|

시장보고서

상품코드

2063248

첨단 에너지 저장 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Advanced Energy Storage Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

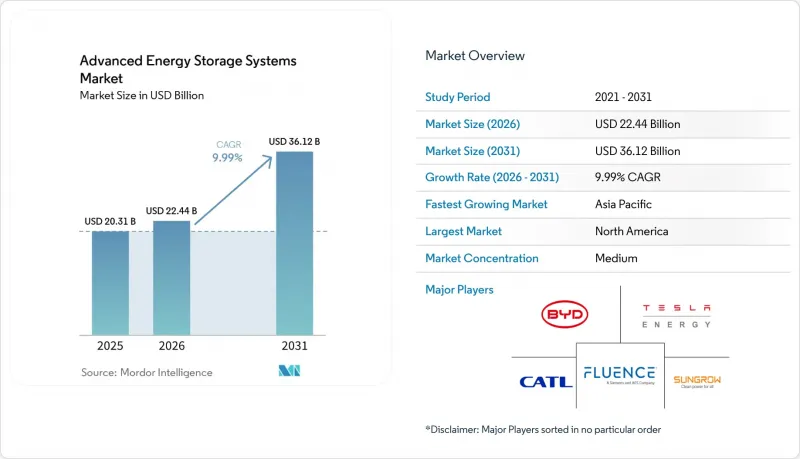

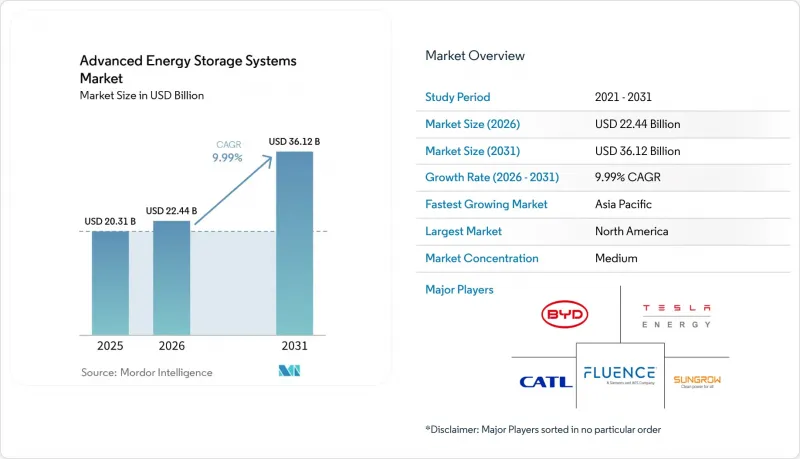

Mordor Intelligence에 의하면, 첨단 에너지 저장 시스템 시장 규모는 2025년 203억 1,000만 달러로 평가되었고, 2026년에는 224억 4,000만 달러로 추정되고, 2031년까지 361억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 9.99%로 성장할 전망입니다.

본 보고서는 유형별(전기화학식 에너지 저장, 열 에너지 저장, 기계식 에너지 저장, 기타), 용도별(계통 연계용 축전, 재생에너지 통합, 기타), 최종 사용자별(유틸리티, 상업 및 산업, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 첨단 에너지 저장 시스템 시장 동향 및 분석

리튬 이온 배터리의 kWh당 가격이 급락

리튬 이온 배터리 팩의 평균 가격은 2025년에 kWh당 108달러까지 하락할 것으로 예상되며, 2026년에는 kWh당 105달러에 달할 것으로 전망됩니다. 반면, 대규모 전력회사의 조달에서는 이미 팩 단위로 kWh당 70달러 미만의 가격이 확보되어 있습니다. 양극재가 리튬철인산염으로 전환됨에 따라 코발트에 대한 의존도가 해소되고 사이클 수명이 향상되었기 때문에 4시간 규모의 프로젝트라면 보조금 없이도 머천트 아비트라지 시장에서 수익성을 확보할 수 있게 되었습니다. CATL의 닝더 거점에서의 규모의 경제 효과로 인해, 2024년에는 69GWh가 생산되어 경쟁사들이 따라야 할 생산량 기준이 확립되었습니다. 비용 곡선은 정체세를 보이고 있으며, 향후 비용 절감은 현재 시범 단계에 있는 전고체 전지 및 나트륨 이온 전지의 기술적 돌파구에 달려 있습니다. 따라서 셀 제조업체들은 이익을 확보하기 위해 다운스트림 공정으로의 통합을 추진하고 있으며, 이로 인해 순수한 시스템 통합사업자들은 소프트웨어의 가치에 집중할 수밖에 없는 상황에 몰리고 있습니다.

세계 각국의 청정 에너지 의무화 및 에너지 저장 조달 목표

2032년까지 미국 투자 세액 공제 제도의 연장은 캘리포니아주의 16.9GW 요건이나 뉴저지주의 2GW 목표와 같은 주 차원의 목표와 맞물려, 자금 조달 리스크를 완화하는 확실한 파이프라인을 형성하고 있습니다. 유럽의 REPowerEU에는 독일의 17.5GW와 영국의 50GW라는 목표가 포함되어 있는 반면, 중국은 재생에너지 정격 용량의 최대 20%에 해당하는 에너지 저장 용량을 요구하고 있습니다. 이러한 의무화 조치로 인해 모든 신규 태양광 및 풍력 발전 프로젝트에 축전지가 포함되게 되었으며, 개발 사업자들은 18-24개월 후를 대비해 시스템을 미리 발주해야 하는 상황에 놓여 공급망이 급박해지고 있습니다. IEC 62933 성능 기준 및 ISO 22600 안전 프로토콜은 입찰의 보편적인 전제조건으로 자리 잡고 있으며, 품질 기준이 공식적으로 확립되고 있습니다.

중요 광물의 가격 및 공급 변동

콩고 민주 공화국의 수출 할당제 시행으로 출하량이 감소한 결과, 2025년 코발트 가격은 240% 급등했습니다. 한편, 리튬 탄산염은 중국 수요에 대한 불확실성으로 인해 톤당 1만 2,000달러에서 2만 8,000달러 사이에서 급등락했습니다. 니켈은 반대 양상을 보였는데, 인도네시아의 생산 증가로 인해 가격이 하락했으나, 고비용 광산이 가동 중단 상태를 유지한다면 향후 공급에 차질이 생길 우려가 있습니다. 이에 대해 배터리 제조업체들은 인산철 리튬을 채택하여 대응하고 있습니다. 이를 통해 코발트와 니켈의 위험은 피할 수 있지만, 인산염에 대한 의존도가 높아지게 됩니다. 현재, 다년간의 오프테이크 계약이나 업스트림 부문에서의 합작 사업이 표준이 되어 있으며, 공급 안정성을 확보하기 위해 광산에 선불금을 지급할 수 있는 수직 통합형 거대 기업들이 유리한 입장에 있습니다.

부문별 분석

2025년, 전기화학 시스템은 첨단 에너지 저장 시스템 시장 점유율의 57.9%를 차지했습니다. 이는 kWh당 약 105달러의 가격과 8,000회 이상의 수명을 자랑하는 인산철 리튬 배터리에 힘입은 결과입니다. 따라서, 전기화학 기반 첨단 에너지 저장 시스템 시장 규모는 4시간의 지속 시간으로 시장 가격 격차를 해소할 수 있는 분야에서 가장 빠르게 확대되고 있습니다. 흐름 전지나 나트륨-황 솔루션은 6-10시간의 시간대에 대응하고 있지만, 고온성이나 바나듐 비용의 높음으로 인해 그 보급은 틈새 시장에 국한되어 있습니다. 예측 기간 동안 추가 비용의 감소와 컨테이너의 표준화로 인해 전기화학 계열 포트폴리오는 주요 피크 수요 용도로 확대될 전망이지만, 장시간 저장 기능은 화학 계열 및 기계 계열 형식으로 이전되는 경향이 강해지고 있습니다.

그린 수소와 합성 연료가 단순한 피크 수요 조정 수단을 넘어 전력망 안정화의 기반이 됨에 따라, 화학적 접근 방식은 연평균 성장률(CAGR) 13.3%로 성장할 것입니다. 미쓰비시 전력의 유타주 317MW 프로젝트는 동굴 저장 시설과 220MW 규모의 전해조를 결합한 것으로, 수일에 걸친 방전 시에도 피크용 가스 발전과 경쟁할 수 있는 내부수익률(IRR)을 달성할 수 있음을 입증하고 있습니다. 용융염 탱크에서 압축 공기 저장고로 이어지는 열 및 기계식 시스템은 여전히 입지 조건이나 인허가 제약을 받고 있지만, 8시간 이상의 용도에서는 kWh당 비용을 낮게 유지할 수 있어 첨단 에너지 저장 시스템 시장에서 다양한 구성 요소를 확보하고 있습니다.

지역별 분석

2025년에는 아시아태평양이 매출의 46.2%를 차지한 것으로 평가되었으며, 그 배경에는 중국의 수직 통합형 밸류체인이 있습니다. 해당 지역에서는 CATL, BYD, EVE Energy 등 3개사가 합쳐서 연간 300GWh가 넘는 생산량을 기록했습니다. 모든 재생에너지 발전소에 15-20%의 에너지 저장 설비를 설치하도록 의무화하는 각 성의 규제가 지속적인 수요를 창출하고 있으며, 산둥성의 3.5GW 규모 설비 도입과 같은 메가 프로젝트는 대규모 실행력을 보여주고 있습니다. 일본은 장시간의 내장애성을 실현하기 위해 나트륨-황 전지를 추진하고 있으며, 인도의 PLI(생산 연계형 인센티브) 제도는 동남아시아 공급망을 뒷받침하는 기가팩토리에 자금을 지원하고 있어, 이를 통해 첨단 에너지 저장 시스템 시장이 해당 지역에 지속적으로 정착할 수 있게 되었습니다.

북미에서는 '인플레이션 억제법'에 따른 세액 공제와 테슬라의 40GWh 메가팩 생산 라인, LG의 애리조나주 확장 등 조달을 현지 생산으로 유도하는 국내 조달률 인센티브에 힘입어 연평균 성장률(CAGR) 14.5%를 기록하며 성장하고 있습니다. ERCOT(텍사스 전력 시장)은 성능 기반의 부가 서비스 가격 체계를 통해 1초 미만의 응답이 가능한 설비에 보상을 제공하는 방식으로, 2025년 연간 도입량에서 캘리포니아주를 앞질렀습니다. 캐나다와 멕시코도 이에 발맞추어 재생에너지의 출력 평활화를 목적으로 한 정책 지원형 입찰을 실시했습니다.

유럽에서는 영국의 50GW 목표, 독일의 17.5GW 목표, 그리고 EU 내 조달 요건으로 인해 개발 사업자들은 공급 안정성과 현지 조립에 따른 15-20% 높은 설비 투자 비용 간의 균형을 맞추지 않을 수 없습니다. 북유럽에서는 양수식 발전이 계절별 전력 균형을 맞추는 역할을 하고, 동유럽에서는 확대되는 태양광 발전 프로젝트를 안정화하기 위해 리튬 배터리 저장 시스템에 관심이 쏠리고 있습니다. 남미에서는 브라질과 아르헨티나에서 첫 대규모 입찰이 준비되고 있으며, 출력 제한을 완화하기 위해 태양광과 에너지 저장 장치를 결합한 하이브리드 시스템에 기대가 모아지고 있습니다. 중동 및 아프리카에서는 2026년 1월 사우디아라비아가 7.8GWh 규모의 배터리 저장 설비를 전력망에 연계하여 지역 신기록을 세운 것을 계기로, 관련 움직임이 가속화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the advanced energy storage systems market size is expected to increase from USD 20.31 billion in 2025 to USD 22.44 billion in 2026 and reach USD 36.12 billion by 2031, growing at a CAGR of 9.99% over 2026-2031.

This report is Segmented by Type (Electrochemical Storage, Thermal Energy Storage, Mechanical Storage, Others), Application (Grid Storage, Renewable Integration, and More), End-User (Utilities, Commercial and Industrial, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Advanced Energy Storage Systems Market Trends and Insights

Rapid Decline in Lithium-Ion Battery USD /kWh

Average lithium-ion pack prices fell to USD 108 per kWh in 2025 and are projected at USD 105 per kWh in 2026, while large utility procurements already secure sub-USD 70 per kWh pricing at the pack level. Cathode shifts toward lithium iron phosphate have removed cobalt exposure and improved cycle life, letting 4-hour projects clear merchant arbitrage markets without subsidies. Scale advantages at CATL's Ningde base produced 69 GWh in 2024, setting a volume benchmark competitors must match. The cost curve is flattening, and future savings hinge on solid-state or sodium-ion breakthroughs that are in the pilot stage. Cell maker, therefore, integrates downstream to secure margin, pressuring pure-play integrators to focus on software value.

Global Clean-Energy Mandates & Storage Procurement Targets

Extension of the U.S. investment tax credit through 2032 combines with state targets such as California's 16.9 GW requirement and New Jersey's 2 GW goal, generating a visible pipeline that derisks finance. Europe's REPowerEU includes Germany's 17.5 GW and the UK's 50 GW ambitions, while China demands storage equal to up to 20% of renewable nameplate capacity. These mandates embed batteries into every new solar and wind business case and push developers to preorder systems 18-24 months ahead, tightening supply chains. IEC 62933 performance standards and ISO 22600 safety protocols are becoming universal bid prerequisites, formalizing quality thresholds.

Critical-Mineral Price & Supply Volatility

Cobalt jumped 240% in 2025 after export quotas in the Democratic Republic of Congo cut shipments, while lithium carbonate swung between USD 12 000 and USD 28 000 per metric ton on Chinese demand uncertainty. Nickel saw the opposite trend as Indonesian output depressed prices, threatening future supply if high-cost mines stay idle. Battery makers respond with lithium iron phosphate adoption, which removes cobalt and nickel risk but introduces phosphate dependencies. Multi-year offtake contracts and upstream joint ventures are now standard, favoring vertically integrated giants that can prepay mines for security of supply.

Other drivers and restraints analyzed in the detailed report include:

- Revenue Stacking in Ancillary-Service Markets

- EV-Scale Manufacturing Lowering Stationary Costs

- Thermal-Run-Away & Fire-Safety Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrochemical systems held 57.9% of the advanced energy storage systems market share in 2025, supported by lithium iron phosphate cells priced near USD 105 per kWh and life cycles beyond 8 000 cycles. The advanced energy storage systems market size attached to electrochemical chemistries, therefore, scales fastest where a four-hour duration can clear merchant spreads. Flow batteries and sodium-sulfur solutions address 6-10-hour windows, yet high temperature or vanadium costs confine uptake to niches. Over the forecast, incremental cost declines and standardized containers will let electrochemical portfolios expand into critical-peak applications, although long-duration roles increasingly migrate to chemical or mechanical formats.

Chemical pathways grow at a 13.3% CAGR as green hydrogen and synthetic fuels become grid-stability backstops rather than marginal peak shavers. Mitsubishi Power's 317 MW Utah project blends cavern storage with 220 MW of electrolyzers, proving that multiday discharge can reach IRRs competitive with peaking gas. Thermal and mechanical variants, from molten-salt tanks to compressed-air caverns, remain constrained by site geology and permitting but fetch lower USD-per-kWh numbers for eight-hour-plus applications, ensuring a diversified mix within the advanced energy storage systems market.

Geography Analysis

Asia-Pacific captured 46.2% revenue in 2025, underpinned by China's vertically integrated value chain, where CATL, BYD, and EVE Energy collectively surpassed 300 GWh of annual output. Provincial mandates that every renewable plant include 15-20% storage create recurring demand, and mega projects such as Shandong's 3.5 GW installation demonstrate execution at scale. Japan pursues sodium-sulfur for long-duration resilience, and India's PLI scheme funds gigafactories that will feed Southeast Asian pipelines, ensuring the advanced energy storage systems market remains anchored in the region.

North America grows at 14.5% CAGR on the back of Inflation Reduction Act tax credits and domestic content bonuses that tilt procurement toward local manufacturing, including Tesla's 40 GWh Megapack line and LG's Arizona expansion. ERCOT overtook California in yearly additions during 2025 as performance-based ancillary prices reward sub-second response assets. Canada and Mexico follow with policy-backed auctions targeting renewable firming.

Europe's 50 GW UK goal, 17.5 GW German target, and made-in-EU procurement thresholds force developers to balance supply security with 15-20% higher capex linked to local assembly. Nordic pumped hydro provides seasonal balancing, while Eastern Europe eyes lithium storage to stabilize growing solar pipelines. South America readies its first large tenders in Brazil and Argentina, banking on hybrid solar-storage to curb curtailment. The Middle East and Africa accelerate as Saudi Arabia grid-connected 7.8 GWh of batteries in January 2026, setting a regional record

- Tesla, Inc.

- Siemens AG

- LG Energy Solution

- Fluence Energy, Inc.

- Samsung SDI Co., Ltd.

- General Electric Company

- BYD Company Ltd.

- Hitachi Energy

- Panasonic Holdings Corporation

- Saft Groupe S.A.

- VARTA AG

- Mitsubishi Power

- NGK Insulators, Ltd.

- ESS Inc.

- EnerSys

- Hydrostor Inc.

- Ambri Inc.

- Invinity Energy Systems

- Energy Vault Holdings, Inc.

- Stryten Energy

- Contemporary Amperex Technology Co. Ltd. (CATL)

- Sungrow Power Supply Co., Ltd.

- EVE Energy Co., Ltd.

- HyperStrong Technology

- CRRC Zhuzhou Institute

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid decline in lithium-ion battery $/kWh

- 4.2.2 Global clean-energy mandates & storage procurement targets

- 4.2.3 Revenue stacking in ancillary-service markets

- 4.2.4 EV-scale manufacturing lowering stationary costs

- 4.2.5 Second-life EV packs opening low-CAPEX markets

- 4.2.6 AI-driven dispatch boosting project IRRs

- 4.3 Market Restraints

- 4.3.1 Critical-mineral price & supply volatility

- 4.3.2 Thermal-run-away & fire-safety compliance costs

- 4.3.3 US/EU trade barriers & local-content mandates

- 4.3.4 Competition from non-battery long-duration storage

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Electrochemical Storage

- 5.1.1.1 Lithium-ion Batteries

- 5.1.1.2 Sodium-Sulfur Batteries

- 5.1.1.3 Flow Batteries

- 5.1.1.4 Lead-acid Batteries

- 5.1.1.5 Nickel-based Batteries

- 5.1.2 Thermal Energy Storage

- 5.1.2.1 Sensible Heat

- 5.1.2.2 Latent Heat

- 5.1.2.3 Thermochemical

- 5.1.3 Mechanical Storage

- 5.1.3.1 Pumped Hydro Storage

- 5.1.3.2 Compressed-Air (CAES)

- 5.1.3.3 Flywheel Storage

- 5.1.4 Chemical Storage

- 5.1.4.1 Hydrogen

- 5.1.4.2 Synthetic Natural Gas

- 5.1.4.3 Ammonia

- 5.1.5 Hybrid Storage Systems

- 5.1.1 Electrochemical Storage

- 5.2 By Application

- 5.2.1 Grid Storage

- 5.2.2 Renewable Integration

- 5.2.3 Backup Power Systems

- 5.2.4 Electric-Vehicle Infrastructure

- 5.2.5 Industrial Energy Management

- 5.2.6 Off-grid and Remote Area Storage

- 5.2.7 Residential Storage

- 5.3 By End-user

- 5.3.1 Utilities

- 5.3.2 Commercial and Industrial

- 5.3.3 Residential

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Tesla, Inc.

- 6.4.2 Siemens AG

- 6.4.3 LG Energy Solution

- 6.4.4 Fluence Energy, Inc.

- 6.4.5 Samsung SDI Co., Ltd.

- 6.4.6 General Electric Company

- 6.4.7 BYD Company Ltd.

- 6.4.8 Hitachi Energy

- 6.4.9 Panasonic Holdings Corporation

- 6.4.10 Saft Groupe S.A.

- 6.4.11 VARTA AG

- 6.4.12 Mitsubishi Power

- 6.4.13 NGK Insulators, Ltd.

- 6.4.14 ESS Inc.

- 6.4.15 EnerSys

- 6.4.16 Hydrostor Inc.

- 6.4.17 Ambri Inc.

- 6.4.18 Invinity Energy Systems

- 6.4.19 Energy Vault Holdings, Inc.

- 6.4.20 Stryten Energy

- 6.4.21 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.22 Sungrow Power Supply Co., Ltd.

- 6.4.23 EVE Energy Co., Ltd.

- 6.4.24 HyperStrong Technology

- 6.4.25 CRRC Zhuzhou Institute

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment