|

시장보고서

상품코드

2062445

위협 감지 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Threat Detection Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

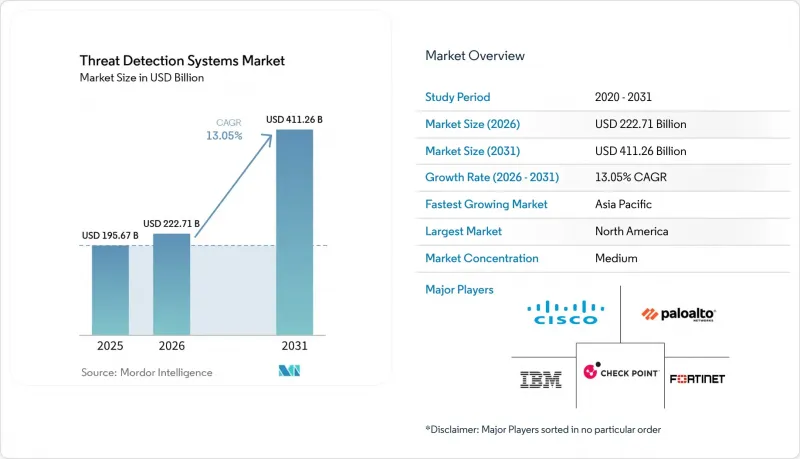

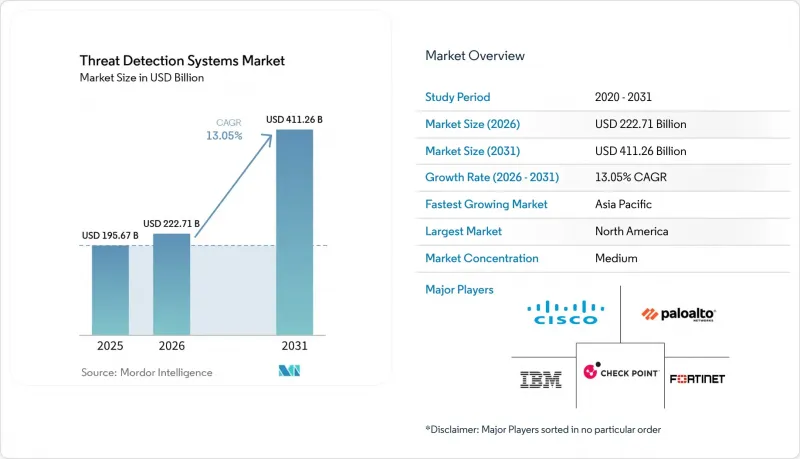

Mordor Intelligence에 의하면, 위협 감지 시스템 시장 규모는 2025년에 1,956억 7,000만 달러로 평가되었고, 2026년 2,227억 1,000만 달러로 추정되고, 2031년까지 4,112억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 13.05%를 나타낼 전망입니다.

본 보고서는 감지 기술별(네트워크 침입 감지 시스템, 호스트 기반 IDS, 통합 위협 관리, 위협 인텔리전스 플랫폼 등), 도입 형태별(온프레미스, 클라우드 기반 등), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 정부 및 국방 등), 구성 요소별(하드웨어, 소프트웨어 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 위협 감지 시스템 시장 동향 및 인사이트

제로데이 공격의 격화

2025년에는 그동안 알려지지 않았던 90건의 취약점이 악용되면서, 기업들은 시그니처 기반 도구에서 벗어나 횡방향 이동이나 데이터 스테이징과 같은 공격 후 전술을 감지하는 행동 분석 방식의 기법으로 전환할 수밖에 없었습니다. 공개에서 대규모 악용까지의 평균 기간이 5일로 단축되면서 대응을 위한 유예 기간이 줄어들자, 새로운 패턴을 자율적으로 학습하는 솔루션에 대한 수요가 높아졌습니다. 랜섬웨어 공격 그룹은 전체 사고의 38%에서 제로데이 취약점을 침입 경로로 이용했으며, 보고된 손실액은 125억 달러에 달했습니다. 그 결과, 조달 팀은 현재 알려진 지표와 일치하는 능력을 기준으로 플랫폼을 평가하는 것이 아니라, 알려지지 않은 기법을 감지하는 능력을 바탕으로 플랫폼을 평가하게 되었습니다.

중요 인프라에서의 OT와 IT의 급속한 융합

산업용 제어 시스템의 디지털화로 인해, 과거에는 물리적으로 분리되어 있던 경계가 사라지면서, 프로그래머블 로직 컨트롤러(PLC)와 예측 유지보수를 지원하는 클라우드 대시보드가 통합되고 있습니다. EU의 NIS2 지침 및 FERC 명령 918에 따르면, 영향이 적은 자산이라 하더라도 침입 감지가 의무화되어 있으며, 이에 따라 유틸리티자는 Modbus, DNP3, OPC-UA 트래픽을 분석할 수 있는 프로토콜 인식형 모니터링 시스템의 도입을 요구받고 있습니다. 아시아태평양에서는 각국 정적층 가공 거점을 보호하기 위한 대규모 시범 사업에 자금을 지원하고 있지만, 규정 준수 요건을 충족하는 솔루션을 도입한 공장은 30% 미만에 그치고 있습니다. 이러한 융합이 가속화됨에 따라, OT 환경에 특화된 시각화 솔루션을 제공하는 벤더가 유리한 고지를 차지할 것입니다.

SOC 팀의 높은 오감지 피로감

2025년, 분석가는 주당 4,484건의 경보를 처리했으며, 그중 67%를 오탐으로 판단해 제외했기 때문에 나머지 42%의 경보는 확인되지 않은 채로 남게 되었습니다. 번아웃 비율은 67%에 달하고, 이직 위험은 56%에 이르러 인건비 증가와 조직 지식의 손실을 초래하고 있습니다. 조직은 SOC 가동 시간의 약 4분의 1을 무해한 노이즈에 소비하고 있으며, 복잡한 하이브리드 환경이 튜닝 문제를 더욱 심각하게 만들고 있습니다. 검토 기간을 연장하고 ID, 엔드포인트, 네트워크의 이상 징후를 상호 연관하여 분석하는 플랫폼은 오탐을 79% 줄였으며, 알림의 품질은 구매 시 가장 시급한 선정 기준이 되고 있습니다.

부문별 분석

행동 분석은 연평균 성장률(CAGR) 13.74%를 기록하며 위협 감지 시스템 시장 전체를 상회했습니다. SIEM은 2025년 매출의 34.74%를 차지했으나, 현재 그 우위는 감지 정확도를 78-85%에서 95-98%로 끌어올리는 내장형 머신러닝 모듈에 달려 있습니다. 포춘 500대 기업의 89%가 기준선 설정 도구를 도입하고 있는 것으로 나타나, 행동 분석 시장의 급속한 성장이 예상됩니다. 한편, 패킷 수준 검사에는 여전히 네트워크 침입 감지가 필수적이며, 올인원형 스택을 필요로 하는 중견 기업들 사이에서는 통합 위협 관리가 선호되고 있습니다. 신흥 데셉션 및 샌드박스 기술은 위협 감지 시스템 시장에서 아직 규모는 작지만 꾸준히 시장 점유율을 확대되고 있습니다.

위협 인텔리전스 플랫폼에 대한 수요가 증가하고 있으며, 주요 정보 공유 센터의 85%가 현재 주요 플랫폼에서 STIX 2.1 지표 교환을 자동화하고 있습니다. 실시간 피드와 내부 텔레메트리 데이터를 통합하는 벤더는 신뢰할 수 있는 경보를 제공함으로써 트리아지 업무의 부담을 줄여주고 있습니다. SIEM 데이터 레이크가 확대되는 가운데, 구매자들은 데이터 수집 비용, 저장 정책, 그리고 AI의 설명 가능성을 면밀히 검토하고 있습니다. 경쟁의 초점은 단순한 로그 집계에서 심층 분석으로 이동하고 있으며, 이는 시장 전반에 걸쳐 고도화된 행동 분석 엔진의 꾸준한 성장을 뒷받침하고 있습니다.

중요 인프라 사업자와 정부 기관이 기밀성이 높은 로그를 온프레미스에 계속 보관하고 있기 때문에 2025년 매출의 51.19%는 여전히 온프레미스 방식이 차지했습니다. 그러나 연평균 성장률(CAGR) 13.64%로 성장하고 있는 클라우드 모델은 급증하는 워크로드에 대응할 수 있는 유연한 컴퓨팅 능력과 어플라이언스의 처리 능력을 뛰어넘는 고도의 분석 기능을 제공함으로써 그 격차를 점차 좁혀가고 있습니다. 2026년에는 유틸리티 사업자가 온사이트 운영 텔레메트리 데이터를 유지하면서 ID 로그를 하이퍼스케일 분석 환경으로 전송하게 됨에 따라, 위협 감지 시스템 시장 점유율은 하이브리드형으로 기울었습니다. 하이브리드 웹 애플리케이션 방화벽 등 두 영역에서 정책을 동기화하는 솔루션은 주권 관련 규정을 준수하면서도 클라우드 네이티브의 효율성을 활용하고 있습니다.

하이브리드 도입을 가로막는 7가지 과제에는 ID 불일치, 섀도 IT, 규정 준수 위반 등이 포함됩니다. 에이전트리스 커넥터를 통해 복잡성을 추상화하는 공급업체는 더 빠른 도입을 실현합니다. 예를 들어, 밀리초 단위의 제어 루프를 모니터링하는 공장 현장 등 지연 시간이 중요한 환경에서는 온프레미스 방식이 계속 유지될 것입니다. 그럼에도 불구하고, 가격 책정과 스토리지의 유연성이 규제상의 장벽을 상쇄하고 위협 감지 시스템 시장을 확대함에 따라, 거시적인 추세는 클라우드 확장을 뒷받침하고 있습니다. 가격 정책과 스토리지의 유연성이 규제상의 장벽을 상쇄하며, 밀리초 단위의 제어 루프를 모니터링하는 위협 감지 시스템 시장을 확대하고 있는 반면, 온프레미스 환경도 성장을 이어가고 있습니다. 온프레미스 환경은 버스트 워크로드에 대응하는 탄력적인 컴퓨팅을 제공함으로써 그 격차를 좁혀가고 있으며, 매출의 상당 부분을 차지하고 있습니다. 이는 중요 인프라 운영자나 정부 기관이 기밀성이 높은 로그를 온프레미스에 계속 보관하고 있기 때문입니다. 또한, 유틸리티자는 온프레미스 환경을 유지하면서 현장의 운영 텔레메트리 데이터를 계속 보관하고 있기 때문입니다.

지역별 분석

북미는 금융 허브, 클라우드 서비스 제공업체 및 주요 방위 기업들의 성장에 힘입어 2025년 매출의 38.91%를 차지했습니다. 2026년 1월에 발효된 대통령령 제918호는 침입 감지 대상을 영향이 적은 전력망 자산까지 확대하여 고객층을 넓혔습니다. CISA는 2026년 4월, 악용된 취약점 8건을 카탈로그에 추가하고 연방 기관 및 중요 인프라 사업자 전체에 패치 적용을 촉구했습니다. 미국 국방부는 2027년도 예산에서 사이버 공간 활동에 205억 달러를 편성하여 국내 수요를 뒷받침했습니다. 캐나다와 멕시코 역시 전력 부문의 규제와 국경을 초월한 데이터 공유 협정을 통해 유사한 길을 걷고 있으며, 시장 투자 기준을 높이고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 13.88%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 이 지역의 각국 정부는 수십억 달러 규모의 사이버 보안 예산을 발표했으며, 보안 책임자의 79%가 2026년에 위협 인텔리전스 관련 지출을 늘릴 계획입니다. 일본은 공급망의 회복탄력성을 강화하고 19만 명의 인력 부족을 해소하기 위한 사이버 인재 양성에 38억 달러를 배정했습니다. 중국, 인도, 한국, 호주에서는 국영 기업, 통신 사업자, 결제 시스템에 대한 보호 조치가 추진되고 있습니다. 이는 전 세계 국가 지원형 사이버 공격의 27%가 현재 이 지역을 표적으로 삼고 있기 때문입니다. 현지의 데이터 거주지 관련 법률이 아키텍처 선택에 영향을 미치며, 기업들이 국내 클라우드나 하이브리드 환경으로 전환하도록 이끌고 있습니다.

유럽에서는 '네트워크 및 정보 보안 지침 2'와 향후 시행될 '사이버 복원력 법'을 통해 기업의 의무를 강화하고 있으며, 2027년까지 연결된 기기에 양자 내성 암호화 기술을 도입해야 합니다. 중동 및 아프리카와 남미는 여전히 초기 단계에 있지만, 중요 인프라 보호 대책이 마련되고 클라우드 도입이 가속화되고 있어 유망한 시장으로 부상하고 있습니다. 데이터 주권과 관련된 제약 사항 및 기술 인력 부족으로 인해 단기적인 수익은 제한되고 있으나, 다자간 사이버 협정 및 보험료 인상으로 인해 구매자들의 시급성이 높아지면서 위협 감지 시스템 시장의 장기적인 잠재 시장 규모가 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the threat detection systems market size was valued at USD 195.67 billion in 2025 and estimated to grow from USD 222.71 billion in 2026 to reach USD 411.26 billion by 2031, at a CAGR of 13.05% during the forecast period (2026-2031).

This report is Segmented by Detection Technology (Network Intrusion Detection Systems, Host-Based IDS, Unified Threat Management, Threat Intelligence Platforms, and More), Deployment Mode (On-Premises, Cloud-Based, and More), End-User Industry (BFSI, Government and Defense, and More), Component (Hardware, Software, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Threat Detection Systems Market Trends and Insights

Escalating Zero-Day Exploits

Ninety previously unknown vulnerabilities were weaponized during 2025, forcing enterprises to pivot from signature-driven tools to behavioral methods that flag post-exploitation tactics such as lateral movement and data staging. The median lag between public disclosure and mass exploitation shrank to five days, compressing response windows and lifting demand for solutions that learn new patterns autonomously. Ransomware crews leveraged zero-day flaws as the entry vector in 38% of all incidents, accounting for USD 12.5 billion in reported losses. As a result, procurement teams now benchmark platforms on their ability to surface unknown techniques rather than match known indicators.

Rapid OT-IT Convergence in Critical Infrastructure

Digitization of industrial control systems is dissolving formerly air-gapped perimeters, merging programmable-logic controllers with cloud dashboards that support predictive maintenance. The EU's NIS2 directive and FERC Order 918 require intrusion detection even on low-impact assets, pushing utilities to deploy protocol-aware monitoring able to parse Modbus, DNP3, and OPC-UA traffic. In Asia-Pacific, governments are funding large-scale pilots to protect manufacturing hubs, yet fewer than 30% of plants have compliant solutions. Vendors offering tailored OT visibility stand to gain as convergence accelerates.

High False-Positive Fatigue among SOC Teams

Analysts processed 4,484 alerts per week in 2025, discarding 67% as false positives, which left 42% of remaining alerts unreviewed. Burnout reached 67% and churn risk hit 56%, inflating labor costs and eroding institutional knowledge. Organizations lose roughly one-quarter of SOC hours to benign noise, and complex hybrid environments exacerbate tuning challenges. Platforms that extend look-back periods and correlate identity, endpoint, and network anomalies have trimmed false positives by 79%, making alert quality an urgent buying criterion.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Cloud-Native Detection Stacks

- Proliferation of LLM-Generated Malware Variants

- Shortage of Threat-Hunting Talent Pool

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Behavioral analytics posted a 13.74% CAGR, outpacing the overall threat detection systems market. SIEM retained 34.74% revenue in 2025, but its dominance now hinges on embedded machine learning modules that raise detection accuracy from 78-85% to 95-98%. The market for behavioral analytics is projected to grow sharply, as 89% of Fortune 500 companies have adopted baselining tools. Meanwhile, network intrusion detection remains essential for packet-level inspection, and unified threat management appeals to midsize firms that seek an all-in-one stack. Emerging deception and sandbox techniques account for a modest yet growing slice of the threat detection systems market.

Demand for threat intelligence platforms has intensified; 85% of major information-sharing centers now automate STIX 2.1 indicator exchanges on one leading platform. Vendors that fuse real-time feeds with internal telemetry deliver higher-confidence alerts that reduce triage burden. As SIEM data lakes swell, buyers scrutinize ingestion pricing, retention policies, and AI explainability. The competitive focus is shifting toward analytics depth rather than simple log aggregation, underpinning the steady growth of advanced behavior engines across the market.

On-premises options still accounted for 51.19% of 2025 revenue, as critical infrastructure operators and sovereign entities continue to keep sensitive logs on-premises. Yet cloud models, growing at a 13.64% CAGR, are closing the gap by offering elastic compute for bursty workloads and advanced analytics that exceed appliance capacity. The threat detection systems market share tilted toward hybrid in 2026, as utilities retained on-site operational telemetry while shipping identity logs to hyperscale analytics. Solutions that synchronize policies across both realms, such as hybrid web application firewalls, satisfy sovereignty rules while tapping cloud-native efficiencies.

Seven pain points hinder hybrid rollouts, including misaligned identities, shadow IT, and compliance drift. Providers that abstract complexity through agentless connectors win faster adoption. In latency-critical setups, for example, factory floors that monitor millisecond control loops, on-prem will persist. Still, macro trends favor cloud expansion, as pricing and storage flexibility offset regulatory hurdles, broadening the market for threat detection systems. As pricing and storage flexibility offset regulatory hurdles, broadening the market for threat detection systems that monitor millisecond control loops, on-premise growing, are closing the gap by offering elastic compute for burstworkloads, accounting for a major share of revenue because critical infrastructure operators and sovereign entities keep sensitive logs on-premises, as utilities retain on-site operational telemetry while shipping on-premises.

Geography Analysis

North America accounted for 38.91% of 2025 revenue, driven by financial hubs, cloud service providers, and defense primes. Order 918, effective January 2026, extends intrusion detection to low-impact grid assets, broadening the customer pool. CISA added eight exploited vulnerabilities to its catalog in April 2026, prompting patching across federal agencies and critical infrastructure operators. The United States Department of Defense earmarked USD 20.5 billion for cyberspace activities in its fiscal 2027 budget, reinforcing domestic demand. Canada and Mexico mirror this trajectory through power-sector regulations and cross-border data-sharing accords that raise the baseline for investment in the market.

Asia-Pacific is the fastest-growing region at a 13.88% CAGR. Governments there unveiled multibillion-dollar cyber budgets, and 79% of security leaders plan to increase threat intelligence spending in 2026. Japan allocated USD 3.8 billion to bolster supply-chain resilience and train cyber talent to address a 190,000-person shortfall. China, India, South Korea, and Australia are safeguarding state-run enterprises, telcos, and payment systems as 27% of global state-backed campaigns now target the region. Local data-residency laws shape architecture choices, nudging firms toward in-country clouds or hybrid builds.

Europe tightens corporate obligations through the Network and Information Security Directive 2 and the forthcoming Cyber Resilience Act, which will require quantum-safe cryptography in connected devices by 2027. Middle East, Africa, and South America remain early-stage yet promising, as critical infrastructure protections emerge and cloud adoption accelerates. Data-sovereignty limits and skills gaps temper near-term revenue, but multilateral cyber accords and rising insurance premiums are increasing buyer urgency, expanding the long-run addressable share of the threat detection systems market.

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- Trellix

- IBM Corporation

- Rapid7, Inc.

- Splunk Inc.

- LogRhythm, Inc.

- Darktrace plc

- CrowdStrike Holdings, Inc.

- Cynet Security Ltd.

- ExtraHop Networks, Inc.

- Vectra AI, Inc.

- AT&T Cybersecurity

- F-Secure Oyj

- RSA Security LLC

- Sophos Ltd.

- Elastic N.V.

- Securonix, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Zero-Day Exploits

- 4.2.2 Rapid OT-IT Convergence in Critical Infrastructure

- 4.2.3 Shift to Cloud-Native Detection Stacks

- 4.2.4 Proliferation of LLM-Generated Malware Variants

- 4.2.5 Mandatory Quantum-Readiness Audits in Supply Chains

- 4.2.6 6G-Enabled Micro-Segmentation of Critical Assets

- 4.3 Market Restraints

- 4.3.1 High False-Positive Fatigue among SOC Teams

- 4.3.2 Shortage of Threat-Hunting Talent Pool

- 4.3.3 Legacy System Integration Complexity

- 4.3.4 Data-Sovereignty Restrictions on Telemetry Sharing

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Detection Technology

- 5.1.1 Network Intrusion Detection Systems (NIDS)

- 5.1.2 Host-Based IDS (HIDS)

- 5.1.3 Security Information and Event Management (SIEM)

- 5.1.4 Unified Threat Management (UTM)

- 5.1.5 Threat Intelligence Platforms

- 5.1.6 Behavior Analytics

- 5.1.7 Other Detection Technologies

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud-Based

- 5.2.3 Hybrid

- 5.3 By End-User Industry

- 5.3.1 Banking, Financial Services and Insurance (BFSI)

- 5.3.2 Government and Defense

- 5.3.3 Healthcare

- 5.3.4 IT and Telecom

- 5.3.5 Energy and Utilities

- 5.3.6 Manufacturing

- 5.3.7 Retail

- 5.3.8 Transportation and Logistics

- 5.3.9 Other End-User Industries

- 5.4 By Component

- 5.4.1 Hardware

- 5.4.2 Software

- 5.4.3 Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Palo Alto Networks, Inc.

- 6.4.3 Fortinet, Inc.

- 6.4.4 Check Point Software Technologies Ltd.

- 6.4.5 Trend Micro Incorporated

- 6.4.6 Trellix

- 6.4.7 IBM Corporation

- 6.4.8 Rapid7, Inc.

- 6.4.9 Splunk Inc.

- 6.4.10 LogRhythm, Inc.

- 6.4.11 Darktrace plc

- 6.4.12 CrowdStrike Holdings, Inc.

- 6.4.13 Cynet Security Ltd.

- 6.4.14 ExtraHop Networks, Inc.

- 6.4.15 Vectra AI, Inc.

- 6.4.16 AT&T Cybersecurity

- 6.4.17 F-Secure Oyj

- 6.4.18 RSA Security LLC

- 6.4.19 Sophos Ltd.

- 6.4.20 Elastic N.V.

- 6.4.21 Securonix, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment