|

시장보고서

상품코드

2063379

로보택시 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Robo Taxi - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

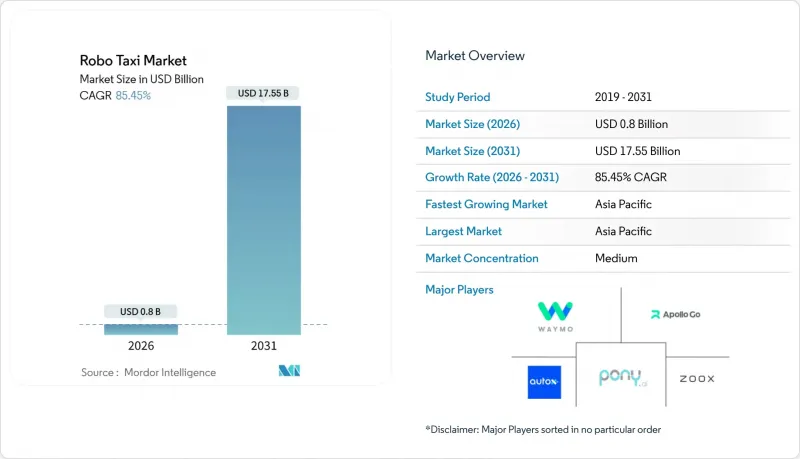

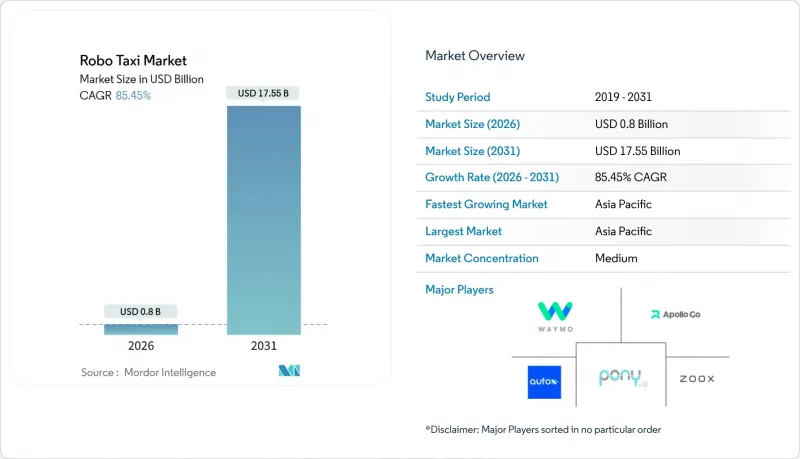

Mordor Intelligence에 의하면, 로보택시 시장 규모는 2026년에 8억 달러로 평가되었고, 2031년까지 175억 5,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 85.45%로 확대해 갈 전망입니다.

본 보고서는 자율주행 수준별(레벨 4 및 레벨 5), 추진 방식별(배터리 전기차, 하이브리드 전기차 등), 차종별(승용차 및 밴/셔틀), 용도별(여객 운송 및 화물/소포 운송), 서비스 유형별, 비즈니스 모델별, 차량 소유 형태별, 운영 환경별, 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(대수)으로 제시되어 있습니다.

세계의 로보택시 시장 동향 및 인사이트

정부의 자율주행차 실증 실험 및 규제 샌드박스

조건부 면제를 통해 이론 모델 대신 실제 데이터를 사용할 수 있게 됨으로써, 로보택시 시장의 검증 기간이 단축됩니다. 2025년 8월, Zoox는 자율주행차 면제 프로그램(AVEP)에 따라 미국 도로교통안전국(NHTSA)으로부터 최초로 실증 면제를 획득했습니다. 이 획기적인 성과로 인해, Zoox가 미국에서 제조한 전용 설계 자율주행차는 특정 조건이 충족된다는 전제 하에, 기존의 수동 제어 없이 운행할 수 있게 되었습니다. 중국 교통운수부는 2024년 중반 이후 여러 주요 도시에서 완전 무인 주행의 공개 시험을 허용해 왔으며, 이를 통해 수백만 마일에 달하는 승객 수송이 실현되고 있습니다. 아부다비는 2025년 11월, 안전 운전기사 없이 운행하는 상업 운행을 승인함으로써 해당 지역에서의 비약적인 보급을 위한 토대를 마련했습니다. 사업자들은 이러한 초기 인가를 활용하여 안전 실적을 쌓아, 보다 보수적인 시장으로의 진출을 용이하게 하고 있습니다.

2025년 8월 6일, 미국 도로교통안전국(NHTSA)은 미국산 전용 자율주행 차량에 대해 자율주행 차량 면제 프로그램(AVEP)에 근거한 사상 최초의 시범 운행 면제를 Zoox에 부여함으로써, 특정 조건 하에서 기존의 수동 제어 없이 운행할 수 있도록 허용했습니다.

자율주행 모빌리티 벤처 기업에 사상 최대 규모의 자금 유입

2024년 10월, Waymo는 Alphabet이 주도하고 외부 투자자들의 지원을 받은 56억 달러 규모의 자금 조달 라운드를 완료했습니다. 이러한 움직임은 로보택시 시장의 상용화가 코앞으로 다가왔습니다는 점에 대한 투자자들의 신뢰가 높아지고 있음을 여실히 보여주었습니다. 한편, Waabi는 AI 기반 시뮬레이션 플랫폼을 강화하기 위해 막대한 자금을 조달함으로써 대규모 도로 시험의 필요성을 대폭 줄였습니다. 주요 기업들의 기업공개(IPO)와 전략적 분사(스핀아웃)가 잇따르는 가운데, 자원은 엄선된 소수의 선도 기업에 집중되고 있어 기존의 규모의 경제 효과가 더욱 강화되고 있습니다.

막대한 초기 설비 투자와 불투명한 회수 기간

로보택시 시장의 경우, 전용 차량과 센서 시스템의 비용이 높기 때문에 대부분의 도시에서 손익분기점에 도달하기까지의 기간이 상당히 길어지고 있습니다. 2024년 12월, 제너럴 모터스(GM)는 누적 손실이 확대됨에 따라 자율주행 차량 호출 사업에서 철수했습니다. 바이두(Baidu)의 RT6와 같이 고도로 최적화된 설계라 하더라도, 이러한 차량이 운행을 시작하려면 막대한 초기 투자가 필요합니다. 여전히 해결해야 할 과제가 남아 있습니다. 즉, 한산한 시간대의 가동률이 현저히 낮아져, 이로 인해 전반적인 수익성이 하락하고 있습니다.

부문별 분석

2025년 도입 대수에서 레벨 4 시스템은 62.05%를 차지했습니다. 그러나 안전 운전사의 인건비가 운영비에서 사라질 것으로 예상에 따라, 레벨 5 시스템은 2031년까지 연평균 성장률(CAGR) 88.02%를 기록하며 이를 상회할 것으로 전망됩니다. 2025년 하반기 Waymo가 고속도로 노선에 서비스를 확대한 것은 진입로 합류나 고속 주행 중 차선 변경이 현재의 인지 및 계획 능력 범위 내에 있음을 보여주었습니다.

운용 설계 영역이 확대됨에 따라 공항 운행, 지방 지역 서비스 범위 확대, 도시 간 회랑이 실현되어 차량당 수익 주행 거리가 증가할 것으로 보입니다. Zoox는 NHTSA로부터 스티어링 휠이 필요 없는 특별 승인을 획득했으며, 이는 중복화된 제동, 조향 및 인식 각 계층이 동등한 안전성을 달성할 경우 규제 당국이 레벨 5를 인증할 것임을 시사합니다. 원격 운용 센터가 운영자 1명당 50대 이상의 차량을 관리함으로써, 인건비는 차량 내 안전 운영자를 지속적으로 배치하는 비용보다 낮아지며, 경제성 측면에서는 완전 자율 주행 쪽으로 기울게 됩니다.

2025년에는 배터리식 전기차 플랫폼이 72.13%의 점유율을 차지했습니다. 이는 제로 배출 구역에 대한 인센티브와 마일당 에너지 비용이 저렴하다는 점이 영향을 미쳤습니다. 하이브리드 차량은 두 가지 파워트레인의 정비가 필요하며, 많은 주요 도시의 혼잡통행료 면제 대상에도 포함되지 않습니다. 배터리식 전기자동차의 로보택시 시장 점유율은 배터리 팩 가격 하락과 시의회의 배기가스 규제 강화에 힘입어 2031년까지 연평균 성장률(CAGR) 87.14%로 확대될 것으로 전망됩니다.

특별히 설계된 Baidu의 RT6는 운전자용 하드웨어를 배제함으로써 에너지 효율을 최적화하고, 놀라운 주행 거리를 실현하고 있습니다. 이러한 접근 방식을 통해 하이브리드 세단과 동등한 성능을 유지하면서 에너지 비용을 절감하고 있습니다. Zoox사는 133kWh 배터리를 탑재한 전용 설계 차량이 한 번 충전으로 16시간 이상 주행할 수 있다고 주장하고 있습니다. 이를 통해 정해진 충전 간격을 설정함으로써 하루 종일 서비스를 제공할 수 있게 됩니다. 그러나 연료전지 시제품은 수소 인프라가 미비하고 관련 비용이 높다는 등의 과제에 직면해 있습니다.

2025년에는 편의성 기준과 기존 세단용 공급망을 배경으로 승용차가 전체 운행의 68.22%를 차지했습니다. 한편, 밴 및 셔틀 서비스는 소포 배송 계약과 캠퍼스 내 고정 노선 서비스에 힘입어 연평균 성장률(CAGR) 86.03%를 기록하며 성장할 것으로 전망됩니다. 누로의 3세대 카고팟은 교외 식료품 배송 노선을 운행하며, 주간 가동률이 매우 높아, 피크 시간대에 집중되는 경향이 있는 승용차 활용 사례보다 더 높은 자산 생산성을 보여주고 있습니다.

EasyMile의 EZ10과 Navya의 Autonom Shuttle은 공항 및 비즈니스 단지에서 100만 킬로미터 이상의 상용 주행 실적을 기록하고 있으며, 이는 저속 자율주행이 규제 측면에서 시장 진입을 앞당기는 효과적인 수단임을 입증하고 있습니다. 내부 구조를 재구성할 수 있어 주야간 모드를 전환할 수 있으며, 기기당 수익을 극대화할 수 있습니다.

지역별 분석

아시아태평양은 2025년에 46.09%의 점유율로 로보택시 시장을 주도한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 85.79%를 기록하며 성장할 것으로 전망됩니다. 중국 교통운수부는 여러 주요 도시에서 완전 무인 운전 서비스를 승인했으며, 이에 따라 2025년 1월까지 Apollo Go의 누적 승차 횟수는 900만 회를 돌파했습니다. Pony.ai가 선전에서 취득한 전 지역 운행 허가는 다수의 자율주행차를 대상으로 하고 있으며, 이는 해당 지역의 규제 측면에서 보여주는 추진력을 보여줍니다. 일본과 한국은 국내 제조 역량을 활용해 지역 내 실증 실험을 추진하고 있는 반면, 인도는 정책 진전이 더딘 편이지만 교통 체증 완화에 대한 기대감으로 인해 주목을 받고 있습니다.

북미는 2위를 차지했으며, Waymo의 여러 도시에서의 운영이 이를 주도하고 있습니다. 현재 이 회사의 운영 구역에는 고속도로 구간도 포함되어 있습니다. NHTSA가 스티어링 휠이 없는 전용 차량을 규제 대상에서 제외하겠다는 의사를 밝힌 것은 주별 보험 요건에 차이가 있음에도 불구하고 연방 정부의 지지를 시사합니다. 토론토와 밴쿠버에서 진행 중인 캐나다의 시범 사업은 운영 설계 영역(ODD)을 확대하기 위해 한랭 지역에서의 검증에 주력하고 있습니다.

유럽은 보수적인 형식 인증 절차와 분산된 책임 기준 때문에 규모 면에서 뒤처져 있습니다. 그럼에도 불구하고, 독일의 레벨 4 관련 법규는 제조업체의 책임을 명확히 규정하고 있어, 국내 OEM 각사에서 시험 운용 차량이 모여들고 있습니다. EasyMile과 Navya의 자율주행 캠퍼스 셔틀은 100만 킬로미터 이상을 주행했으며, 저속 주행 영역이 시장 진입의 관문임을 여실히 보여주고 있습니다. 중동은 비약적인 발전을 이루는 지역으로 부상하고 있습니다. 아부다비에서는 세계 최초로 완전 자율주행 기반의 상용 서비스가 시작되었으며, 두바이에서는 운영 사업자와 수익을 분배하는 정부의 우대 조치를 바탕으로 차량을 대폭 증차할 계획입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the robo taxi market size reached USD 0.80 billion in 2026 and is projected to touch USD 17.55 billion by 2031, advancing at an 85.45% CAGR over the forecast period.

This report is Segmented by Level of Autonomy (Level 4 and Level 5), Propulsion (Battery-Electric, Hybrid-Electric, and More), Vehicle Type (Car and Van/Shuttle), Application (Passenger Transportation and Goods/Parcel Transportation), Service Type, Business Model, Fleet Ownership, Operating Environment, and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Robo Taxi Market Trends and Insights

Government AV Pilots and Regulatory Sandboxes

Conditional exemptions enable the use of real-world data to substitute for theoretical models, thereby reducing validation timelines in the Robo Taxi Market. In August 2025, Zoox became the first recipient of a demonstration exemption from the National Highway Traffic Safety Administration under the Automated Vehicle Exemption Program (AVEP). This milestone enables Zoox's American-built, purpose-designed automated vehicle to operate without conventional manual controls, provided that certain specified conditions are met China's Ministry of Transport has permitted fully driverless public trials across multiple tier-1 cities since mid-2024, enabling millions of passenger-carrying miles. Abu Dhabi authorized commercial operations without safety drivers in November 2025, setting the stage for regional leapfrog adoption. Operators use early approvals to accrue safety records that ease expansion into more conservative markets.

On August 6, 2025, NHTSA granted Zoox the first-ever demonstration exemption under the Automated Vehicle Exemption Program (AVEP) for an American-built purpose-built automated vehicle, enabling operation without traditional manual controls under specified conditions."

Record Capital Inflows into Autonomous-Mobility Ventures

In October 2024, Waymo secured a USD 5.6 billion funding round, spearheaded by Alphabet and bolstered by external investors. This move highlighted the escalating investor confidence in the imminent commercialization of the Robo Taxi Market. Meanwhile, Waabi raised substantial capital to enhance its AI-driven simulation platform, significantly reducing the need for extensive on-road testing. As major IPOs and strategic spin-outs emerge, they're centralizing resources among a select few leaders, intensifying the prevailing scale advantages.

High Upfront CAPEX and Uncertain Payback

In most cities, breakeven periods for purpose-built vehicles and sensor suites are significantly long due to their high costs in the Robo Taxi Market. In December 2024, General Motors discontinued its autonomous ride-hailing venture after incurring substantial cumulative losses. Even with highly optimized designs, like Baidu's RT6, considerable upfront investment is required before these vehicles can enter service. A persistent challenge remains: off-peak hours experience significant underutilization, which dampens overall returns.

Other drivers and restraints analyzed in the detailed report include:

- Declining AD-Sensor and Computing Costs

- Maas Platform Integration Unlocking Fleet Utilization

- Persistent Public-Trust and Safety-Perception Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Level 4 systems accounted for 62.05% of 2025 deployments; however, Level 5 is projected to outpace this with an 88.02% CAGR to 2031, as safety-driver wages are expected to disappear from operating ledgers. Waymo's expansion to freeway routes in late 2025 showed that on-ramp merging and high-speed lane changes are within current perception-and-planning capabilities.

Wider operational design domains will unlock airport runs, rural coverage, and inter-city corridors, raising revenue miles per vehicle. Zoox has obtained a steering-wheel-free exemption from the NHTSA, indicating that regulators will certify Level 5 once redundant braking, steering, and perception layers achieve safety equivalency. As remote operations centers supervise 50-plus vehicles per human, labor overhead falls below the cost of retaining in-car safety operators, tipping economics toward full autonomy.

Battery-electric platforms held a 72.13% share in 2025, reflecting the influence of zero-emission zone incentives and low per-mile energy costs. Hybrid alternatives carry dual-powertrain maintenance and fail to qualify for congestion-pricing exemptions in multiple capitals. The robo taxi market share for battery-electric vehicles is forecast to expand with a 87.14% CAGR through 2031 as pack prices decrease and city councils tighten emissions regulations.

Baidu's RT6, designed for a purpose, achieves an impressive range by optimizing energy efficiency through the removal of driver-centric hardware. This approach aligns its performance with hybrid sedans while reducing energy costs. Zoox claims that its purpose-built vehicle, equipped with a 133 kWh battery, can go over 16 hours on a single charge. This enables full-day service with designated charging intervals. However, fuel-cell prototypes face challenges due to the limited availability of hydrogen infrastructure and higher associated costs.

Passenger cars accounted for 68.22% of rides in 2025, driven by comfort benchmarks and existing sedan supply chains. Vans and shuttles, however, are forecast to grow at 86.03% CAGR, propelled by parcel contracts and fixed-route campus services. Nuro's third-generation cargo pod runs suburban grocery loops with notable daytime utilization, demonstrating higher asset productivity than peak-biased passenger use cases.

EasyMile's EZ10 and Navya's Autonom Shuttle log over 1 million commercial kilometers across airports and business parks, validating low-speed autonomy as a fast-track regulatory entry point. Reconfigurable interiors permit day-night mode switching, maximizing revenue per chassis.

Geography Analysis

The Asia-Pacific region led the robo taxi market with a 46.09% share in 2025 and is projected to grow at an 85.79% CAGR through 2031. China's Ministry of Transport has authorized fully driverless services in multiple tier-1 cities, accelerating cumulative ride counts beyond nine million for Apollo Go by January 2025 . Pony.ai's city-wide permit in Shenzhen covers a significant number of autonomous cars, demonstrating the region's regulatory momentum. Japan and South Korea leverage domestic manufacturing strength to push local pilots, while India attracts interest for congestion relief despite slower policy progress.

North America ranks second, led by Waymo's multi-city operations, which now include freeway segments. NHTSA's willingness to exempt purpose-built vehicles without steering wheels signals federal support, even as state-level insurance requirements remain uneven. Canadian pilots in Toronto and Vancouver concentrate on cold-weather validation to expand operational design domains.

Europe trails in volume due to conservative type-approval processes and fragmented liability norms. Nevertheless, Germany's Level 4 statute clarifies manufacturer responsibility, drawing pilot fleets from domestic OEMs. Autonomous campus shuttles from EasyMile and Navya have logged over 1 million kilometers, highlighting lower-speed niches as entry points. The Middle East emerges as a leapfrog region: Abu Dhabi hosts the first fully driverless commercial service, and Dubai plans to significantly expand its fleets, backed by government concessions that share revenue with operators.

- Waymo LLC

- Apollo Go

- AutoX Inc.

- Pony.ai

- Zoox, Inc.

- Tesla, Inc.

- DiDi Autonomous Driving

- Avride Inc. (Yandex Self-Driving Group)

- EasyMile SAS

- Navya Mobility SAS

- Nuro Inc.

- Motional, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government AV Pilots and Regulatory Sandboxes

- 4.2.2 Record Capital Inflows into Autonomous-Mobility Ventures

- 4.2.3 Declining AD-Sensor and Computing Costs

- 4.2.4 MaaS Platform Integration Unlocking Fleet Utilization

- 4.2.5 Purpose-Built Autonomous Van Architectures for Last-Mile Logistics

- 4.2.6 Urban Congestion Pricing Nudging Shared Autonomy

- 4.3 Market Restraints

- 4.3.1 High Upfront CAPEX and Uncertain Pay-Back

- 4.3.2 Persistent Public Trust and Safety-Perception Gap

- 4.3.3 Patchy Global Liability and Safety Certification Regimes

- 4.3.4 V2X Cybersecurity Vulnerabilities

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Level of Autonomy

- 5.1.1 Level 4

- 5.1.2 Level 5

- 5.2 By Propulsion

- 5.2.1 Battery-Electric Vehicles

- 5.2.2 Hybrid-Electric Vehicles

- 5.2.3 Fuel-Cell Electric Vehicles

- 5.3 By Vehicle Type

- 5.3.1 Car

- 5.3.2 Van / Shuttle

- 5.4 By Application

- 5.4.1 Passenger Transportation

- 5.4.2 Goods / Parcel Transportation

- 5.5 By Service Type

- 5.5.1 Rental-Based (free-floating)

- 5.5.2 Station-Based (hub-to-hub)

- 5.6 By Business Model

- 5.6.1 B2C (direct to riders)

- 5.6.2 B2B (corporate / logistics contracts)

- 5.6.3 Public-Transit Integration

- 5.7 By Fleet Ownership

- 5.7.1 OEM-Owned

- 5.7.2 Operator-Owned (TNCs and start-ups)

- 5.7.3 Public-Agency-Owned

- 5.8 By Operating Environment

- 5.8.1 Urban Core

- 5.8.2 Sub-Urban / Campus

- 5.8.3 Highway / Inter-city

- 5.8.4 Mixed-Use Zones

- 5.9 By Geography

- 5.9.1 North America

- 5.9.1.1 United States

- 5.9.1.2 Canada

- 5.9.1.3 Rest of North America

- 5.9.2 South America

- 5.9.2.1 Brazil

- 5.9.2.2 Argentina

- 5.9.2.3 Rest of South America

- 5.9.3 Europe

- 5.9.3.1 Germany

- 5.9.3.2 United Kingdom

- 5.9.3.3 France

- 5.9.3.4 Italy

- 5.9.3.5 Spain

- 5.9.3.6 Russia

- 5.9.3.7 Rest of Europe

- 5.9.4 Asia-Pacific

- 5.9.4.1 China

- 5.9.4.2 Japan

- 5.9.4.3 India

- 5.9.4.4 South Korea

- 5.9.4.5 Rest of Asia-Pacific

- 5.9.5 Middle East and Africa

- 5.9.5.1 Turkey

- 5.9.5.2 Saudi Arabia

- 5.9.5.3 United Arab Emirates

- 5.9.5.4 South Africa

- 5.9.5.5 Nigeria

- 5.9.5.6 Rest of the Middle East and Africa

- 5.9.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Waymo LLC

- 6.4.2 Apollo Go

- 6.4.3 AutoX Inc.

- 6.4.4 Pony.ai

- 6.4.5 Zoox, Inc.

- 6.4.6 Tesla, Inc.

- 6.4.7 DiDi Autonomous Driving

- 6.4.8 Avride Inc. (Yandex Self-Driving Group)

- 6.4.9 EasyMile SAS

- 6.4.10 Navya Mobility SAS

- 6.4.11 Nuro Inc.

- 6.4.12 Motional, Inc.

7 Market Opportunities & Future Outlook

- 7.1 Autonomous Ride-Hailing Integration into City MaaS Platforms

- 7.2 Dedicated Robo-Van Networks for Last-Mile Parcel Delivery

- 7.3 Subscription-Based Robo-Taxi Services for Senior Mobility

- 7.4 Cross-Border Robo-Taxi Corridors (e.g., EU Schengen Pilot)

- 7.5 Carbon-Credit Monetization for Zero-Emission Robo-Taxi Fleets