|

시장보고서

상품코드

2062385

블로우 성형 용기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Blow Molded Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

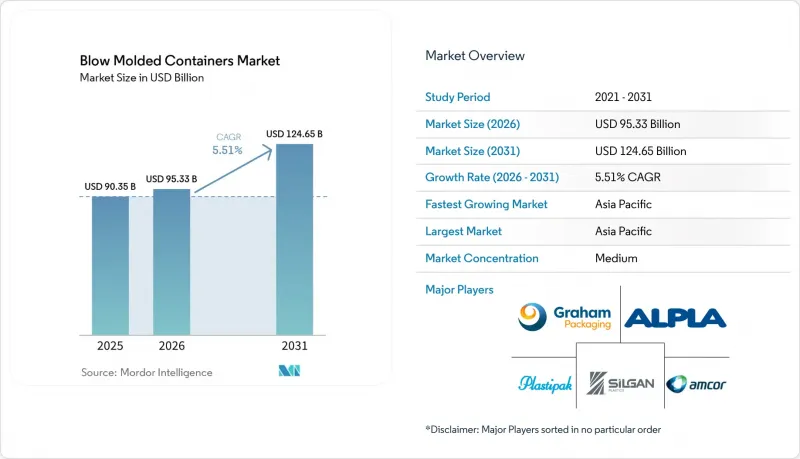

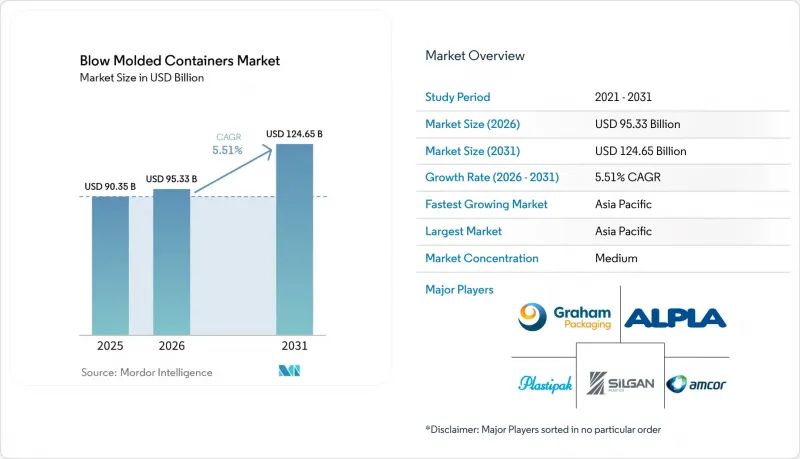

Mordor Intelligence에 의하면, 블로우 성형 용기 시장 규모는 2025년 903억 5,000만 달러, 2026년 953억 3,000만 달러에서 2031년까지 1,246억 5,000만 달러로 확대되어 2026년부터 2031년까지 사이에 CAGR 5.51%를 나타낼 것으로 예측됩니다.

본 보고서는 소재(고밀도 폴리에틸렌(HDPE) 등), 용기 유형(병, 항아리·용기 등), 기술(압출 블로우 성형(EBM) 등), 최종 사용자 산업(식품 및 음료 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 블로우 성형 용기 시장 동향 및 분석

1회분 및 휴대용 음료 시장의 성장

음료 및 의약품 분야 모두에서 1회분(단일 용량) 형태의 SKU가 확대되고 있으며, 500ml 미만의 경량 폴리에틸렌 테레프탈레이트(PET) 병이 선호되고 있습니다. 모듈식 금형 시스템을 도입한 제조업체들은 재고 관리상의 문제 없이 SKU의 복잡화에 대응하고 있습니다. 예를 들어, FlexBlow 플랫폼을 사용하면 5분 이내에 금형 교체가 가능해져 업무 효율이 향상되고 있습니다. 캡 디자인도 진화하고 있으며, 플립탑 방식의 스포츠 캡이나 내장형 빨대 등의 개발을 통해 가치의 초점이 병 본체에서 목 부분 마감으로 이동하면서 기능성과 편의성이 향상되고 있습니다.

전자상거래 택배 물류의 확대

자동화된 물류 센터에서는 낙하 높이와 진동 강도가 높아짐에 따라, 리브가 있는 측면 벽이나 보강된 바닥이 채택되고 있습니다. 이러한 설계 변경으로 인해 수지 사용량은 8-12% 증가하지만, 운송 중 파손으로 인한 클레임을 방지하고 제품의 무결성을 확보하는 데 도움이 됩니다. 또한, 소포 내 빈 공간을 제재 대상으로 삼는 유럽연합(EU)의 규제로 인해 각 브랜드는 배송용 골판지 상자의 사용을 효율적으로 최적화할 수 있는 적절한 크기와 형태를 채택해야 하는 상황에 놓여 있으며, 이를 통해 배송 비용 절감과 지속가능성 향상을 도모하고 있습니다.

석유화학 원료 가격의 변동

2026년 초, 폴리에틸렌 가격은 전년 동기 대비 15% 하락했으나, 월간 18-22%의 변동세가 이어지면서 고정 가격 판매 계약 하에 사업을 영위하는 가공업체들에 지속적인 영향을 미치고 있습니다. 재생 폴리에틸렌 테레프탈레이트(rPET) 플레이크의 가격은 버진 수지에 비해 25-35% 더 비쌉니다. 이는 유럽에서 회수된 폴리에틸렌 테레프탈레이트(PET) 중 식품 등급 용도에 적합한 제품이 고작 58%에 불과하기 때문입니다. 이러한 가격 차이는 식품 등급 rPET공급이 제한적이기 때문이며, 재활용 공정의 비효율성이 그 공급을 더욱 제약하고 있습니다.

부문별 분석

고밀도 폴리에틸렌(HDPE)은 우유, 세제, 산업용 화학약품 포장에 필수적인 내화학성과 내충격성 덕분에 2025년 매출의 35.11%를 차지했습니다. 바이오 및 재활용 플라스틱 관련 블로우 성형 용기 시장은 투자자들의 환경·사회·지배구조(ESG) 이니셔티브에 힘입어 2031년까지 연평균 성장률(CAGR) 5.64%로 성장할 것으로 전망됩니다. 토탈에너지스 코르비온의 폴리젖산(PLA) ‘루미니’는 병입 식수 시범 프로젝트를 지원하기 위해 2025년에 7만 5,000톤의 생산 능력에 도달했습니다. 한편, 폴리에틸렌 테레프탈레이트(PET)는 무게 15g의 500ml 병을 사용한 탄산음료 포장 시장에서 여전히 지배적인 위치를 차지하고 있지만, 시장의 포화와 재충전 가능한 유리 용기 프로그램의 부상으로 인해 추가적인 성장은 제한되고 있습니다. 재활용 소재가 함유된 폴리올레핀은 밸류체인에서 지속적으로 발전하고 있으며, INEOS사의 rPP1025C는 70%의 재활용 소재를 함유하면서도 화장품 등급 용도에 필요한 강성 요건을 충족합니다.

폴리염화비닐(PVC)은 프탈레이트에 대한 우려로 인해 서유럽 시장에서 점유율을 잃어, 한 자릿수 수준까지 떨어졌습니다. 폴리하이드록시알카노에이트(PHA)는 해양 생분해성 잠재력을 지니고 있음에도 불구하고, 생산 능력이 5,000톤 미만에 그치고 있어 여전히 제약을 받고 있습니다. 압출 블로우 성형(EBM) 분야에서 HDPE가 확고히 자리 잡은 것은 급속한 대체 현상에 대한 일정한 완충 역할을 하고 있지만, 확대 생산자 책임(EPR) 요금이 더욱 엄격해짐에 따라 HDPE의 경쟁력은 재생 HDPE(rHDPE) 블렌드나 색상별 분리 수거 시스템의 발전에 점점 더 의존하게 될 것입니다.

2025년 매출액 중 병이 64.12%를 차지했으나, 손잡이가 달린 주전자, 2실 디스펜서, 에어리스 펌프 등 특수 형태의 제품은 5.88%라는 더 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 예측됩니다. 그라이프사의 2실식 캐니스터는 사용 시까지 반응성 접착제를 분리해 두어 보관 기간을 4배로 연장합니다. 에어리스 폴리에틸렌 테레프탈레이트(PET) 용기는 산소 유입을 차단하여 비타민 C 세럼의 효능을 유지함으로써, 스킨케어 시장에서 프리미엄 가격 책정이 가능하도록 합니다. Graham Packaging사의 AccuStrength 소프트웨어는 손잡이가 달린 용기의 무게를 11-15% 줄여, 북미 전역에서 연간 8,000-1만 톤의 HDPE를 절감하고 있습니다.

용기나 주전자는 사출 성형 폴리프로필렌(PP)에서 압출 블로우 성형 HDPE로 전환되고 있으며, 이를 통해 금형 교체가 신속해지고 있습니다. 한편, 드럼통이나 중간 벌크 컨테이너(IBC)는 유엔(UN) 인증 규격으로 통일되고 있습니다. 재활용이 가능한 병이 널리 보급되는 가운데, 디스펜서 구조와 인체공학에 기반한 디자인 혁신이 브랜드의 이익률을 유지하기 위한 중요한 차별화 요인으로 부상하고 있습니다.

지역별 분석

아시아태평양은 2025년 예상 매출의 41.18%를 차지하며, 연평균 성장률(CAGR) 6.22%로 성장하고 있습니다. 중국 광둥성과 저장성에 위치한 통합 석유화학 클러스터는 원자재 흐름의 효율성을 높이고 있습니다. 한편, 인도의 ‘의약품 및 화장품법’에 따르면 1만 곳의 의약품 제조 공장에서 부정 개봉 방지 용기 사용이 의무화되어 있습니다.

북미에서는 온사이트 블로우 성형 도입에 더해, 2020년 이후 140억 달러 규모의 플라스틱 산업 국내 복귀 투자가 이루어지고 있는 점이 호재로 작용하고 있습니다. Logoplaste사는 62개의 현장 공장을 운영하고 있으며, 이를 통해 고객의 이산화탄소(CO2) 배출량을 연간 1만 2,000톤 줄이고 있습니다. 유럽에서는 수지 가격 급등 및 에너지 가격 변동과 같은 과제에 직면해 있지만, 포장 및 포장 폐기물 규정(PPWR)의 재생 소재 함유율 요건을 충족하기 위해 재생 폴리에틸렌 테레프탈레이트(rPET) 생산 라인에 대한 투자를 추진하고 있습니다. 중동 및 아프리카에서는 이집트에 위치한 아셉트(Acsept)사의 1억 2,600만 달러 규모 무균 생산 라인을 포함한 신규 설비 도입을 통해, 해당 지역이 독립국가연합(CIS) 및 사하라 이남 시장을 대상으로 한 잠재적인 수출 거점으로서의 입지를 확고히 하고 있습니다.

독일과 스칸디나비아 국가들의 보증금 반환 제도는 폴리에틸렌 테레프탈레이트(PET) 회수를 촉진하고 있지만, rPET 공급 부족량은 연간 70만 톤에 달하고, 튀르키예와 사우디아라비아로부터의 수입이 필요하게 되었습니다. 이러한 원자재 수급 동향은 아시아태평양의 비용 경쟁력을 강화하여, 블로우 성형 용기 시장에서 해당 지역의 높은 점유율을 유지하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the blow molded containers market size is projected to expand from USD 90.35 billion in 2025 and USD 95.33 billion in 2026 to USD 124.65 billion by 2031, registering a CAGR of 5.51% between 2026 to 2031.

This report is Segmented by Material (High-Density Polyethylene (HDPE) and More), Container Type (Bottles, Jars and Pots, and More), Technology (Extrusion Blow Molding (EBM) and More), End-User Industry (Food and Beverages and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Blow Molded Containers Market Trends and Insights

Growth in Single-Serve and On-the-Go Beverages

Unit-dose formats are expanding in both beverage and pharmaceutical stock-keeping units (SKUs), with a preference for lightweight polyethylene terephthalate (PET) bottles under 500 milliliters. Manufacturers using modular tooling systems are addressing the increasing complexity of SKUs without incurring inventory challenges. For example, FlexBlow platforms enable mold changes in less than five minutes, improving operational efficiency. Closure designs are also evolving, with developments such as flip-top sports caps and built-in straws shifting value emphasis from bottle bodies to neck finishes, enhancing functionality and convenience.

E-commerce Home-Delivery Logistics Expansion

Automated fulfillment centers are introducing higher drop heights and vibration profiles, leading to the adoption of ribbed sidewalls and reinforced bases. These design changes increase resin usage by 8-12% but help prevent damage claims, ensuring product integrity during transit. Additionally, European Union (EU) regulations penalizing empty space within parcels are driving brands to adopt right-sized geometries that optimize the use of shipping cartons efficiently, reducing shipping costs and improving sustainability.

Petrochemical Feedstock Price Volatility

Polyethylene prices decreased by 15% year-on-year in early 2026; however, monthly fluctuations of 18-22% continue to impact converters operating under fixed-price sales agreements. Recycled Polyethylene Terephthalate (rPET) flake is priced at a 25-35% premium over virgin resin, as only 58% of collected Polyethylene Terephthalate (PET) in Europe qualifies for food-grade applications. This disparity in pricing is driven by the limited availability of food-grade rPET, which is further constrained by inefficiencies in the recycling process.

Other drivers and restraints analyzed in the detailed report include:

- Brand Shift to Mono-Material Designs for Recyclability

- Plasma-Coated PET Enabling Glass-Like Barrier

- European Union PPWR 30% Recycled-Content Mandate

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-density polyethylene (HDPE) accounted for 35.11% of 2025 revenue, driven by its chemical resistance and impact durability, which are essential for packaging milk, detergents, and industrial chemicals. The blow-molded containers market linked to bio-based and recycled plastics is projected to grow at a compound annual growth rate (CAGR) of 5.64% through 2031, supported by environmental, social, and governance (ESG) initiatives from investors. TotalEnergies Corbion's Luminy polylactic acid (PLA) reached a production capacity of 75,000 tons in 2025 to support bottled water pilot projects. While polyethylene terephthalate (PET) continues to dominate carbonated soft drink packaging with lightweight 15-gram 500-milliliter bottles, market saturation and the rise of refillable glass programs limit further growth. Recycled-content polyolefins are advancing in the value chain, with INEOS's rPP1025C containing 70% recyclate while meeting the stiffness requirements for cosmetics-grade applications.

Polyvinyl chloride (PVC) is losing market share in Western Europe, dropping to single-digit levels due to concerns over phthalates. Polyhydroxyalkanoates (PHA), despite their marine biodegradability potential, remain constrained by production capacities below 5,000 tons. HDPE's established presence in extrusion blow molding (EBM) provides some insulation against rapid displacement, but the competitiveness of HDPE will increasingly depend on recycled HDPE (rHDPE) blends and advancements in color-sorted separation systems as extended producer responsibility (EPR) fees become more stringent.

Bottles accounted for 64.12% of 2025 revenue, but specialty shapes, such as handleware jugs, dual-chamber dispensers, and airless pumps, are expected to grow at a faster CAGR of 5.88%. Greif's dual-compartment canisters, which separate reactive adhesives until use, extend shelf life by four times. Airless polyethylene terephthalate (PET) containers preserve the potency of vitamin-C serums by preventing oxygen ingress, enabling premium pricing in the skincare market. Graham Packaging's AccuStrength software reduces handleware gram weights by 11-15%, saving 8,000-10,000 tons of HDPE annually across North America.

Jars and pots are transitioning from injection-molded polypropylene (PP) to extrusion-blown HDPE, which allows for faster tool changes. Meanwhile, drums and intermediate bulk containers (IBCs) are consolidating around United Nations (UN)-certified formats. As bottles increasingly become recyclable commodities, innovations in dispensing mechanisms and ergonomic designs are emerging as key differentiators to maintain brand margins.

Geography Analysis

Asia-Pacific accounted for 41.18% of the projected 2025 revenue and is growing at a compound annual growth rate (CAGR) of 6.22%. China's integrated petrochemical clusters in Guangdong and Zhejiang improve raw material flow efficiency, while India's Drugs and Cosmetics Act mandates tamper-evident bottles across 10,000 drug manufacturing plants.

North America benefits from the adoption of on-site blow molding and USD 14 billion in reshored plastics investments since 2020. Logoplaste operates 62 embedded plants, reducing clients' carbon dioxide (CO2) emissions by 12,000 tons annually. Europe faces challenges such as resin premiums and energy price volatility, but is investing in recycled polyethylene terephthalate (rPET) production lines to meet Packaging and Packaging Waste Regulation (PPWR) recycled-content requirements. In the Middle East and Africa, new installations, including Asepto's USD 126 million aseptic line in Egypt, position the region as a potential export hub for the Commonwealth of Independent States (CIS) and Sub-Saharan markets.

Deposit-return schemes in Germany and Scandinavia support polyethylene terephthalate (PET) collection; however, rPET shortfalls persist at 0.7 million tons annually, necessitating imports from Turkey and Saudi Arabia. These feedstock dynamics reinforce Asia-Pacific's cost advantage and sustain its significant share in the blow molded containers market.

- Alpha Packaging

- ALPLA

- Amcor plc

- APEX Plastics

- Comar

- Graham Packaging

- Greif

- Jokey SE

- Logoplaste

- Pharmapack Co., Ltd.

- Plastipak Holdings, Inc.

- Pretium Packaging

- RESILUX NV

- Retal Industries LTD

- Sidel

- Silgan Plastics

- SRPCO Packaging

- Takween Advanced Industries

- Time Technoplast Ltd.

- Zhejiang Zhink New Materials Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in single-serve and on-the-go beverages

- 4.2.2 E-commerce home-delivery logistics expansion

- 4.2.3 Brand shift to mono-material designs for recyclability

- 4.2.4 Plasma-coated PET enabling glass-like barrier

- 4.2.5 On-site, just-in-time blow-molding at fillers

- 4.3 Market Restraints

- 4.3.1 Petrochemical feedstock price volatility

- 4.3.2 European Union PPWR 30 % recycled-content mandate

- 4.3.3 Brand pilots of paper-based rigid packs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 High-Density Polyethylene (HDPE)

- 5.1.2 Polyethylene Terephthalate (PET)

- 5.1.3 Low-Density/Linear-Low-Density Polyethylene (LD/LLDPE)

- 5.1.4 Polypropylene (PP)

- 5.1.5 Polyvinyl Chloride (PVC)

- 5.1.6 Bio-based and Recycled Plastics (rPET, rHDPE, PLA, PHA)

- 5.2 By Container Type

- 5.2.1 Bottles

- 5.2.2 Jars and Pots

- 5.2.3 Jerry Cans and F-style Containers

- 5.2.4 Drums and Intermediate Bulk Containers (IBCs)

- 5.2.5 Specialty Shapes (Handleware, Dual-chamber, Etc.)

- 5.3 By Technology

- 5.3.1 Extrusion Blow Molding (EBM)

- 5.3.2 Injection Blow Molding (IBM)

- 5.3.3 Stretch Blow Molding (SBM)

- 5.4 By End-User Industry

- 5.4.1 Food and Beverages

- 5.4.2 Personal Care and Cosmetics

- 5.4.3 Pharmaceutical and Healthcare

- 5.4.4 Home Care and Household Chemicals

- 5.4.5 Industrial Chemicals and Lubricants

- 5.4.6 Automotive Fluids and Coolants

- 5.4.7 Agriculture and Horticulture

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Alpha Packaging

- 6.4.2 ALPLA

- 6.4.3 Amcor plc

- 6.4.4 APEX Plastics

- 6.4.5 Comar

- 6.4.6 Graham Packaging

- 6.4.7 Greif

- 6.4.8 Jokey SE

- 6.4.9 Logoplaste

- 6.4.10 Pharmapack Co., Ltd.

- 6.4.11 Plastipak Holdings, Inc.

- 6.4.12 Pretium Packaging

- 6.4.13 RESILUX NV

- 6.4.14 Retal Industries LTD

- 6.4.15 Sidel

- 6.4.16 Silgan Plastics

- 6.4.17 SRPCO Packaging

- 6.4.18 Takween Advanced Industries

- 6.4.19 Time Technoplast Ltd.

- 6.4.20 Zhejiang Zhink New Materials Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment