|

시장보고서

상품코드

2062460

차량내 네트워킹 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)In-Vehicle Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

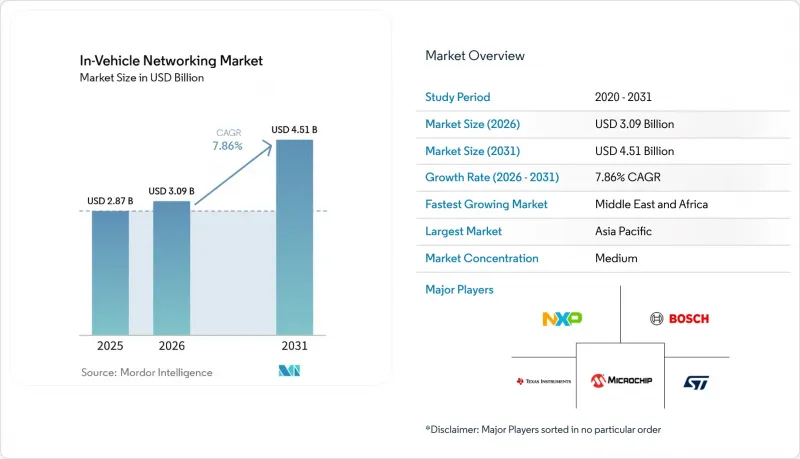

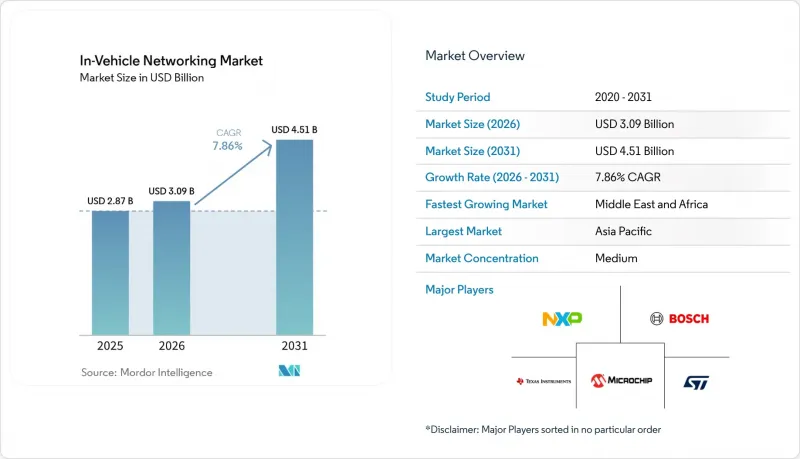

Mordor Intelligence에 의하면, 차량내 네트워킹 시장 규모는 2025년에 28억 7,000만 달러로 평가되었습니다. 2026년 30억 9,000만 달러에서 2031년까지 45억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.86%를 나타낼 전망입니다.

본 보고서는 프로토콜/기술(로컬 인터커넥트 네트워킹, FlexRay 등), 차종(승용차, 소형 상용차 등), 용도(파워트레인 및 섀시 제어, 안전 및 ADAS, 인포테인먼트 및 텔레매틱스 등), 구성 요소(트랜시버, 컨트롤러 및 게이트웨이 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 차량내 네트워킹 시장 동향과 인사이트

차량의 전동화와 증가하는 ADAS 대역폭 수요

배터리식 전기차 및 플러그인 하이브리드차의 플랫폼에는 내연기관 차량에 비해 최대 40% 더 많은 센서가 탑재되어 있으며, 시간당 수 테라바이트의 원시 데이터를 생성하고 있습니다. 기존의 5Mbps CAN-FD 링크로는 이 데이터 양을 효율적으로 처리할 수 없기 때문에 센서 퓨전의 백홀로 100BASE-T1 및 1000BASE-T1 이더넷이 널리 도입되고 있습니다. 현재 마이크로컨트롤러 제조업체들은 에지 노드에 10BASE-T1S 저속 이더넷을 통합하고 있으며, 이를 통해 저가의 온도 및 압력 센서가 존 게이트웨이에 데이터를 전송할 수 있게 되고, 존 게이트웨이는 집계된 트래픽을 기가비트 트렁크로 업링크합니다. 또한, 집중형 아키텍처는 배선 길이를 대폭 단축하여, 고에너지 밀도 배터리 팩의 주행 거리 향상에 기여합니다. 지각 소프트웨어의 무선 업데이트는 기기당 10기가바이트를 초과하는 경우가 있으며, 이러한 부하를 처리할 수 있는 것은 5G나 위성 오프로드와 결합된 기가비트 이더넷뿐입니다. 중국의 GB/T 32960 실시간 텔레매틱스 규격은 업링크 수요를 더욱 촉진하고, 이더넷 도입을 뒷받침하고 있습니다.

OEM을 통한 도메인형에서 존형 E 및 E 아키텍처로의 전환

기존의 도메인 구성에서는 수 킬로미터에 달하는 배선 하네스와 최대 100개의 컨트롤러가 필요했습니다. 존형 토폴로지에서는 연산 처리를 물리적 부하 근처에 배치된 3-5개의 리저널 게이트웨이로 이전함으로써 케이블 무게를 최대 30% 줄이고, 도메인 간 홉을 제거하여 지연을 줄입니다. 초기 실증 사례로는 폭스바겐의 ‘중국 전자 아키텍처’를 들 수 있습니다. 이를 통해 컨트롤러 수를 30% 줄이고, 소프트웨어 출시 주기를 절반으로 단축했습니다. 존 게이트웨이는 LIN, CAN-FD, FlexRay, 이더넷을 브리지하는 동시에 ISO 21434의 사이버 보안 요구 사항 및 AUTOSAR Adaptive와의 호환성을 충족해야 합니다. 따라서 16개 이상의 CAN 채널을 통합하고, TSN 스위치 및 하드웨어 보안 모듈을 내장한 반도체에 대한 수요가 증가하고 있습니다.

하네스의 중량 및 비용 증가 대 BOM 목표

배터리식 전기차 모델의 경우, 와이어 하네스의 무게가 최대 80Kg에 달하고, 주행 거리 감소의 원인이 되고 있습니다. 2026년 초, 구리의 평균 가격은 톤당 1만 700달러, 은은 온스당 99달러까지 상승하여 케이블 원가를 5분의 1 가까이 끌어올렸습니다. 400V 아키텍처에서 800V 아키텍처로 전환함에 따라 도체의 단면적은 절반으로 줄어들지만, 정격이 높은 커넥터가 필요하게 되어 그만큼의 비용 절감 효과는 상쇄되고 맙니다. 존 통합을 통해 케이블 길이는 약 4분의 1로 단축되지만, 추가적인 게이트웨이용 반도체가 필요해져 컨트롤러 비용을 3분의 1 이상 증가시키게 됩니다. 생산 연계형 인센티브 제도 하에서 현지 생산을 진행하는 인도공급업체들은 특히 엄격한 부품 원가(BOM) 제한에 직면해 있습니다.

부문별 분석

CAN 및 CAN-FD는 저비용이라는 장점 외에도 파워트레인 및 차체 제어 루프에서 널리 사용됨에 따라, 2025년에도 차량내 네트워킹 시장 점유율 36.89%를 유지했습니다. FlexRay는 틈새 시장 제품이지만, 스티어 바이 와이어 및 Brake-by-wire 플랫폼에서 그 결정론적 듀얼 채널 중복성이 필수적이기 때문에 연평균 성장률(CAGR) 7.93%가 예상됩니다. 현재 자동차용 이더넷은 10메가비트에서 10기가비트/초까지 확장 가능하며, 이를 통해 인포테인먼트, ADAS, 중앙 집중형 컴퓨팅이 단일 백본 상에서 공존할 수 있게 되었습니다. 이러한 변화는 IEEE 802.1DG-2025에 의해 공식적으로 규정되어 있습니다. LIN은 시트, 미러, 조명 기능을 위한 20킬로비트 미만의 주력 규격으로 계속해서 사용되고 있습니다. MOST는 150메가비트라는 상한선이 4K 스트리밍 수요를 따라가지 못하기 때문에 계속해서 감소 추세를 보이고 있습니다.

CAN-FD, LIN, FlexRay를 통합한 멀티프로토콜 마이크로컨트롤러는 존 게이트웨이가 차체 기능을 흡수함에 따라 기판 수를 줄이고 검증 기간을 단축합니다. 신규 등장한 CAN-XL은 프레임당 페이로드를 2,048바이트로 확대하여, 기존 제어 루프와 이더넷 터널 간의 가교 역할을 확고히 하고 있습니다. MACsec 및 1588 타임스탬프 기능을 내장한 보안형 1000BASE-T1 PHY는 디스크리트 구현에 비해 기판 면적을 최대 15% 줄여줍니다. 따라서 포트당 평균 가격이 상승함에 따라, 이더넷 PHY와 관련된 차량내 네트워킹 시장 규모는 노드 수보다 더 빠르게 성장하게 될 것입니다.

2025년에는 승용차가 총 매출의 55.34%를 차지했으며, 연간 생산 대수는 약 7,000만 대에 달했습니다. 건설, 농업, 광업용 기계의 생산 대수는 이보다 적었으나, 연평균 성장률(CAGR)은 8.23%를 나타낼 것으로 예측됩니다. 이러한 성장은 이더넷 게이트웨이가 필요한 예측 유지보수 및 원격 진단을 원하는 차량 소유주가 증가하고 있기 때문입니다. 이러한 기계 분야에서 첨단 텔레매틱스 시스템 및 IoT 통합의 도입 확대 역시 이러한 추세를 더욱 뒷받침하고 있습니다.

소형 상용차는 승용차와의 부품 공통화의 이점을 누리고 있어, 최소한의 추가 비용으로 기가비트 백본을 계승할 수 있습니다. 대형 트럭은 확실성이 보장된 이더넷을 필수로 하는 새로운 자동 조향 규정을 충족해야 합니다. 오프로드 차량 설계자들은 장비가 먼지, 진동 및 물 분사에 견딜 수 있도록 IP69K 규격을 준수하는 CAN-to-Ethernet 브리지를 채택하고 있습니다. 이러한 동향에 따라 특수 차량 부문의 차량 내 네트워킹 시장 규모는 시장 전체에 비해 더욱 가파른 성장 곡선을 그리고 있습니다.

지역별 분석

아시아태평양은 중국의 승용차 생산 대수 2,700만 대와, NEV(신에너지차)의 현지 조달률 75%를 목표로 하는 인도가 새로 발표한 30만 대 규모의 공장에 힘입어, 2025년 매출의 43.78%를 차지했습니다. GB/T 32960에 기반한 플랫폼 규제로 인해 중국의 모든 자동차 제조업체들은 5G 업링크가 통합된 이더넷 게이트웨이를 도입해야 하는 상황에 놓여 있으며, 이로 인해 반도체 출하량이 증가하고 있습니다. 인도의 생산 연계형 인센티브는 네트워킹 부품 공급업체들을 현지 클러스터로 유치함으로써 관세 위험을 줄이고, 지역 차량내 네트워킹 시장을 활성화하고 있습니다. 일본과 한국은 프리미엄 ADAS 기능에 주력하고 있으며, 이로 인해 TSN 하드웨어에 대한 조기 수요가 발생하고 있습니다.

북미는 2025년 지출의 약 4분의 1을 차지했으며, 이는 미국 내 1,100만 대의 소형 트럭 및 SUV 생산과 멕시코의 수출 지향적 조립 생산에 힘입은 결과입니다. 차량 라인 유지 관리 및 사이버 보안 대책을 적용한 무선 업데이트에 관한 규제의 발전이 이더넷의 보급을 뒷받침하고 있습니다. 실리콘밸리의 한 스타트업이 제공하는 SDV 미들웨어는 디트로이트 지역 자동차 제조업체들의 통합 기간을 단축하고, 게이트웨이 및 중앙 집중식 컴퓨팅에 대한 건전한 투자를 뒷받침하고 있습니다. 미국의 인플레이션 억제법은 국내 배터리 및 전자 부품 공급을 촉진하고, 간접적으로 차량내 네트워킹 시장을 뒷받침하는 보조금을 제공합니다.

유럽은 존형 토폴로지, 집중형 ADAS 및 ISO 21434 인증 분야에서 선도적인 위치를 차지하고 있는 고급차 및 고성능차 브랜드를 바탕으로 20-22%의 시장 점유율을 확보했습니다. 유엔 유럽경제위원회(UN ECE)의 규제 제정을 통해 회원국 간 안전 및 사이버 보안 관련 기한이 통일됨에 따라, 이더넷 및 FlexRay 업그레이드를 위한 예측 가능한 도입 일정이 촉진되고 있습니다. 동유럽의 공장들은 저렴한 인건비를 활용해 와이어 하네스와 광섬유 링크를 조립함으로써 지역적 비용 경쟁력을 확보하고 있습니다. 중동 및 아프리카의 현재 시장 점유율은 한 자릿수 중반에 그치고 있지만, 스마트시티 메가 프로젝트가 차량과 인프라 간의 연동을 의무화함에 따라 2031년까지 연평균 성장률(CAGR) 8.94%를 나타낼 것으로 전망됩니다. 남미는 현지에서 생산된 CAN-FD 및 이더넷 부품에 대한 수입 관세를 인하하는 메르코수르(Mercosur) 규정의 혜택을 받고 있지만, 거시경제의 변동으로 인해 절대적인 시장 규모 성장은 제한되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the in-vehicle networking market size was valued at USD 2.87 billion in 2025 and estimated to grow from USD 3.09 billion in 2026 to reach USD 4.51 billion by 2031, at a CAGR of 7.86% during the forecast period (2026-2031).

This report is Segmented by Protocol/Technology (Local Interconnect Network, Flexray, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Application (Powertrain and Chassis Control, Safety and ADAS, Infotainment and Telematics, and More), Component (Transceivers, Controllers and Gateways, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global In-Vehicle Networking Market Trends and Insights

Vehicle Electrification and Escalating ADAS Bandwidth Needs

Battery-electric and plug-in hybrid platforms embed up to 40% more sensors than internal-combustion counterparts, producing several terabytes of raw data every hour. Legacy five-megabit-per-second CAN-FD links cannot move this volume efficiently, prompting widespread deployment of 100BASE-T1 and 1000BASE-T1 Ethernet for sensor fusion backhaul. Microcontroller vendors now integrate 10BASE-T1S low-speed Ethernet into edge nodes so inexpensive temperature and pressure sensors can feed zonal gateways, which then uplink aggregated traffic to gigabit trunks. Centralized architectures also slash wiring length, driving range gains for energy-dense battery packs. Over-the-air updates for perception software can exceed ten gigabytes per vehicle, a load that only gigabit Ethernet paired with 5G or satellite offload can manage. China's GB/T 32960 real-time telematics rule further boosts uplink demand, reinforcing Ethernet adoption.

OEM Migration from Domain to Zonal E and E Architecture

Traditional domain layouts required kilometers of harnesses and up to 100 controllers. Zonal topologies reposition compute into three to five regional gateways located near the physical loads, trimming cable weight by as much as 30% and reducing latency by eliminating inter-domain hops. Early production proof came from Volkswagen's China Electronic Architecture, which cut its controller count by 30% and halved software release cycles. Zonal gateways must bridge LIN, CAN-FD, FlexRay, and Ethernet while satisfying ISO 21434 cybersecurity and AUTOSAR Adaptive compatibility. Silicon that unifies 16 or more CAN channels with integrated TSN switches and hardware security modules is therefore in high demand.

Harness Weight and Cost Inflation Versus BOM Targets

Wiring looms weigh up to 80 kilograms in battery-electric models, adding drag on driving range. Early-2026 copper averaged USD 10,700 per tonne, and silver rose to USD 99 per ounce, inflating cable bills by nearly one-fifth. Moving from 400-volt to 800-volt architectures halves the conductor cross-section but requires higher-rated connectors that claw back some savings. Zonal integration cuts cable length by roughly one-quarter, yet it demands additional gateway silicon that pushes controller costs up more than one-third. Indian suppliers localizing under production-linked incentives face especially tight bill-of-materials limits.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Time-Sensitive Networking in Automotive Ethernet

- Infotainment and Telematics Feature Proliferation

- Cyber-Security Certification Complexity for Multi-Protocol Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CAN and CAN-FD maintained 36.89% of the in-vehicle networking market share in 2025 thanks to their low cost and entrenched use in powertrain and body-control loops. FlexRay, though a niche, is positioned for a 7.93% CAGR because steer-by-wire and brake-by-wire platforms need its deterministic dual-channel redundancy. Automotive Ethernet now scales from 10 megabits to 10 gigabits per second, so infotainment, ADAS, and centralized compute can coexist on one backbone, a shift formalized by IEEE 802.1DG-2025. LIN remains the sub-20-kilobit workhorse for seat, mirror, and lighting functions. MOST continues to decline as its 150-megabit ceiling cannot keep pace with 4K streaming demands.

Multi-protocol microcontrollers that integrate CAN-FD, LIN, and FlexRay reduce board count and shorten validation time as zonal gateways absorb body functions. Emerging CAN-XL raises single-frame payloads to 2,048 bytes, positioning itself as the bridge between legacy control loops and Ethernet tunnels. Secure 1000BASE-T1 PHYs with built-in MACsec and 1588 timestamping now reduce board area by up to 15% compared with discrete implementations. The in-vehicle networking market size attached to Ethernet PHYs will therefore outgrow node counts as the average price per port climbs.

In 2025, passenger cars accounted for 55.34% of total revenue, translating to an annual output of approximately 70 million units. While construction, agriculture, and mining machinery saw lower volumes, they are projected to experience a CAGR of 8.23%. This growth is driven by fleet owners increasingly seeking predictive maintenance and remote diagnostics, both of which necessitate Ethernet gateways. The rising adoption of advanced telematics systems and IoT integration in these machinery segments further supports this trend.

Light commercial vehicles benefit from passenger-car component commonality, allowing them to inherit gigabit backbones at minimal incremental cost. Heavy trucks must meet new automated steering regulations that make deterministic Ethernet mandatory. Off-highway designers adopt IP69K-rated CAN-to-Ethernet bridges so equipment can survive dust, vibration, and water jets. These trends keep the in-vehicle networking market size in the specialty-vehicle segment on a steeper slope than the overall base.

Geography Analysis

Asia-Pacific retained 43.78% of 2025 revenue, anchored by China's 27 million-unit passenger-car output and India's newly announced 300,000-unit plant that targets 75% NEV content localization. Platform rules under GB/T 32960 push every Chinese OEM toward Ethernet gateways with integrated 5G uplink, accelerating silicon volume. India's production-linked incentives are drawing network-component suppliers into local clusters, lowering tariff exposure and bolstering the regional in-vehicle networking market. Japan and South Korea concentrate on premium ADAS features, creating early demand for TSN hardware.

North America held roughly one-quarter of 2025 spending, supported by 11 million light-truck and SUV builds in the United States and export-oriented assembly in Mexico. Regulatory momentum for automated lane keeping and over-the-air cyber-secure updates sustains Ethernet penetration. Silicon Valley start-ups provide SDV middleware that reduces integration time for Detroit-area OEMs, supporting healthy investment in gateways and centralized compute. The United States Inflation Reduction Act spurs domestic battery and electronics supply, giving subsidies that indirectly boost the in-vehicle networking market.

Europe achieved a 20-22% share on the back of luxury and performance brands that lead in zonal topologies, centralized ADAS, and ISO 21434 certification. UN ECE rulemaking synchronizes safety and cybersecurity deadlines across member states, stimulating predictable rollout schedules for Ethernet and FlexRay upgrades. Eastern European plants leverage lower wage costs to assemble wiring harnesses and optical-fiber links, ensuring regional cost competitiveness. Middle East and Africa, although only a mid-single-digit base today, is tracking toward an 8.94% CAGR through 2031 as smart-city megaprojects mandate vehicle-to-infrastructure connectivity. South America benefits from Mercosur rules that reduce import duties on localized CAN-FD and Ethernet components, but macro volatility tempers absolute market size growth.

- NXP Semiconductors N.V.

- Robert Bosch GmbH

- Texas Instruments Incorporated

- Microchip Technology Inc.

- STMicroelectronics N.V.

- Broadcom Inc.

- Marvell Technology, Inc.

- Infineon Technologies AG

- ON Semiconductor Corporation

- Renesas Electronics Corporation

- Analog Devices, Inc.

- Realtek Semiconductor Corp.

- Rohm Co., Ltd.

- Melexis N.V.

- ON Semiconductor Corporation

- Molex LLC

- TE Connectivity Ltd.

- Aptiv PLC

- Continental AG

- Marvell Technology, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Vehicle Electrification and Escalating ADAS Bandwidth Needs

- 4.2.2 Infotainment/Telematics Feature Proliferation

- 4.2.3 Regulatory Mandates for Advanced Safety Networks

- 4.2.4 OEM Migration from Domain to Zonal E/E Architecture

- 4.2.5 China's NEV Platform Standardisation Pressure

- 4.2.6 Adoption of Time-Sensitive Networking (TSN) in Automotive Ethernet

- 4.3 Market Restraints

- 4.3.1 Harness Weight and Cost Inflation Versus BOM Targets

- 4.3.2 Cyber-Security Certification Complexity for Multi-Protocol Stacks

- 4.3.3 Thermal/EMC Integrity Limits at >=1 Gbps

- 4.3.4 OEM-Specific Proprietary Network Stacks Hindering Interoperability

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Protocol / Technology

- 5.1.1 Local Interconnect Network (LIN)

- 5.1.2 Controller Area Network (CAN and CAN-FD)

- 5.1.3 FlexRay

- 5.1.4 Automotive Ethernet (10 Mbps - 10 Gbps)

- 5.1.5 Media Oriented Systems Transport (MOST)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Heavy Commercial Vehicles

- 5.2.4 Off-Highway and Specialized Vehicles

- 5.3 By Application

- 5.3.1 Powertrain and Chassis Control

- 5.3.2 Safety and ADAS

- 5.3.3 Infotainment and Telematics

- 5.3.4 Body Control and Comfort

- 5.3.5 Autonomous Driving Compute Domains

- 5.4 By Component

- 5.4.1 Transceivers

- 5.4.2 Controllers and Gateways

- 5.4.3 Switches and Routers

- 5.4.4 Cabling and Connectors

- 5.4.5 Network ICs and PHYs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NXP Semiconductors N.V.

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Texas Instruments Incorporated

- 6.4.4 Microchip Technology Inc.

- 6.4.5 STMicroelectronics N.V.

- 6.4.6 Broadcom Inc.

- 6.4.7 Marvell Technology, Inc.

- 6.4.8 Infineon Technologies AG

- 6.4.9 ON Semiconductor Corporation

- 6.4.10 Renesas Electronics Corporation

- 6.4.11 Analog Devices, Inc.

- 6.4.12 Realtek Semiconductor Corp.

- 6.4.13 Rohm Co., Ltd.

- 6.4.14 Melexis N.V.

- 6.4.15 ON Semiconductor Corporation

- 6.4.16 Molex LLC

- 6.4.17 TE Connectivity Ltd.

- 6.4.18 Aptiv PLC

- 6.4.19 Continental AG

- 6.4.20 Marvell Technology, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment