|

시장보고서

상품코드

2063373

자동차용 하이퍼바이저 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Hypervisor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

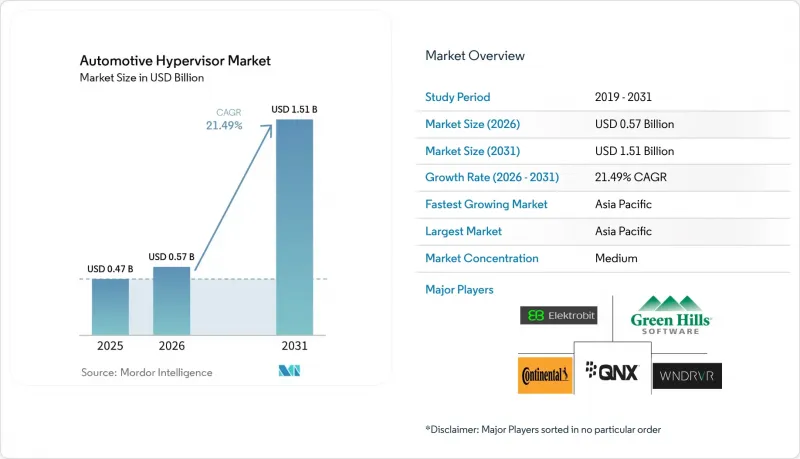

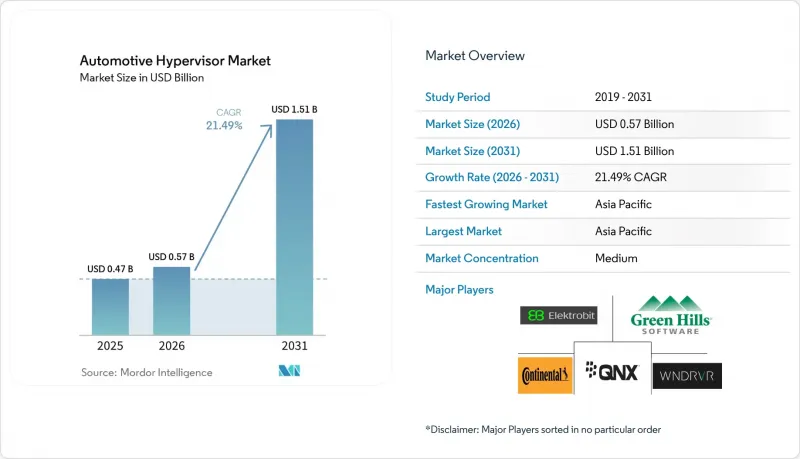

Mordor Intelligence에 의하면, 자동차용 하이퍼바이저 시장 규모는 2025년 4억 7,000만 달러로 평가되었습니다. 2026년에는 5억 7,000만 달러로 확대되어 2031년까지 15억 1,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR 21.49%로 성장할 전망입니다.

본 보고서는 유형별(유형 1 베어메탈 하이퍼바이저, 유형 2 호스트형 하이퍼바이저), 차종별(승용차, 소형 상용차, 기타), 운용 모드별(자율주행차, 기타), 용도별(ADAS(첨단 운전자 지원 시스템), 기타), 수요 유형별(OEM, 교체용), 지역별(북미, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 자동차용 하이퍼바이저 시장 동향 및 인사이트

도메인 컨트롤러형 E/E 아키텍처의 보급

자동차 산업에서 분산형 ECU 아키텍처에서 집중형 도메인 컨트롤러로의 전환은 차량의 전기 및 전자(E/E) 시스템을 근본적으로 재구축하는 것이며, 100개 이상의 개별 ECU를 10개 이하의 고성능 컴퓨팅 유닛으로 통합하기 위한 핵심 요소로서 하이퍼바이저가 기능합니다. 이러한 아키텍처 전환을 통해 차량 중량이 약 15-20kg 감소하고, 와이어 하네스의 복잡성이 최대 40% 줄어들어 전기차의 주행 거리와 제조 비용에 직접적인 영향을 미치고 있습니다. 또한, 이러한 통합은 자동차용 하이퍼바이저 시장에도 큰 기회를 가져다주고 있습니다. 각 도메인 컨트롤러에는 ASIL-D 안전 기능과 비안전 용도를 아우르는 중요도가 서로 다른 워크로드를 관리하기 위한 고도의 가상화 소프트웨어가 필요하기 때문입니다. 각 OEM 업체들은 진화하는 소프트웨어 요구 사항에 대응하고 미래를 내다보는 차량 플랫폼을 구축하기 위해 하이퍼바이저 기반 아키텍처를 점점 더 많이 채택하고 있으며, 테슬라, BMW, 폭스바겐이 소프트웨어 정의 차량으로의 전환을 주도하고 있습니다.

사이버 보안 규정 준수 의무화(ISO/SAE 21434, UNECE R155/R156)

자동차 사이버 보안에 관한 규제 요건이 자동차용 하이퍼바이저 시장의 규정 준수 주도 성장을 이끌고 있습니다. UNECE R155에 따르면, 2024년 7월 이후 EU 회원국, 일본, 한국에서 차량 형식 승인을 받기 위한 전제조건으로 사이버 보안 관리 시스템(CSMS) 인증이 의무화됩니다. 이 규제가 조직 차원의 사이버 보안 프로세스와 정기적인 위협 분석 및 위험 평가(TARA) 활동을 중시하고 있기 때문에 각 OEM 업체들은 안전이 중요한 영역과 연결성 영역 사이에 하드웨어를 통한 분리를 제공하는 하이퍼바이저 기반 아키텍처를 채택해야 하는 상황에 놓여 있습니다. ISO/SAE 21434의 적합성 요건은 혼합 중요도 시스템에서 특히 엄격하며, 하이퍼바이저는 공유 하드웨어 리소스에서 실행되는 서로 다른 ASIL 등급의 용도 간에 간섭이 발생하지 않음을 입증해야 합니다.

Tier 1 공급업체의 레거시 ECU에 대한 투자 고착화

자동차 산업이 레거시 ECU 아키텍처에 막대한 투자를 하고 있는 것은 자동차용 하이퍼바이저 시장의 성장에 있어 여전히 큰 과제로 남아 있습니다. 이는 Tier 1 공급업체들이 분산 제어 시스템에 최적화된 기존 툴체인, 제조 설비, 엔지니어링 전문 지식과 관련해 수십억 달러 규모의 평가 손실을 기록할 가능성이 있기 때문입니다. 많은 유서 깊은 공급업체들은 독자적인 AUTOSAR Classic 구현 및 안전 인증을 받은 소프트웨어 스택을 개발하고 있으며, 이를 하이퍼바이저 환경 내에서 구동하려면 대규모 재설계가 필요하기 때문에 신속한 전환에 있어 경제적 장벽이 되고 있습니다. 이 과제는 자동차 개발 주기가 길다는 점 때문에 더욱 복잡해지고 있습니다. 2022-2023년에 설계가 확정된 ECU는 2028-2030년에 걸쳐서도 양산 차량에 계속 탑재될 것이므로, 예측 기간 동안 하이퍼바이저 솔루션의 잠재 시장 규모는 제한적일 것입니다.

부문별 분석

2025년에는 Type 1 베어메탈 하이퍼바이저가 62.04%의 시장 점유율을 차지했습니다. 이는 안전성이 극히 중요한 자동차 용도에 필수적인, 뛰어난 성능과 하드웨어에 대한 직접 접근 기능을 반영한 것입니다. 이러한 하이퍼바이저는 기반 운영 체제를 거치지 않고 차량 하드웨어에서 직접 작동하며, ADAS 및 파워트레인 제어 시스템에 필수적인 결정론적 실시간 성능과 최소한의 지연 오버헤드를 제공합니다. 유형 2 호스트형 하이퍼바이저는 시장 점유율은 작지만, 개발 환경에서의 유연성과 기존 리눅스 기반 인포테인먼트 플랫폼과의 통합 용이성을 바탕으로 2031년까지 연평균 성장률(CAGR) 16.82%라는 급속한 성장을 이루고 있습니다.

베어 메탈 아키텍처의 성능상 이점은 ASIL-D 수준의 안전 기능이 공유 하드웨어 리소스 상에서 비안전 용도과 공존해야 하는 중요도가 혼재된 시나리오에서 특히 두드러집니다. Green Hills의 INTEGRITY Multivisor나 Wind River의 Helix Virtualization Platform과 같은 유형 1 하이퍼바이저는 기능 안전 규정 준수에 필요한 엄격한 시간적 및 공간적 분할을 가능하게 하는 하드웨어 지원형 가상화 기능을 갖추고 있습니다. 그러나 소프트웨어 개발, 테스트, 비안전 인포테인먼트 용도과 같은 특정 이용 사례에서는 이러한 단순화된 배포 모델이 성능상의 우려를 상쇄하기 때문에 유형 2 솔루션이 점차 지지를 얻고 있습니다. 시장 동향은 유형 1 하이퍼바이저가 양산차 도입을 주도하는 한편, 유형 2 솔루션이 개발 도구 및 애프터마켓 부문을 장악할 것이라는 양극화된 미래를 시사하고 있습니다.

2025년 자동차용 하이퍼바이저 도입에서 승용차가 58.28%를 차지했습니다. 이는 해당 부문에서의 대량 생산과 도메인 통합의 혜택을 받는 첨단 인포테인먼트 기능 및 ADAS 기능의 통합이 진행되고 있기 때문입니다. 승용차 부문의 우위는 견고한 가상화 플랫폼이 필요한 소프트웨어 정의 기능과 무선 업데이트를 통해 소비자용 차량의 차별화를 꾀하는 각 OEM 업체들의 노력을 반영하고 있습니다. 소형 상용차(LCV)와 중대형 상용차(HCV)가 나머지 시장 점유율을 합쳐 차지하고 있으며, 상용차 부문에서는 하이퍼바이저를 활용한 차량 관리 및 텔레매틱스 용도에 대한 관심이 높아지고 있습니다.

LCV(소형 상용차) 부문은 차량 함대의 운영이 급속히 디지털화되고, 커넥티드 및 소프트웨어 주도형 아키텍처가 도입됨에 따라 자동차용 하이퍼바이저 시장에서 가장 빠르게 성장하고 있는 분야입니다. 물류 및 라스트 마일 배송 차량에서 실시간 텔레매틱스, 운전 지원, 무선 업데이트에 대한 수요가 증가함에 따라 LCV 플랫폼 전반에 걸친 하이퍼바이저 통합이 가속화되고 있습니다. 자동차 제조업체들은 하드웨어 비용 절감과 시스템 효율 향상을 위해 인포테인먼트, ADAS, 파워트레인 등 여러 제어 영역을 가상화된 ECU에 통합하고 있습니다. 또한, 사이버 보안 규정을 준수하고 전기 LCV로 전환하기 위해서는 안전하고 확장 가능한 가상화 프레임워크가 필요합니다. 그 결과, 예측 기간 동안 LCV 부문은 자동차용 하이퍼바이저에 있어 가장 큰 도입 잠재력을 지니고 있습니다.

지역별 분석

아시아태평양은 2025년에 37.81%의 점유율로 1위를 차지했으며, 중국의 OEM 기업들이 실리콘 현지화와 소프트웨어 정의 아키텍처 도입을 서두르는 가운데 연평균 성장률(CAGR) 14.79%로 성장하고 있습니다. 2025년형 모델로 중국에서 생산되는 차량의 약 3분의 1에는 도메인 컨트롤러가 탑재되며, 각 차량에는 최소 1개의 하이퍼바이저 인스턴스가 내장됩니다. 국내 칩 제조업체들은 현재 초기 단계의 RISC-V 자동차용 SoC를 출하하고 있으며, 중국의 보안 알고리즘에 맞추어 조정된 현지화된 가상화 스택의 개발이 촉진되고 있습니다.

북미에서도 이에 이어 38개 주에 걸친 광범위한 자율주행 테스트와, 안전한 로깅을 의무화하는 NHTSA(미국 도로교통안전국)의 새로운 데이터 공유 요건(이는 하이퍼바이저의 고유한 이용 사례입니다)에 힘입고 있습니다. 중국의 텔레매틱스 부품 사용을 제한하는 미국공급망 리스크 완화 조치로 인해, 각 OEM 업체들은 자국 및 동맹국의 소프트웨어 공급업체로 눈을 돌리고 있습니다.

유럽은 여전히 엄격한 기능 안전 기준을 적용하는 시장으로 남아 있습니다. UNECE R156의 갱신 절차에서는 3년마다 재인증 주기가 요구되며, 이는 규정 준수 모니터링 서비스를 제공하는 하이퍼바이저 공급업체에 지속적인 수익을 가져다주고 있습니다. 독일의 2024년 레벨 4 조례와 프랑스의 2025년 블랙박스 규제는 충돌 시에도 데이터가 분리된 상태를 보장하는 솔루션에 새로운 기회를 제공합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the automotive hypervisor market size is expected to increase from USD 0.47 billion in 2025 to USD 0.57 billion in 2026 and reach USD 1.51 billion by 2031, growing at a CAGR of 21.49% over 2026-2031.

This report is Segmented by Type (Type 1 Bare-Metal Hypervisor, Type 2 Hosted Hypervisor), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Mode of Operation (Autonomous Vehicles, and More), Application (Advanced Driver Assistance Systems, and More), Demand Type (OEM, Replacement), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Hypervisor Market Trends and Insights

Proliferation of Domain-Controller E/E Architectures

The automotive industry's transition from distributed ECU architectures to centralized domain controllers fundamentally reshapes vehicle electrical/electronic (E/E) systems, with hypervisors as the critical enabler for consolidating 100+ individual ECUs onto fewer than 10 high-performance computing units. This architectural shift reduces vehicle weight by approximately 15-20 kilograms while cutting wiring harness complexity by up to 40%, directly impacting electric vehicle range and manufacturing costs. The consolidation is also creating significant opportunities in the automotive hypervisor market, as each domain controller requires advanced virtualization software to manage mixed-criticality workloads across ASIL-D safety functions and non-safety applications. OEMs are increasingly adopting hypervisor-based architectures to future-proof vehicle platforms against evolving software demands, with Tesla, BMW, and Volkswagen leading the move toward software-defined vehicles.

Mandatory Cybersecurity Compliance (ISO/SAE 21434, UNECE R155/R156)

Regulatory mandates for automotive cybersecurity are driving compliance-led growth in the automotive hypervisor market. UNECE R155 requires Cybersecurity Management Systems (CSMS) certification as a precondition for vehicle type approval in EU member countries, Japan, and South Korea since July 2024. The regulation's emphasis on organizational-level cybersecurity processes and regular threat analysis and risk assessment (TARA) activities drives OEMs to adopt hypervisor-based architectures that provide hardware-backed isolation between safety-critical and connectivity domains. ISO/SAE 21434 compliance requirements are particularly stringent for mixed-criticality systems, where hypervisors must demonstrate freedom from interference between different ASIL-rated applications running on shared hardware resources.

Legacy ECU Investment Lock-ins at Tier-1s

The automotive industry's heavy investment in legacy ECU architectures remains a major challenge for growth in the automotive hypervisor market, as Tier-1 suppliers face potential write-offs of billions of dollars in existing toolchains, manufacturing equipment, and engineering expertise optimized for distributed control systems. Many established suppliers have developed proprietary AUTOSAR Classic implementations and safety-certified software stacks requiring extensive re-engineering to operate within hypervisor environments, creating financial disincentives for rapid migration. The challenge is compounded by long automotive development cycles. ECU designs frozen in 2022-2023 will continue shipping in production vehicles through 2028-2030, limiting the addressable market for hypervisor solutions during the forecast period.

Other drivers and restraints analyzed in the detailed report include:

- Consolidation of Infotainment, ADAS and Powertrain on Single SoCs

- OEM Push Toward Software-Defined Vehicles (SDVs)

- Hypervisor Certification Costs for ASIL-D Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type 1 bare-metal hypervisors hold 62.04% market share in 2025, reflecting their superior performance and direct hardware access capabilities, which are essential for safety-critical automotive applications. These hypervisors operate directly on vehicle hardware without an underlying operating system, providing deterministic real-time performance and minimal latency overhead crucial for ADAS and powertrain control systems. Type 2 hosted hypervisors, despite a smaller market share, are experiencing rapid growth at a 16.82% CAGR through 2031, driven by their flexibility in development environments and ease of integration with existing Linux-based infotainment platforms.

The performance advantages of bare-metal architectures become particularly pronounced in mixed-criticality scenarios, where ASIL-D safety functions must coexist with non-safety applications on shared hardware resources. Type 1 hypervisors, such as Green Hills' INTEGRITY Multivisor and Wind River's Helix Virtualization Platform, provide hardware-assisted virtualization features that enable strict temporal and spatial partitioning required for functional safety compliance. However, Type 2 solutions are gaining traction in specific use cases such as software development, testing, and non-safety infotainment applications where their simplified deployment model outweighs performance considerations. The market evolution suggests a bifurcated future, with Type 1 hypervisors dominating production vehicle deployments while Type 2 solutions capture development tool and aftermarket segments.

Passenger cars account for 58.28% of automotive hypervisor deployments in 2025, driven by the segment's high-volume production and the increasing integration of advanced infotainment and ADAS features that benefit from domain consolidation. The passenger car segment's dominance reflects OEMs' focus on differentiating consumer vehicles through software-defined features and over-the-air updates, which require robust virtualization platforms. Light Commercial Vehicles (LCVs) and Medium/Heavy Commercial Vehicles (HCVs) collectively account for the remaining market share, with commercial segments showing growing interest in hypervisor-enabled fleet management and telematics applications.

The LCV (Light Commercial Vehicle) segment is the fastest-growing category in the automotive hypervisor market, owing to the rapid digitalization of fleet operations and the adoption of connected, software-driven architectures. Rising demand for real-time telematics, driver assistance, and over-the-air updates in logistics and last-mile delivery fleets is accelerating the integration of hypervisors across LCV platforms. Automakers are consolidating multiple control domains-infotainment, ADAS, and powertrain-into virtualized ECUs to reduce hardware costs and enhance system efficiency. Furthermore, compliance with cybersecurity regulations and the shift toward electrified LCVs require secure and scalable virtualization frameworks. As a result, the LCV segment offers the highest deployment potential for automotive hypervisors during the forecast period.

Geography Analysis

Asia-Pacific led with 37.81% share in 2025 and is advancing at a 14.79% CAGR as Chinese OEMs race to localize silicon and adopt software-defined architectures. Roughly one-third of vehicles built in China for the 2025 model year will feature domain controllers, each of which embeds at least one hypervisor instance. Domestic chipmakers are now shipping early RISC-V automotive SoCs, prompting the development of localized virtualization stacks tuned for Chinese security algorithms.

North America follows, buoyed by widespread autonomous testing across 38 states and emerging NHTSA data-sharing mandates that require secure logging-an inherent hypervisor use case. U.S. supply-chain de-risking policies curtailing the use of Chinese telematics components are pushing OEMs toward domestic and allied software vendors.

Europe remains the reference market for rigorous functional safety. UNECE R156 update processes call for three-year re-certification cycles, generating recurring revenue for hypervisor suppliers offering compliance monitoring. Germany's 2024 Level 4 ordinance and France's 2025 black-box rules create unique opportunities for solutions that guarantee crash-proof data isolation.

- BlackBerry QNX

- Green Hills Software

- Wind River

- Continental AG

- Elektrobit

- Vector Informatik

- Renesas Electronics

- Siemens Digital Industries (Embedded Mentor)

- NXP Semiconductors

- LYNX Software Technologies

- Real-Time Systems (RTX)

- Bosch ETAS

- Aptiv

- Harman (Samsung)

- Denso

- Qualcomm

- KPIT Technologies

- TTTech Auto

- SYSGO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Domain-Controller E/E Architectures

- 4.2.2 Mandatory Cybersecurity Compliance (ISO/SAE 21434, UNECE R155/R156)

- 4.2.3 Consolidation of Infotainment, ADAS, and Powertrain on Single SoCs

- 4.2.4 Rise of "Vehicle-as-a-Service" Subscription Models

- 4.2.5 Adoption of Zonal Architecture Enabling Mixed-Criticality Workloads

- 4.2.6 OEM Push Toward Software-Defined Vehicles (SDVs)

- 4.3 Market Restraints

- 4.3.1 Legacy ECU Investment Lock-Ins at Tier-1s

- 4.3.2 Hypervisor Certification Costs for ASIL-D Compliance

- 4.3.3 Real-Time Performance Overhead and Latency Jitter

- 4.3.4 Scarcity of Automotive-Grade Virtualization Skillsets

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Type

- 5.1.1 Type 1 (Bare-Metal Hypervisor)

- 5.1.2 Type 2 (Hosted Hypervisor)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (LCVs)

- 5.2.3 Medium and Heavy Commercial Vehicles (HCVs)

- 5.3 By Mode of Operation

- 5.3.1 Autonomous Vehicles

- 5.3.2 Semi-Autonomous Vehicles

- 5.4 By Application

- 5.4.1 Advanced Driver Assistance Systems (ADAS)

- 5.4.2 Infotainment Systems

- 5.4.3 Connectivity and Telematics

- 5.4.4 Powertrain and Engine Control Systems

- 5.4.5 Others

- 5.5 By Demand Type

- 5.5.1 OEM

- 5.5.2 Replacement

- 5.6 By Region

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 Spain

- 5.6.3.4 Italy

- 5.6.3.5 France

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 BlackBerry QNX

- 6.4.2 Green Hills Software

- 6.4.3 Wind River

- 6.4.4 Continental AG

- 6.4.5 Elektrobit

- 6.4.6 Vector Informatik

- 6.4.7 Renesas Electronics

- 6.4.8 Siemens Digital Industries (Embedded Mentor)

- 6.4.9 NXP Semiconductors

- 6.4.10 LYNX Software Technologies

- 6.4.11 Real-Time Systems (RTX)

- 6.4.12 Bosch ETAS

- 6.4.13 Aptiv

- 6.4.14 Harman (Samsung)

- 6.4.15 Denso

- 6.4.16 Qualcomm

- 6.4.17 KPIT Technologies

- 6.4.18 TTTech Auto

- 6.4.19 SYSGO

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment