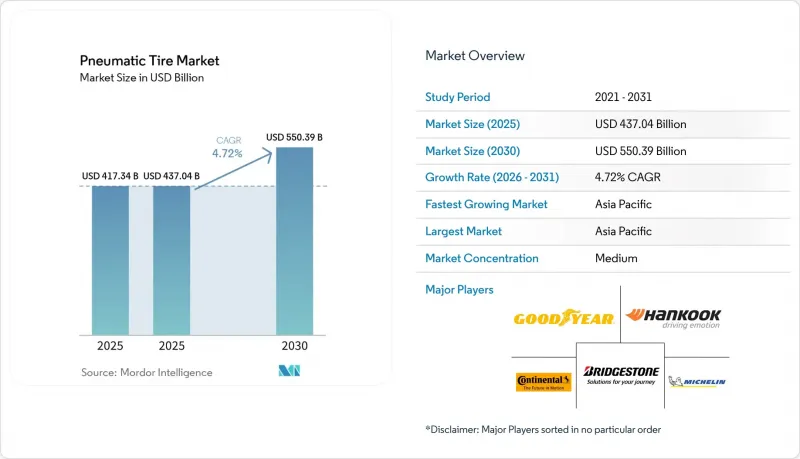

Mordor Intelligence에 의하면, 공기입 타이어 시장 규모는 2025년 4,173억 4,000만 달러로 평가되었고, 2025년 4,370억 4,000만 달러에서 2030년까지 5,503억 9,000만 달러로 확대될 전망이며, 2025-2030년 CAGR 4.72%를 나타낼 것으로 예측됩니다.

본 보고서는 타이어 유형별(레이디얼 타이어 및 바이애스 타이어), 유통 채널별(OEM 및 애프터마켓), 차량 유형별(승용차, 소형 상용차, 대형 상용차, 이륜차 및 오프로드 차량), 그리고 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 공기입 타이어 시장 동향 및 인사이트

연비 효율이 높고 성능이 뛰어난 타이어에 대한 수요 증가

플릿 사업자들은 2027년 모델 연도부터 강화될 기업 평균 연비 기준(CAFE)을 준수하기 위해 구름 저항을 줄이는 데 주력하고 있습니다. 이에 따라 미국 도로교통안전국(NHTSA)이 지적한 바와 같이, 젖은 노면 접지 성능을 저해하지 않으면서 히스테리시스를 줄여주는 실리카가 풍부하게 함유된 트레드 컴파운드와 바이오 오일의 사용이 확대되고 있습니다. 유럽연합(EU) 연비 라벨에서 A 등급을 획득한 콘티넨탈(Continental)의 EcoContact이나 미쉐린(Michelin)의 e.Primacy와 같은 제품들은 고성능과 안전 요건을 동시에 충족할 수 있음을 입증하고 있습니다. 또한, 전기차(EV)의 토크 증가로 인해 타이어 마모율이 약 20% 상승함에 따라, OEM 업체들은 타이어의 수명을 연장하기 위해 강화된 사이드월과 최적화된 트레드 패턴을 요구하고 있습니다. 이러한 발전 덕분에 공급업체들은 공기입 타이어 시장에서 가격 프리미엄을 유지할 수 있게 되었습니다. 기술 혁신은 계속해서 고성능 타이어 부문의 성장을 주도하고 있으며, 그 성장률은 교체용 타이어 시장 전체의 성장률을 상회하고 있습니다.

전자상거래 및 물류 차량의 확대

미국 우정공사(USPS)는 2028년까지 10만 6,000대의 차세대 배송 차량을 도입할 계획이며, 그중 6만 6,000대는 배터리식 전기차가 될 것입니다. 이러한 변화는 도시 지역의 배송 주행 거리 증가를 여실히 보여주고 있습니다. 굿이어가 로턴 공장에 3억 2,000만 달러를 투자해 진행하는 설비 현대화는 주거 지역 배송 노선을 위해 특별히 설계된, 사이드월이 강화된 저소음 타이어의 생산 능력 확대를 목적으로 하고 있습니다. 인도나 인도네시아 등 시장에서는 온라인 쇼핑의 급속한 성장에 힘입어 경상용차 차량군이 바이어스 타이어에서 레이디얼 타이어로 전환되고 있습니다. 레이디얼 타이어는 잦은 출발과 정지를 반복할 때 열 관리에 적합합니다. 소포 처리량이 증가함에 따라, 차량 관리자들은 텔레매틱스 시스템과 연동되는 데이터 지원 타이어를 도입하고 있으며, 이로 인해 교체 비용이 증가하고 있습니다. 이러한 동향들이 복합적으로 작용하여 공기입 타이어 시장의 수익이 점진적으로 증가하는 데 기여하고 있습니다.

폐기물 및 미세플라스틱에 관한 환경 규제 강화

유로 7 규제로 인해 미세먼지 배출 기준이 강화되었으며, 2032년까지 더욱 엄격해질 것으로 예측됩니다. 또한, 미국에서는 24개 주에서 확대 생산자 책임(EPR)법을 시행하여 폐기 비용을 제조업체에 전가하고 있습니다. 내구성 향상을 목적으로 경질 트레드 컴파운드를 사용하면 젖은 노면 접지력에 영향을 미칠 수 있으므로, 안전 기준을 유지하기 위해서는 실리카 분산 기술 및 폴리머 가교 기술에 대한 새로운 투자가 필요합니다. Pew Charitable Trusts에 따르면, 2050년까지 도로 운송에서 발생하는 미세먼지 배출량의 90%가 타이어와 브레이크의 마모로 인해 발생할 것으로 예측되며, 규제 당국의 감시가 강화될 전망입니다. 이러한 규정을 준수함에 따라 단위 비용이 2%-4% 상승할 것으로 추정되며, 특히 공기입 타이어 시장의 낮은 이익률을 기록하는 공급업체들에게는 가격 경쟁력에 영향을 미칠 것으로 보입니다.

부문별 분석

레이디얼 타이어는 연비 효율과 고속 주행 시 안전성에 대한 규제가 강화된 것을 배경으로, 2025년에는 시장 가치의 77.12%를 차지했습니다. 바이아스 타이어 시장은 2031년까지 연평균 성장률(CAGR) 5.15%를 기록하며, 공기입 타이어 시장 전체의 연평균 성장률을 상회할 것으로 전망됩니다. 인도에서는 이륜차 보유 대수가 2억 2,000만 대를 넘어선 탓에, 특히 농촌 지역 사용자들 사이에서 펑크 방지 성능과 합리적인 가격 덕분에 바이어스 타이어가 여전히 인기를 끌고 있습니다. 마찬가지로, 사하라 사막 이남의 아프리카에서는 비포장 도로를 주행하는 소형 트럭이나 삼륜차에 바이어스 타이어가 선호되고 있습니다. 레이디얼 타이어는 특히 전기차(EV) 분야에서 여전히 매출의 대부분을 차지하고 있습니다. 브리지스톤은 일본 국내에 270억 엔(1억 7,000만 달러)을 투자하여, 대형 전기차 배터리 팩용으로 설계된 고강성 레이디얼 타이어의 생산 능력을 확대했습니다.

바이어스 타이어 제조업체들도 현대화를 추진하고 있습니다. 중책고무나 트라이앵글 타이어와 같은 기업들은 레이디얼 타이어의 우위가 그리 두드러지지 않는 광업 및 건설 분야에 대응하기 위해 엔지니어링 타이어 라인업을 강화하고 있습니다. 한편, 콘티넨탈의 태국 공장은 승차감과 토크 제어를 향상시키는 오토바이용 및 전기차용 레이디얼 타이어 생산에 주력하고 있습니다. 각 제조업체는 성능과 지속가능성의 균형을 맞추기 위해, 공기입 타이어 시장의 다양한 이용 사례에 대응할 수 있도록 제품 포트폴리오의 다각화를 추진하고 있습니다.

지역별 분석

아시아태평양은 2025년에 시장 가치의 44.15%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 5.49%로 성장할 것으로 전망됩니다. 이러한 성장은 중국의 연간 생산량 8억 4,000만 개, 인도의 레이디얼 타이어로의 전환, 그리고 아세안(동남아시아 국가 연합) 국가들의 상용차 시장 확대에 힘입은 것입니다. 링롱(Linglong)이 7억 5,000만 달러를 투자한 안후이성 공장은 생산 능력을 1,400만 개 증대할 예정이며, ZC Rubber의 5G 대응 항저우 공장은 승용차용 레이디얼 타이어 생산량을 2,000만 개로 두 배로 늘릴 예정입니다. 이러한 전개는 지역 수요에 부응하고 수출 역량을 강화함으로써, 공기입 타이어 시장에서 아시아태평양의 입지를 공고히할 것입니다.

북미에서는 판매량 증가세가 둔화되고 있지만, 고급 전기차(EV)용 타이어의 채택이 확대됨에 따라 단가 상승이라는 혜택을 누리고 있습니다. 미국 타이어 제조업체 협회(USTMA)는 2025년 출하량을 3억 4,040만 개로 전망하고 있으며, 이는 판매량이 고작 0.9% 증가하는 수준에 그칠 것으로 보입니다. 그러나 가격 구조의 개선으로 인해 매출 증가가 예상됩니다. 굿이어는 로턴에서 3억 2,000만 달러 규모의 확장 프로젝트와 캐나다에서 5억 7,500만 캐나다 달러(4억 1,516만 달러) 규모의 현대화 프로젝트를 통해 센서 탑재형 저소음 전기차 타이어 생산에 주력하고 있습니다. 한편, 유럽은 비용 면에서 어려움을 겪고 있으며, 2024년에는 독일의 생산량이 4.3% 감소할 것으로 전망됩니다. 또한, 콘티넨탈은 비용이 많이 드는 생산 능력을 축소하기 위해 말레이시아의 알로스터 공장을 폐쇄했습니다.

남미와 중동 및 아프리카는 여전히 소규모 시장이지만, 전략적으로 중요한 위치를 차지하고 있습니다. Linglong의 브라질 합작 사업은 반덤핑 관세를 회피하며, 메르코수르(Mercosur) 회원국의 조립 제조업체에 타이어를 공급하고 있습니다. 중동에서는 사우디아라비아와 아랍에미리트(UAE)의 인프라 개발이 수요를 견인하고 있지만, 환율 변동이 투자 의욕을 위축시키고 있습니다. 아프리카에서는 교체용 타이어 판매의 최대 40%를 위조품이 차지하고 있어, 공기입 타이어 시장의 정식 제조업체들에게 과제가 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the pneumatic tire market size is projected to expand from USD 417.34 billion in 2025 and USD 437.04 billion in 2025 to USD 550.39 billion by 2030, registering a CAGR of 4.72% between 2025 to 2030.

This report is Segmented by Tire Type (Radial Tires and Bias Tires), Distribution Channel (OEM and Aftermarket), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two-Wheelers, and Off-The-Road Vehicles), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Pneumatic Tire Market Trends and Insights

Rising Demand for Fuel-Efficient and High-Performance Tires

Fleet operators are focusing on reducing rolling resistance to comply with the Corporate Average Fuel Economy (CAFE) standards, which will become stricter starting with model-year 2027. This has led to the use of silica-rich tread compounds and bio-based oils that lower hysteresis without affecting wet grip, as noted by the National Highway Traffic Safety Administration (NHTSA). Products such as Continental EcoContact and Michelin e.Primacy, which holds A-ratings for European Union (EU) fuel-efficiency labels, demonstrates that high performance can align with safety requirements. Additionally, the increased torque of electric vehicles (EVs) raises tire wear rates by approximately 20%, prompting original equipment manufacturers (OEMs) to require reinforced sidewalls and optimized tread patterns to extend tire service life. These advancements enable suppliers to maintain price premiums in the pneumatic tire market. Technological innovation continues to drive growth in high-performance tire segments, outpacing overall replacement market growth.

Expansion of E-Commerce and Logistics Fleets

The United States Postal Service (USPS) plans to deploy 106,000 next-generation delivery vehicles by 2028, with 66,000 of these being battery-electric vehicles. This shift highlights the increasing urban delivery mileage. Goodyear's USD 320 million upgrade to its Lawton facility aims to expand production capacity for low-noise tires with reinforced sidewalls, specifically designed for residential delivery routes. In markets like India and Indonesia, the rapid growth of online shopping is driving light-commercial fleets to transition from bias-ply to radial tires, which are better suited for managing heat during frequent stop-start cycles. As parcel volumes increase, fleet managers are adopting data-enabled tires that integrate with telematics systems, thereby increasing switching costs. These trends collectively contribute to incremental revenue growth in the pneumatic tire market.

Tighter Environmental Rules on Disposal and Micro-Plastics

Euro 7 regulations introduce stricter particulate limits, with further tightening expected by 2032. Additionally, 24 United States (U.S.) states have implemented Extended Producer Responsibility (EPR) laws, transferring disposal costs to manufacturers. The use of harder tread compounds, while addressing durability, can affect wet-grip performance, necessitating new investments in silica dispersion and polymer cross-linking technologies to maintain safety standards. According to the Pew Charitable Trusts, tire and brake wear is projected to account for 90% of road-transport particulates by 2050, leading to increased regulatory scrutiny. Compliance with these regulations is estimated to raise unit costs by 2%-4%, impacting price competitiveness, particularly for low-margin suppliers in the pneumatic tire market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Aftermarket Demand from Ageing Vehicle Parc

- Stringent Tire-Efficiency and Labeling Regulations

- Counterfeit and Low-Quality Tire Influx in Developing Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radial tires accounted for 77.12% of market value in 2025, driven by regulatory emphasis on fuel efficiency and high-speed safety. Bias tires are projected to grow at a compound annual growth rate (CAGR) of 5.15% through 2031, surpassing the overall pneumatic tire market CAGR. In India, with a two-wheeler base exceeding 220 million units, bias tires remain popular due to their puncture resistance and affordability, particularly among rural users. Similarly, in Sub-Saharan Africa, bias tires are preferred for light trucks and three-wheelers operating on unpaved roads. Radial tires continue to dominate revenue generation, especially in electric vehicles. Bridgestone's JPY 27 billion (USD 0.17 billion) investment in Japan has expanded capacity for high-rigidity radial tires designed for heavier electric vehicle (EV) battery packs.

Bias tire manufacturers are also modernizing. Companies like Zhongce Rubber and Triangle Tire are enhancing their engineering tire lines to cater to the mining and construction sectors, where radial advantages are less pronounced. Meanwhile, Continental's plant in Thailand focuses on motorcycle and EV radial tires, which improve ride quality and torque management. As manufacturers aim to balance performance and sustainability, they are diversifying their product portfolios to address varied use cases across the pneumatic tire market.

Geography Analysis

Asia-Pacific accounted for 44.15% of the market value in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 5.49% through 2031. This growth is supported by China's annual output of 840 million units, India's transition to radial tires, and the expansion of commercial vehicle markets in ASEAN (Association of Southeast Asian Nations) countries. Linglong's USD 750 million Anhui plant adds 14 million units to its capacity, while ZC Rubber's 5G-enabled Hangzhou facility doubles its output to 20 million passenger radials. These developments address regional demand and enhance export capabilities, reinforcing Asia-Pacific's role in the pneumatic tire market.

North America shows slower volume growth but benefits from higher per-unit values due to the increasing adoption of premium electric vehicle (EV) tires. The United States Tire Manufacturers Association (USTMA) projects 340.4 million shipments in 2025, reflecting a modest 0.9% volume growth. However, an improved price mix is expected to drive revenue. Goodyear's USD 320 million expansion in Lawton and a CAD 575 million (USD 415.16 million) modernization project in Canada focus on producing sensor-ready, low-noise EV tires. Meanwhile, Europe faces cost challenges, with German production declining by 4.3% in 2024. Additionally, Continental closed its Malaysian Alor Setar plant to reduce high-cost capacity.

South America and the Middle East & Africa remain smaller markets but hold strategic importance. Linglong's joint venture in Brazil circumvents anti-dumping tariffs and supplies tires to Mercosur assemblers. In the Middle East, infrastructure development in Saudi Arabia and the United Arab Emirates (UAE) drives demand, although currency volatility dampens investment enthusiasm. In Africa, counterfeit products account for up to 40% of replacement tire sales, posing challenges for legitimate players in the pneumatic tire market.

- Apollo Tyres Ltd

- Bridgestone

- Continental AG

- Giti Tire

- Hankook Tire & Technology

- Kumho Tire Co., Inc.

- Linglong Tire

- Maxxis International

- Michelin

- MRF Tyres

- Nokian Tyres plc

- Pirelli & C. S.p.A.

- Sailun Group Co., Ltd

- Sumitomo Rubber Industries, Ltd

- The Goodyear Tire & Rubber Company

- The Yokohama Rubber Co., Ltd

- Toyo Tire Corporation

- Zhongce Rubber Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Fuel-Efficient and High-Performance Tires

- 4.2.2 Expansion of E-Commerce and Logistics Fleets

- 4.2.3 Accelerated Aftermarket Demand from Ageing Vehicle Parc

- 4.2.4 Stringent Tire-Efficiency and Labelling Regulations

- 4.2.5 Integration of Smart-Tire Sensors for Predictive Maintenance

- 4.3 Market Restraints

- 4.3.1 Tighter Environmental Rules on Disposal and Micro-Plastics

- 4.3.2 Counterfeit and Low-Quality Tire Influx in Developing Markets

- 4.3.3 Emergence of Airless and Solid Tires in Niche Uses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Tire Type

- 5.1.1 Radial Tires

- 5.1.2 Bias Tires

- 5.2 By Distribution Channel

- 5.2.1 OEM

- 5.2.2 Aftermarket

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Two-Wheelers

- 5.3.5 Off-the-Road Vehicles

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Australia and New Zealand

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Egypt

- 5.4.5.6 Nigeria

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Apollo Tyres Ltd

- 6.4.2 Bridgestone

- 6.4.3 Continental AG

- 6.4.4 Giti Tire

- 6.4.5 Hankook Tire & Technology

- 6.4.6 Kumho Tire Co., Inc.

- 6.4.7 Linglong Tire

- 6.4.8 Maxxis International

- 6.4.9 Michelin

- 6.4.10 MRF Tyres

- 6.4.11 Nokian Tyres plc

- 6.4.12 Pirelli & C. S.p.A.

- 6.4.13 Sailun Group Co., Ltd

- 6.4.14 Sumitomo Rubber Industries, Ltd

- 6.4.15 The Goodyear Tire & Rubber Company

- 6.4.16 The Yokohama Rubber Co., Ltd

- 6.4.17 Toyo Tire Corporation

- 6.4.18 Zhongce Rubber Group Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment