|

시장보고서

상품코드

2063296

언더 필 디스펜서 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Underfill Dispenser - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

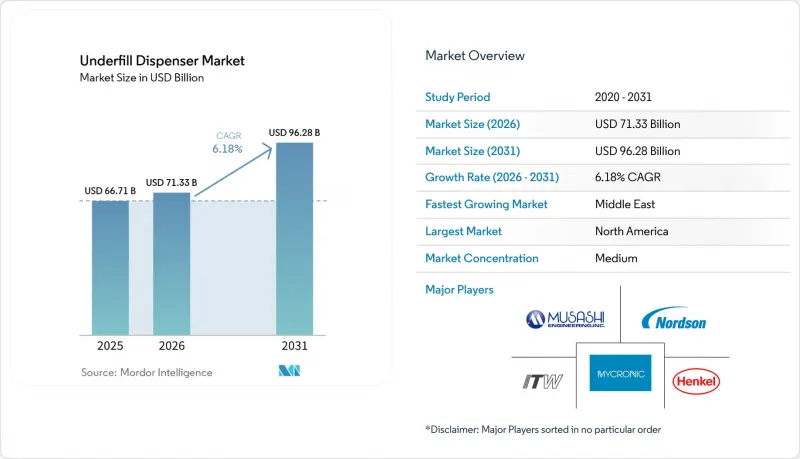

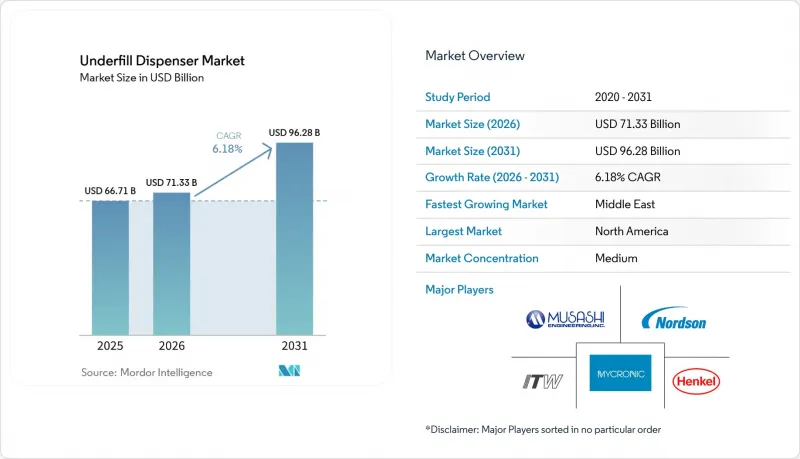

Mordor Intelligence에 의하면, 언더 필 디스펜서 시장 규모는 2025년에 667억 1,000만 달러로 평가되었고, 2026년 713억 3,000만 달러로 추정되고, 2031년까지 962억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.18%를 나타낼 전망입니다.

본 보고서는 제품 유형별(모세관 유동, 언더필, 디스펜서 등), 기술별(압전 제트, 공압 니들 등), 용도별(플립 칩 패키징 등), 최종 사용자별(반도체 조립 및 테스트 수탁 기업(OSAT) 등), 디스펜싱 용량 범위별(5나노리터 미만 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러)으로 제시되어 있습니다.

세계의 언더필 디스펜서 시장 동향 및 분석

AI로 최적화된 디스펜싱 경로 계획으로 사이클 타임을 단축

비전 시스템에 통합된 머신러닝 알고리즘은 규칙 기반 프로그래밍과 비교하여 언더필 공정의 사이클 타임을 15-25% 단축하는 디스펜스 경로를 생성합니다. 이는 Coherix사가 2025년에 TSMC의 CoWoS 패키징 라인에 도입한 3D 비전 검사 시스템에 탑재된 기능입니다. 이 모델들은 표면 형상, 기판의 뒤틀림, 리플로우 온도 이력을 평가하여 노즐의 접근 각도와 압력을 실시간으로 조정합니다. 이 기술을 도입한 주요 조립 제조업체에 따르면, 레시피 개발 시간이 50시간에서 10시간 미만으로 단축되어, 엔지니어링 자원을 새로운 패키지의 인증 작업에 투입할 수 있게 되었습니다. 신뢰성 향상은 실리콘 카바이드(SiC) 파워 모듈에서 두드러집니다. 이 분야에서는 비뉴턴 유체인 언더필 재료가 요구하는 압력 프로파일을 기존의 규칙 기반 제어기로는 유지할 수 없었습니다. 또한, 경로 계획의 고속화를 통해 설비 가동률이라는 중요한 지표도 향상됩니다. 이는 최상위급 제트 시스템의 자본 비용이 100만 달러를 초과하기 때문입니다.

고밀도 이종 통합 패키지 채택

칩렛 토폴로지는 인공지능 가속기나 고성능 CPU에 널리 채택되어 있으며, 다이 간 범프 피치를 40마이크로미터 미만으로 낮추고 있습니다. 언더필 재료는 솔더 접합부 간의 브리징을 방지하기 위해 2마이크로미터 이하의 필러 입자를 함유해야 하며, 디스펜서는 ±1마이크로미터의 정밀도로 1-4나노리터의 도트를 분사할 수 있어야 합니다. 듀얼 밸브 방식 제트 플랫폼은 현재 모세관 유동계와 성형계 언더필 재료를 순식간에 전환할 수 있어, 라인 전환 시간을 90분에서 15분으로 단축했습니다. 동일한 교대 근무 시간 내에 여러 기판 레이아웃을 처리하는 조립 제조업체로부터 처리량이 20-25% 향상되었다는 보고가 있었으며, 이는 언더필 디스펜서 시장에서 정밀 제트 기술의 높은 경쟁력을 입증해 주고 있습니다.

첨단 제트 플랫폼에 대한 막대한 설비 투자액

인라인 비전, 듀얼 밸브 구성, 클래스 100 인클로저를 통합한 차세대 압전식 제트 디스펜서의 가격대는 대당 80만-120만 달러입니다. 기존의 볼 그리드 어레이(BGA) 패키지를 낮은 이익률로 처리하고 있는 중소규모의 조립 업체들은 외부 자금 없이는 이러한 비용을 감당할 수 없습니다. 반도체 제조 장비 업계의 총 설비 투자액은 2026년에 2,000억 달러에 달했으나, 언더필 디스펜서의 설비 가동률은 평균 65-70%에 그쳤습니다. 이는 조립 라인이 플립 칩, 볼 그리드 어레이, 웨이퍼 레벨 패키징과 같은 서로 다른 공정 간을 전환하기 때문입니다. 이러한 공정에서는 각각 다른 디스펜싱 레시피가 필요하며, 재료 교체 시 한 번에 2-4시간이 소요되기 때문입니다. 라인 가동률이 평균 65-70%인 경우, 작업자가 1교대당 여러 번 레시피를 변경하게 되므로 ROI(투자 대비 효과) 산정이 더욱 어려워집니다. 그 결과, 많은 2차 공급업체들은 자동차 및 항공우주 프로그램의 공극(void) 목표를 충족하지 못함에도 불구하고, 25만 달러 미만의 가격인 공압식 니들 디스펜서를 계속 선택하고 있습니다.

부문별 분석

2025년 매출액 기준, 제트 디스펜서가 가장 큰 점유율을 차지했으며, 제트 플랫폼용 언더필 디스펜서 시장은 2026-2031년 연평균 성장률(CAGR) 6.77%로 성장할 것으로 전망됩니다. 이러한 비접촉 작동 방식 덕분에 기판의 흠집을 방지하고, 5나노리터 미만의 도트 형성이 가능합니다. 이는 25 마이크로미터 이하로 분리된 치플릿에게 있어 매우 중요한 특성입니다. 모세관 흐름과 제트 헤드를 단일 프레임에 통합한 하이브리드 장비는 설치 면적을 40% 줄여, 공장에서 여러 기존 공정을 단일 라인으로 통합할 수 있게 해줍니다.

점도가 50,000 cP를 초과하는 고점도 실링재 분야에서는 여전히 니들 시스템이 주류를 이루고 있지만, 소재 공급업체들이 압전식 이젝터의 전단 특성에 맞도록 배합을 재검토하고 있어 이에 대한 관심은 점차 줄어들고 있습니다. 비용 절감을 고려할 때, 3-5%의 공극률이 허용 범위로 간주되는 소비자용 전자기기 분야에서는 여전히 모세관 유동식 디스펜서가 중요한 역할을 하고 있습니다. 그럼에도 불구하고, AI를 활용한 경로 계획 덕분에 제트식 플랫폼의 가동률은 80% 가까이 향상되었으며, 총 소유 비용(TCO)의 차이는 줄어들고 있습니다. 그 결과, 언더필 디스펜서 시장에서는 다국적 기업과 지역 밀착형 OSAT(반도체 수탁 조립 업체) 모두에서 조달 예산이 제트식 시스템으로 결정적으로 전환되고 있습니다.

2025년에는 압전 제트 방식이 매출 점유율의 34.54%를 차지한 것으로 평가되었으며, 언더필 디스펜서 시장 내 점유율은 연평균 성장률(CAGR) 6.94%에 기반하여 확대될 전망입니다. 1,500개 이상의 노즐을 탑재한 프린트 헤드는 현재 20kHz로 구동되며, ±2마이크로미터의 위치 정밀도를 유지하면서 시간당 도트 수를 9만 개 이상으로 끌어올렸습니다. 0.5mm 피치의 BGA를 다루는 동남아시아 생산 라인에서는 여전히 공압식 니들 툴이 시장 점유율을 유지하고 있지만, 주요 첨단 패키징 로드맵에는 20마이크로미터 미만의 다이 갭에 대해 압전식 기능의 도입이 명시되어 있습니다.

용적식 펌프와 오거 스크류는 10mL/min을 초과하는 지속적인 유량이 필요한 웨이퍼 레벨 패키징의 틈새 시장을 충족시키고 있으며, 이는 피에조 스택이 대응하기 어려운 유량 범위입니다. 필름 전사 기술은 두께 200μm 미만의 초박형 MEMS 모듈 분야에서 확고한 입지를 다지고 있으나, 폭넓은 화학적 지원이 부족하다는 점이 현재의 성장을 제한하고 있습니다. 전반적으로, 머신 비전 통합의 확대와 실시간 디스펜싱 검증을 통해, 언더필 디스펜서 시장의 주요 이종 통합 프로그램 전반에 걸쳐 압전 기술의 리더십이 확고해지고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 53.73%를 차지했으며, 그 중심에는 대만의 첨단 패키징 공장들이 자리 잡고 있으며, 이곳에서는 총 500대 이상의 고정밀 디스펜서가 가동되고 있습니다. 한국에서는 2026년, 129억 달러 규모의 HBM 복합단지 착공으로 인해 성장세가 가속화되어, 최소 40대의 일류 제트 툴 수주가 확실시되고 있습니다. 중국 본토에서는 국내 GPU 스타트업 기업들이 주도한 2.5D 이니셔티브 덕분에, 수출 규제로 인해 EUV 웨이퍼 생산 능력이 제한되었음에도 불구하고 현지 수요는 두 자릿수 성장세를 보였습니다. 일본은 안정적인 상태를 유지하고 있지만, 보수적인 인증 일정을 중시하는 자동차 업계 고객들이 선호하는 단계적 업그레이드를 제공하는 국내 공급업체에 의존하고 있습니다.

중동은 연평균 성장률(CAGR) 6.57%를 나타낼 것으로 예측되며, 지역별로는 가장 빠르게 성장하고 있습니다. 정부계 펀드는 칩렛 조립 기능을 갖춘 160억 달러 규모의 로직 라인을 포함해 아랍에미리트(UAE)와 사우디아라비아의 여러 팹을 지원하고 있습니다. 지역 정책 목표로 2028년까지 50개의 국내 반도체 기업을 육성하겠다고 밝혔으며, 조달 문서에는 이미 대만에서 사용되고 있는 것과 동일한 나로우갭 언더필 디스펜서가 명시되어 있습니다.

북미와 유럽은 CHIPS법에 따른 인센티브가 국내 패키징 산업을 지원하고 있음에도 불구하고, 엔지니어링 인력 부족으로 어려움을 겪고 있어 한 자릿수 중반대의 성장률을 기록하고 있습니다. 애리조나주와 작센주의 시범 생산 라인에는 정밀 제트 디스펜서가 도입되었으나, 전 세계적으로 웨이퍼 레벨 언더필을 전문으로 하는 엔지니어가 수백 명에 불과하기 때문에 작업자 교육 기간이 길어지고 있는 것으로 보고되고 있습니다. 남미와 아프리카는 여전히 개발도상국이지만, 브라질의 자동차 부품 공급업체가 플렉스 연료 컨트롤러용 보이드 프리 실란트의 인증을 시작함에 따라, 향후 해당 지역의 언더필 디스펜서 시장 수주가 증가할 가능성이 시사되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the underfill dispenser market size was valued at USD 66.71 billion in 2025 and estimated to grow from USD 71.33 billion in 2026 to reach USD 96.28 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031).

This report is Segmented by Product Type (Capillary Flow Underfill Dispensers, and More), Technology (Piezoelectric Jetting, Pneumatic Needle, and More), Application (Flip Chip Packaging, and More), End-User (Outsourced Semiconductor Assembly and Test (OSAT) Companies, and More), Dispensing Volume Range (Less Than 5 Nanolitres, and More), and Geography. The Market Forecasts are Provided in Value (USD).

Global Underfill Dispenser Market Trends and Insights

AI-Optimized Dispense Path Planning Reduces Cycle Time

Machine-learning algorithms embedded in vision systems now generate dispense trajectories that cut underfill cycle time by 15-25%, compared to rule-based programming, a capability that Coherix introduced in its 3D vision inspection systems deployed at TSMC's CoWoS packaging lines in 2025. These models assess the topography, substrate warpage, and reflow temperature history, then adjust nozzle approach angles and pressure in real time. Major assembly houses deploying the technology report that recipe development time has fallen from 50 hours to less than 10, freeing engineering resources for new package qualifications. Reliability gains are notable in silicon carbide power modules, where non-Newtonian underfill chemistries demand pressure profiles that legacy rule-based controllers cannot sustain. Faster path planning also raises equipment utilization, a key metric, as capital costs for top-tier jetting systems exceed USD 1 million.

Adoption of High-Density Heterogeneous Integration Packages

Chiplet topologies permeate artificial-intelligence accelerators and high-performance CPUs, driving die-to-die bump pitch below 40 micrometers. Underfill materials must carry filler particles no larger than 2 micrometers to avoid bridging between solder joints, pushing dispensers to deliver 1-4 nanoliter dots with +-1 micrometer accuracy. Dual-valve jetting platforms now switch instantly between capillary-flow and molded underfill chemistries, reducing line changeover from 90 minutes to 15 minutes. Assembly houses handling multiple substrate layouts inside the same shift report throughput lifts of 20-25%, reinforcing the competitive case for precision jetting in the underfill dispenser market.

High Capex of Advanced Jetting Platforms

Next-generation piezoelectric jetting dispensers bundled with inline vision, dual-valve setups, and Class-100 enclosures command USD 800,000-1,200,000 per unit. Small and mid-size assembly houses that process legacy ball-grid-array packages at modest margins cannot absorb these costs without external financing. The semiconductor equipment industry's aggregate capital expenditure reached USD 200 billion in 2026, yet equipment utilization rates for underfill dispensers averaged 65-70% as assembly lines cycled between flip chip, ball grid array, and wafer-level packaging processes that require different dispense recipes and material changeovers consuming 2-4 hours per transition. The ROI equation becomes more challenging when line utilization averages 65-70%, since crews change recipes several times per shift. Consequently, many second-tier providers still opt for pneumatic needle dispensers priced below USD 250,000, even though those tools cannot meet void targets for automotive or aerospace programs.

Other drivers and restraints analyzed in the detailed report include:

- Transition to 3D Chip-Stacking Demands Void-Free Underfill

- Increasing Demand for Automotive-Grade Power Semiconductors

- Limited Dispensing Throughput for Panel-Level Packaging Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Jet dispensers accounted for the largest share of 2025 revenue, and the underfill dispenser market for jet platforms is forecast to grow at a 6.77% CAGR over 2026-2031. Their non-contact operation eliminates substrate scratches and allows sub-5-nanoliter dots, attributes crucial for chiplets separated by 25 micrometers or less. Hybrid machines that combine capillary-flow and jetting heads in a single frame now cut floor space by 40% and help factories consolidate multiple legacy processes onto a single line.

Needle systems still dominate high-viscosity encapsulants above 50,000 cP, but interest is waning as material suppliers reformulate chemistries to match the shear profiles of piezoelectric ejectors. Cost sensitivity keeps capillary-flow dispensers relevant in consumer electronics, where 3-5% void levels remain acceptable. Even so, AI-driven path planning lifts utilization for jetting platforms to nearly 80%, narrowing the total cost of ownership gap. As a result, the underfill dispenser market is seeing procurement budgets tilt decisively toward jet systems at both multinational and regional OSATs.

Piezoelectric jetting captured 34.54% of the revenue share in 2025, and its share of the underfill dispenser market is on track to widen, with a 6.94% CAGR projection. Printheads packing more than 1,500 nozzles now fire at 20 kHz, pushing hourly dot counts beyond 90,000 while holding +-2 micrometer positional tolerance. Pneumatic needle tools keep a share in Southeast Asian lines running 0.5 mm-pitch BGAs, but every major advanced-package roadmap specifies piezoelectric capability for die gaps below 20 micrometers.

Positive-displacement pumps and auger screws fill a niche for wafer-level packaging that requires sustained flow above 10 mL/min, volumes outside the comfort zone of piezo stacks. Film transfer has gained a foothold among ultra-thin MEMS modules under 200 μm tall, yet the lack of broad chemical support limits growth today. Overall, expanded machine vision integration and real-time dispense verification consolidate piezoelectric technology's leadership across mainstream heterogeneous integration programs in the underfill dispenser market.

Geography Analysis

Asia-Pacific generated 53.73% of 2025 revenue, anchored by Taiwan's cluster of advanced packaging plants that together consume more than 500 high-precision dispensers. South Korea added momentum in 2026 as a USD 12.9 billion HBM complex broke ground, underwriting orders for at least 40 top-tier jetting tools. Mainland China's 2.5D initiatives, driven by domestic GPU startups, lifted local demand by double digits even as export controls constrained EUV wafer capacity. Japan remains steady but leans on domestic suppliers that deliver incremental upgrades favored by automotive customers with conservative qualification schedules.

The Middle East is poised for a 6.57% CAGR and is the fastest regional climber. Sovereign wealth funds back multiple fabs in the United Arab Emirates and Saudi Arabia, including a USD 16 billion logic line bundled with chiplet assembly capability. Regional policy targets 50 homegrown semiconductor firms by 2028, and procurement documents already specify narrow-gap underfill dispensers matching those used in Taiwan.

North America and Europe progress at mid-single-digit rates as CHIPS Act incentives subsidize domestic packaging but struggle with engineering talent shortages. Pilot lines in Arizona and Saxony have installed precision jetters yet report extended operator-training times because only a few hundred engineers worldwide specialize in wafer-level underfill. South America and Africa remain nascent, although Brazilian automotive suppliers have begun qualifying void-free encapsulants for flex-fuel controllers, hinting at future uptick in regional orders for the underfill dispenser market.

- Nordson Corporation

- Musashi Engineering, Inc.

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc. (Camalot Systems)

- Fisnar Inc.

- GPD Global

- Essemtec AG

- Mycronic AB

- MKS Instruments, Inc.

- Scheugenpflug GmbH

- Techcon Systems, Inc.

- SMART VISION Co., Ltd.

- bdtronic GmbH

- Shenzhen Second Intelligent Equipment Co., Ltd.

- Dispensing Technology Corporation

- PVA (Precision Valve & Automation, Inc.)

- ViscoTec Pumpen- u. Dosiertechnik GmbH

- Universal Instruments Corporation

- Fuji Corporation

- Panasonic Holdings Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-optimised Dispense Path Planning Reduces Cycle Time

- 4.2.2 Adoption of High-Density Heterogeneous Integration Packages

- 4.2.3 Transition to 3D Chip-Stacking Demands Void-Free Underfill

- 4.2.4 Increasing Demand for Automotive-Grade Power Semiconductors

- 4.2.5 Growth of Silicon Photonics and Co-Packaged Optics Assemblies

- 4.2.6 Emergence of Chiplet-Based Substrates with Narrow Gap Spacing

- 4.3 Market Restraints

- 4.3.1 High Capex of Advanced Jetting Platforms

- 4.3.2 Limited Dispensing Throughput for Panel-Level Packaging Lines

- 4.3.3 Shrinking Die Gaps Intensify Flux/Contamination Risk

- 4.3.4 Talent Shortage in Process Engineering for Wafer-Level Underfill

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Capillary Flow Underfill Dispensers

- 5.1.2 Jet Dispensing Systems

- 5.1.3 Combination / Hybrid Systems

- 5.1.4 Needle Dispensing Systems

- 5.2 By Technology

- 5.2.1 Piezoelectric Jetting

- 5.2.2 Pneumatic Needle

- 5.2.3 Auger Screw

- 5.2.4 Positive Displacement Pump

- 5.2.5 Film Transfer Systems

- 5.3 By Application

- 5.3.1 Flip Chip Packaging

- 5.3.2 Ball Grid Array (BGA) Packaging

- 5.3.3 Wafer Level Packaging (WLP)

- 5.3.4 MEMS and Sensor Packaging

- 5.3.5 Photonics and Optoelectronic Packaging

- 5.3.6 Power Semiconductor Packaging

- 5.4 By End-User

- 5.4.1 Outsourced Semiconductor Assembly and Test (OSAT) Companies

- 5.4.2 Integrated Device Manufacturers (IDMs)

- 5.4.3 Foundries

- 5.4.4 Electronics Manufacturing Services (EMS) Providers

- 5.4.5 Photonics Device Manufacturers

- 5.4.6 Research and Development Institutions / Labs

- 5.5 By Dispensing Volume Range

- 5.5.1 Less than 5 Nanolitres

- 5.5.2 5-30 Nanolitres

- 5.5.3 More than 30 Nanolitres

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Saudi Arabia

- 5.6.4.2 United Arab Emirates

- 5.6.4.3 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nordson Corporation

- 6.4.2 Musashi Engineering, Inc.

- 6.4.3 Henkel AG & Co. KGaA

- 6.4.4 Illinois Tool Works Inc. (Camalot Systems)

- 6.4.5 Fisnar Inc.

- 6.4.6 GPD Global

- 6.4.7 Essemtec AG

- 6.4.8 Mycronic AB

- 6.4.9 MKS Instruments, Inc.

- 6.4.10 Scheugenpflug GmbH

- 6.4.11 Techcon Systems, Inc.

- 6.4.12 SMART VISION Co., Ltd.

- 6.4.13 bdtronic GmbH

- 6.4.14 Shenzhen Second Intelligent Equipment Co., Ltd.

- 6.4.15 Dispensing Technology Corporation

- 6.4.16 PVA (Precision Valve & Automation, Inc.)

- 6.4.17 ViscoTec Pumpen- u. Dosiertechnik GmbH

- 6.4.18 Universal Instruments Corporation

- 6.4.19 Fuji Corporation

- 6.4.20 Panasonic Holdings Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment