|

시장보고서

상품코드

2062438

차량 도난 방지 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vehicle Anti-Theft System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

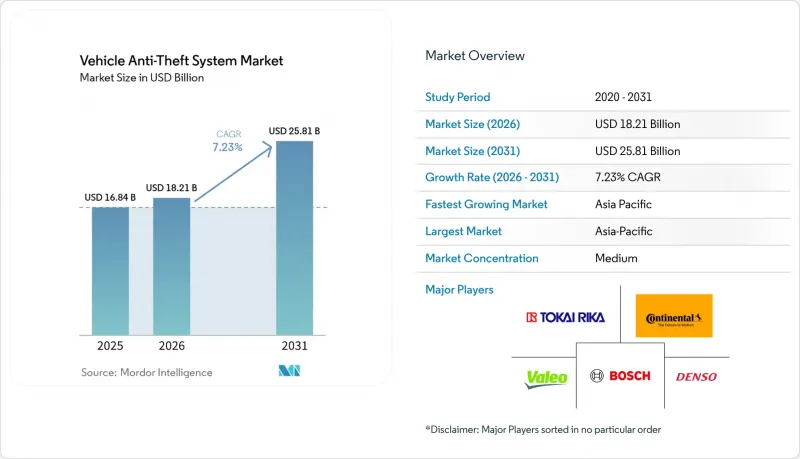

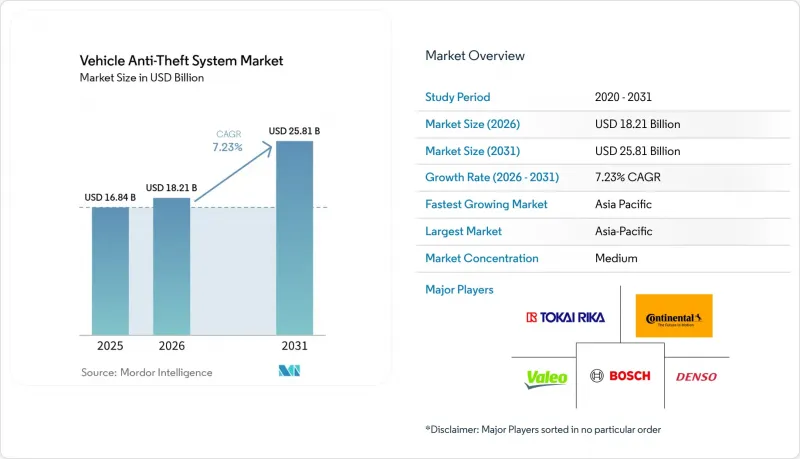

Mordor Intelligence에 의하면, 차량 도난 방지 시스템 시장 규모는 2025년에 168억 4,000만 달러로 평가되었고, 2026년 182억 1,000만 달러로 추정되고, 2031년까지 258억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.23%를 나타낼 전망입니다.

본 보고서는 제품 유형별(경보 장치, 이모빌라이저, 스티어링 휠 및 컬럼 잠금장치, 패시브 키리스 엔트리 등), 기술별(RFID, GPS/GNSS, GSM/LTE/5G, Bluetooth/BLE 등), 차종별(승용차, 소형 상용차, 대형 상용차 등), 판매 채널별(OEM 탑재 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 차량 도난 방지 시스템 시장 동향 및 분석

세계의 차량 도난 사건 증가

2025-2026년 조직 범죄 집단의 릴레이 공격과 CAN 버스 공격이 격화되었습니다. 리우데자네이루에서는 2026년 첫 2개월 동안 5,344건의 절도 사건이 기록되었으며, 인도에서는 2023년에 22만 4,187건의 오토바이 절도 사건이 기록되었습니다. 미국에서는 2025년에 65만 9,880건의 도난 사건이 보고되었으나, 이모빌라이저가 장착되지 않은 특정 브랜드의 경우 유난히 많은 피해가 발생했습니다. 한편, 200유로(213달러) 미만의 저렴한 가격의 다크웹산 중계 장치가 유럽 전역으로 확산되면서, OEM 제조업체들에게 GPS 추적 및 생체 인식 기능을 갖춘 이모빌라이저 도입을 요구하는 압력이 거세지고 있습니다.

이모빌라이저 의무화를 위한 정부의 규제

인도의 AIS-140 규정은 차량의 안전성과 감시 시스템 강화를 목적으로, 배기량 1,500cc를 초과하는 모든 승용차로 적용 범위를 확대했습니다. 한편, 중국의 GB 44495-2024는 종합적인 사이버 보안 감사와 연간 약 2,800만 대의 차량에 대한 암호화 이모빌라이저 도입을 의무화하고 있으며, 이는 중국이 자동차 사이버 보안에 주력하고 있음을 반영합니다. 브라질에서는 수년에 걸쳐 Contran 규정이 시행되고 있는 반면, 유럽의 형식 승인 규정(EU) 2018/858은 제조업체에 엄격한 규정 준수 요건을 부과하고 있습니다. 이러한 규제의 변화에 따라 OEM(원청 제조업체)의 개발 주기가 대폭 단축됨에 따라, 1차 공급업체들은 안전하고 규정을 준수하는 자동차 기술에 대한 수요 증가에 부응하기 위해 초광대역(UWB) 키 솔루션 및 암호화 모듈의 출시를 서두르고 있습니다.

고급 시스템의 높은 초기 도입 비용과 교체 비용

출고 시 300-800달러의 추가 비용이 발생하고, 사후 시장에서는 그 비용이 더욱 높아지는 생체 인식 출입 시스템은 제조업체와 소비자 모두에게 중요한 고려 사항이 되고 있습니다. 그러나 스마트 키를 분실했을 때의 교체 비용이 고액이며(최대 600달러에 더해 딜러의 프로그래밍 비용도 발생), 특히 가격에 민감한 아시아태평양 시장에서는 이러한 점이 도입의 걸림돌이 되고 있습니다. 또한, 차량 텔레매틱스용 하드웨어 및 관련 구독 요금은 3년간의 소유 비용을 차량 당 최대 2,300달러까지 증가시킬 수 있습니다. 이러한 비용 부담으로 인해 텔레매틱스 솔루션 도입이 주춤하고 있으며, 특히 예산이 한정되어 비용 효율성을 우선시하는 소규모 물류 업체에서 이러한 현상이 두드러집니다.

부문별 분석

이모빌라이저는 유럽 전역에서 거의 보편적으로 탑재되고 있으며, 인도에서의 의무화 확대에 힘입어 2025년 매출의 37.25%를 차지했으며, 차량 도난 방지 시스템 시장을 독점했습니다. 이러한 시스템은 엄격한 규제와 차량 보안 강화에 대한 소비자 수요가 증가함에 따라 많은 차량에 기본 사양으로 탑재되고 있습니다. 그러나 현재 시장에서는 초광대역(UWB) 디지털 키가 보급되기 시작하며 연평균 성장률(CAGR) 8.11%로 성장하고 있어 변화가 나타나고 있습니다. 이러한 성장은 자동차 제조업체(OEM)들이 릴레이 공격에 대한 내성을 갖춘 기술 개발에 주력하고 있기 때문입니다. 예를 들어, BMW의 비행 시간 인증 기술은 신호 증폭 범위를 10cm 미만으로 제한하도록 설계되어, 고정 주파수 RFID 키의 심각한 취약점을 효과적으로 해결하고 있습니다. 이러한 혁신은 진화하는 위협에 대응하여 보안 대책을 강화하려는 업계의 노력을 여실히 보여주고 있습니다.

북미에서는 애프터마켓용 경보 시스템이, 특히 차량 보안을 한층 더 강화하고 싶어 하는 소비자들 사이에서 여전히 인기를 끌고 있습니다. 그러나 제조업체 순정 이모빌라이저와 경보기가 세트로 제공되는 추세가 강해짐에 따라, 단독형 애프터마켓 경보기 시스템에 대한 수요는 점차 감소하고 있습니다. 그럼에도 불구하고, 스티어링 칼럼 잠금 장치와 같은 기존의 보안 대책이 눈에 띄게 부활하고 있습니다. 예를 들어, 현대자동차는 USB를 이용한 시동 우회 공격에 취약한 차량 소유자들에게 6만 2,000개의 스티어링 칼럼 잠금 장치를 배포했습니다. 이러한 움직임은 특정 취약점을 해결하고 차량 보안 시스템에 대한 대중의 신뢰를 유지하는 데 있어, 저기술 하드웨어 솔루션이 여전히 중요하다는 점을 강조하고 있습니다.

2025년에는 RFID 트랜스폰더가 매출의 45.16%를 차지했으며, 자동차 시장에서 주요 이모빌라이저 기술로 자리매김했습니다. 이러한 트랜스폰더는 고정 주파수 아키텍처로 작동하는데, 이는 효과적이긴 하지만 중계 증폭 공격에 취약합니다. 이러한 공격은 주파수의 고정성을 악용하는 것으로, 차량에 심각한 보안 위험을 초래합니다. 이러한 과제가 있음에도 불구하고, RFID 트랜스폰더는 저렴한 가격과 기존 차량 시스템과의 호환성 덕분에 여전히 인기 있는 선택지로 남아 있습니다. 이러한 기술의 광범위한 도입은 위험을 줄이고 소비자의 신뢰를 유지하기 위해 강화된 보안 대책을 마련해야 할 필요성을 여실히 보여주고 있습니다.

초광대역(UWB) 시장은 연평균 성장률(CAGR) 7.56%로 성장하고 있으며, 이 기술은 자동차 업계에 새로운 차원의 보안과 편의성을 제공합니다. UWB는 나노초 단위의 비행 시간을 측정하여 작동하며, 스마트폰을 안전한 디지털 키로 활용하게 합니다. 2025년까지 이 혁신적인 기능이 18가지 다른 차종에 탑재될 것으로 예상되며, 보안과 사용자 편의성이 향상될 전망입니다. 또한, 셀룰러 연결형 GPS 추적기는 도난 차량 회수 및 예측 유지보수를 지원하기 위해 수조 개의 데이터 포인트를 처리하는 차량 관리에 있어 필수적인 도구가 되었습니다. 그러나, 고도의 보안 기능을 제공하는 생체 인증 모듈은 제조 비용이 높기 때문에 여전히 고급차 사양으로 한정되어 있어, 그 보급은 제한적입니다.

지역별 분석

아시아태평양은 2025년 매출 점유율 35.34%로 차량 도난 방지 시스템 시장을 주도한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 7.74%를 기록하며 성장할 것으로 전망됩니다. 인도의 AIS-140 GPS 의무화 및 중국의 2026년 1월 시행 예정인 사이버 보안 규정에 따라, 연간 2,800만 대의 신차에 암호화된 이모빌라이저 탑재가 의무화됨에 따라 OEM 모듈 및 인증된 애프터마켓용 트래커에 대한 수요가 증가하고 있습니다. 특히 마하라슈트라주와 카르나타카주에서 오토바이 도난 사건이 증가함에 따라, 이륜차용 텔레매틱스 제품 판매가 가속화되고 있습니다. 또한, 해당 지역에서 커넥티드카 기술의 보급 확대가 첨단 도난 방지 시스템의 통합을 촉진하고 있습니다. 일본과 한국에서는 이모빌라이저 보급률이 90%를 넘고 있으며, 현재 릴레이 공격에 대응하기 위한 패치를 배포하고 있습니다. 또한, 차량의 안전성과 보안을 강화하기 위한 정부의 이니셔티브이 해당 지역 시장 성장을 견인할 것으로 예측됩니다.

유럽에서는 규정(EU) 2018/858에 따라 이모빌라이저에 대한 엄격한 적합성 요건이 유지되고 있지만, 도난 발생 추세에는 지역별 차이가 있습니다. 영국에서는 2025년 도난 건수가 11.36% 감소해 9만 625건을 기록한 반면, 네덜란드에서는 저렴한 릴레이 도구가 온라인으로 유통되면서 12% 증가세를 보였습니다. 유럽연합 집행위원회가 2025년에 제안한, 2028년까지 자율주행 차량에 생체 인증 시스템을 의무적으로 탑재하도록 하는 방안은 콘티넨탈이나 발레오와 같은 부품 공급업체들에게 새로운 계약 기회를 가져다줄 것으로 예측됩니다. 또한, 해당 지역에서의 전기차 보급 확대는 첨단 도난 방지 시스템에 대한 수요 창출로 이어질 것으로 예측됩니다. 텔레매틱스 및 커넥티드카 기술의 보급 확대 또한 시장 성장을 뒷받침하고 있습니다. 또한, 자동차 제조업체와 기술 제공업체 간의 협력을 통해 유럽의 규제 및 소비자 선호도에 부합하는 도난 방지 솔루션의 혁신이 추진되고 있습니다.

북미에서는 2025년에 65만 9,880건의 도난 사건이 기록되어 전년 대비 23% 감소했으나, 이모빌라이저가 장착되지 않은 현대 및 기아 모델은 여전히 취약한 상태였으며, 이에 따라 무료 스티어링 락 캠페인 및 소프트웨어 업데이트가 실시되었습니다. 해당 지역에서 ADAS(첨단 운전자 지원 시스템) 및 커넥티드카 기술에 대한 집중 투자가 통합형 도난 방지 솔루션 도입을 촉진하고 있습니다. 남미에서는 픽업트럭 도난 사건이 급증하고 있으며, 리우데자네이루에서는 전년 대비 5% 증가했고, 픽업트럭 전체로는 12.2% 증가했습니다. 저렴한 가격의 애프터마켓용 도난 방지 장치의 입수 가능성이 높아지고 있는 점도 해당 지역 시장에 영향을 미치고 있습니다. 중동 및 아프리카는 여전히 개발도상국이지만, 걸프협력회의(GCC)의 안전 규정에 따라 GPS 탑재가 의무화된 상용차용 추적기에 대한 수요가 증가하고 있습니다. 또한, 해당 지역의 자동차 보유 대수 증가와 물류 및 운송 부문의 확대가 도난 방지 시스템 도입을 촉진할 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the vehicle anti-theft system market size was valued at USD 16.84 billion in 2025 and estimated to grow from USD 18.21 billion in 2026 to reach USD 25.81 billion by 2031, at a CAGR of 7.23% during the forecast period (2026-2031).

This report is Segmented by Product Type (Alarm, Immobilizer, Steering-Wheel/Column Lock, Passive Keyless Entry, and More), Technology (RFID, GPS/GNSS, GSM/LTE/5G, Bluetooth/BLE, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and More), Sales Channel (OEM-Installed, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Vehicle Anti-Theft System Market Trends and Insights

Rising Global Vehicle-Theft Incidents

Organized crime rings intensified relay and CAN-bus attacks during 2025-2026, with Rio de Janeiro logging 5,344 thefts in the first two months of 2026 and India recording 224,187 motorcycle thefts in 2023. The United States reported 659,880 thefts in 2025, yet specific brands without immobilizers saw disproportionate losses. Meanwhile, affordable dark-web relay devices priced below EUR 200 (USD 213) are spreading across Europe, widening pressure on OEMs to layer on immobilizers with GPS tracking and biometric authentication.

Government Mandates Making Immobilizers Compulsory

India's AIS-140 regulation now extends to all passenger vehicles with engine capacities exceeding 1,500 cc, aiming to enhance vehicle safety and monitoring systems. Meanwhile, China's GB 44495-2024 mandates comprehensive cybersecurity audits and the implementation of encrypted immobilizers across approximately 28 million vehicles annually, reflecting the country's focus on automotive cybersecurity. Brazil continues to enforce its long-standing Contran rules, while Europe's Type Approval Regulation (EU) 2018/858 imposes stringent compliance requirements on manufacturers. These evolving regulations are significantly compressing original equipment manufacturers' (OEMs) development cycles, driving tier-1 suppliers to expedite the launch of ultra-wideband (UWB) key solutions and encrypted modules to meet the growing demand for secure and compliant automotive technologies.

High Upfront and Replacement Cost of Advanced Systems

Biometric entry systems, which add USD 300-800 at the factory and even higher costs in the aftermarket, are becoming a significant consideration for manufacturers and consumers alike. However, the high replacement cost of a lost smart key, which can reach up to USD 600 plus dealer programming fees, has discouraged adoption, particularly in price-sensitive Asia-Pacific markets. Additionally, fleet telematics hardware and associated subscription fees can increase three-year ownership costs by up to USD 2,300 per vehicle. This cost burden has slowed the adoption of telematics solutions, especially among small logistics operators who often operate on tight budgets and prioritize cost-efficiency.

Other drivers and restraints analyzed in the detailed report include:

- OEM Integration of Smart Keys and Connected Security

- Insurance Premium Discounts for Certified Systems

- Cyber-Security and Data-Privacy Vulnerabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Immobilizers dominated the vehicle anti-theft system market, accounting for 37.25% of 2025 revenue, driven by their near-universal fitment across Europe and expanding mandates in India. These systems have become a standard feature in many vehicles, driven by stringent regulations and increasing consumer demand for enhanced vehicle security. However, the market is witnessing a shift as Ultra-Wideband (UWB) digital keys are gaining traction, growing at a compound annual growth rate (CAGR) of 8.11%. This growth is attributed to the increasing focus of original equipment manufacturers (OEMs) on developing relay-attack-resistant technologies. For instance, BMW's time-of-flight authentication technology has been designed to limit signal amplification to less than 10 cm, effectively addressing a critical vulnerability in fixed-frequency RFID keys. This innovation highlights the industry's commitment to advancing security measures in response to evolving threats.

Aftermarket alarms remain popular in North America, particularly among consumers seeking additional layers of security for their vehicles. However, the growing trend toward factory-installed immobilizer-plus-alarm packages is gradually eroding demand for standalone aftermarket alarm systems. Despite this, traditional security measures like steering-column locks have made a notable comeback. For example, Hyundai distributed 62,000 steering-column locks to owners of vehicles prone to USB-ignition bypass attacks. This move underscores the enduring relevance of low-tech hardware solutions in addressing specific vulnerabilities and maintaining public trust in vehicle security systems.

RFID transponders accounted for 45.16% of the revenue in 2025, serving as the primary immobilizer technology in the automotive market. These transponders operate on a static-frequency architecture, which, while effective, is vulnerable to relay amplification attacks. Such attacks exploit the static nature of the frequency, posing significant security risks to vehicles. Despite these challenges, RFID transponders remain a popular choice due to their affordability and compatibility with existing vehicle systems. Their widespread adoption underscores the need to develop enhanced security measures to mitigate risks and maintain consumer trust in this technology.

The ultra-wideband (UWB) market is growing at a CAGR of 7.56%, and its technology has introduced a new layer of security and convenience in the automotive sector. UWB operates by registering nanosecond-level time-of-flight measurements, enabling smartphones to function as secure digital keys. By 2025, this innovative feature is expected to be integrated into 18 different vehicle model lines, offering enhanced security and user convenience. Additionally, cellular-linked GPS trackers have become a critical tool for fleet management, processing trillions of data points to support theft recovery and predictive maintenance. However, biometric modules, which offer advanced security features, remain confined to luxury vehicle trims due to their high production costs, limiting their broader adoption.

Geography Analysis

Asia-Pacific led the vehicle anti-theft system market with 35.34% revenue share in 2025 and is projected to grow at a 7.74% CAGR through 2031. India's AIS-140 GPS mandate and China's January 2026 cybersecurity rules compel encrypted immobilizers across 28 million new vehicles annually, lifting demand for OEM modules and certified aftermarket trackers. Rising motorcycle theft, especially in Maharashtra and Karnataka, is accelerating sales of two-wheeler telematics. Additionally, the increasing adoption of connected vehicle technologies in the region is driving the integration of advanced anti-theft systems. Japan and South Korea maintain over 90% immobilizer penetration, yet now roll out patches to counter relay exploits. Furthermore, government initiatives promoting vehicle safety and security are expected to bolster the market growth in the region.

Europe maintains strict immobilizer compliance under Regulation (EU) 2018/858, yet theft patterns diverge. The United Kingdom cut theft by 11.36% to 90,625 incidents in 2025, while the Netherlands saw a 12% increase as inexpensive relay tools circulated online. The European Commission's 2025 proposal to mandate biometrics on autonomous-ready models by 2028 positions suppliers such as Continental and Valeo for new contracts. Additionally, the growing adoption of electric vehicles in the region is expected to create opportunities for advanced anti-theft systems. The growing adoption of telematics and connected vehicle technologies is also driving market growth. Moreover, collaborations between automakers and technology providers are fostering innovation in anti-theft solutions tailored to European regulations and consumer preferences.

North America recorded 659,880 thefts in 2025, a 23% decline, yet Hyundai and Kia models without immobilizers remained vulnerable, prompting free steering-lock campaigns and software updates. The region's focus on advanced driver assistance systems (ADAS) and connected vehicle technologies is driving the adoption of integrated anti-theft solutions. South America faces surging pick-up theft, with Rio de Janeiro up 5% year-on-year and pick-up trucks up 12.2%. The increasing availability of affordable aftermarket anti-theft devices is also influencing the market in the region. Middle East and Africa remain nascent but register growing demand for GPS-mandated commercial-vehicle trackers under Gulf Cooperation Council safety rules. Additionally, rising vehicle ownership and the expansion of logistics and transportation sectors in these regions are expected to drive the adoption of anti-theft systems.

- Continental AG

- Robert Bosch GmbH

- Valeo SE

- Denso Corporation

- Tokai Rika Co., Ltd.

- HELLA GmbH & Co. KGaA

- Huf Hulsbeck & Furst GmbH & Co. KG

- Minda Corporation Limited

- U-Shin Ltd. (MinebeaMitsumi Inc.)

- Lear Corporation

- Marquardt GmbH

- Alps Alpine Co., Ltd.

- Omron Corporation

- Stoneridge, Inc.

- Directed LLC

- Scorpion Automotive Ltd.

- Cobra Automotive Technologies S.p.A.

- Meta System S.p.A.

- Zhejiang Daibang Lock Co., Ltd.

- Jingjing Guanghua Smart Lock Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Vehicle-Theft Incidents

- 4.2.2 Government Mandates Making Immobilizers Compulsory

- 4.2.3 OEM Integration of Smart Keys and Connected Security

- 4.2.4 Insurance Premium Discounts for Certified Systems

- 4.2.5 Ultra-Wideband Digital-Key Ecosystems (Under-Reported)

- 4.2.6 AI-Driven Telematics Anomaly Detection for Fleets (Under-Reported)

- 4.3 Market Restraints

- 4.3.1 High Upfront and Replacement Cost of Advanced Systems

- 4.3.2 Cyber-Security and Data-Privacy Vulnerabilities

- 4.3.3 Sophisticated Relay, CAN-Bus Injection Attacks

- 4.3.4 After-Market Installation Quality Variability (Under-Reported)

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Alarm

- 5.1.2 Immobilizer

- 5.1.3 Steering-Wheel / Column Lock

- 5.1.4 Passive Keyless Entry

- 5.1.5 Biometric Capture Device

- 5.1.6 GPS / GSM Tracking System

- 5.1.7 Ultra-Wideband Digital Key

- 5.2 By Technology

- 5.2.1 RFID

- 5.2.2 GPS / GNSS

- 5.2.3 GSM / LTE / 5G

- 5.2.4 Bluetooth / BLE

- 5.2.5 Ultra-Wideband (UWB)

- 5.2.6 Biometric (Fingerprint / Facial)

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Two-Wheelers and Powersports

- 5.3.5 Off-Road and Construction Equipment

- 5.4 By Sales Channel

- 5.4.1 OEM-Installed

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Valeo SE

- 6.4.4 Denso Corporation

- 6.4.5 Tokai Rika Co., Ltd.

- 6.4.6 HELLA GmbH & Co. KGaA

- 6.4.7 Huf Hulsbeck & Furst GmbH & Co. KG

- 6.4.8 Minda Corporation Limited

- 6.4.9 U-Shin Ltd. (MinebeaMitsumi Inc.)

- 6.4.10 Lear Corporation

- 6.4.11 Marquardt GmbH

- 6.4.12 Alps Alpine Co., Ltd.

- 6.4.13 Omron Corporation

- 6.4.14 Stoneridge, Inc.

- 6.4.15 Directed LLC

- 6.4.16 Scorpion Automotive Ltd.

- 6.4.17 Cobra Automotive Technologies S.p.A.

- 6.4.18 Meta System S.p.A.

- 6.4.19 Zhejiang Daibang Lock Co., Ltd.

- 6.4.20 Jingjing Guanghua Smart Lock Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment