|

시장보고서

상품코드

2063259

태양광 패널 세정 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Solar Panel Cleaning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

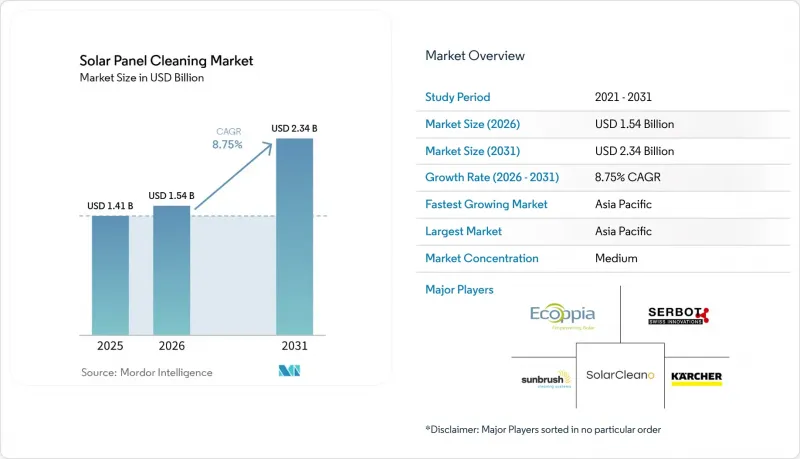

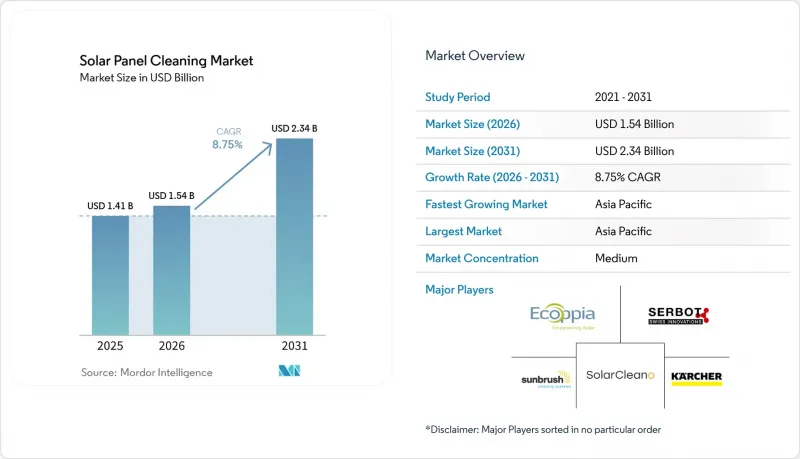

Mordor Intelligence에 의하면, 태양광 패널 세정 시장 규모는 2025년 14억 1,000만 달러로 평가되었습니다. 2026년 15억 4,000만 달러에서 2031년까지 23억 4,000만 달러로 확대되고 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.75%를 나타낼 것으로 예측됩니다.

본 보고서는 세정 방법(습식, 건식, 정전기식, 코팅식), 기술 수준(수동, 반자동, 자율형 로봇, 드론), 도입 형태(주거용, 상업 및 산업용, 유틸리티 규모, 부유식 태양광 발전), 서비스 모델(자사 운영, 제3자 제공, Raas), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)에 따라 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 태양광 패널 세정 시장 동향과 인사이트

건조 지역에서의 대규모 태양광 발전소 건설 가속화

사우디아라비아의 슈아이바 및 수다이르 복합 시설에서는 오염으로 인해 최대 70%에 달하는 출력 손실이 발생하고 있어, 빈번한 청소 주기가 경제적으로 필수적입니다. 이에 따라 라자스탄 주의 1GW 규모 푸갈 파크에서는 성능 미달 시 사업자에게 1kWh당 6루피의 벌금을 부과하는 계약상 의무가 마련되었습니다. 퀸즐랜드주와 뉴사우스웨일스주의 대규모 태양광 발전소에서는 모래폭풍과의 싸움이 계속되고 있으며, 현재는 20도 경사면을 오를 수 있는 LiFePO4 배터리를 탑재한 로봇 군단이 24시간 365일 가동되는 것이 정당화되고 있습니다. 국제에너지기구(IEA)의 추산에 따르면, 오염으로 인해 전 세계 태양광 발전 용량의 4-7%가 손실되고 있으며, 이는 연간 50억 유로의 수익 손실에 해당합니다. 각 공급업체들은 지형에 적합한 크롤러와 경량 복합 소재를 채택함으로써, 외딴 사막 현장에 대한 운송 비용을 절감하고 있습니다. 이러한 혁신 기술은 자동 청소를 통해 전력 구매 계약(PPA)을 보호하고, 기가와트 규모의 건설 프로젝트에 대한 자금 조달 가능성을 뒷받침하는 생태계를 강화하고 있습니다.

보다 엄격한 O&M 및 성과 비율 계약

서벵골주의 10MW 옥상 입찰 및 칠레의 181.25MWac ENGIE 프로젝트에 포함된 발전 기준치로 인해, 서비스 제공업체들은 오염 위험을 감수할 수밖에 없게 되었으며, 이로 인해 모든 청소 주기에 대한 사진 증거를 촬영하고 전송하는 로봇에 대한 수요가 증가하고 있습니다. SECI의 표준화된 O&M 템플릿에 따르면, 몬순기나 수확 후 먼지가 가장 많이 발생하는 시기에는 2주에 한 번씩 청소를 의무화하고 있어, 인도의 관행이 EU 재생에너지 지침의 기준에 부합하도록 되어 있습니다. 스페인과 이탈리아의 자산 소유주들은 인센티브 지급을 실시간 차량 데이터와 연동하고 있으며, 공급업체에 클라우드 기반 대시보드 및 예측 유지보수 분석의 통합을 요구하고 있습니다. 그 결과, 설비 가격뿐만 아니라 청소 빈도에 따라 계약 성패가 결정되는 성과 중심의 조달 환경이 조성되고 있습니다.

완전 자율형 로봇에 대한 막대한 설비 투자

대당 5만-15만 달러의 가격 책정은 연간 수익이 고작 4,500달러에 불과한 미국의 10kW 규모 옥상 설치 시스템의 경우, 10년 이상의 회수 기간을 감수해야 함을 의미합니다. Serbot사의 조이스틱 조작 방식인 ‘PV Eco STANDARD’는 비용 장벽을 완화해 주지만, 여전히 사람의 감독이 필요하기 때문에 50kW 미만의 규모에서는 도입이 더딘 임베디드니다. 부문 매출의 18%를 차지하는 BladeRanger는 여러 MW 규모의 계약에 주력하고 있으며, 해당 계약에 도입된 로봇 군이 규모의 경제를 통해 비용을 상각합니다. 금리 상승과 넷미터링 인센티브 축소로 인해 2024년 미국의 주택용 태양광 발전 도입량은 31-32% 감소했으며, 이로 인해 고가의 자동화 시스템에 대한 수요도 위축되고 있습니다. 리스 모델이나 Robot-as-a-Service(RaaS)는 설비 투자(Capex)를 운영비(OpEx)로 전환하지만, 흩어져 있는 지붕 소유주들에게는 여전히 구독료가 경제적으로 타당하지 않습니다.

부문별 분석

2025년, 태양광 패널 세정 시장 규모의 60.0%를 습식 세정이 차지한 가운데, 건식 브러시 로봇이 시장 점유율을 확대했습니다. 염분막으로 인해 정기적인 세척이 필요한 스페인 연안 지역, 이탈리아, UAE에서는 고압 제트 시스템이 주류를 이루고 있지만, Solaris Hydrobotics사의 수력 모터 로봇은 패널 1장당 고작 0.5-1.5리터의 물만 소비하기 때문에 물은 풍부하지만 전력망이 없는 지역에서 활약하고 있습니다.

에코피아(Ecoppia)의 3,900MW 무수 도입 실적은 사막 지대에서 탱크로리를 이용한 물류를 없애줌으로써 운영비를 30-40% 절감할 수 있음을 보여줍니다. 블루스카이(Bluesky)와 노마드(Nomadd)가 시험한 마찰 발전식 전자기 스크린은 7분 만에 먼지의 90%를 제거하며, 향후 브러쉬리스 솔루션을 제시하고 있습니다. Chemitek사의 생분해성 약제를 사용하면 드론을 통해 아그리볼타익(농업과 태양광 발전의 융합) 시설의 작물 줄 사이로 살포할 수 있게 되어, 습식 및 공중 살포 기술을 융합한 하이브리드 툴킷을 구현할 수 있습니다. 중동·북아프리카(MENA) 지역에서 물 가격이 1세제곱미터당 5달러를 초과하는 가운데, 건식 방식 플랫폼이 습식 방식의 우위를 꾸준히 잠식하고 있으며, 태양광 패널 세척 업계에서는 2026년 이후 가동을 시작하는 발전소에 대해 기본적으로 무수 옵션을 채택하는 조달 방침이 나타나고 있습니다.

태양광 패널 세정 시장에서 2025년 매출의 50.2%는 여전히 수동식 장비가 차지하고 있는데, 이는 주로 주택용 및 1MW 미만의 옥상 시설에서 낮은 인건비가 효율성 향상을 상쇄하고 있기 때문입니다. 반자동식 트롤리는 지붕 경사가 고르지 않은 인도 및 동남아시아의 상업 및 산업(C&I) 시설에서 비용 측면의 격차를 해소하고 있습니다.

완전 자율형 로봇은 ±10cm의 정밀도를 자랑하는 GPS 위치 측정, 머신 비전, 열충격을 피하는 야간 가동 등을 바탕으로 연평균 성장률(CAGR) 11.4%를 기록하며 성장하고 있습니다. 2025년 FAA가 태양광 발전용 멀티드론 운용을 승인함에 따라, 지형이 험한 지역에서는 지상 크롤러를 보완하는 형태로 공중 시스템이 활용될 전망입니다. EAUAV의 드론은 하루에 8,000-1만 제곱미터를 청소하며, 높은 곳에 설치된 태양광 패널에 대한 접근성을 높이고 있습니다. 한편, Infosys-Kaynes의 ‘Kleinbot’은 에어컨 기기의 그늘에 가려진 소형 지붕을 대상으로 합니다. 태양광 패널 청소 업계 전반적으로 지상 로봇과 드론을 결합한 통합형 차량 체계로의 전환이 진행되고 있으며, 순수한 수작업 방식의 폐지가 가속화되고 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 매출의 45.1%를 차지했으며, 2031년까지 연평균 10.0%의 성장률을 보일 것으로 전망됩니다. 중국의 모듈 생산량 289GW와 인도의 격주 청소 의무가 수요의 기반이 되고 있는 반면, TrinaRobot의 열간 청소 시스템은 알바니아의 152MW 및 말레이시아의 100MW 태양광 발전소에서 발전량을 8-15% 향상시켰습니다. 일본, 한국 및 아세안(ASEAN) 국가들에서는 2022년에 41.4GW의 태양광 발전 용량이 추가되어, 밀집된 도시 지역의 옥상에 적합한 휴대용 로봇의 보급을 촉진했습니다.

북미에서는 인플레이션 억제법(Inflation Reduction Act)을 배경으로 2021년부터 2024년에 걸쳐 대규모 태양광 발전소 건설이 73% 급증했으나, 금리 상승에 따라 2024년 주택용 설치량은 31-32% 감소했습니다. 애리조나주나 소노라주 등의 사막 지대에서는 1,000달러 이상이 드는 급수차 운행을 피하기 위해, 건조한 잡목림 청소를 담당하는 로봇 군단에 의존하고 있습니다. 캐나다 온타리오주와 앨버타주에서는 모듈의 보증을 해치지 않으면서 제설 도구로도 겸용할 수 있는 반자동 플랫폼이 선호되고 있습니다.

유럽에서는 2022년에 41.4GW가 추가되었으며, ‘REPowerEU’에 따라 450GWac를 목표로 하고 있지만, 스페인에서는 계절적인 모래먼지로 인해 건기에는 발전량이 최대 15% 감소합니다. 일상적인 유지보수에는 건조 로봇을, 철저한 청소에는 습식 시스템을 사용하는 하이브리드 방식이 현재 스페인과 포르투갈에서는 표준으로 자리 잡고 있습니다. 북유럽의 태양광 발전소에서는 소프트 롤러 방식의 제설 솔루션이 우선적으로 채택되고 있는 반면, 독일의 고정가격임베디드제도(FIT)가 옥상 설치 확대를 뒷받침하고 있어 가볍고 휴대하기 쉬운 장비가 요구되고 있습니다.

중동 및 아프리카에서는 하루 최대 0.9%라는 세계 최악의 오염률을 기록하고 있어, 물을 사용하지 않는 로봇의 도입이 필수적입니다. 사우디아라비아의 ‘비전 2030’ 복합 시설에서는 Ecoppia의 로봇 군이 물 1리터도 사용하지 않고 99.92%의 청소 효율을 달성하고 있습니다. 남아프리카와 이집트도 이에 발맞추고 있으며, 물 부족과 야심 찬 태양광 발전 계획이 맞물리면서 이 지역은 건조 지대 혁신의 선구자로서의 입지를 공고히 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the solar panel cleaning market size is projected to expand from USD 1.41 billion in 2025 and USD 1.54 billion in 2026 to USD 2.34 billion by 2031, registering a CAGR of 8.75% between 2026 to 2031.

This report is Segmented by Cleaning Method (Wet, Dry, Electrostatic, Coating-Based), Technology Level (Manual, Semi-Automatic, Autonomous Robots, Drones), Deployment (Residential, Commercial & Industrial, Utility-Scale, Floating PV), Service Model (In-House, Third-Party, Raas), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are in Value (USD).

Global Solar Panel Cleaning Market Trends and Insights

Rapid Utility-Scale PV Build-Outs in Arid Zones

Soiling losses of up to 70% in Saudi Arabia's Shuaibah and Sudair complexes have made frequent cleaning cycles financially critical, triggering contractual mandates in Rajasthan's 1 GW Pugal park that fine operators INR 6 per kWh for under-performance. Large arrays in Queensland and New South Wales battle dust storms that now justify 24/7 robotic fleets equipped with LiFePO4 batteries capable of climbing 20-degree slopes. The IEA estimates soiling erodes 4-7% of global PV output, equal to EUR 5 billion in lost revenue each year . Suppliers respond with terrain-adaptive tracks and lightweight composites that lower transport costs to remote desert sites. These innovations reinforce an ecosystem where automated cleaning protects power-purchase guarantees and underpins bankability for gigawatt-scale builds.

Stricter O&M Performance-Ratio Contracts

Generation thresholds embedded in West Bengal's 10 MW rooftop tender and Chile's 181.25 MWac ENGIE project force service providers to shoulder soiling risk, catalyzing demand for robots that capture and transmit photographic proof of every cleaning cycle. SECIs standardized O&M template now requires biweekly cleaning during monsoon and post-harvest dust peaks, aligning Indian practice with EU Renewable Energy Directive standards. Asset owners in Spain and Italy link incentive payments to real-time fleet data, compelling vendors to integrate cloud-based dashboards and predictive maintenance analytics. The net result is a performance-driven procurement environment where cleaning cadence, not just equipment price, determines contract awards.

High Capex of Fully-Autonomous Robots

Price tags of USD 50,000-150,000 per unit impose decade-long paybacks on 10 kW U.S. rooftops earning only USD 4,500 annually. Serbot's joystick-controlled PV Eco STANDARD eases cost barriers but still demands human presence, slowing adoption below the 50 kW threshold. BladeRanger, holding 18% segment revenue, focuses on multi-MW contracts where fleets amortize cost over scale. Rising interest rates and declining net-metering incentives kept U.S. residential solar installations down 31-32% in 2024, dampening demand for expensive automation. Leasing models and Robot-as-a-Service convert capex to opex, yet subscription fees remain uneconomic for scattered rooftop owners.

Other drivers and restraints analyzed in the detailed report include:

- Falling LCOE of Dry-Brush Robotic Systems

- PV Module Warranties Adding Anti-Soiling KPIs

- Skilled-Labor Shortages for Robot Fleet Servicing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dry-brush robots captured a growing share as wet cleaning retained 60.0% of the solar panel cleaning market size in 2025. High-pressure jet systems dominate coastal Spain, Italy, and the UAE, where salt films demand periodic rinsing, while Solaris Hydrobotics' water-motor robots consume only 0.5-1.5 liters per panel and thrive where water is plentiful yet grid power is absent .

Ecoppia's 3,900 MW of water-free deployments illustrate how eliminating tanker-truck logistics cuts operating expenses 30-40% in deserts. Triboelectric electrodynamic screens tested by Bluesky and Nomadd remove 90% of dust in seven minutes, offering a future zero-brush solution. Biodegradable agents from Chemitek enable drone spraying over agrivoltaic rows, blending wet and aerial techniques into a hybrid toolkit. As water prices surpass USD 5 per m3 in MENA, dry platforms are steadily eroding wet dominance, and the solar panel cleaning industry is witnessing procurement policies that now default to zero-water options for plants entering service after 2026.

Manual equipment still holds 50.2% of 2025 revenue in the solar panel cleaning market share, chiefly across residential and sub-MW rooftops where low labor costs outweigh efficiency gains . Semi-automatic trolleys bridge affordability gaps for Indian and Southeast Asian C&I sites with mixed roof angles.

Fully autonomous robots are scaling at an 11.4% CAGR, aided by GPS positioning accurate to +-10 cm, machine vision, and night-time operation that avoids thermal shock. FAA approval for multi-drone solar missions in 2025 positions aerial systems to complement ground crawlers on irregular terrain. EAUAV drones cleaning 8,000-10,000 m2 daily expand access to high-elevation arrays, while Infosys-Kaynes' Kleinbot targets compact roofs shaded by HVAC units. The solar panel cleaning industry as a whole is moving toward integrated fleets mixing ground robots and drones, accelerating the retirement of purely manual regimes.

Geography Analysis

Asia-Pacific accounted for 45.1% of global revenue in 2025 and is forecast to grow at 10.0% annually through 2031. China's module output of 289 GW and India's biweekly cleaning mandates anchor demand, while TrinaRobot's cross-row systems improved generation 8-15% across 152 MW in Albania and 100 MW in Malaysia. Japan, South Korea, and ASEAN nations added 41.4 GW of solar capacity in 2022, driving the uptake of portable robots suited to dense urban rooftops.

North America's utility-scale buildout surged 73% from 2021 to 2024 on the back of the Inflation Reduction Act, but residential installations fell 31-32% in 2024 as interest rates climbed. Desert states like Arizona and Sonora rely on dry-brush fleets to avoid USD 1,000-plus water-truck runs. Canada's Ontario and Alberta favor semi-automatic platforms that can double as snow-removal tools without violating module warranties.

Europe added 41.4 GW in 2022 and aims for 450 GWac under REPowerEU, with Spain's seasonal dust curtailing output up to 15% during dry spells. Hybrid regimes using dry robots for routine cycles and wet systems for deep cleans are now standard in Spain and Portugal. Nordic arrays prioritize soft-roller snow solutions, while Germany's feed-in tariffs spur rooftop growth, demanding lightweight portable equipment.

The Middle East and Africa experience the planet's worst soiling rates up to 0.9% per day,y making water-free robots essential. Saudi Arabia's Vision 2030 complexes employ Ecoppia fleets that reach 99.92% cleaning efficiency without a single liter of water. South Africa and Egypt follow suit as water scarcity converges with ambitious solar pipelines, reinforcing the region's status as a bellwether for dry-brush innovation.

- Ecoppia

- SunBrush mobil GmbH

- Karcher

- Serbot AG

- SolarCleano

- RST CleanTech

- Heliotex

- Sunpure Technology

- IPC Eagle

- PV Clean Mobile (USA)

- Clean Solar Industries

- KP Group

- TrinaRobot

- ChemiTek

- IFBOT Robotics

- Exosun

- Energy Robotics

- Aqua Solar Cleaners

- Limpeza Solar (Brazil)

- Muller Solar Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid utility-scale PV build-outs in arid zones

- 4.2.2 Stricter O&M performance-ratio contracts

- 4.2.3 Falling LCOE of dry-brush robotic systems

- 4.2.4 PV module warranties adding anti-soiling KPIs

- 4.2.5 ESG-driven water-neutral O&M mandates

- 4.3 Market Restraints

- 4.3.1 High capex of fully-autonomous robots

- 4.3.2 Limited ROI for rooftops <50 kW

- 4.3.3 Regulatory gray-zones on micro-plastics from brush wear

- 4.3.4 Skilled-labor shortages for robot fleet servicing

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Cleaning Method

- 5.1.1 Wet (Water-Fed Brush, High-Pressure Jet)

- 5.1.2 Dry (Rotary Brush, Air-Blast)

- 5.1.3 Electrostatic / Ionic

- 5.1.4 Coating-Based Self-Cleaning (Hydrophobic, Anti-Soiling)

- 5.2 By Technology Level

- 5.2.1 Manual Tools

- 5.2.2 Semi-Automatic (Trolley, Tractor-Mounted)

- 5.2.3 Fully-Autonomous Robots

- 5.2.4 Drone-Based Systems

- 5.3 By Deployment

- 5.3.1 Residential Rooftop (Up to 20 kW)

- 5.3.2 Commercial and Industrial (20 kW to 1 MW)

- 5.3.3 Utility-Scale (Above 1 MW)

- 5.3.4 Floating PV Arrays

- 5.4 By Service Model

- 5.4.1 In-House O&M Teams

- 5.4.2 Third-Party Cleaning Service Providers

- 5.4.3 Robot-as-a-Service (RaaS) Subscriptions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Ecoppia

- 6.4.2 SunBrush mobil GmbH

- 6.4.3 Karcher

- 6.4.4 Serbot AG

- 6.4.5 SolarCleano

- 6.4.6 RST CleanTech

- 6.4.7 Heliotex

- 6.4.8 Sunpure Technology

- 6.4.9 IPC Eagle

- 6.4.10 PV Clean Mobile (USA)

- 6.4.11 Clean Solar Industries

- 6.4.12 KP Group

- 6.4.13 TrinaRobot

- 6.4.14 ChemiTek

- 6.4.15 IFBOT Robotics

- 6.4.16 Exosun

- 6.4.17 Energy Robotics

- 6.4.18 Aqua Solar Cleaners

- 6.4.19 Limpeza Solar (Brazil)

- 6.4.20 Muller Solar Services

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment