|

시장보고서

상품코드

2062397

나노클레이 보강재 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Nanoclay Reinforcement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

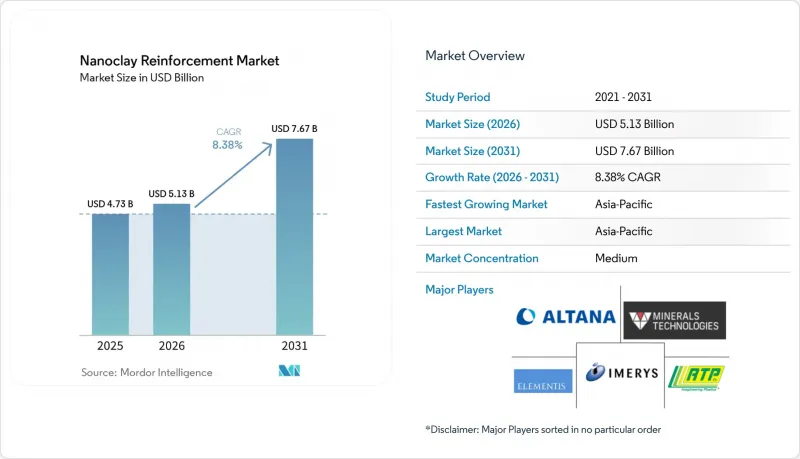

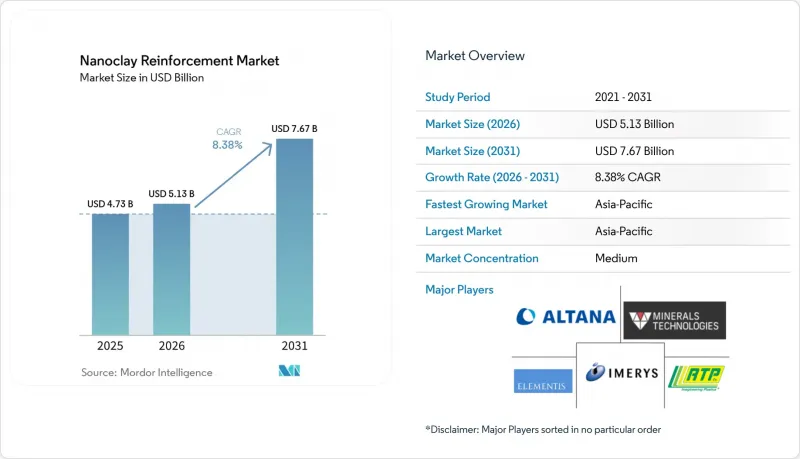

Mordor Intelligence에 의하면, 나노클레이 보강재 시장 규모는 2025년에 47억 3,000만 달러로 평가되었고, 2026년 51억 3,000만 달러로 추정되고, 2031년까지 76억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.38%를 나타낼 전망입니다.

본 보고서는 유형별(몬모릴로나이트, 카올린나이트, 스메크타이트, 할로이사이트, 일라이트, 헥트라이트), 형태별(분말, 마스터배치, 분산액), 보강 매트릭스별(열가소성 수지, 열경화성 수지, 엘라스토머, 바이오폴리머, 기타), 최종 사용자별(포장, 자동차, 건설, 전자, 헬스케어 등), 지역별(아시아태평양, 북미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준입니다.

세의계 나노클레이 보강재 시장 동향 및 인사이트

고성능이자 경량인 복합재료에 대한 수요의 급증

항공우주 분야의 OEM 제조업체들은 현재 2차 구조재로 몬모릴로나이트 강화 에폭시 프리프레그를 채택하고 있습니다. 이러한 경량화 방안을 통해 항공기 1대당 수명 주기 연료비가 대폭 절감됩니다. 자동차 분야에서는 1차 공급업체들이 배터리 하우징에 이와 유사한 접근 방식을 적용하고 있습니다. 이러한 용도에서 나노클레이 개질 폴리아미드 6은 화염 전파 속도를 임계치 이하로 낮출 뿐만 아니라, 케이스의 무게도 줄여줍니다. 풍력 터빈 블레이드 제조업체는 헥트라이트계 티크소트로픽제를 사용하고 있습니다. 이로 인해 폐기물이 줄어들고 경화 주기가 단축되므로, 프로젝트 리드타임이 단축됩니다. 이러한 발전으로 인해, 고객이 공급업체를 변경할 때 발생하는 비용은 높아집니다. 각 용도별로 사용하는 수지에 맞추어 조정된 독자적인 표면 개질 레시피가 필요하며, 이를 통해 기존 공급업체들은 원자재 가격 변동으로부터 보호받고 있습니다. 그 결과, 원유 가격에 연동되는 폴리머 가격이 하락세를 보이고 있음에도 불구하고, 나노클레이 보강재 시장에서는 신규 수주가 급증하고 있습니다.

자동차 및 항공우주 분야에서의 나노복합재 활용 확대

배터리 팩, 실내 공기 관리 부품, 나셀 패널에서는 나노클레이와 인의 시너지 효과가 점점 더 많이 활용되고 있습니다. 이러한 조합을 통해 최소한의 첨가량으로도 높은 한계 산소 지수 값을 실현하고 있습니다. 탄소섬유 제조업체는 현재 유기 클레이로 전처리가 된 원사를 공급하고 있으며, 이를 통해 프리프레그 제조업체의 공정이 합리화되고, 로트 간 품질이 균일하게 유지됩니다. 항공우주 분야에서는 판상 점토로 강화된 비스마레이미드계 소재에서 흡습성이 감소한 것으로 확인되었습니다. 이러한 발전 덕분에 검사 간격을 연장할 수 있게 되었습니다. 이러한 발전은 컴파운더에 대한 높은 수요를 유지할 뿐만 아니라, 시장이 나노클레이 보강 제품의 산발적인 도입에서 체계적인 통합으로 전환되고 있다는 중요한 변화를 여실히 보여주고 있습니다.

높은 가공 비용과 분산의 복잡성

가공업체들은 일관된 박리 성능을 보장하기 위해 맞춤형 사양의 2축 스크류 압출기를 선택하는 경우가 많습니다. 그러나 분산이 불충분하면 큰 응집 덩어리가 생겨, 완벽함을 추구하는 업계에서 인장 강도가 저하되고 불량률이 높아질 우려가 있습니다. 나노 클레이가 함유된 마스터배치는 이 문제를 해결할 수 있지만, 일반적인 유기 클레이 분말보다 가격이 비쌉니다. 또한, 독자적인 계면활성제 패키지는 혼합 과정을 간소화하지만, 가공업체를 독점 계약에 묶어두어 경쟁 입찰을 제한하는 결과도 초래합니다. 이러한 요인들이, 특히 소규모 컴파운더의 경우, 나노클레이 보강재 시장의 성장을 저해해 왔습니다.

부문별 분석

2025년, 몬모릴로나이트는 나노클레이 보강재 시장에서 40.21%라는 압도적인 점유율을 차지했으며, 주로 대중 시장인 자동차 및 포장 부문을 뒷받침했습니다. 한편, 할로이사이트는 시장 점유율은 작지만, 2026-2031년 예측 기간 동안 연평균 성장률(CAGR) 8.77%라는 놀라운 성장을 기록했습니다. 이러한 성장은 할로이사이트의 10:1에서 30:1에 이르는 유리한 종횡비에 기인하며, 이를 통해 10-15%의 약제 부하가 가능해져 혈소판형 점토를 크게 능가하는 성능을 발휘합니다.

와이오밍주의 벤토나이트 광산과 튀르키예의 헥트라이트 광산은 몬모릴로나이트의 안정적인 공급을 보장하며, 벌크 시장에서 이 광물의 우위를 공고히 하고 있습니다. 반면, 병원에서는 수 주간에 걸쳐 은 이온을 서서히 방출하는 의약품 등급의 할로사이트 코팅에 훨씬 더 많은 예산을 할당하고 있으며, 나노클레이 보강재 시장에서 프리미엄 틈새 시장을 구축하고 있습니다.

2025년, 나노클레이 보강재 시장에서 분말이 47.48%라는 압도적인 점유율을 차지했습니다. 한편, 마스터배치의 매출액은 2026-2031년 예측 기간 동안 연평균 성장률(CAGR) 8.92%로 증가할 전망입니다. 이러한 성장은 주로 가공업체들이 기존의 2축 스크류에 대한 설비 투자를 피하고, 바로 사용할 수 있는 분산액을 선호하는 경향에 기인합니다.

RTP의 유기 점토 마스터배치는 정확한 희석 비율로 도포될 경우, 폴리에틸렌 필름의 산소 차단성을 대폭 향상시킵니다. 이러한 발전은 전환 시간을 최소화하여 가동을 최적화할 뿐만 아니라, RTP 제품의 뛰어난 효율성을 더욱 돋보이게 합니다. 분산액이나 용액 형태는 주로 용매 처리에 따른 높은 비용이라는 과제에 직면해 있지만, 특히 설비의 전단력이 제한적인 상황에서 스프레이 도포 코팅에 있어 매우 중요한 역할을 수행하고 있습니다.

지역별 분석

2025년, 아시아태평양은 37.04%라는 압도적인 점유율로 수익 시장을 독점했으며, 2026-2031년 예측 기간 동안 연평균 성장률(CAGR) 9.18%를 기록하며 견조한 성장세를 보였습니다. 중국이 주도하여 GB 38031-2020 표준을 준수하는 나노클레이 복합 배터리 팩을 탑재한 수백만 대의 전기차를 시장에 출시했습니다. 인도에서는 식품안전 당국의 수입 제한 강화가 성장의 계기가 되어, 연포장재에 사용되는 혈소판형 점토의 사용량이 크게 증가했습니다. 일본에서는 고순도의 의료용 등급을 생산하기 위해 할로사이트 가공을 확대한 반면, 한국의 배터리 제조업체들은 정밀 충전 공정을 거친 폴리아미드 하우징을 활용함으로써 눈부신 경량화를 실현했습니다.

북미에서는 와이오밍주가 중심적인 역할을 수행하며 큰 시장 점유율을 확보했습니다. 와이오밍주가 연간 수백만 톤 규모로 공급하는 벤토나이트는 국내 컴파운더들에게 안정적인 원료 공급원이 되었습니다. 항공우주 업계의 주요 기업들은 NASA의 연료 효율 목표에 따라 나노 클레이 프리프레그를 엔진 나셀에 적용했습니다. 2025년, 니어쇼어링의 혜택을 받은 멕시코의 자동차 산업 거점에서는 엔진룸 내부 부품 수요가 급증했습니다.

유럽에서는 EFSA로 인한 지연을 극복하고, 큰 시장 점유율을 확보하며 꾸준한 성장을 이룩했습니다. 2024년, 독일의 각 OEM 기업들은 자사 플랫폼 전반에 UL 94 V-0 규격의 나노클레이 폴리아미드 재질 케이스를 도입했습니다. 프랑스에서는 혈소판 배리어 병을 활용한 혁신적인 기술을 통해 와인의 유통기한을 현저히 연장하는 데 성공했습니다. 스페인에서 나노클레이 멀치를 도입한 결과, 제초제 유출이 대폭 감소했습니다. 한편, 영국에서 섬유 시멘트 재질의 외장재를 시범 도입한 사례는 소규모에 그쳤으나, 글렌펠 화재 이후 강화된 안전 규제로 인해 주목을 받게 되었습니다.

남미는 중동 및 아프리카와 마찬가지로 시장 점유율은 비교적 낮았으나, 브라질의 석유화학용 라이너와 사우디아라비아의 실란트는 안정적인 판매량을 확보했으며, 남아프리카의 광업용 슬러리 라인에서는 마모가 현저히 감소했습니다. 시장 점유율은 다소 낮았지만, 이들 지역은 꾸준히 수주 수요를 충족시켜 2026-2031년 예측 기간 동안 나노클레이 보강재 시장의 전반적인 성장에 기여했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the nanoclay reinforcement market size was valued at USD 4.73 billion in 2025 and is estimated to grow from USD 5.13 billion in 2026 to reach USD 7.67 billion by 2031, at a CAGR of 8.38% during the forecast period (2026-2031).

This report is Segmented by Type (Montmorillonite, Kaolinite, Smectite, Halloysite, Illite, and Hectorite), Form (Powder, Masterbatch, and Dispersion), Matrix (Thermoplastics, Thermosets, Elastomers, Biopolymers, and Others), End-User (Packaging, Automotive, Construction, Electronics, Healthcare, and More), and Geography (Asia-Pacific, North America, and More). Market Forecasts in Value (USD).

Global Nanoclay Reinforcement Market Trends and Insights

Rapid Demand for High-Performance and Lightweight Composites

Aerospace original-equipment makers are now choosing montmorillonite-reinforced epoxy prepregs for secondary structures. This weight-reduction choice leads to significant lifetime fuel savings per aircraft. In the automotive sector, tier-1 suppliers are applying the same rationale to battery housings. In this application, nanoclay-modified polyamide 6 not only reduces flame-spread rates to below a critical threshold but also decreases the enclosure's mass. Wind-turbine blade manufacturers are adopting hectorite-based thixotropes, which cut down on scrap and speed up cure cycles, thereby shortening project lead times. These advancements make it costlier for customers to switch suppliers. Each application demands unique surface-modification recipes tailored to its resin, granting established vendors protection against commodity price swings. As a result, the nanoclay reinforcement market is witnessing a surge in new orders, even as crude-oil-linked polymer prices see a downturn.

Growing Nanocomposite Use in Automotive and Aerospace

Battery packs, cabin air-management components, and nacelle panels are increasingly leveraging a synergy of nanoclay and phosphorus. This combination achieves elevated limiting-oxygen-index values with minimal loading. Carbon-fiber manufacturers are now providing tows pre-treated with organoclay, which streamlines the process for prepreggers and ensures consistent quality across batches. In the aerospace sector, bismaleimide systems, now enhanced with platelet clays, have seen a reduction in moisture absorption. This advancement extends inspection intervals. Collectively, these advancements not only maintain a high demand for compounders but also highlight a significant shift - the market is moving from sporadic to systematic integration of nanoclay reinforcement products.

High Processing Cost and Dispersion Complexity

Processors frequently opt for twin-screw extruders with tailored configurations to ensure consistent exfoliation. Yet, inadequate dispersion can create sizable agglomerates, diminishing tensile strength and elevating scrap rates in industries aiming for perfection. Although a nanoclay-infused masterbatch can remedy this challenge, it commands a higher price than the standard organoclay powder. Moreover, while proprietary surfactant packages simplify mixing, they also tether processors to exclusive contracts, limiting competitive bidding. These factors have hindered the expansion of the nanoclay reinforcement market, especially for smaller compounders.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Barrier-Enhanced Sustainable Packaging

- Cost-Effective Intercalation and Exfoliation Breakthroughs

- EHS and Regulatory Uncertainty for Food-Contact Nanoclays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, montmorillonite dominated the nanoclay reinforcement market with a commanding 40.21% share, primarily supporting the mass-market automotive and packaging sectors. Meanwhile, halloysite, although holding a smaller share, experienced significant growth with an 8.77% CAGR during the forecast period of 2026-2031. This growth is attributed to halloysite's advantageous aspect ratio of 10:1 to 30:1, enabling a drug payload of 10 to 15 percent, which significantly outperforms platelet clays.

Wyoming's bentonite and Turkish hectorite mines ensure a steady supply of montmorillonite, reinforcing its dominance in the bulk market. In contrast, hospitals allocate significantly higher budgets for pharmaceutical-grade halloysite coatings, which provide a gradual release of silver ions over weeks, establishing a premium niche in the nanoclay reinforcement market.

In 2025, powder held a dominant 47.48% share of the nanoclay reinforcement market. Meanwhile, revenues from masterbatches have been climbing at a CAGR of 8.92% during the forecast period of 2026-2031. This growth is primarily driven by the processors' preference for ready dispersions, steering away from conventional twin-screw capital investments.

RTP's organoclay masterbatch, when applied at a precise let-down ratio, significantly bolsters oxygen barriers in polyethylene films. This advancement not only optimizes operations by minimizing changeover durations but also highlights the superior efficiency of RTP's product. Although dispersion and solution formats face challenges, mainly due to the elevated costs tied to solvent handling, they play pivotal roles in spray-applied coatings, particularly in scenarios with limited equipment shear.

Geography Analysis

In 2025, the Asia-Pacific region dominated the revenue landscape with a commanding 37.04% share and a robust growth trajectory, boasting a 9.18% CAGR during the forecast period of 2026-2031. China led the charge, rolling out millions of electric vehicles, each outfitted with GB 38031-2020 compliant nanoclay composite battery packs. In India, the food-safety agency's tightening of migration limits catalyzed growth, resulting in a significant uptick in the use of platelet clays for flexible packaging. Japan ramped up halloysite processing to produce high-purity medical grades, while South Korean battery manufacturers, leveraging polyamide housings with precise loading, achieved impressive weight reductions.

North America, with Wyoming as a pivotal player, secured a substantial market share. Wyoming's annual supply of millions of tons of bentonite ensured a steady feedstock for domestic compounders. Aerospace leaders, aligning with NASA's fuel efficiency goals, integrated nanoclay prepregs into nacelles. In 2025, Mexico's auto hubs, benefiting from nearshoring, experienced a surge in demand for under-hood parts.

Europe, despite navigating delays from EFSA, carved out a significant market share and experienced steady growth. In 2024, German OEMs rolled out UL 94 V-0 nanoclay polyamide enclosures across their platforms. French innovations, harnessing platelet-barrier bottles, achieved a remarkable extension of wine shelf life. Spain's adoption of nanoclay mulches led to a significant drop in herbicide run-off. While the United Kingdom's trials with fiber-cement cladding were modest, they gained prominence in the wake of post-Grenfell safety regulations.

South America, alongside the Middle-East and Africa, held a smaller slice of the market. Brazilian petrochemical liners and Saudi sealants ensured steady volumes, while South Africa's mining slurry lines enjoyed a marked reduction in abrasion. Despite their modest market share, these regions consistently met order demands, contributing to the overarching growth of the nanoclay reinforcement market during the forecast period of 2026-2031.

- 3M

- ALTANA (BYK Additives)

- Amcol corporation

- Elementis PLC

- Globela Pharma

- HTMC Group

- Imerys

- Ionic Mineral Technologies

- KPL International Limited

- KUNIMINE INDUSTRIES CO., LTD.

- Laviosa S.p.A.

- Minerals Technologies Inc

- Mitsubishi Chemical Corporation

- Pipelinepharma

- R.T. Vanderbilt Holding Company, Inc.

- Reade

- RTP Company

- Sika AG

- Techmer PM

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid demand for high-performance and lightweight composites

- 4.2.2 Growing nanocomposite use in automotive and aerospace

- 4.2.3 Regulatory push for barrier-enhanced sustainable packaging

- 4.2.4 Cost-effective intercalation and exfoliation breakthroughs

- 4.2.5 EV battery enclosures needing flame-resistant composites

- 4.3 Market Restraints

- 4.3.1 High processing cost and dispersion complexity

- 4.3.2 EHS/regulatory uncertainty for food-contact nanoclays

- 4.3.3 Competition from graphene, CNTs and other nano-additives

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Montmorillonite

- 5.1.2 Kaolinite

- 5.1.3 Smectite

- 5.1.4 Halloysite

- 5.1.5 Illite

- 5.1.6 Hectorite

- 5.2 By Form

- 5.2.1 Powder

- 5.2.2 Masterbatch

- 5.2.3 Dispersion/Solution

- 5.3 By Reinforcement Matrix

- 5.3.1 Thermoplastics

- 5.3.2 Thermosets

- 5.3.3 Elastomers

- 5.3.4 Biopolymers

- 5.3.5 Other Polymer Systems

- 5.4 By End-user Industry

- 5.4.1 Packaging

- 5.4.2 Automotive and Transportation

- 5.4.3 Building and Construction

- 5.4.4 Consumer Goods and Electronics

- 5.4.5 Healthcare and Medical

- 5.4.6 Aerospace and Defense

- 5.4.7 Energy, Marine and Industrial

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Nordic Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 ALTANA (BYK Additives)

- 6.4.3 Amcol corporation

- 6.4.4 Elementis PLC

- 6.4.5 Globela Pharma

- 6.4.6 HTMC Group

- 6.4.7 Imerys

- 6.4.8 Ionic Mineral Technologies

- 6.4.9 KPL International Limited

- 6.4.10 KUNIMINE INDUSTRIES CO., LTD.

- 6.4.11 Laviosa S.p.A.

- 6.4.12 Minerals Technologies Inc

- 6.4.13 Mitsubishi Chemical Corporation

- 6.4.14 Pipelinepharma

- 6.4.15 R.T. Vanderbilt Holding Company, Inc.

- 6.4.16 Reade

- 6.4.17 RTP Company

- 6.4.18 Sika AG

- 6.4.19 Techmer PM

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Opportunities in Fire-Retardant and Antimicrobial Nanocomposites

- 7.3 Rising use in Bio-polymer and Recyclable Packaging