|

시장보고서

상품코드

2063269

도어 제어 모듈 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Door Control Modules - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

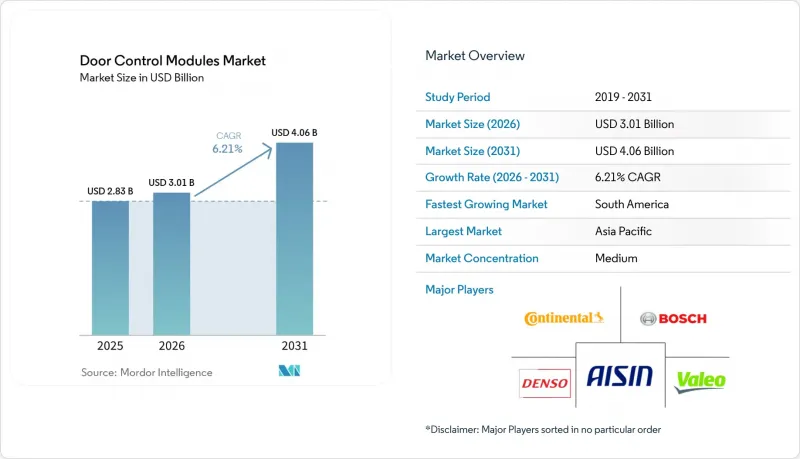

Mordor Intelligence에 의하면, 도어 제어 모듈 시장 규모는 2025년 28억 3,000만 달러로 평가되었고, 2026년에는 30억 1,000만 달러로 추정되고, 2031년까지 40억 6,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR)은 6.21%가 될 것으로 전망됩니다.

본 보고서는 유형별(집중형 도어 제어 모듈 등), 용도별(도어 잠금, 미러 조절, 윈도우 리프트, 조명 등), 구성 요소별(액추에이터, 센서 등), 판매 채널별(OEM 및 애프터마켓), 지역별(북미, 남미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(대수)으로 제시되어 있습니다.

세계의 도어 제어 모듈 시장 동향 및 분석

전동화로 인해 도어당 전자 부품 탑재량이 증가

전기차(EV) 플랫폼은 충분한 저전압 전원을 공급하므로, 차체 엔지니어는 제스처 제어, 레이더 기반 장애물 감지, 배터리 차단 로직을 단일 도어 컨트롤러에 통합할 수 있게 됩니다. 컨트롤러당 기능이 늘어나는 것은 소프트웨어의 설치 공간 확대를 의미하기 때문에 Tier 1 공급업체들은 현재 AUTOSAR 스택과 사이버 보안 라이브러리를 기본 기능으로 묶어 제공합니다. 배터리 관리 시스템과 도어 제어 모듈 시장의 긴밀한 연동을 통해, 고전압 접촉기가 열려 있는 상태에서도 충돌 후 도어를 안전하게 해제할 수 있습니다. 중국 제조업체들이 이 접근 방식을 선구적으로 도입했으며, 현재는 유사한 아키텍처를 유럽으로 수출하고 있습니다. 고도로 통합된 드라이버 IC를 제공하는 업체는 레이아웃 간소화, 하네스 경량화, 검증 주기 단축을 실현할 수 있어 설계 채택을 확보하고 있습니다.

ADAS 지원 스마트 도어 모듈의 도입 확대

첨단 운전자 보조 기능은 전방 감시 카메라에 그치지 않고, 도어 패널 내부에 탑재된 측면 감시 레이더까지 확대되고 있습니다. 이 센서들은 자전거가 접근하면 문을 잠그고, 통행로가 확보되는 시점에 잠금을 해제함으로써 '도어링' 사고를 예방합니다. Euro NCAP이 이러한 기능에 대해 안전 평가 점수를 부여하고 있기 때문에 주요 자동차 브랜드들은 고급차 부문에서 이를 선점하기 위해 경쟁하고 있습니다. 레이더나 카메라 데이터는 변조 방지가 필수적이므로, 현재 도어용 ECU에는 보안 부팅 및 인증 기반 펌웨어 업데이트 프로세스가 탑재되어 있습니다. 이러한 요건은 하드웨어 기반 신뢰 경로를 내장한 반도체 공급업체에 유리하게 작용합니다. 그 결과, 더욱 탄탄한 기술 스택이 구축됨에 따라 도어 제어 모듈 시장은 파워트레인 및 ADAS 분야와 동등한 수준의 엄격한 사이버 보안 기준을 향해 나아가고 있습니다.

반도체 공급 변동

메모리 공급업체들이 AI 데이터센터용 고대역폭 제품으로 생산 능력을 전환함에 따라, 자동차 제조업체들은 기존 DRAM 공급 부족에 직면해 있습니다. 2025년 하반기에는 리드타임이 불과 몇 주로 단축되어, 모듈 통합업체들은 프로그램이 확정되기 훨씬 전에 취소 불가능한 주문을 해야만 하는 상황에 처하게 됩니다. 일부 자동차 제조업체들은 현재 새로운 메모리 규격에 대응하기 위해 컨트롤러를 재설계하고 있어, 비용과 엔지니어링 부담이 증가하면서 출시가 지연되고 있습니다. 그 결과, 플랫폼 소유자가 부품 공급이 안정될 때까지 선택 사양의 편의 장비 도입을 연기하고 있어, 도어 제어 모듈 시장은 정체 상태에 있습니다.

부문별 분석

2025년 기준으로, 집중형 컨트롤러는 도어 제어 모듈 시장의 60.55% 점유율을 차지했습니다. 4개의 도어를 모두 단일 ECU로 통합함으로써 CAN 노드 수와 소프트웨어의 유형을 줄일 수 있어, 생산 주기가 긴 대량 생산 플랫폼에 매력적인 솔루션입니다. 엔지니어들은 이 레이아웃이 제공하는 예측 가능한 전력 예산과 간소화된 진단 체계를 높이 평가했습니다. 그러나 와이어 하네스의 무게가 늘어나고 기능이 다양해짐에 따라, 1그램의 경량화도 중요한 전기자동차(EV) 분야에서는 이 아키텍처의 매력이 점차 줄어들고 있습니다.

연평균 성장률(CAGR) 8.51%로 성장하고 있는 분산형 또는 존형 유닛은 개별 도어 간에 연산 능력을 분산시키고, 하네스 길이를 단축하며, 설계자가 로컬 코드만 수정하여 기능을 추가할 수 있도록 합니다. 이러한 모듈성은 업그레이드를 통해 각 도어별로 휴면 상태의 하드웨어를 활성화할 수 있게 해주므로, 새롭게 등장한 소프트웨어 구독 모델과 잘 부합합니다. 바이너리 크기가 줄어들면 무선 업데이트도 더 빠르게 완료되어 고객 경험이 향상됩니다. 차내 여러 설치 위치에 사용할 소형 컨트롤러를 사전에 검증한 공급업체는 더 많은 세계 플랫폼을 확보할 가능성이 높으며, 이는 도어 제어 모듈 시장의 점진적인 변화를 시사합니다.

도어 제어 모듈 시장에서 2025년에는 도어 잠금 모듈이 시장 점유율의 42.42%를 차지했습니다. 패시브 엔트리, 충돌 시 잠금 해제 연동 및 어린이 안전 기능의 통합으로 인해, 다른 도어 기능들이 중앙 차체 컨트롤러로 이전되더라도 이 하위 부문은 여전히 필수적인 역할을 수행할 것입니다. 또한, 록 모터의 물리적 특성상 교체 주기는 마모 정도에 따라 달라지기 때문에 애프터마켓 채널에서 수요가 확보됩니다.

연평균 성장률(CAGR) 11.07%로 가장 빠르게 성장하고 있는 하위 부문인 일렉트로크로믹 미러 컨트롤러는 눈부심 감소 및 카메라 기반 후방 시야 확보에 대한 프리미엄 수요에 힘입어 성장하고 있습니다. 이러한 미러에는 동적 전압 제어와 광 센서가 필요하기 때문에 관련 ECU는 기본적인 윈도우 리프터보다 더 정교한 아날로그 프런트엔드를 탑재하고 있는 경우가 많습니다. 현재 미러, 방향지시등, 실내 조명을 단일 LIN 노드 아래로 통합하는 추세가 나타나고 있으며, 고급차 등급 이외의 분야로 보급이 확대될 길이 열리고 있습니다.

지역별 분석

도어 제어 모듈 시장에서는 아시아태평양이 주도적인 위치를 차지하고 있으며, 2025년에는 39.12%의 점유율을 기록할 것으로 전망됩니다. 중국의 전기차 급속한 보급과 한국의 메카트로닉스 분야에 대한 지속적인 투자가 이 지역의 지속적인 우위를 뒷받침하고 있습니다. 인도의 현지 1차 공급업체들은 지역 내 OEM 업체와 수출처 고객 모두에 제품을 공급하기 위해 생산 능력을 확대하고 있으며, 이로 인해 해당 지역 공급망에서 그 중요성이 더욱 커지고 있습니다. 또한, 해당 지역에서 소프트웨어 정의 차량(SDV)의 성장세 역시 고도로 통합된 컨트롤러에 대한 수요를 가속화하고 있습니다.

남미는 절대 규모로는 작지만, 연평균 성장률(CAGR) 8.83%로 가장 빠르게 성장하고 있는 지역입니다. 아시아 공급업체를 통한 니어쇼어링으로 관세 위험이 줄어들었고, 브라질과 아르헨티나의 조립 공장으로의 납기 기간이 단축되었습니다. 멕시코에서 부상하고 있는 새로운 무역 회랑은 수입된 전자 부품과 현지에서 프레스 가공된 케이스를 결합한 하이브리드 생산 모델을 촉진하고 있으며, 향후 지역 연구개발(R&D)의 기반을 마련하고 있습니다.

북미와 유럽은 자동차 보급률이 성숙 단계에 접어들었기 때문에 성장이 비교적 완만합니다. 미국의 안전벨트 착용 알림 장치에 관한 새로운 안전 규제와 유로 NCAP의 어린이 탑승 감지 평가 기준이 선택적 기능 업그레이드를 촉진하고 있지만, 거시경제에 대한 경계감으로 인해 판매 대수는 주춤하고 있습니다. 그러나 강력한 애프터마켓 네트워크가 그 영향을 완화하고 있어, 구형 차량에 도어 모듈을 사후 장착하는 것이 널리 보급되고 있습니다. 전반적으로, 이러한 지역별 수요 패턴은 공급업체로 하여금 선진 시장의 첨단 기술 요구 사항과 성장 지역의 비용 중심 요구 사항 사이의 균형을 맞추도록 요구하고 있으며, 이는 도어 제어 모듈 시장 전체의 투자 동향을 형성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

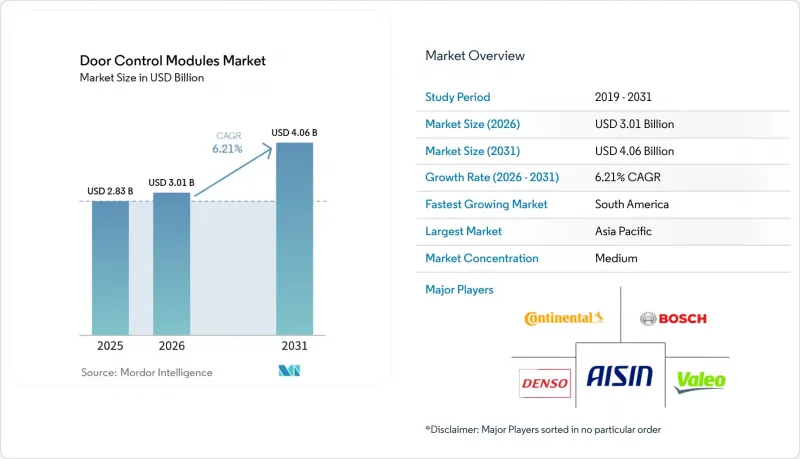

AJY 26.06.22According to Mordor Intelligence, the door control modules market size is expected to grow from USD 2.83 billion in 2025 to USD 3.01 billion in 2026, and is forecast to reach USD 4.06 billion by 2031, growing at a CAGR of 6.21% from 2026 to 2031.

This report is Segmented by Type (Centralized Door Control Modules, and More), Application (Door Lock, Mirror Adjustment, Window Lift, Illumination, and More), Component (Actuators, Sensors, and More), Sales Channel (OEM and Aftermarket), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Door Control Modules Market Trends and Insights

Electrification Boosting Electronic Content Per Door

Electric-vehicle platforms provide ample low-voltage power, enabling body engineers to integrate gesture control, radar-based obstacle sensing, and battery-disconnect logic in a single door controller. More functions per controller translate into larger software footprints, so tier-one suppliers now bundle AUTOSAR stacks and cybersecurity libraries as default features. Tight coordination between the battery-management system and the door control modules market enables safe post-crash unlocking even when high-voltage contactors are open. Chinese manufacturers pioneered the approach and now export similar architectures to Europe. Component vendors that ship highly integrated driver ICs are gaining design wins because they simplify layout, shrink harness weight, and cut validation cycles.

Rising Adoption of ADAS-Ready Smart Door Modules

Advanced driver-assistance features have grown beyond forward-looking cameras to include side-looking radar inside door skins. These sensors prevent "dooring" incidents by locking a door if a cyclist approaches, then releasing it once the path is clear. Euro NCAP awards safety credit for such functions, so mainstream brands are following earlier luxury-segment deployments. Because radar and camera data must remain tamper-proof, door ECUs now incorporate secure boot and authenticated firmware update processes, requirements that favor silicon suppliers with built-in hardware root of trust. The upshot is a richer technology stack that pushes the door control modules Market toward the same cybersecurity rigor as powertrain and ADAS domains.

Semiconductor Supply Volatility

Memory vendors have shifted capacity to high-bandwidth products for AI data centers, leaving automotive customers short on legacy DRAM. Lead times tightened to just a few weeks in late 2025, forcing module integrators to place non-cancellable orders long before program freeze. Some automakers now redesign controllers to support newer memory standards, adding cost and engineering overhead that stalls launches. The result is a drag on the door control modules market as platform owners delay optional comfort features until component availability stabilizes.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Passive Keyless Entry Systems

- Ageing Vehicle Parc Driving Aftermarket Replacements

- Price Pressure on Tier-1 Suppliers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centralized controllers held 60.55% of the Door Control Modules market share in 2025. Integrating all four doors into a single ECU reduces the CAN node count and software variants, appealing to high-volume platforms with long production lifecycles. Engineers appreciate the predictable power budget and simplified diagnostic schemes that accompany this layout. However, the weight of wiring harnesses and the increasing diversity of features are making the architecture less attractive for electric vehicles, where every gram matters.

Decentralized or zonal units, advancing at an 8.51% CAGR, split compute power between individual doors, trimming harness length, and letting designers add features by flashing only local code. This modularity aligns with emerging software subscription models because upgrades can activate dormant hardware on a per-door basis. Over-the-air updates also complete faster when the binary size shrinks, improving customer experience. Suppliers that pre-validate smaller controllers for multiple locations in the vehicle stand to win more global platforms, signaling a gradual pivot in the door control modules market.

Door-lock modules controlled 42.42% of the Door Control Modules market share in 2025 within the Door Control Modules Market. Passive entry, crash unlock coordination, and child-safety integration keep this sub-segment essential even when other door functions migrate to central body controllers. The lock motor's physical nature also means replacement cycles are tied to wear, ensuring volume for aftermarket channels.

Electrochromic-mirror controllers, the fastest sub-segment at 11.07% CAGR, ride on premium demand for glare reduction and camera-based rear visibility. Because these mirrors require dynamic voltage control and light sensing, the associated ECU often carries richer analog front ends than a basic window lift. Integration trends now merge mirror, indicator, and ambient lighting under a single LIN node, paving the way for wider adoption beyond luxury tiers.

Geography Analysis

Asia-Pacific leads the Door Control Modules Market, holding 39.12% share in 2025. Rapid electric-vehicle rollout in China and sustained investment in South Korean mechatronics underwrite continued dominance. Local tier-ones expand capacity in India to supply both regional OEMs and export customers, further reinforcing the area's supply-chain gravity. The region's software-defined-vehicle momentum also accelerates demand for highly integrated controllers.

South America, while smaller in absolute terms, is the fastest-growing territory at 8.83% CAGR. Near-shoring by Asian suppliers reduces tariff exposure and shortens delivery times for Brazilian and Argentine assembly plants. Emerging trade corridors in Mexico encourage hybrid production models that pair imported electronics with locally stamped housings, seeding a base for future regional R&D.

North America and Europe grow more modestly as vehicle penetration is mature. New safety rules on seat-belt reminders in the United States and Euro NCAP child-presence scoring drive selective feature upgrades, but macroeconomic caution tempers unit volumes. Strong aftermarket networks, however, cushion the impact, allowing retrofit door-modules to proliferate in older fleets. Overall, geographic demand patterns force suppliers to balance high-tech requirements of advanced markets with cost-sensitive needs of growth regions, shaping investment across the door control modules market.

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- Valeo SA

- Aisin Corporation

- Hella GmbH and Co. KGaA

- Mitsuba Corporation

- Kiekert AG

- Lear Corporation

- LG Electronics

- Magna International

- Visteon Corporation

- Brose Fahrzeugteile

- Strattec Security

- Huf Hulsbeck and Furst

- Minth Group

- Seoyon Electronics

- Omron Automotive

- Shanghai STEC

- Beijing Hainachuan Auto Parts

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification Boosting Electronic Content Per Door

- 4.2.2 Rising Adoption Of ADAS-Ready Smart Door Modules

- 4.2.3 Surge In Passive Keyless Entry Systems

- 4.2.4 Ageing Vehicle Parc Driving Aftermarket Replacements

- 4.2.5 OTA-Capable Cyber-Secure Module Demand

- 4.2.6 Child-Presence Detection Mandates

- 4.3 Market Restraints

- 4.3.1 Semiconductor Supply Volatility

- 4.3.2 Price Pressure on Tier-1 Suppliers

- 4.3.3 Harsh-Environment Reliability Challenges

- 4.3.4 Shift to Solid-State E-Latches

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Type

- 5.1.1 Centralized Door Control Modules

- 5.1.2 Decentralized Door Control Modules

- 5.2 By Application

- 5.2.1 Door Lock

- 5.2.2 Mirror Adjustment

- 5.2.3 Window Lift

- 5.2.4 Illumination

- 5.2.5 Mirror Defroster

- 5.2.6 Central Locks and Child Lock

- 5.2.7 Electrochromic Mirror

- 5.3 By Component

- 5.3.1 Actuators

- 5.3.2 Sensors

- 5.3.3 Wires

- 5.3.4 Switches

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 Spain

- 5.5.3.4 Italy

- 5.5.3.5 France

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Denso Corporation

- 6.4.4 Valeo SA

- 6.4.5 Aisin Corporation

- 6.4.6 Hella GmbH and Co. KGaA

- 6.4.7 Mitsuba Corporation

- 6.4.8 Kiekert AG

- 6.4.9 Lear Corporation

- 6.4.10 LG Electronics

- 6.4.11 Magna International

- 6.4.12 Visteon Corporation

- 6.4.13 Brose Fahrzeugteile

- 6.4.14 Strattec Security

- 6.4.15 Huf Hulsbeck and Furst

- 6.4.16 Minth Group

- 6.4.17 Seoyon Electronics

- 6.4.18 Omron Automotive

- 6.4.19 Shanghai STEC

- 6.4.20 Beijing Hainachuan Auto Parts

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment