|

시장보고서

상품코드

2063280

영국의 자동차 인포테인먼트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United Kingdom Automotive Infotainment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

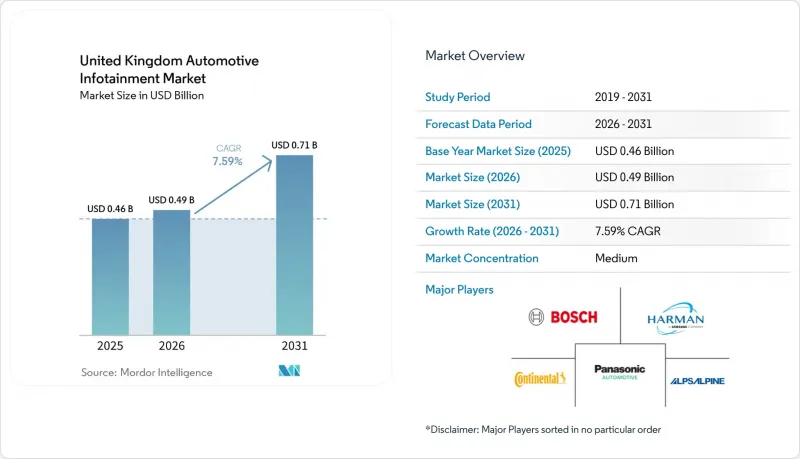

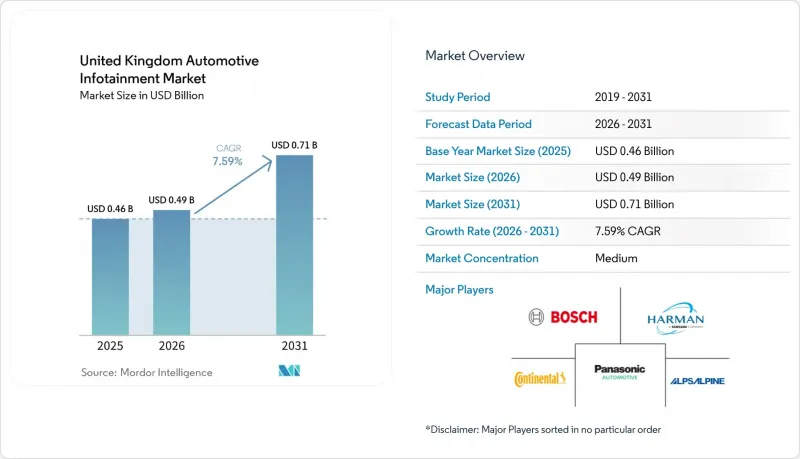

Mordor Intelligence에 의하면, 영국의 자동차 인포테인먼트 시장 규모는 2025년에 4억 6,000만 달러로 평가되었습니다. 2026년 4억 9,000만 달러에서 2031년까지 7억 1,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR은 7.59%를 나타낼 전망입니다.

본 보고서는 설치 유형(대시보드 내장형 인포테인먼트 및 뒷좌석용 인포테인먼트), 차종(승용차, 소형 상용차 등), 구성 요소(디스플레이/터치스크린 모듈, 헤드 유닛/도메인 컨트롤러 등), 구동 방식, 커넥티비티 세대, 운영 체제, 판매 채널별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

영국의 자동차 인포테인먼트 시장 동향과 인사이트

전기차 보급이 가속화됨에 따라, 더욱 풍부한 HMI 경험이 요구되고 있습니다.

2025년 BEV(배터리식 전기차)의 등록 대수는 47만 3,348대에 달했으며, 이는 신차 판매의 23.4%를 차지했습니다. 또한, 2026년 초의 수치는 인센티브가 축소되었음에도 불구하고 그 기세가 계속되고 있음을 보여줍니다. 배출가스 제로 모델 구매자들은 더 넓은 OLED 패널, 증강현실(AR) 내비게이션, 충전 일정을 설정할 수 있는 음성 비서 등을 기대하고 있기 때문에 각 OEM 업체들은 디스플레이 혁신과 소프트웨어 생태계에 대한 투자를 확대되고 있습니다. 집중형 전기 아키텍처 덕분에 기둥 사이를 덮는 스크린을 설치할 수 있는 차량 내 공간이 확보되었으며, 한편 무선 업데이트(OTA)는 지속적인 수익원을 창출하고 있습니다. 정부의 자금 지원에 힘입어 충전 네트워크 통합이 가속화되면서, 공급업체들에게는 확실한 사업 기회가 열리고 있습니다. BEV의 보급과 콕핏 컨텐츠 간의 선순환 효과로 인해, 이 하위 부문은 두 자릿수 성장세를 유지하고 있습니다.

커넥티드카 및 스마트폰 연동 기능에 대한 수요 증가

소비자들은 스마트폰과 대시보드 간의 원활한 연동을 원하고 있으며, 이것이 자동차 제조업체들이 엄선한 앱 스토어의 도입을 촉진하고 있습니다. 그러나 규제 당국은 화면 조작과 운전 중 주의 산만으로 인한 사고를 연관 짓고 있기 때문에 공급업체들은 운전자의 주의가 산만해질 때 디스플레이 밝기를 낮추는 운전자 모니터링 카메라를 통합하고 있습니다. 사용 편의성과 규정 준수의 균형을 맞추는 것이 사용자 인터페이스의 로드맵을 형성하며, 커넥티드 서비스의 도입을 꾸준히 증가시키고 있습니다.

고성능 디스플레이 및 프로세서의 높은 비용

OEM 업체들이 배터리 비용 절감 방안을 모색하고 있는 바로 그 시점에, 메모리와 OLED 패널 가격이 급등하면서 공급업체들의 이익률을 압박하고 있습니다. 대형 기존 기업들은 수직 통합이나 장기 공급 계약을 통해 이러한 압박을 완화하고 있지만, 중소규모의 2차 공급업체들은 프로젝트 지연 위험에 직면해 있습니다. 가격 변동성은 단기적으로 디스플레이 시장의 확장을 억제하고, 성장 전망을 소폭 둔화시킬 가능성이 있습니다.

부문별 분석

2025년, 영국의 자동차 인포테인먼트 시장에서 인대시 시스템은 85.15%의 점유율을 차지했습니다. 이러한 우위는 내비게이션, 미디어, 운전 지원 정보를 하나의 화면에 통합한 주요 인간-기계 인터페이스라는 점에 기인합니다. 자동차 제조업체들은 안전 규제 당국과 기술에 정통한 운전자의 요구를 충족시키기 위해, 더욱 고해상도의 그래픽, 적응형 위젯, 음성 우선 조작 기능을 활용하여 이러한 전면 디스플레이를 개선하고 있습니다. 이 공급업체는 칩 제조업체 및 UI 스튜디오와 협력하여 지연 시간을 줄이는 동시에, 계기판과 센터 스크린 간에 매끄럽게 전환되는 상황 인식형 컨텐츠를 제공합니다. 지속적인 무선 업데이트를 통해 하드웨어를 교체할 필요 없이 인터페이스를 최신 상태로 유지할 수 있습니다.

후석용 시스템 시장은 2031년까지 연평균 성장률(CAGR) 8.54%로 확대되고 있으며, 이는 차량용 시스템 시장 내에서 가장 높은 성장률입니다. 고급 자동차 브랜드와 차량 공유 업체들은 승객 한 명 한 명에게 화면을 제공하는 것을, 높은 요금을 정당화하는 차별화 요인으로 보고 있습니다. 전기자동차의 실내 레이아웃 덕분에 더 큰 시트 등받이 패널을 설치할 수 있는 공간이 확보되었으며, 5G 연결을 통해 각 승객은 버퍼링 없이 맞춤형 컨텐츠를 스트리밍할 수 있습니다. 각 통합 업체들은 무선 캐스팅, 멀티존 오디오, 자녀 보호 모드를 추가하여, 임원용 셔틀 이외의 분야에서도 매력을 넓혀가고 있습니다. 그 결과, 서비스 수익 증가가 기내 엔터테인먼트의 추가적인 혁신을 촉진하는 선순환이 형성되고 있습니다.

2025년, 영국의 자동차 인포테인먼트 시장 점유율 중 67.13%를 승용차가 차지했습니다. 이러한 방대한 잠재 고객층 덕분에 제조업체는 대량 생산을 통해 소프트웨어 개발 비용을 상쇄할 수 있게 되었으며, 이로 인해 보급형 모델에서도 기능이 풍부한 계기판을 구현하는 데 박차를 가하고 있습니다. 신규 진출기업들의 경쟁 압박으로 인해 기존 제조업체들은 제품 주기를 단축하고, 스마트폰과 같은 생태계를 통합해야 하는 상황에 몰리고 있습니다. 소비자들은 이제 직관적인 음성 비서, 스마트폰과의 원활한 연동, 클라우드에 동기화된 설정을 기본 기능으로 기대하고 있습니다. 이러한 기대에 힘입어 인포테인먼트는 ‘있으면 편리한 것’에서 구매의 주요 판단 기준으로 위상이 높아졌습니다.

이 부문은 가장 빠른 성장세를 보이고 있으며, 2031년까지 연평균 성장률(CAGR) 10.47%를 나타낼 전망입니다. 정숙성이 뛰어난 파워트레인 덕분에 차량 내부의 음향 환경과 화면의 선명도가 주목받고 있어, 각 OEM 업체들은 필러 사이를 감싸는 OLED 바와 증강현실(AR) 내비게이션을 탑재하여 감각적인 경험을 높이고 있습니다. 통합된 전자 아키텍처를 통해 에너지 사용량을 관리하거나 급속 충전기를 검색하는 등의 새로운 앱을 쉽게 추가할 수 있게 됩니다. 제로 에미션 차량을 지원하는 규제 당국은 인센티브를 커넥티드 서비스의 확대와 연계함으로써 더욱 큰 추진력을 창출하고 있습니다. 이러한 요인들이 복합적으로 작용하여, BEV의 인포테인먼트는 미래 디자인 언어의 지표가 되고 있습니다.

2025년, 디스플레이 모듈은 영국의 자동차 인포테인먼트 시장 점유율의 45.25%를 차지하며 최대의 단일 하드웨어 구성 요소가 되었습니다. 각 패널 제조업체들은 치열해지는 경쟁 속에서 주도권을 유지하기 위해, 더욱 얇아진 적층 구조와 밝기 향상에 투자하고 있습니다. 자동차 디자이너들은 이러한 기술 발전을 활용하여 계기판과 센터 스크린을 일체화한 유리 콕핏으로 융합하는 곡면 디자인을 창출하고 있습니다. 한편, 접착제 및 라미네이트 공급업체들은 눈부심을 줄이고 터치 반응성을 높이는 광학 접착 기술을 지속적으로 발전시키고 있습니다. 이러한 협력을 통해 얻은 성과는 콕핏의 가치 창출에서 패널이 차지하는 핵심적 위상을 강화하고 있습니다.

OS 소프트웨어와 앱은 연평균 성장률(CAGR) 8.15%로 성장하고 있으며, 이는 구성 요소 중 가장 높은 성장률입니다. 비즈니스 모델이 지속적인 수익 창출로 전환됨에 따라, OTA(무선 업데이트)를 통해 제공되는 기능은 하드웨어의 이익률보다 수익성이 더 높은 것으로 나타나고 있습니다. 자동차 제조업체들은 내비게이션, 스트리밍, 진단 기능을 구독 서비스로 묶어 자사 브랜드의 앱 스토어를 운영하고 있습니다. 개발자들이 이러한 스토어를 타겟으로 삼는 이유는 설치 기반이 확실한 수익 창출을 보장하기 때문입니다. 플랫폼 소유자와 컨텐츠 제공업체 간의 이러한 공생 관계로 인해, 협상력은 차량의 매력을 장기간 유지할 수 있는 소프트웨어 기업 쪽으로 이동하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the united kingdom automotive infotainment market size was valued at USD 0.46 billion in 2025 and is expected to increase from USD 0.49 billion in 2026 to reach USD 0.71 billion by 2031, growing at a 7.59% CAGR over 2026-2031.

This report is Segmented by Installation Type (In-Dash Infotainment and Rear-Seat Infotainment), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component (Display/Touch-screen Module, Head Unit/Domain Controller, and More), Propulsion Type, Connectivity Generation, Operating System, and Sales Channel. The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Automotive Infotainment Market Trends and Insights

Accelerated EV Adoption Requiring Richer HMI Experiences

BEV registrations reached 473,348 units in 2025, equal to 23.4% of new-car sales, and early-2026 figures show continued momentum despite tapering incentives. Buyers of emission-free models expect wider OLED panels, augmented-reality navigation, and voice assistants that schedule charging, so OEMs invest in display innovation and software ecosystems. Centralized electrical architectures free cabin space for pillar-to-pillar screens, while over-the-air updates create durable revenue streams. Government funding accelerates charging-network integration, giving suppliers a clear commercial path. The positive feedback loop between BEV uptake and cockpit content sustains double-digit growth for this sub-segment.

Rising Demand for Connected-Car and Smartphone-Integrated Features

Consumers want seamless handoffs between phones and dashboards, driving the adoption of automaker-curated app stores. Regulators, however, link screen interaction to distracted-driving incidents, so suppliers integrate driver-monitoring cameras that dim displays when attention strays. Balancing convenience and compliance shapes the user interface roadmap and keeps connected-service adoption on a steady climb.

High BOM Cost for Advanced Displays and Processors

Sharp increases in memory and OLED panel pricing squeeze supplier margins just when OEMs seek cost offsets for batteries. Larger incumbents mitigate pressure through vertical integration and long-term supply contracts, yet smaller tier-twos risk program delays. Price volatility may temper near-term display-area expansion, slightly dampening growth expectations.

Other drivers and restraints analyzed in the detailed report include:

- Nationwide 5G Roll-Out Enabling High-Bandwidth In-Car Services

- Centralized Domain Controllers in Software-Defined Vehicles

- Driver-Distraction Regulations Limiting Visual UX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In-dash systems held 85.15% of the United Kingdom automotive infotainment market share in 2025. Their dominance stems from being the primary human-machine interface, combining navigation, media, and driver-assistance cues in a single focal point. Carmakers refine these front-row displays with richer graphics, adaptive widgets, and voice-first controls to satisfy safety regulators and tech-savvy drivers. Suppliers collaborate with chipmakers and UI studios to reduce latency and deliver context-aware content that shifts seamlessly between the cluster and the center screen. Continuous over-the-air updates keep the interface up to date without requiring hardware swaps.

Rear-seat systems are expanding at an 8.54% CAGR through 2031, the fastest rate within the installation segment. Luxury brands and ride-hailing fleets view individual passenger screens as a differentiator that justifies premium fares. Electric-vehicle floor layouts free space for larger seat-back panels, while 5G connectivity lets each rider stream personalized content without buffering. Integrators are adding wireless-casting, multi-zone audio, and parental-control modes to broaden appeal beyond executive shuttles. The result is a virtuous circle in which rising service revenues encourage still more cabin-entertainment innovation.

Passenger cars accounted for 67.13% of the United Kingdom automotive infotainment market share in 2025. Their large addressable base lets manufacturers amortize software-development costs across high volumes, encouraging feature-rich dashboards even in entry trims. Competitive pressure from new entrants pushes incumbents to shorten release cycles and integrate smartphone-style ecosystems. Consumers now expect intuitive voice assistants, seamless phone pairing, and cloud-synced preferences as standard equipment. These expectations elevate infotainment from a nice-to-have to a central purchase criterion.

The segment posts the fastest growth, advancing at a 10.47% CAGR through 2031. Silent powertrains spotlight cabin acoustics and screen clarity, so OEMs fit pillar-to-pillar OLED bars and augmented-reality navigation to heighten the sensory experience. Centralized electronic architectures simplify adding new apps that manage energy use or locate high-speed chargers. Regulators rewarding zero-emission fleets add momentum by aligning incentives with connected services rollouts. Together, these factors make BEV infotainment a bellwether for future design language.

Display modules accounted for 45.25% of the United Kingdom automotive infotainment market share in 2025, making them the largest single hardware component. Panel makers invest in thinner stacks and improved brightness to maintain leadership amid rising competition. Automotive stylists use these advances to create curved surfaces that blend clusters and center screens into unified glass cockpits. Adhesive and lamination suppliers, meanwhile, refine optical bonding techniques that reduce glare and enhance touch response. These collaborative gains reinforce the panel's position at the heart of cockpit value creation.

Operating-system software and apps are climbing at an 8.15% CAGR, the fastest within the component mix. As business models tilt toward recurring revenue, OTA-delivered features become more lucrative than hardware margins. Carmakers curate branded app stores, bundling navigation, streaming, and diagnostics under subscription umbrellas. Developers target these storefronts because the installed base ensures predictable monetization. This symbiosis between platform owners and content providers shifts bargaining power toward software firms that can keep vehicles fresh over time.

List of Companies Covered in this Report:

- Robert Bosch GmbH

- Harman International

- Continental AG

- Panasonic Automotive Systems Co., Ltd.

- Alps Alpine

- Pioneer Corporation

- DENSO Corporation

- Visteon Corporation

- Aptiv PLC

- Magna International

- Valeo SA

- Hyundai Mobis Co., Ltd.

- Forvia SE

- JVC Kenwood

- BlackBerry Limited (QNX)

- Google LLC

- Qualcomm Technologies, Inc.

- NXP Semiconductors N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated EV Adoption Requiring Richer HMI Experiences

- 4.2.2 Rising Demand for Connected-Car and Smartphone-Integrated Features

- 4.2.3 Nationwide 5G Roll-Out Enabling High-Bandwidth In-Car Services

- 4.2.4 Centralized Domain Controllers in Software-Defined Vehicles

- 4.2.5 Usage-Based-Insurance Data Monetization via Infotainment

- 4.2.6 Mobility-as-a-Service and Ride-Hailing Comfort Differentiation

- 4.3 Market Restraints

- 4.3.1 High BOM Cost for Advanced Displays and Processors

- 4.3.2 Driver-Distraction Regulations Limiting Visual UX

- 4.3.3 Legacy Fleet Retrofit Complexity and CAN-Bus Variance

- 4.3.4 Escalating Cyber-Insurance Premiums for Connected Vehicles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Installation Type

- 5.1.1 In-dash Infotainment

- 5.1.2 Rear-seat Infotainment

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.3 By Component

- 5.3.1 Display / Touch-screen Module

- 5.3.2 Head Unit / Domain Controller

- 5.3.3 Operating-System Software and Apps

- 5.3.4 Connectivity ICs and Antenna Modules

- 5.4 By Propulsion Type

- 5.4.1 Internal-Combustion Engine Vehicles

- 5.4.2 Hybrid Electric Vehicles

- 5.4.3 Battery Electric Vehicles

- 5.5 By Connectivity Generation

- 5.5.1 4G LTE

- 5.5.2 5G

- 5.5.3 Legacy 2G/3G

- 5.6 By Operating System

- 5.6.1 Linux-Based (AAOS, AGL, etc.)

- 5.6.2 QNX

- 5.6.3 Android Automotive OS

- 5.6.4 Others (Proprietary, RTOS)

- 5.7 By Sales Channel

- 5.7.1 OEM-Installed

- 5.7.2 Aftermarket

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Harman International

- 6.4.3 Continental AG

- 6.4.4 Panasonic Automotive Systems Co., Ltd.

- 6.4.5 Alps Alpine

- 6.4.6 Pioneer Corporation

- 6.4.7 DENSO Corporation

- 6.4.8 Visteon Corporation

- 6.4.9 Aptiv PLC

- 6.4.10 Magna International

- 6.4.11 Valeo SA

- 6.4.12 Hyundai Mobis Co., Ltd.

- 6.4.13 Forvia SE

- 6.4.14 JVC Kenwood

- 6.4.15 BlackBerry Limited (QNX)

- 6.4.16 Google LLC

- 6.4.17 Qualcomm Technologies, Inc.

- 6.4.18 NXP Semiconductors N.V.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment