|

시장보고서

상품코드

2063366

위협 모델링 도구 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Threat Modeling Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

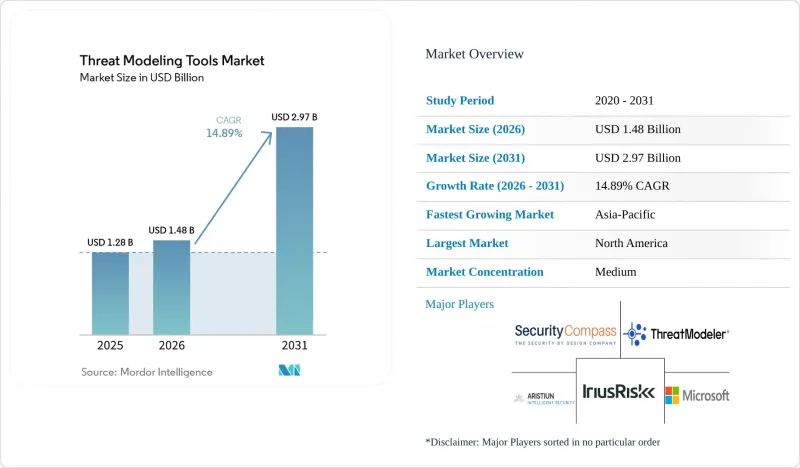

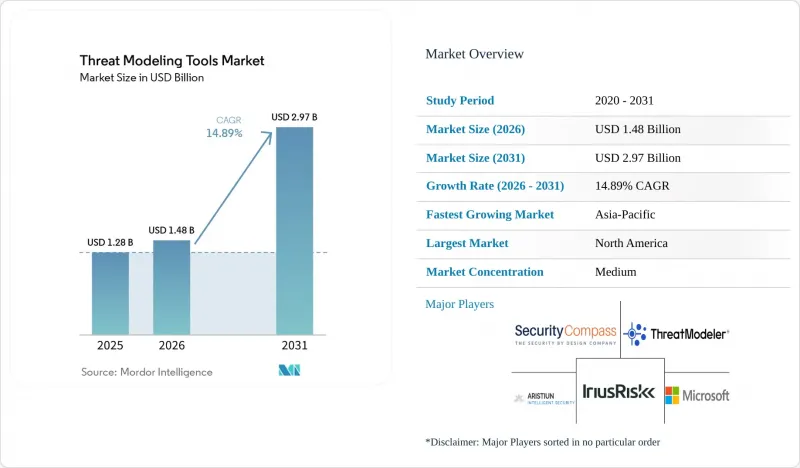

Mordor Intelligence에 의하면, 위협 모델링 도구 시장 규모는 2025년에 12억 8,000만 달러로 평가되었습니다. 2026년 14억 8,000만 달러에서 2031년까지 29억 7,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 14.89%를 나타낼 전망입니다.

본 보고서는 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 도구 유형(엔터프라이즈 상용 플랫폼, 오픈소스/커뮤니티 버전, 기타), 조직 규모(대기업, 중소기업(SME)), 최종 사용자 업종(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 제조업, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 위협 모델링 도구 시장 동향 및 인사이트

보안 소프트웨어 개발에 대한 규제 요건의 강화

각국 정부는 자발적인 모범 사례를 구속력 있는 조달 기준으로 전환하고 있습니다. 유럽연합(EU)의 ‘사이버 복원력 법’은 디지털 제품 제조업체에 제품 수명 주기 전반에 걸친 위협 모델을 문서화할 것을 의무화하고 있으며, 2027년 9월에 전면 시행될 예정입니다. 미국에서는 대통령령 제14144호에 따라 연방 정부의 소프트웨어 공급업체는 NIST 보안 소프트웨어 개발 프레임워크(SSDF)에 따른 자체 인증을 의무적으로 수행해야 하며, 위협 모델링이 기본 요건으로 격상되었습니다. 브라질의 ‘사이버 보안 법 체계’ 초안에 따르면, 기준을 충족하지 못하는 공급업체를 공공 계약에서 배제할 권한을 가진 국가 기관이 설립될 전망입니다. 사우디아라비아의 ‘비중요 국가 인프라 사이버 보안 관리 조치’에 따르면, 직원이 불과 6명 정도인 기업에 대해서도 위협 평가 의무가 확대되었습니다. 이러한 법규는 위협 모델링 도구 시장의 규정 준수를 중시하는 잠재 고객 기반을 전반적으로 확대하는 역할을 합니다.

소프트웨어 공급망을 표적으로 한 사이버 공격의 급증

주목을 받은 이 사건은 경계 통제만으로는 전이적 의존성 위험을 차단할 수 없음을 입증하고 있습니다. 2026년 3월, 공격자는 axios의 npm 패키지에 백도어를 심어 1만 8,000개 이상의 하위 저장소에서 인증 정보를 수집했습니다. TeamPCP 캠페인에서는 트로이 목마가 심어진 Python 아티팩트가 악용되어, 다양한 산업 분야의 빌드 시스템이 침해되었습니다. 2024년 2월 Change Healthcare에서 발생한 해킹 사건은 제3자의 인증 정보가 유출된 것이 계기가 되어, 1억 명 이상의 환자 처방전 처리에 차질을 빚었습니다. 이러한 현상으로 인해 기업들은 의존 관계를 매핑하고, 공격 트리를 생성하며, 완화 조치를 지속적으로 검증할 수 있는 플랫폼의 도입을 요구받고 있으며, 그 결과 위협 모델링 도구 시장의 성장이 촉진되고 있습니다.

숙련된 위협 모델링 전문가의 부족

세계 사이버 보안 인력 부족 규모는 350만 명을 넘어섰으며, 시스템 설계를 공격 트리로 변환할 수 있는 실무자는 더욱 드뭅니다. 만안 지역 고용주들의 87%가 자격을 갖춘 인재 채용에 어려움을 겪고 있다고 보고한 가운데, 이에 따라 사우디아라비아는 2030년까지 2만 명의 전문가를 양성하는 것을 목표로 하는 프로그램을 시작했습니다. 플랫폼 자동화만으로는 전문가의 판단을 완전히 대체할 수 없기 때문에 인력 부족이 도입 속도를 늦추고 있으며, 특히 복잡한 운영 기술(OT) 환경에서는 위협 모델링 도구 시장의 확산을 제한하고 있습니다.

부문별 분석

규제 대상 기업들이 On-Premise 데이터 관리와 클라우드의 확장성을 결합해 나감에 따라, 하이브리드 환경의 도입은 2031년까지 연평균 성장률(CAGR) 15.44%로 확대될 것으로 전망됩니다. 2025년에는 클라우드 서비스가 위협 모델링 도구 시장의 53.52%를 차지했으나, 사우디아라비아와 아랍에미리트의 국가 주권 관련 규제로 인해 워크로드는 여전히 원격 분석에 의존하는 주권 클라우드 구성으로 전환되고 있습니다. 그 결과, 위협 모델링 도구 시장 규모는 데이터를 중복하지 않고 환경 간에 모델을 동기화하는 벤더 쪽으로 점차 이동하고 있습니다.

하이브리드 수요는 멀티클라우드 도입으로 인해 더욱 증가하고 있습니다. 자산은 AWS, Azure, Google Cloud에 분산되어 있지만, 단일 위험 평가 기준을 통해 평가해야 합니다. 시스코의 Splunk를 핵심으로 하는 포트폴리오는 Amazon S3와 로컬 로그 저장소를 아우르는 통합 분석을 실현하고 있으며, 기업이 기밀성이 높은 텔레메트리 데이터의 일원화된 관리를 거부하는 경우 공급업체가 어떻게 수익을 확보할 수 있는지를 보여주고 있습니다. 이처럼 하이브리드 기능은 대규모 입찰에서 사실상 필수 요건으로 자리 잡고 있으며, 위협 모델링 도구 시장의 성장세를 유지하고 있습니다.

엔터프라이즈용 상용 제품군은 정책 엔진, 시각적 대시보드, 감사 추적 기록 등의 기능을 통해 2025년에도 매출 점유율 43.41%를 유지했으나, Git 워크플로에 직접 통합되는 ‘Threat-as-Code’ 제품에 의해 점유율이 급속히 잠식당하고 있습니다. 'Threat-as-Code' 위협 모델링 도구 시장 규모가 확대되고 있는 이유는 보안 팀이 풀 리퀘스트와 함께 진화하는 YAML 및 JSON 정의를 선호하기 때문이며, 이를 통해 거버넌스가 Infrastructure-as-Code의 릴리스 주기와 일치하게 되었습니다.

Threagile이나 OWASP Threat Dragon과 같은 오픈소스 이니셔티브는 특히 중소기업에서 도입 장벽을 낮추고 있는 반면, 유료 제품은 확률적 공격 그래프와 정량적 위험 점수 산정을 통해 차별화를 꾀하고 있습니다. securiCAD와 같은 시뮬레이션 도구는 IT와 OT(운영 기술)가 융합된 네트워크 전체에서 발생하는 연쇄적인 장애를 모델화하여, 일반적인 도표 작성 제품으로는 해결할 수 없는 과제를 해결합니다. 이러한 다양성 덕분에 위협 모델링 도구 시장은 적정 수준의 하위 세분화를 이루고 있음에도 불구하고 높은 혁신성을 유지하고 있습니다.

지역별 분석

북미는 2025년에 매출의 39.11%를 차지하며 1위를 차지했습니다. 이는 위협 모델링을 전제조건으로 제시하는 연방 정부의 의무적 자기 신고서에 근거한 것입니다. 주요 벤더의 대부분은 미국에 본사를 두고 있으며, 파트너 및 컨설턴트에 의한 긴밀한 지역 생태계가 형성되어 플랫폼의 확산을 가속화하고 있습니다. 캐나다의 ‘중요 사이버 시스템 보호법’은 통신 및 에너지 사업자에게도 유사한 의무를 확대 적용함으로써 지역적 수요를 늘리고 있습니다.

유럽에서는 ‘사이버 복원력법’이 시행된 이후, 이 법이 널리 보급되고 있습니다. 독일, 프랑스, 이탈리아의 자동차, 산업, 가전 제조업체들은 현재 유럽 시장에 제품을 출시할 때 위협 모델링을 필수 요건으로 간주하고 있습니다. 2027년까지의 적합성 평가 기한이 다가옴에 따라, 다년간의 플랫폼 계약이 체결되어 위협 모델링 도구 시장에 막대한 수익을 가져다주고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 16.13%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 중국은 사이버 보안법을 개정하여, 중요 인프라에 서비스를 제공하는 업체에 대해 보안 개발 검토를 의무화했습니다. 인도의 ‘디지털 개인 데이터 보호법’은 데이터 수탁자에 대한 위험 평가를 의무화하고 있으며, 일본이 개정한 ‘사이버 보안 전략’은 공급망 보증을 중시하고 있습니다. 이러한 지침은 종합적으로 볼 때, 현지 규정 준수 요건을 잘 파악하고 있는 서비스 제공업체에게 거대한 잠재 시장을 개척할 기회를 제공합니다.

중동 및 아프리카는 하이브리드 클라우드의 대표 사례로 부상하고 있습니다. 사우디아라비아가 DSShield에 2억 300만 사우디 리얄(5,410만 달러)을 투자하고 관리형 보안 운영 센터(MSOC)에 대한 신규 라이선스를 취득한 것은 현지 전문 지식에 대한 국가적 의지를 보여주는 반면, 아랍에미리트(UAE)는 현재 예산에서 사이버 보안에 20억 달러 이상을 배정하고 있습니다. 남미도 이에 뒤따르고 있습니다. 브라질의 결의안 제538/2025호와 심의 중인 사이버 보안 법안은 금융 및 공공 부문 시스템에서의 위협 모델링을 제도화함으로써, 위협 모델링 도구 시장을 새로운 영역으로 확장하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the threat modeling tools market size was valued at USD 1.28 billion in 2025 and is estimated to grow from USD 1.48 billion in 2026 to reach USD 2.97 billion by 2031, at a CAGR of 14.89% during the forecast period (2026-2031).

This report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Tool Type (Enterprise Commercial Platforms, Open-Source/Community Editions, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises (SMEs)), End-User Vertical (BFSI, IT and Telecom, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Threat Modeling Tools Market Trends and Insights

Growing Regulatory Mandates For Secure Software Development

Governments are converting voluntary best practices into binding procurement criteria. The European Union's Cyber Resilience Act compels digital-product makers to document threat models across the product lifecycle, with full enforcement slated for September 2027. In the United States, Executive Order 14144 obliges federal software suppliers to self-attest against the NIST Secure Software Development Framework, elevating threat modeling to a baseline requirement. Brazil's draft Cybersecurity Legal Framework would create a national authority empowered to bar non-conforming vendors from public contracts. Saudi Arabia's Non-Critical National Infrastructure Cybersecurity Controls extend mandatory threat assessments to firms with as few as six employees. These statutes collectively expand the compliance-driven addressable base for the threat modeling tools market.

Surge In Cyberattacks Targeting Software Supply Chains

High-profile incidents prove that perimeter controls cannot contain transitive dependency risks. In March 2026, attackers back-doored the axios npm package, harvesting credentials from more than 18,000 downstream repositories. The TeamPCP campaign exploited trojanized Python artifacts to compromise build systems across multiple industries. The February 2024 Change Healthcare breach, triggered by compromised third-party credentials, disrupted prescription processing for over 100 million patients. These events are driving companies to adopt platforms that map dependencies, generate attack trees, and validate mitigations continuously, thereby fueling growth of the threat modeling tools market.

Lack Of Skilled Threat Modeling Professionals

The worldwide cybersecurity talent gap exceeds 3.5 million roles, and practitioners who can translate system designs into attack trees are rarer still. Gulf-region employers report that 87% struggle to hire qualified staff, prompting Saudi Arabia to launch programs that aim to train 20,000 specialists by 2030. Because platform automation cannot fully replace expert judgment, staffing shortages dampen adoption velocity, especially for complex operational-technology environments, limiting penetration of the threat modeling tools market.

Other drivers and restraints analyzed in the detailed report include:

- Shift-Left Security Adoption In DevSecOps Pipelines

- Increasing Integration With AI-Driven Code Generation Platformsdels

- High Initial Setup And Integration Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid installations are projected to grow at a 15.44% CAGR to 2031 as regulated entities combine on-premise data custodianship with cloud scalability. Although cloud delivery held 53.52% of the threat modeling tools market share in 2025, national sovereignty rules in Saudi Arabia and the United Arab Emirates are steering workloads toward sovereign-cloud configurations that still rely on remote analytics. The threat modeling tools market size is consequently shifting toward vendors that synchronize models across environments without duplicating data.

Hybrid demand is reinforced by multi-cloud adoption, where assets reside in AWS, Azure, and Google Cloud yet must be evaluated through a single risk lens. Cisco's Splunk-anchored portfolio enables federated analytics across Amazon S3 and local log stores, illustrating how vendors capture spend when enterprises refuse to centralize sensitive telemetry. As such, hybrid capabilities are becoming a de-facto checklist item in large tenders, sustaining momentum for the threat modeling tools market.

Enterprise commercial suites retained 43.41% revenue share in 2025, due to policy engines, visual dashboards, and audit trails, yet they face rapid erosion from threat-as-code products that slot directly into Git workflows. The threat modeling tools market size for threat-as-code is expanding because security teams prefer YAML or JSON definitions that evolve with pull requests, aligning governance with the pace of infrastructure-as-code releases.

Open-source initiatives such as Threagile and OWASP Threat Dragon reduce experimental friction, especially for SMEs, whereas paid offerings differentiate through probabilistic attack graphs and quantitative risk scoring. Simulation tools like securiCAD model cascading failures across converged information-technology and operational-technology networks, addressing gaps that generic diagramming products cannot. This variety keeps the threat modeling tools market moderately fragmented yet highly innovative.

Geography Analysis

North America topped revenue at 39.11% in 2025, underpinned by mandatory federal self-attestation forms that list threat modeling as a prerequisite. Most leading vendors are headquartered in the United States, creating a dense local ecosystem of partners and consultants that accelerates platform rollouts. Canada's Critical Cyber Systems Protection Act extends similar obligations to telecommunications and energy operators, enlarging regional demand.

Europe follows with widespread uptake after the Cyber Resilience Act entered into force. Automotive, industrial, and consumer-electronics manufacturers in Germany, France, and Italy now consider threat modeling non-negotiable when placing products on the European market. Conformity-assessment deadlines for 2027 are prompting multi-year platform deals, contributing substantial revenue to the threat modeling tools market.

Asia-Pacific is the fastest-growing territory at a 16.13% CAGR. China amended its Cybersecurity Law to impose secure-development reviews on vendors serving critical infrastructure, India's Digital Personal Data Protection Act requires risk assessments for data fiduciaries, and Japan's revamped Cybersecurity Strategy stresses supply-chain assurance. Collectively, these directives open large addressable pools for providers fluent in local compliance dialects.

The Middle East and Africa region is emerging as a hybrid-cloud showcase. Saudi Arabia's SAR 203 million (USD 54.10 million) investment in DSShield and new licensing for managed security operations centers demonstrate national commitment to local expertise, while the United Arab Emirates earmarked over USD 2 billion for cybersecurity in its current budget. South America is following suit: Brazil's Resolution 538/2025 and pending cybersecurity bill institutionalize threat modeling for financial and public-sector systems, nudging the threat modeling tools market into fresh territory.

- ThreatModeler Software Inc.

- IriusRisk Limited

- Security Compass Inc.

- Foreseeti AB

- Aristiun Inc.

- CAIRIS Services Ltd.

- OWASP Foundation

- Microsoft Corporation

- Threagile UG

- ThreatSpec Ltd.

- Lucid Software Inc.

- Miro International GmbH

- Splunk Inc.

- Cisco Systems, Inc.

- SecureFlag Ltd.

- Tutamen GmbH

- Amazon Web Services, Inc.

- Kenna Security LLC

- International Business Machines Corporation

- Devici LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Regulatory Mandates for Secure Software Development

- 4.2.2 Surge in Cyberattacks Targeting Software Supply Chains

- 4.2.3 Shift-Left Security Adoption in DevSecOps Pipelines

- 4.2.4 Increasing Integration with AI-Driven Code Generation Platforms

- 4.2.5 Rise of Infrastructure-as-Code Threat Modeling Demand

- 4.2.6 Adoption of Threat Modeling Standards in Safety-Critical IoT Systems

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled Threat Modeling Professionals

- 4.3.2 High Initial Setup and Integration Costs

- 4.3.3 Limited Support for Emerging Edge Computing Architectures

- 4.3.4 Fragmented Open-Source Alternatives Diluting Commercial Adoption

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Tool Type

- 5.2.1 Enterprise Commercial Platforms

- 5.2.2 Open-Source / Community Editions

- 5.2.3 Threat-as-Code / CLI Tools

- 5.2.4 Diagramming-Centric Tools

- 5.2.5 Simulation and Attack-Graph Tools

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises (SMEs)

- 5.4 By End-User Vertical

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Government and Defense

- 5.4.5 Retail and E-Commerce

- 5.4.6 Energy and Utilities

- 5.4.7 Manufacturing

- 5.4.8 Other End-User Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of the Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ThreatModeler Software Inc.

- 6.4.2 IriusRisk Limited

- 6.4.3 Security Compass Inc.

- 6.4.4 Foreseeti AB

- 6.4.5 Aristiun Inc.

- 6.4.6 CAIRIS Services Ltd.

- 6.4.7 OWASP Foundation

- 6.4.8 Microsoft Corporation

- 6.4.9 Threagile UG

- 6.4.10 ThreatSpec Ltd.

- 6.4.11 Lucid Software Inc.

- 6.4.12 Miro International GmbH

- 6.4.13 Splunk Inc.

- 6.4.14 Cisco Systems, Inc.

- 6.4.15 SecureFlag Ltd.

- 6.4.16 Tutamen GmbH

- 6.4.17 Amazon Web Services, Inc.

- 6.4.18 Kenna Security LLC

- 6.4.19 International Business Machines Corporation

- 6.4.20 Devici LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment