|

시장보고서

상품코드

2062476

차세대 에너지 저장 시스템 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Next-Generation Energy Storage Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

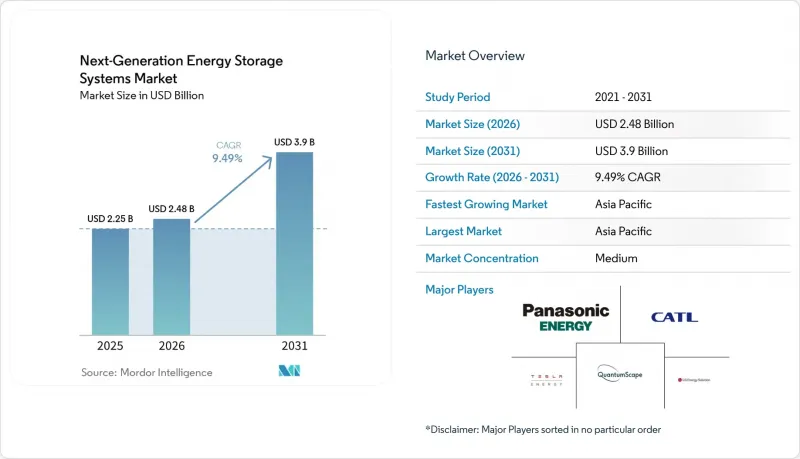

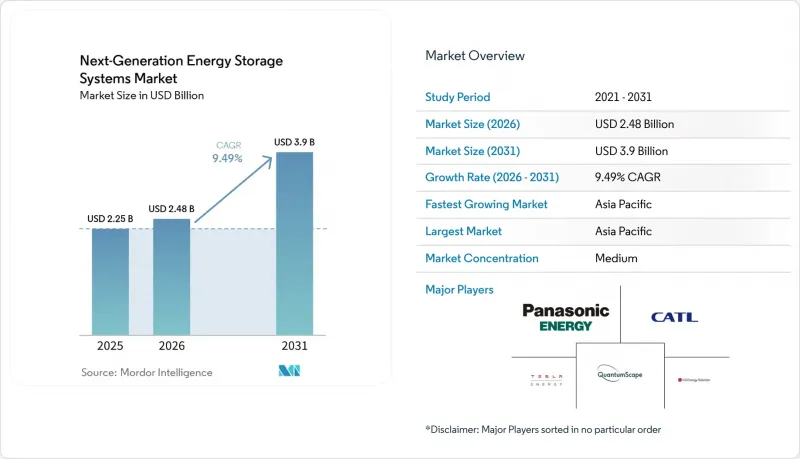

Mordor Intelligence에 의하면, 차세대 에너지 저장 시스템 시장 규모는 2025년 22억 5,000만 달러로 평가되었습니다. 2026년 24억 8,000만 달러에서 2031년까지 39억 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 9.49%를 나타낼 것으로 예측됩니다.

본 보고서는 기술별(리튬-황 전지, 전고체 전지, 흐름 전지, 금속-공기 전지, 기계식 및 기타 첨단 에너지 저장 기술), 용도별(계통 연계용 에너지 저장, 가정용 전자기기 등), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 차세대 에너지 저장 시스템 시장 동향 및 인사이트

전 세계 자동차 제조업체들의 전기차 생산 목표 급증

각 제조업체들은 고에너지 밀도의 화학계 배터리 개발 주기를 단축하고 있습니다. BYD는 2027년에 황화물계 고체 배터리의 시범 생산을 시작하고, 2030년까지 약 400 Wh/kg의 양산을 목표로 하고 있으며, 이는 해당 회사의 ‘Blade Battery’ 플랫폼에 비해 60% 향상된 수치입니다. CATL은 500 Wh/kg의 고밀도 배터리를 시범 생산 중이며, 2027년부터 전기 항공기 기단에 도입될 가능성이 있습니다. 도요타는 10분 만에 충전이 가능하며 주행 거리 745마일인 전고체 배터리 팩의 출시 시기를 2027년에서 2028년으로 예상하고 있습니다. 미국 에너지부가 2024년도에 지급한 1,600만 달러의 보조금 등 공공 자금 지원은 시범 생산 라인의 위험을 줄이고, 정책과 자동차 제조업체의 로드맵을 조화롭게 맞춥니다. 이러한 움직임은 종합적으로 볼 때, 고체 전지가 액체 전해질 리튬 이온 기술을 대체하기 위해 필요한 ‘kWh당 100달러’라는 비용 장벽을 넘어야 할 시기를 앞당기는 것입니다.

송전 사업자에 대한 재생에너지 통합 의무화

개정된 도매시장 규정에 따르면, 축전 설비는 보조 서비스가 아닌 용량으로 취급되게 되었습니다. FERC 명령 제841호 및 제2222호는 지역 시장에 대해 배터리가 전력, 용량 및 보조 서비스 경매에 참여할 수 있도록할 것을 의무화하고 있습니다. 뉴욕주, 매사추세츠주, 뉴저지주 등은 2030년까지 총 13GW를 도입하는 것을 목표로 하고 있으며, 장기 구매 계약을 강화하고 있습니다. 흐름형 배터리 공급업체들은 이 기회를 활용하여, ESS Tech는 27MWh 규모의 철-흐름형 배터리 유닛에 대해 미국 공군으로부터 990만 달러 규모의 수주를 따냈습니다. 한편, Form Energy는 100시간 동안 방전이 가능한 1,500MWh 규모의 철-공기 배터리 플랜트 건설에 착수했습니다. 이는 4시간밖에 지속되지 않는 리튬 이온 시스템을 뛰어넘는 성능입니다. NREL이 2035년까지 리튬이온 시스템의 비용을 1kWh당 243달러로 예측하고 있는 만큼, 가동 시간이 길어질수록 비용 격차는 줄어들고 있습니다.

고에너지 화학계 배터리의 안전성과 열폭주 위험

주목을 끄는 리콜 사태가 잇따르면서 보험료는 높은 수준을 유지하고 있습니다. 제너럴 모터스, 피스커, 메르세데스-벤츠, 리비안은 배터리 발화 우려로 인해 2024년에 총 12만 대 이상의 전기차를 리콜했습니다. UL 9540A 및 IEC 62619 규격은 시험 절차를 규정하고 있으나, 전고체 전지는 대규모 운용 실적이 부족하여 보험 인수 승인이 지연되고 있습니다. NFPA 855 설치 기준에 따라 보호 비용이 kWh당 20-30달러 증가하지만, 이는 초기 단계에 있는 화학 기업에게는 지나치게 큰 부담입니다. 리튬 금속 음극에서 발생하는 덴드라이트의 성장은 여전히 해결되지 않은 고장 모드이지만, 세라믹 분리막과 전해질 첨가제는 실험실 테스트에서 유망한 결과를 보여주고 있습니다. 실제 데이터가 축적되기 전까지는 구매자들은 검증되지 않은 화학 계열 제품을 꺼릴 것입니다.

부문별 분석

2025년 기준으로 고체 전지는 차세대 에너지 저장 시스템 시장 점유율의 51.6%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 9.9%를 나타낼 것으로 전망됩니다. 이는 고급 자동차 및 신흥 전기 항공기 프로그램에 대한 수요가 높음을 보여줍니다. 고체 배터리 기술을 기반으로 한 차세대 에너지 저장 시스템 시장 규모는 비용이 kWh당 100달러 미만으로 떨어지면 급속히 확대될 전망입니다. 많은 분석가들은 이러한 비용 평준화가 2028년에 달성될 것으로 예측했습니다. QuantumScape사의 산화물 전해질은 흑연 음극을 배제함으로써 재료 비용을 4분의 1로 절감하고, 체적 에너지 밀도를 향상시킵니다. 한편, Solid Power사의 황화물 계열 기술은 더 높은 이온 전도도를 실현하지만, 무수 환경에서 취급해야 합니다. 도요타, 삼성SDI, LG에너지솔루션은 모두 2027년부터 2029년 사이에 상용화를 목표로 하고 있으며, 기술이 본격적인 규모에 도달하기 훨씬 전부터 시장은 치열한 경쟁 구도가 될 전망입니다.

흐름 전지, 리튬-황 전지, 금속-공기 전지와 같은 화학계 전지들은 직접적인 경쟁 관계라기보다는 각각 전문적인 역할을 담당하고 있습니다. ESS Tech사의 철-유동 전지 플랫폼은 8-24시간 지속형 고정형 틈새 시장을 장악하고 있으며, Form Energy사의 100시간 지속형 철-공기 전지 시스템은 계절적 변동에 대응하는 새로운 분야를 개척하고 있습니다. 400 Wh/kg의 에너지 밀도로 주목받고 있는 리튬-황 전지는 항공우주 분야에서 큰 관심을 받고 있습니다. 예를 들어 에어버스는 Sion Power와 협력하여 실증용 셀 개발을 추진하고 있습니다. Zinc8과 같은 아연-공기 전지 공급업체들은 농촌 지역의 마이크로그리드를 대상으로 사이클 수가 적은 시스템을 포지셔닝하고 있습니다. Energy Vault의 기계식 중력 에너지 저장 시스템은 토지 가격이 저렴한 시장을 대상으로 초장주기 에너지 저장(LDES)을 목표로 하고 있습니다. 이러한 대체 기술 전반을 고려할 때, 고체 에너지 저장 기술이 양산을 주도하는 상황에서도 차세대 에너지 저장 시스템 시장은 기술적 다양성을 유지하게 될 것입니다.

지역별 분석

아시아태평양은 2025년 매출의 45.1%를 차지하며, 차세대 에너지 저장 시스템 시장 규모의 거의 절반을 차지했습니다. 해당 지역은 중국의 2026년 7월 고체 배터리 기준, 한국의 400억 달러 규모 ‘K-Battery’ 이니셔티브, 그리고 일본의 4680형 배터리 지속적인 확대에 힘입어 연평균 성장률(CAGR) 10.1%를 나타낼 것으로 전망됩니다. CATL과 BYD는 2030년까지 총 1.2TWh 이상의 생산 능력을 확보할 것으로 전망되며, 응축형 및 황화물계 화학 배터리의 시범 생산 라인은 2027년까지 양산 단계에 진입할 가능성이 있습니다. 서울에 본사를 둔 LG 에너지솔루션과 삼성SDI는 아시아의 규모와 서유럽와의 파트너십을 결합하여, 중국의 지배적 지위와 미국의 정책 인센티브 사이에서 공급 기반을 구축하고 있습니다.

북미 시장 점유율은 ‘인플레이션 억제법’ 제45X조를 배경으로 확대되고 있습니다. 해당 조항에 따르면, 국내 배터리 셀 생산에 대해 kWh당 35달러의 환급에 더해, 공장에 대한 30%의 투자 세액 공제가 적용됩니다. LG 에너지 솔루션의 55억 달러 규모 애리조나 복합 단지와 파나소닉의 캔자스주 확장 계획은 합쳐서 2026년까지 57GWh를 넘는 생산 능력을 갖출 것이라고 발표되었으며, 또한 포드·SK와 테슬라도 기가와트시 단위의 생산량을 추가할 전망입니다. 연방 에너지 시장 규제인 대통령령 제841호, 제2222호, 제901호는 배터리 시장 진입 조건을 통일하고 있으며, 각 주의 목표에 따라 2030년까지 13GW의 최소 수요 기준이 설정되어 있습니다. 이를 통해 자동차 업계 이외 수요처를 염두에 둔 개발자들에게는 미래 전망이 확보되어 있습니다.

유럽에서는 재활용 업체에 인센티브를 제공하고, 탄소 배출량이 많은 공급망에 벌금을 부과하는 등 규제 체계가 점차 강화되는 가운데 사업이 전개되고 있습니다. ‘배터리 규제’에 따른 탄소 발자국 표시 의무 및 재료 회수율 기준은 규정 준수 비용을 증가시켜 수직 통합형 제조업체에 유리하게 작용하고 있습니다. 노스볼트사의 2024년 사업 재편은 자금 조달의 어려움을 여실히 드러냈지만, 이 회사의 리튬 공장은 여전히 연간 60GWh의 생산 능력을 목표로 하고 있습니다. Automotive Cells Company는 2030년까지 총 120GWh 규모의 3개 기가팩토리 건설을 추진하고 있는 반면, 영국의 패러데이 연구소는 전고체 배터리 및 나트륨 이온 배터리의 연구 개발에 자금을 지원하고 있습니다. 그 밖의 지역에서는 리튬 자원이 풍부한 남미가 2020년대 중반 정제 개시를 목표로 하고 있으며, 중동의 개발업체들은 사막에서 재생에너지용 장주기 에너지 저장(LDES)을 검토하고 있지만, 2026년까지는 공급량이 아직 초기 단계에 머물러 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the next-generation energy storage systems market size is projected to expand from USD 2.25 billion in 2025 and USD 2.48 billion in 2026 to USD 3.9 billion by 2031, registering a CAGR of 9.49% between 2026 and 2031.

This report is Segmented by Technology (Lithium-Sulfur Batteries, Solid-State Batteries, Flow Batteries, Metal-Air Batteries, Mechanical and Other Advanced Storage), Application (Grid Storage, Consumer Electronics, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Next-Generation Energy Storage Systems Market Trends and Insights

Surging EV Production Targets by Global Automakers

Manufacturers are compressing development cycles for high-energy chemistries. BYD plans sulfide-based solid-state pilot output in 2027 and mass output by 2030 at roughly 400 Wh/kg, a 60% uplift on its Blade Battery platform. CATL is piloting 500 Wh/kg condensed batteries that could debut in electric aircraft fleets starting in 2027. Toyota maintains a 2027-2028 launch window for a 745-mile solid-state pack promising 10-minute charging. Supportive public funding, such as the U.S. Department of Energy's USD 16 million 2024 grant round, lowers pilot-line risk and aligns policy with automaker roadmaps. Collectively, these moves advance the timeline by which solid-state cells must cross the USD 100 per kWh cost threshold to displace liquid-electrolyte lithium-ion technology.

Renewable-Integration Mandates for Grid Operators

Re-written wholesale-market rules now treat storage as capacity, not an ancillary service. FERC Orders 841 and 2222 require regional markets to let batteries bid into energy, capacity, and ancillary-service auctions. States such as New York, Massachusetts, and New Jersey together target 13 GW of deployments by 2030, reinforcing long-duration purchase agreements. Flow-battery suppliers have exploited the opening: ESS Tech secured a USD 9.9 million U.S. Air Force award for 27 MWh iron-flow units, while Form Energy broke ground on a 1,500 MWh iron-air plant that can discharge for 100 hours, capabilities beyond four-hour lithium-ion systems. With NREL projecting lithium-ion system costs at USD 243 per kWh by 2035, the cost gap narrows as duration lengthens.

Safety & Thermal-Runaway Risks in High-Energy Chemistries

High-profile recalls keep insurance premiums elevated. General Motors, Fisker, Mercedes-Benz, and Rivian collectively recalled more than 120,000 EVs in 2024 over battery-fire concerns. UL 9540A and IEC 62619 standards provide test pathways, but solid-state cells lack large-sample operating histories, delaying underwriting approvals. NFPA 855 installation codes add USD 20-30 per kWh in protection costs that early-stage chemistries can ill afford. Dendrite growth in lithium-metal anodes remains an unresolved failure mode, although ceramic separators and electrolyte additives show promise in lab trials. Until field data accumulate, buyers will discount unproven chemistries.

Other drivers and restraints analyzed in the detailed report include:

- Rapid USD/kWh Cost Decline in Solid-State & Flow Chemistries

- Defense Demand for High-Energy Batteries for Unmanned Systems

- Critical-Metal Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid-state batteries represented 51.6% of the next-generation energy storage systems market share in 2025 and are forecast to post a 9.9% CAGR through 2031, highlighting their pull from premium automotive and emerging electric-aviation programs. The next-generation energy storage systems market size attached to solid-state chemistry is poised to expand rapidly once costs fall below USD 100 per kWh, a parity point most analysts peg for 2028. QuantumScape's oxide electrolyte, which eliminates the graphite anode, trims material cost by a quarter and improves volumetric density, while Solid Power's sulfide pathway delivers higher ionic conductivity but demands moisture-free handling. Toyota, Samsung SDI, and LG Energy Solution all target commercial releases between 2027 and 2029, ensuring a crowded field long before the technology reaches scale.

Flow, lithium-sulfur, and metal-air chemistries occupy specialist roles rather than direct competition. ESS Tech's iron-flow platform commands the 8-24-hour stationary niche, and Form Energy's 100-hour iron-air system is opening a seasonal-shift frontier. Lithium-sulfur, valued for its 400 Wh/kg density, draws aerospace interest; Airbus, for instance, collaborates with Sion Power on demonstration cells. Zinc-air suppliers such as Zinc8 position their low-cycle systems for rural micro-grids. Mechanical gravity storage from Energy Vault targets ultra-long durations in markets with cheap land. Collectively, these alternatives ensure the next-generation energy storage systems market remains technology-diverse even as solid-state leads volumes.

Geography Analysis

Asia-Pacific, holding 45.1% of the 2025 turnover, underpins almost half the next-generation energy storage systems market size. The region should grow at 10.1% CAGR thanks to China's July 2026 solid-state battery standard, South Korea's USD 40 billion K-Battery initiative, and Japan's continued 4680 roll-outs. CATL and BYD together forecast more than 1.2 TWh of capacity by 2030, and combined pilot lines for condensed and sulfide chemistries could enter series production by 2027. Seoul-based LG Energy Solution and Samsung SDI bridge Asian scale with Western partnerships, anchoring supply between Chinese dominance and U.S. policy incentives.

North America's share expands on the back of the Inflation Reduction Act's Section 45X, which rebates USD 35 per kWh for domestic cell output plus 30% investment tax credits for factories. LG Energy Solution's USD 5.5 billion Arizona complex and Panasonic's Kansas expansion together exceed 57 GWh of announced capacity slated for 2026, while Ford/SK and Tesla add further gigawatt-hour volumes. Federal energy-market rules, Orders 841, 2222, and 901, harmonize battery participation, and state targets create a 13 GW demand floor through 2030, ensuring visibility for developers beyond automotive offtake.

Europe operates within a tightening regulatory frame that rewards recyclers and penalizes high-carbon supply chains. The Battery Regulation's carbon-footprint labeling and material-recovery thresholds raise compliance costs that favor vertically integrated producers. Northvolt's 2024 restructuring highlighted financing hurdles, but its Ett plant still aims for 60 GWh of annual capacity. Automotive Cells Company advances three gigafactories totaling 120 GWh by 2030, while the U.K.'s Faraday Institution funds solid-state and sodium-ion R&D. Elsewhere, lithium-rich South America eyes mid-decade refining, and Middle East developers weigh long-duration storage for desert renewables, but volumes remain embryonic through 2026.

- Contemporary Amperex Technology Co. Ltd. (CATL)

- LG Energy Solution Ltd.

- Tesla, Inc.

- Panasonic Energy Co.

- Samsung SDI Co.

- BYD Co. Ltd.

- QuantumScape Corporation

- Solid Power, Inc.

- Sion Power Corporation

- Ambri Inc.

- Energy Vault Holdings, Inc.

- Form Energy, Inc.

- ESS Tech, Inc.

- Redflow Ltd.

- Blue Solutions SA

- Nexeon Ltd.

- Zinc8 Energy Solutions Inc.

- NantEnergy Inc.

- 24M Technologies, Inc.

- Northvolt AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging EV production targets by global automakers

- 4.2.2 Renewable-integration mandates for grid operators

- 4.2.3 Rapid $/kWh cost decline in solid-state & flow chemistries

- 4.2.4 Defense demand for high-energy batteries for unmanned systems

- 4.2.5 Circular-economy incentives for critical-material recovery

- 4.3 Market Restraints

- 4.3.1 Safety & thermal-runaway risks in high-energy chemistries

- 4.3.2 Critical-metal supply-chain volatility

- 4.3.3 Manufacturing scale-up hurdles for solid electrolytes

- 4.3.4 End-of-life stewardship uncertainty for novel chemistries

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment & Funding Landscape

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Lithium-Sulfur Batteries

- 5.1.2 Solid-State Batteries

- 5.1.3 Flow Batteries

- 5.1.4 Metal-Air Batteries

- 5.1.5 Mechanical and Other Advanced Storage

- 5.2 By Application

- 5.2.1 Grid Storage

- 5.2.2 Consumer Electronics

- 5.2.3 Industrial and Commercial Mobility

- 5.2.4 Marine and Aviation

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Nordic Countries

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 ASEAN Countries

- 5.3.3.6 Australia and New Zealand

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.2 LG Energy Solution Ltd.

- 6.4.3 Tesla, Inc.

- 6.4.4 Panasonic Energy Co.

- 6.4.5 Samsung SDI Co.

- 6.4.6 BYD Co. Ltd.

- 6.4.7 QuantumScape Corporation

- 6.4.8 Solid Power, Inc.

- 6.4.9 Sion Power Corporation

- 6.4.10 Ambri Inc.

- 6.4.11 Energy Vault Holdings, Inc.

- 6.4.12 Form Energy, Inc.

- 6.4.13 ESS Tech, Inc.

- 6.4.14 Redflow Ltd.

- 6.4.15 Blue Solutions SA

- 6.4.16 Nexeon Ltd.

- 6.4.17 Zinc8 Energy Solutions Inc.

- 6.4.18 NantEnergy Inc.

- 6.4.19 24M Technologies, Inc.

- 6.4.20 Northvolt AB

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment