|

시장보고서

상품코드

2063242

해양 에너지 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Ocean Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

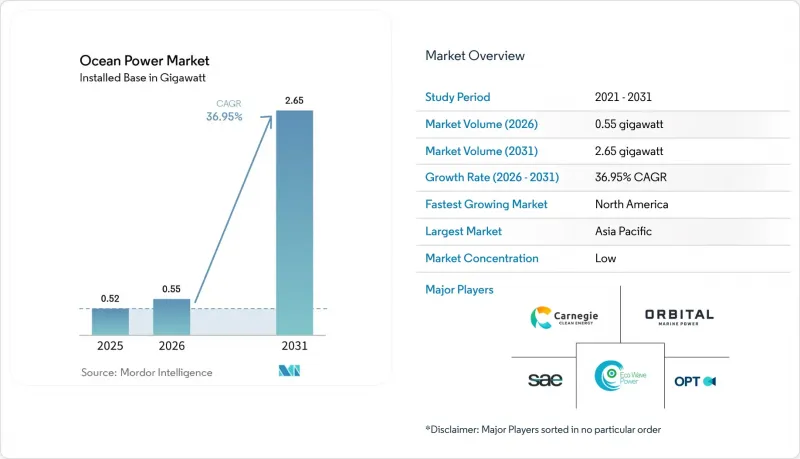

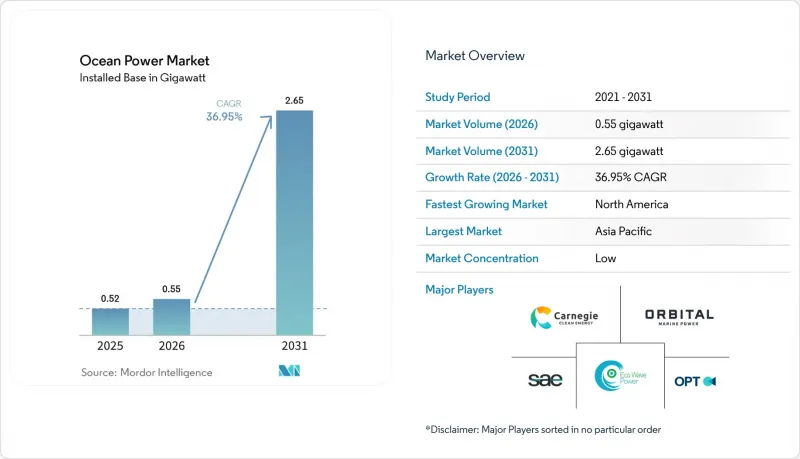

Mordor Intelligence에 의하면, 설치 기반 해양 에너지 시장 규모는 2025년에 0.52기가와트로 평가되었고, 2026년 0.55기가와트로 추정되고, 2031년까지 2.65기가와트에 이를 것으로 추정되고 있으며, 예측 기간(2026-2031년) CAGR은 36.95%를 나타낼 전망입니다.

본 보고서는 기술별(조력 발전, 파력 발전, 해양 열 발전, 염분 농도 구배 발전), 용도별(발전, 해수 담수화, 선박 추진, 데이터 및 통신 플랫폼), 최종 사용자별(유틸리티 및 독립 발전 사업자, 산업용, 상업용), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 규모(기가와트) 단위로 제시되어 있습니다.

세계의 해양 에너지 시장 동향 및 인사이트

재생에너지 목표 및 정책 인센티브

각국의 탈탄소화 로드맵에서는 해양 에너지를 재생에너지의 잔여 범주로 일괄 분류하는 대신, 명확한 용량 배분이 포함되게 되었습니다. 프랑스는 2030년까지 250MW 규모의 조력 발전 목표를 설정하고, 1kWh당 0.16달러의 고정가격매입제도(FIT)를 제공함으로써 예측 가능한 현금 흐름을 보장하고, 개발사가 우선순위 부채를 조달할 수 있도록 지원하고 있습니다. 미국은 2025년, 오리건주 연안의 계통 연계형 PacWave 사이트에서 파력 발전 컨버터 시험에 1억 1,200만 달러를 배정했으며, 장비 제조업체에 상업 규모 실증으로 나아가는 길을 열어주고 있습니다. 스페인은 액화천연가스 수입을 대체하기 위해 카나리아 제도에 60MW 규모의 파력 발전 설비에 투자하고 있으며, 이는 섬 지역이 전력 공급 안정화를 위해 풍부한 파력 자원을 활용하고 있음을 여실히 보여주고 있습니다. 이러한 정책들은 기술별로 가격 하한선을 설정함으로써 발전 사업자의 위험을 줄이고, 주식 투자자들이 최초의 상업용 발전소를 지원하도록 장려하고 있습니다. 규제 체계가 정비되는 가운데, 선도 기업들은 2031년까지의 향후 발전 용량 확대를 뒷받침할 장기 전력 구매 계약을 체결하고 있습니다.

LCOE 하락이 상업적 실현 가능성을 가속화

비용 절감은 터빈의 대형화, 모듈식 어레이, 그리고 해상 풍력 발전에서 얻은 설계적 인사이트에 기인합니다. Orbital Marine Power사의 2MW 'O2' 터빈은 메가와트당 기초 수를 절반으로 줄여 해저 설치 비용을 절감하고, 전력 수거 시스템을 간소화했습니다. CorPower Ocean사의 위상 제어 시스템은 부이의 공진을 현지 해황에 맞추어 조정함으로써, 실증 시험에서 연간 발전량을 30% 증가시키고 균등화 발전 비용을 1kWh당 0.18달러로 낮췄습니다. 스코틀랜드에서는 조력 발전소와 풍력 발전소 간에 승무원용 보트와 잭업식 바지선을 공유함으로써 O&M(운영 및 유지보수) 비용을 18% 절감했습니다. 또한, 자동 섬유 배열기를 통해 복합재 블레이드의 제조 기간이 12주에서 6주로 단축되었습니다. 이러한 프로세스의 개선이 진행됨에 따라, 해양 에너지와 고정식 해상 풍력 발전의 신규 건설에 있어 LCOE(균등화 발전 원가)의 격차는 계속 줄어들고 있으며, 조절 가능한 저탄소 기저부하 전력의 대상 시장이 확대되고 있습니다.

막대한 설비 투자(CAPEX)가 프로젝트 자금 조달의 과제로 대두되고 있습니다.

해양 에너지 발전 어레이의 초기 비용은 1kW당 4,000-7,000달러인 반면, 해상 풍력은 1,300달러로, 구성 부품의 수명에 관한 통계적 데이터를 보유하지 않은 상업 금융 기관들이 투자를 주저하게 만들고 있습니다. 오비탈 마린 파워(Orbital Marine Power)는 영국 인프라 은행이 건설 리스크의 60%를 보증한 후에야 비로소 2024년에 3,693만 달러의 자금 조달에 성공했는데, 이는 여전히 공공 지원이 필수적임을 보여줍니다. 카네기 클린 에너지(Carnegie Clean Energy)는 서호주 주에서 진행하던 파력 발전 프로젝트의 비용이 42% 초과됨에 따라 2024년에 자발적인 파산 절차에 들어갔습니다. 이는 이 분야가 해저 건설 과정에서 예기치 못한 상황에 직면해 있음을 여실히 보여주고 있습니다. 신흥 시장의 개발업체들은 거래 규모가 20MW 미만이고 표준화된 템플릿이 없어, 종종 8% 이상의 차입 비용을 감당해야 하는 상황에 직면하고 있습니다. 다자간 금융기관과의 혼합금융 구조는 도움이 되지만, 그로 인해 복잡한 계약 조건이 겹쳐져 프로젝트의 수익성을 저해하게 됩니다.

부문별 분석

2025년, 조력 발전은 설치 용량의 98.94%를 차지했습니다. 이는 검증된 구성품 수명과 40%를 상회하는 설비 가동률을 반영한 것으로, 이러한 요소들이 대규모 유틸리티 프로젝트의 자금 조달 가능성을 뒷받침하고 있습니다. 경쟁 기술들이 점차 성숙해 가는 가운데서도, 조력 발전은 해양 발전 시장에서 주도적인 위치를 유지할 것으로 보입니다. 이는 사이트 개발자가 원래 해상 풍력 발전용으로 건설된 해저 케이블이나 유지보수 선단을 활용할 수 있기 때문입니다. Minesto사의 저속 카이트형 장치는 고정축 로터가 작동하지 않는 새로운 지역을 개척하여, 지금까지 활용하지 못했던 약 10GW 규모의 자원을 확보할 수 있게 해줍니다. 파력 발전은 전 세계적으로 여전히 50MW 미만이지만, 폭풍이 가장 심할 때 구조물에 가해지는 부하를 줄여주는 위상 제어 부표 시스템 덕분에 가동률이 향상되고 있습니다. OTEC(해양열발전)은 현재 규모는 매우 작지만, 부유식 플랫폼이 비용이 많이 드는 육상 냉수 파이프라인을 불필요하게 만들고, 전력 판매에 해수 담수화 및 양식 수익을 결합함으로써 세 자릿수의 성장률을 기록하며 확대될 것입니다. IEC 62600 규격 준수에 따라 국경을 초월한 장비 판매가 가속화되고 있으며, 해상 발전 시장의 잠재적 규모가 확대되고 있습니다.

2027년 도입이 예정된 Bluerise사의 1.5MW 플랫폼과 같은 부유식 다기능 OTEC 프로토타입은 전력, 담수, 냉수 양식을 하나의 선체에 통합하여 수익원을 확대하는 동시에 고정 비용을 분산시킵니다. CorPower사의 C4와 같은 파력 발전 장치는 실시간 공진 조정을 실현하여, 단위 비용 지표를 전력 회사의 조달 기준에 가깝게 맞추고 있습니다. 2031년까지의 누적 도입량 측면에서 조류 발전 기술은 계속해서 핵심을 차지할 것입니다. 특히 캐나다의 펀디 만이나 인도네시아의 롬복 해협에서는 조류 속도가 45%의 설비 가동률을 뒷받침하고 있습니다. 그러나 다양한 개발 파이프라인을 살펴보면, 2031년까지 신규 도입 용량의 25% 이상이 비조류 시스템에 의해 공급될 것으로 예상되며, 이는 해양 발전 시장의 기술 구성이 완만하지만 꾸준히 확대되고 있음을 보여줍니다.

지역별 분석

2025년, 아시아태평양은 전 세계 총 발전 용량의 51.15%를 차지했습니다. 중국 내 저장성과 푸젠성에만 270MW 규모의 조류 발전 프로젝트를 도입하고, 해상 풍력 발전 공급망을 활용함으로써 송전 비용을 22% 절감했습니다(Nea.Gov.Cn). 한국의 시화 댐은 2025년에 552GWh를 발전할 것으로 예상되며, 조위 차 9m 규모의 하구형 프로젝트에서도 25%의 설비 이용률을 확보할 수 있고, 정부계 펀드로부터 자금을 조달할 수 있음을 입증했습니다. 일본은 외딴 섬을 대상으로 총 12MW 규모의 파력 발전 시범 사업 4건에 자금을 지원했습니다. 이곳에서는 디젤 발전 대체를 통해 1kWh당 0.35달러의 비용 절감을 실현하고 있습니다. 한편, 호주는 퍼스 앞바다에 8MW 규모의 파력 발전 설비를 설치하여 연안 광업 사업을 위한 해수 담수화 플랜트에 전력을 공급하고 있습니다. 동남아시아 전역에서 인도네시아와 필리핀의 미개발 해협은 이론상 18GW의 자원을 보유하고 있으나, 송전망의 제약과 요금 체계의 부재로 인해 도입 용량은 5MW 미만에 그치고 있습니다.

북미에서는 미국 해양에너지청이 2025년 오리건주, 캘리포니아주, 메인주 연안에서 600MW 규모의 조력 및 파력 발전 임대권 입찰을 실시한 데 힘입어, 2031년까지 연평균 성장률(CAGR) 71.9%를 나타낼 것으로 전망됩니다. PacWave 시험 사이트는 대출 기관의 실사 기준을 충족하는 실시간 성능 메타데이터를 제공함으로써, 상용화 전 발전 설비에 대한 상업적 자금 조달을 가능하게 합니다. 캐나다 펀디 만에 위치한 부유식 조력 발전소는 해저 앵커를 사용하지 않고 2024년에 38%의 설비 이용률을 달성했습니다. 한편, 멕시코 바하칼리포르니아주에서는 농업용 해수 담수화 시설에 전력을 공급하기 위해 15MW 규모의 파력 발전 설비를 확보하고 있습니다. 2024년 연방에너지규제위원회(FERC)가 실시한 규제 합리화를 통해 5MW 미만 프로젝트의 해양 에너지 라이선스 취득 소요 기간이 3년으로 단축됨에 따라, 정책적 마찰이 완화되고 있음을 보여줍니다.

유럽 시장은 영국의 12MW 규모 메이젠(MeyGen) 발전소와 프랑스의 '에너지 장기 계획(Programmation Pluriannuelle de l'Energie)'에 기반한 250MW 규모의 조류 발전 로드맵에 의해 주도되고 있습니다. 영국의 크라운 에스테이트(Crown Estate)는 2025년에 최대 1GW 규모의 해저 임대권 11건을 발급할 예정이며, 한편 스페인의 바스크 지방 에너지청은 600가구에 전력을 공급하는 2MW 규모의 수중 진동 발전 설비를 가동했습니다. 네덜란드에서는 바람이 불지 않는 기간 동안 계통 주파수를 조절하기 위해 10MW 규모의 조류 발전 설비를 해상 풍력 발전 시설과 통합했습니다. 또한 덴마크의 WavePiston사는 2029년까지 풍력 발전과 비용 경쟁력을 확보하는 것을 목표로 5MW 규모의 모듈식 파력 발전 패널을 설치했습니다. 남미와 중동에서는 여전히 규모가 제한적이며, 브라질의 10MW 페셈 파력 발전 프로젝트는 자금 조달 문제로 정체되어 있고, 사우디아라비아의 5MW 홍해 시범 사업은 인허가 심사 과정에서 연기되어, 투자 준비 현황에 있어 지역 간 격차가 뚜렷이 드러나고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the ocean power market size in terms of installed base was valued at 0.52 gigawatt in 2025 and is estimated to grow from 0.55 gigawatt in 2026 to reach 2.65 gigawatt by 2031, at a CAGR of 36.95% during the forecast period (2026-2031).

This report is Segmented by Technology (Tidal Energy, Wave Energy, OTEC, Salinity-Gradient), Application (Power Generation, Desalination, Marine Propulsion, Data & Telecom Platforms), End-User (Utilities and IPPs, Industrial, Commercial), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Volume (gigawatt).

Global Ocean Power Market Trends and Insights

Renewable-energy targets & policy incentives

National decarbonization roadmaps now feature explicit capacity allocations for marine energy instead of bundling it into residual renewable categories. France set a 250 MW tidal-stream target for 2030 and offers feed-in tariffs of USD 0.16 per kWh that guarantee predictable cash flow, helping developers raise senior debt. The United States earmarked USD 112 million in 2025 for wave-energy converter testing at the grid-connected PacWave site off Oregon, giving device manufacturers a route to commercial-scale demonstrations. Spain is investing in 60 MW of wave capacity for the Canary Islands to displace liquefied natural-gas imports, underscoring how archipelago jurisdictions are leveraging abundant wave resources for supply security. These policies provide technology-specific price floors that de-risk merchant exposure and encourage equity investors to back first-commercial arrays. As rule-making evolves, early movers are locking in long-term offtake agreements that will underpin the next wave of capacity additions through 2031.

Declining LCOE accelerates commercial viability

Cost reductions stem from turbine upsizing, modular arrays, and design lessons imported from offshore wind. Orbital Marine Power's 2 MW O2 turbine halves the number of foundations per megawatt, trimming subsea installation costs and simplifying electrical collection. CorPower Ocean's phase-control system tunes a buoy's resonance to local sea states, boosting annual energy capture by 30% and pulling levelized costs toward USD 0.18 per kWh in field trials. Shared crew boats and jack-up barges between tidal and wind farms in Scotland have cut O&M expenses by 18%, while automated fiber-placement machines now fabricate composite blades in six weeks instead of twelve. As these process gains propagate, the new-build LCOE gap between marine energy and fixed-bottom offshore wind continues to narrow, expanding the addressable market for dispatchable, low-carbon baseload power.

High CAPEX requirements challenge project financing

Marine-energy arrays cost USD 4,000-7,000 per kW up front, versus USD 1,300 for offshore wind, deterring commercial lenders that lack actuarial data on component lifetimes. Orbital Marine Power secured USD 36.93 million in 2024 only after the UK Infrastructure Bank guaranteed 60% of construction risk, illustrating that public backstops remain critical. Carnegie Clean Energy slipped into voluntary administration in 2024 after a 42% cost overrun on its Western Australian wave project, highlighting the sector's exposure to subsea-construction contingencies. Emerging-market developers often face debt costs above 8% because transactions are sub-20 MW and lack standardized templates. Blended-finance structures with multilateral lenders help, but they introduce complex covenant stacks that erode project returns.

Other drivers and restraints analyzed in the detailed report include:

- Predictable baseload resource availability complements intermittent renewables

- Offshore hydrogen production creates synergistic value chains

- Complex environmental permitting delays project development

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tidal energy delivered 98.94% of installed capacity in 2025, reflecting validated component lifetimes and capacity factors above 40% that anchor utility-scale bankability. The ocean power market size for tidal is poised to maintain leadership even as competing designs mature, because site developers can leverage subsea cables and maintenance fleets originally built for offshore wind. Minesto's low-velocity kite devices open new geographies where fixed-axis rotors cannot function, unlocking an estimated 10 GW of previously stranded resource. Wave energy, still under 50 MW globally, is improving availability through phase-control buoy systems that shave structural loads during storm peaks. OTEC, though negligible today, will grow at a triple-digit pace as floating platforms bypass costly onshore cold-water pipes and pair electricity sales with desalination and aquaculture revenue. Compliance with IEC 62600 standards is accelerating cross-border equipment sales, expanding addressable capacity in the ocean power market.

Floating, multi-output OTEC prototypes such as Bluerise's 1.5 MW platform scheduled for 2027 combine electricity, freshwater, and chilled-water aquaculture in one hull, widening revenue streams while spreading fixed costs. Wave devices like CorPower's C4 achieve real-time resonance tuning that pulls unit-cost metrics toward utility triggers for procurement. Tidal technology will remain the backbone of cumulative installations through 2031, especially in Canada's Bay of Fundy and Indonesia's Lombok Strait, where current velocities support 45% capacity factors. However, the diversified pipeline suggests that by 2031, more than 25% of new capacity additions will come from non-tidal systems, signaling a slow but steady broadening of the ocean power market technology mix.

Geography Analysis

Asia-Pacific commanded 51.15% of global capacity in 2025 as China alone installed 270 MW of tidal-stream projects in Zhejiang and Fujian, leveraging offshore wind supply chains to slash transmission costs by 22% Nea.Gov.Cn. South Korea's Sihwa barrage generated 552 GWh in 2025, proving that estuary-scale projects with 9-m tidal ranges can secure 25% capacity factors and attract sovereign-wealth financing. Japan funded four wave pilots totaling 12 MW for remote islands where diesel displacement saves USD 0.35 per kWh, while Australia deployed 8 MW of wave capacity off Perth that feeds desalination for coastal mining operations. Across Southeast Asia, untapped straits in Indonesia and the Philippines offer 18 GW of theoretical resource, but grid constraints and absent tariffs leave installed capacity below 5 MW.

North America is set to record a 71.9% CAGR through 2031 following the US Bureau of Ocean Energy Management's 2025 auction for 600 MW of tidal and wave leases off Oregon, California, and Maine. The PacWave test site supplies real-time performance metadata that satisfies lender due-diligence standards, unlocking commercial debt for pre-commercial arrays. Canada's Bay of Fundy floating tidal farm achieved a 38% capacity factor in 2024 without seabed anchors, while Mexico's Baja California is procuring 15 MW of wave capacity to feed agricultural desalination facilities. Regulatory streamlining by the Federal Energy Regulatory Commission in 2024 reduced marine-energy licensing timelines to three years for projects under 5 MW, signaling that policy frictions are abating.

Europe's market is anchored by the UK's 12 MW MeyGen array and France's 250 MW tidal-stream roadmap under the Programmation Pluriannuelle de l'Energie. The UK Crown Estate issued 11 seabed leases in 2025 worth up to 1 GW, while Spain's Basque Energy Agency commissioned a 2 MW oscillating water column that serves 600 households. The Netherlands integrated a 10 MW tidal array with offshore wind to balance grid frequency during calm periods, and Denmark's WavePiston installed 5 MW of modular wave plates targeting cost parity with wind by 2029. South America and the Middle East remain subscale, with Brazil's 10 MW Pecem wave project stalled over financing and Saudi Arabia's 5 MW Red Sea pilot postponed amid permitting reviews, underlining regional disparities in investment readiness.

- SIMEC Atlantis Energy

- Orbital Marine Power

- Ocean Power Technologies Inc.

- Eco Wave Power Global AB

- Carnegie Clean Energy

- AW-Energy Oy

- Wello Oy

- CorPower Ocean

- Sabella SA

- Marine Power Systems

- Minesto AB

- Nova Innovation

- Oscilla Power

- Bombora Wave Power

- OceanBased Perpetual Energy

- Xinjiang Goldwind Science & Tech

- Seabased AB

- Arrecife Energy Systems

- IHI Corporation

- Hyundai Heavy Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renewable-energy targets & policy incentives

- 4.2.2 Declining LCOE for tidal & wave technologies

- 4.2.3 Predictable baseload resource availability

- 4.2.4 Offshore hydrogen & aquaculture co-location

- 4.2.5 Naval decarbonisation requirements

- 4.2.6 Island-grid resilience programmes

- 4.3 Market Restraints

- 4.3.1 High CAPEX & financing hurdles

- 4.3.2 Complex environmental permitting

- 4.3.3 Advanced-composite supply bottlenecks

- 4.3.4 Non-standard grid-code compliance

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Tidal Energy

- 5.1.2 Wave Energy

- 5.1.3 Ocean Thermal Energy Conversion (OTEC)

- 5.1.4 Salinity-Gradient (Blue Energy)

- 5.2 By Application

- 5.2.1 Power Generation

- 5.2.2 Desalination

- 5.2.3 Marine Propulsion

- 5.2.4 Data & Telecom Platforms

- 5.3 By End-User

- 5.3.1 Utilities and IPPs

- 5.3.2 Industrial

- 5.3.3 Commercial

- 5.4 By Region

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Spain

- 5.4.2.4 Netherland

- 5.4.2.5 Denmark

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 SIMEC Atlantis Energy

- 6.4.2 Orbital Marine Power

- 6.4.3 Ocean Power Technologies Inc.

- 6.4.4 Eco Wave Power Global AB

- 6.4.5 Carnegie Clean Energy

- 6.4.6 AW-Energy Oy

- 6.4.7 Wello Oy

- 6.4.8 CorPower Ocean

- 6.4.9 Sabella SA

- 6.4.10 Marine Power Systems

- 6.4.11 Minesto AB

- 6.4.12 Nova Innovation

- 6.4.13 Oscilla Power

- 6.4.14 Bombora Wave Power

- 6.4.15 OceanBased Perpetual Energy

- 6.4.16 Xinjiang Goldwind Science & Tech

- 6.4.17 Seabased AB

- 6.4.18 Arrecife Energy Systems

- 6.4.19 IHI Corporation

- 6.4.20 Hyundai Heavy Industries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment