|

시장보고서

상품코드

2062403

근안 디스플레이 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Near-Eye Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

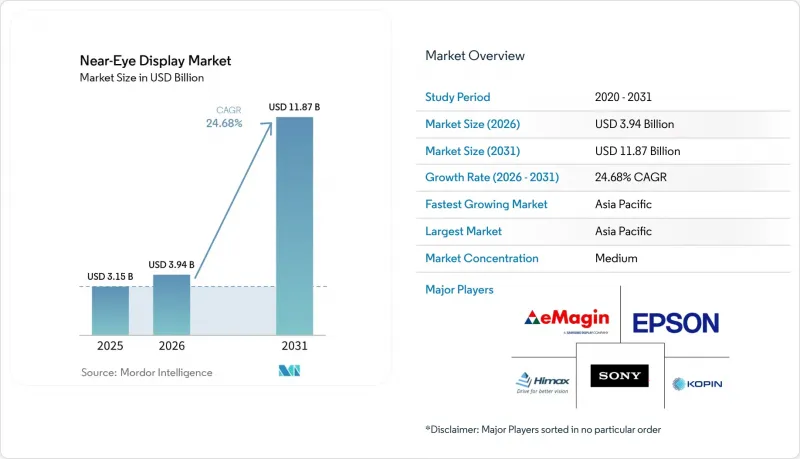

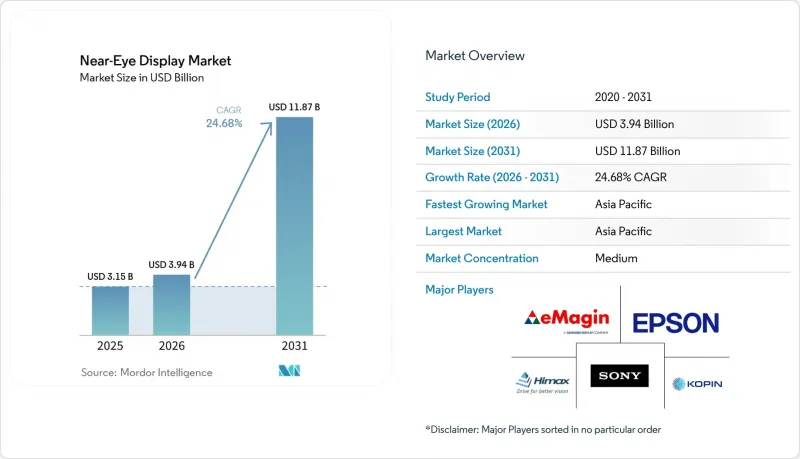

Mordor Intelligence에 의하면, 근안 디스플레이 시장 규모는 2025년 31억 5,000만 달러로 평가되었고, 2026년 39억 4,000만 달러로 추정되고, 2031년까지 118억 7,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 24.68%를 나타낼 것으로 예측됩니다.

본 보고서는 기술별(마이크로 OLED, LCOS, 마이크로 LED, DLP, 레이저 빔 스캐닝), 용도별(가상현실 HMD, 증강현실 스마트글라스, 혼합현실 헤드셋, 자동차용 HUD, 무기용 조준기 및 병사용 HMD), 최종 사용자 산업별(소비자 가전 등), 기본 해상도별(1K 이하 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 근안 디스플레이 시장 동향 및 인사이트

마이크로 OLED 제조 분야의 주요 비용 절감 방안

200mm 웨이퍼에서 300mm 웨이퍼로의 전환을 추진 중인 마이크로 OLED 파운드리 각사는 다이 수율을 향상시키고 단위 비용을 매년 최대 20% 절감하고 있으며, 과거에는 가격 문제로 인해 OLED 마이크로 디스플레이를 채택하기 어려웠던 중가대 헤드셋에도 니어아이 디스플레이 시장 진출의 길을 열어주고 있습니다. 소니 세미컨덕터 솔루션즈는 2025년에 구마모토 공장의 생산 라인을 확장하여 4K 대응 생산 능력을 두 배로 늘리는 한편, 리드 타임을 8주로 단축했습니다. 중국의 경쟁사인 SeeYA Technology는 2025년에 4,000 PPI의 1.03인치 패널을 발표하며, 일본의 기존 제조업체보다 약 15% 더 뛰어난 가성비를 실현하는 비약을 보여주었습니다. 용액 공정을 이용한 폴리머 OLED는 진공 증착 공정을 생략할 수 있어 추가적인 비용 절감이 기대되지만, 신뢰성 데이터에 대해서는 현재 검증 중입니다. 2028년까지 100달러 미만의 모듈이 실현된다면, 500달러 이하의 가격대로 양산되는 AR 글래스가 처음으로 경제적으로 실현 가능해집니다.

VR/MR 헤드셋에서 팬케이크 광학 시스템의 보급

팬케이크 렌즈는 광로를 굴절시켜 헤드셋의 두께를 약 40% 줄여주지만, 광투과율이 최대 80%까지 떨어지기 때문에 디스플레이의 밝기는 1,500니트를 초과해야 합니다. 메타는 2023년에 출시된 퀘스트 3에서 이 방식을 표준화했으며, 2025년에도 여전히 판매량 1위를 유지하고 있습니다. Kopi의 2.6K×2.6K 마이크로 LED 프로토타입은 2025년 초에 10,000니트를 넘어, 무기 LED가 극한의 밝기 요구 사항을 충족할 수 있음을 입증했습니다. 세이코 엡손(Seiko Epson) 등 반사형 LCOS 공급업체들은 패널의 광 손실이 적어 일시적인 우위를 점하고 있으며, 마이크로 LED의 수율이 안정화될 때까지 OEM 제조업체들에게 저비용의 과도기적 해결책을 제공합니다.

고휘도 NED에서 여전히 해결되지 않은 열 관리 과제

메타의 퀘스트 프로는 베퍼 챔버를 채택했음에도 불구하고, 약 1시간 연속 사용 후 사용자에게 불편함을 주었습니다. AR 안경에는 팬을 설치할 공간이 없어, Vuzix의 시제품은 3,000니트에서 10분 후 성능이 저하되었습니다. Kopin과 Applied Materials는 열전도율을 30% 향상시키는 다이아몬드 유사 탄소(DLC) 백플레인에 대한 실험을 진행하고 있습니다. 이러한 소재를 저전력 드라이버와 결합하는 것이 상용화의 핵심이 됩니다. 그렇지 않으면, 근안 디스플레이 시장은 실외에서도 가독성이 확보되는 부문에서 정체될 위험이 있습니다.

부문별 분석

2025년, 마이크로 OLED는 생산 생태계가 성숙하고 수율도 안정적이어서, 근안 디스플레이 시장 매출의 45.94%를 차지했습니다. 그러나 2031년까지 연평균 성장률(CAGR)이 25.21%를 나타낼 것으로 예측되는 마이크로 LED는 가장 빠르게 성장하는 아키텍처로서의 입지를 확고히 하고 있습니다. MicroLED의 근안 디스플레이 시장 점유율은 대량 전사 공정의 수율 문제를 해결할 수 있느냐에 달려 있지만, 5,000니트를 넘는 밝기라는 경쟁력은 이미 AR 안경 OEM 제조업체들의 관심을 끌고 있습니다. LCOS는 ‘충분한’ 밝기와 저렴한 비용이 중시되는 기업용 도구 분야에서 여전히 지지를 받고 있습니다.

DLP는 2025년 코핀(Kopin)이 수주한 2,050만 달러 규모의 미군용 프로젝트에 힘입어, 견고한 무기용 조준기에 채택되고 있습니다. 한편, 레이저 빔 스캔 기술은 저조도 실내용 안경이라는 틈새 시장에 국한되어 있습니다. Guangdong Jade Bird Display의 4μm 픽셀 피치는 아시아의 파운드리 업체들이 어떻게 비용을 절감하고 보급을 가속화하고 있는지를 보여줍니다. 2028년까지 상용 MicroLED 모듈의 가격이 150달러 아래로 떨어지면, 이 기술 분야 내의 근안 디스플레이 시장 규모는 AR 안경 분야에서 Micro-OLED를 능가할 가능성이 있습니다.

2025년에는 게임 수요에 힘입어 VR 헤드마운트 디스플레이가 매출의 63.42%를 차지했으나, AR 스마트글래스는 2031년까지 연평균 성장률(CAGR) 25.53%라는 가장 높은 성장 궤도에 올라 있습니다. 메타는 2025년 말까지 700만 대 이상의 레이밴 스마트글래스를 판매함으로써, 아이웨어라는 폼 팩터가 ‘가제트’라는 꼬리표를 달지 않고도 주류로 받아들여질 수 있음을 사회적으로 입증했습니다.

Xreal의 ‘Air 2 Pro’가 DHL의 물류 현장에 도입되면서, 시범 프로젝트를 넘어 기업 차원의 수용이 이루어졌음이 밝혀졌습니다. 혼합현실(MR) 헤드셋은 투명성과 몰입감을 동시에 확보해야 하는 건축가나 외과의사들이 활용하고 있습니다. LCOS 패널을 채택한 자동차용 헤드업 디스플레이는 Lucid의 ‘Gravity’ SUV와 같은 프리미엄 전기차의 차별화 요소로 자리 잡고 있습니다. 군용 조준기는 생산 대수는 적지만 높은 이익률을 가져다주며, 더 광범위한 근안 디스플레이 시장 전체의 혁신 주기를 뒷받침하고 있습니다.

지역별 분석

아시아태평양은 2025년에 니어아이 디스플레이 매출의 46.81%를 차지한 것으로 평가되었으며, 중국이 실리콘 기판용 OLED 제조 공장을 증설하고 일본이 정밀 코팅 기술을 추진함에 따라 2031년까지 연평균 성장률(CAGR) 25.06%로 확대될 것으로 전망됩니다. BOE의 청두 공장은 2027년까지 연간 100만 대의 OLED 마이크로 디스플레이 생산을 목표로 하고 있으며, 이를 통해 중국의 수입 부품 의존도를 낮출 것으로 전망됩니다. 소니와 세이코 엡손은 전 세계 OEM 제조업체들이 따라잡기 위해 분주한 화소 밀도 기준을 지속적으로 제시하며, 일본의 영향력을 강화하고 있습니다. 한국에서 진행 중인 MicroLED 시범 프로젝트는 차세대 AR 안경용 부품의 현지 조달을 예고하고 있는 반면, 인도의 게이밍 카페는 풀뿌리 차원에서 VR 보급의 발판이 되고 있습니다.

북미는 민수용과 국방용 수요라는 두 가지 축을 바탕으로 성장하고 있습니다. 메타의 퀘스트 생태계가 소매 시장의 성장세를 주도하고 있으며, 레이밴의 스마트 안경이 패션 분야에서 입지를 다지고 있습니다. 코핀이 수주한 2,050만 달러 규모의 무기용 조준기 계약과 이 회사의 헬멧 파일럿 프로젝트는 경기 변동에 민감한 민간 소비 지출에 비해, 연구개발(R&D)을 뒷받침하는 군사 예산의 중요성을 여실히 보여주고 있습니다. 캐나다와 멕시코는 각각 설계 인력과 최종 조립을 담당하며, 수직적으로 다양한 지역 공급망을 형성하고 있습니다.

유럽은 엄격한 규제 체계를 경쟁상의 강점으로 활용하고 있습니다. EU는 2025년에 레이저 안전 기준으로 IEC 62471 및 IEC TS 60825-20을 채택했으며, 제품 출시가 지연되기는 했지만 품질에 대한 평가는 높아지고 있습니다. BMW의 파노라믹 비전(도로용 HUD)이나 메르세데스-벤츠가 진행한 조수석 측 AR 엔터테인먼트 실험은 자동차 분야 수요를 여실히 보여주고 있습니다. 영국과 프랑스의 국방 프로그램에서는 내환경성이 뛰어난 헤드마운트 디스플레이가 도입되고 있는 반면, 중동 및 아프리카 및 남미에서는 스마트폰 보급률 상승과 정부 주도의 스마트시티 구상과 맞물려 초기 단계의 성장이 나타나고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the near-eye display market size is projected to expand from USD 3.15 billion in 2025 and USD 3.94 billion in 2026 to USD 11.87 billion by 2031, registering a CAGR of 24.68% between 2026 to 2031.

This report is Segmented by Technology (Micro-OLED, LCOS, Microled, DLP, and Laser Beam Scanning), Application (Virtual-Reality HMDs, Augmented-Reality Smart Glasses, Mixed-Reality Headsets, Automotive HUDs, Weapon Sights and Soldier HMDs), End-User Industry (Consumer Electronics, and More), Native Resolution (Up To 1K, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Near-Eye Display Market Trends and Insights

Mainstream Cost-Down of Micro-OLED Manufacturing

Micro-OLED foundries shifting from 200 mm to 300 mm wafers are pushing die yields higher and slicing unit costs by as much as 20% each year, opening the near-eye display market to mid-tier headsets that once priced out OLED micro displays. Sony Semiconductor Solutions expanded its Kumamoto line in 2025, doubling 4K-capable output and shrinking lead times to eight weeks. Chinese rival SeeYA Technology unveiled a 1.03-inch panel with 4,000 PPI in 2025, signaling a cost-performance leap that undercuts Japanese incumbents by nearly 15%. Solution-processed polymer OLEDs promise additional savings because they avoid vacuum evaporation, though reliability data remains under validation. If sub-USD 100 modules materialize before 2028, mass-market AR glasses retailing below USD 500 become financially viable for the first time.

Widespread Adoption of Pancake Optics in VR/MR Headsets

Pancake lenses fold the light path, reducing headset depth by roughly 40% yet sacrificing up to 80% of light throughput, which forces displays past 1,500 nits. Meta standardized the approach in Quest 3, released in 2023, and is still the volume leader in 2025. Kopin's 2.6K X 2.6K MicroLED prototype surpassed 10,000 nits in early 2025, proving that inorganic LEDs meet extreme brightness demand. Reflective LCOS suppliers such as Seiko Epson gain an interim advantage because their panels waste less light, giving OEMs a lower-cost bridge until MicroLED yields mature.

Persistent Thermal Management Challenges in High-Brightness NEDs

Meta's Quest Pro used vapor chambers but still triggered user discomfort after about one hour of continuous play. AR glasses lack space for fans, and prototypes from Vuzix throttled after 10 minutes at 3,000 nits. Kopin and Applied Materials are experimenting with diamond-like carbon backplanes that raise thermal conductivity by 30%. Commercial rollout depends on pairing these materials with low-power drivers, or the near-eye display market risks stagnation in outdoor-readable segments.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Gaming/Entertainment Content Ecosystems

- Restraint (~) % Impact on CAGR Forecast Geographic Relevance Impact Timeline Persistent Thermal Management Challenges in High-Brightness NEDs -3.70% Global, acute in compact AR glasses Short term (<= 2 years) Limited Lifetime of Blue Emitters in OLEDoS Panels -2.90% Global, particularly Japan and South Korea manufacturing Medium term (2-4 years) Supply-Chain Fragility for High-PPI Backplanes -2.30% Asia-Pacific and North America Medium term (2-4 years) EU Regulatory Scrutiny on Ocular Safety Limits for XR -1.80% Europe, with global compliance ripple effects Long term (>= 4 years)

- Limited Lifetime of Blue Emitters in OLEDoS Panels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Micro-OLED delivered 45.94% of revenue for the near-eye display market in 2025 as its production ecosystem remains mature and yields stable. However, MicroLED's 25.21% CAGR expectation through 2031 positions it as the fastest rising architecture. The near-eye display market share for MicroLED hinges on solving mass-transfer yields, but brightness advantages above 5,000 nits already attract AR-glass OEMs. LCOS maintains traction in enterprise tools where "good enough" brightness and low-cost rule.

DLP serves rugged weapon sights, supported by Kopin's USD 20.5 million U.S. military order in 2025, while laser beam scanning stays niche for low-light indoor eyewear. Guangdong Jade Bird Display's 4 µm pixel pitch exemplifies how Asian foundries compress costs and accelerate adoption. If commercial MicroLED modules fall below USD 150 by 2028, the near-eye display market size for this technology tier could surpass Micro-OLED in AR glasses.

VR head-mounted displays controlled 63.42% revenue in 2025, sustained by gaming demand, but AR smart glasses are on track for the fastest 25.53% CAGR to 2031. Meta sold over 7 million Ray-Ban smart glasses by late 2025, providing social validation that eyewear form factors can achieve mainstream uptake without "tech-toy" stigma.

Xreal's Air 2 Pro found logistic deployments at DHL, revealing enterprise acceptance beyond pilot projects. Mixed-reality headsets serve architects and surgeons needing transparency plus immersion. Automotive head-up displays using LCOS panels now differentiate premium EVs like Lucid's Gravity SUV. Military weapon sights, though smaller in units, deliver high margins that subsidize innovation cycles across the wider near-eye display market.

Geography Analysis

Asia-Pacific delivered 46.81% of near-eye display revenue in 2025 and should expand at 25.06% CAGR through 2031 as China ramps OLED-on-silicon fabs and Japan advances precision coatings. BOE's Chengdu line aims for 1 million OLED micro displays annually by 2027, trimming Chinese reliance on imported parts. Sony and Seiko Epson continue to set pixel-density benchmarks that global OEMs chase, reinforcing Japan's influence. South Korea's pilot MicroLED initiatives forecast localized supply for next-gen AR eyewear, while India's gaming cafes seed grassroots VR uptake.

North America rides on dual poles of consumer and defense demand. Meta's Quest ecosystem anchors retail momentum, and Ray-Ban smart glasses cement fashion credibility. Kopin's USD 20.5 million weapon-sight award plus its pilot helmet project underscore military budgets that cushion R&D against cyclical consumer spending. Canada and Mexico contribute design talent and final assembly, respectively, rounding out a vertically diverse regional chain.

Europe leverages strict regulatory frameworks as a competitive moat. The EU adopted IEC 62471 and IEC TS 60825-20 for laser safety in 2025, delaying launches but elevating perceived quality. BMW's Panoramic Vision roadway HUD and Mercedes-Benz experiments in passenger-side AR entertainment illustrate automotive demand. Defense programs in the United Kingdom and France procure hardened head-mounted displays, while the Middle East and Africa and South America record early-stage growth linked to rising smartphone penetration and government smart-city initiatives.

- Sony Semiconductor Solutions Corporation

- Seiko Epson Corporation

- eMagin Corporation

- Kopin Corporation

- Himax Display Incorporated

- BOE Technology Group Co., Ltd.

- SeeYA Technology Co., Ltd.

- Guangdong Jade Bird Display Technology Co., Ltd.

- MicroOLED S.A.S.

- Plessey Semiconductors Ltd.

- VueReal Inc.

- Mojo Vision Inc.

- Jasper Display Corporation

- RaonTech Inc.

- Lakeside Optronics Technology Co., Ltd.

- Lumiode Inc.

- SiliconCore Technology Inc.

- MicroVision Inc.

- Texas Instruments Incorporated (DLP Products)

- TCL CSOT - TCL China Star Optoelectronics Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream cost-down of Micro-OLED manufacturing

- 4.2.2 Widespread adoption of pancake optics in VR/MR headsets

- 4.2.3 Surge in gaming/entertainment content ecosystems

- 4.2.4 Emergence of MicroLED-on-silicon pilot fabs

- 4.2.5 AI-generated dynamic foveated rendering algorithms

- 4.2.6 U.S. DoD "Wearable Cockpit" procurement program

- 4.3 Market Restraints

- 4.3.1 Persistent thermal management challenges in high-brightness NEDs

- 4.3.2 Limited lifetime of blue emitters in OLEDoS panels

- 4.3.3 Supply-chain fragility for high-PPI backplanes

- 4.3.4 EU regulatory scrutiny on ocular safety limits for XR

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Micro-OLED

- 5.1.2 LCOS

- 5.1.3 MicroLED

- 5.1.4 DLP

- 5.1.5 Laser Beam Scanning

- 5.2 By Application

- 5.2.1 Virtual-Reality Head-Mounted Displays

- 5.2.2 Augmented-Reality Smart Glasses

- 5.2.3 Mixed-Reality Headsets

- 5.2.4 Automotive Head-Up Displays

- 5.2.5 Weapon Sights and Soldier HMDs

- 5.3 By End-User Industry

- 5.3.1 Consumer Electronics

- 5.3.2 Enterprise and Industrial

- 5.3.3 Healthcare

- 5.3.4 Defense and Security

- 5.4 By Native Resolution

- 5.4.1 Up to 1 K (HD and below)

- 5.4.2 Between 1 K-2 K (FHD class)

- 5.4.3 Between 2 K-4 K

- 5.4.4 Above 4 K

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sony Semiconductor Solutions Corporation

- 6.4.2 Seiko Epson Corporation

- 6.4.3 eMagin Corporation

- 6.4.4 Kopin Corporation

- 6.4.5 Himax Display Incorporated

- 6.4.6 BOE Technology Group Co., Ltd.

- 6.4.7 SeeYA Technology Co., Ltd.

- 6.4.8 Guangdong Jade Bird Display Technology Co., Ltd.

- 6.4.9 MicroOLED S.A.S.

- 6.4.10 Plessey Semiconductors Ltd.

- 6.4.11 VueReal Inc.

- 6.4.12 Mojo Vision Inc.

- 6.4.13 Jasper Display Corporation

- 6.4.14 RaonTech Inc.

- 6.4.15 Lakeside Optronics Technology Co., Ltd.

- 6.4.16 Lumiode Inc.

- 6.4.17 SiliconCore Technology Inc.

- 6.4.18 MicroVision Inc.

- 6.4.19 Texas Instruments Incorporated (DLP Products)

- 6.4.20 TCL CSOT - TCL China Star Optoelectronics Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment