|

시장보고서

상품코드

2063427

마이크로 LED 칩 매스 트랜스퍼 장비 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Micro LED Chip Mass Transfer Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

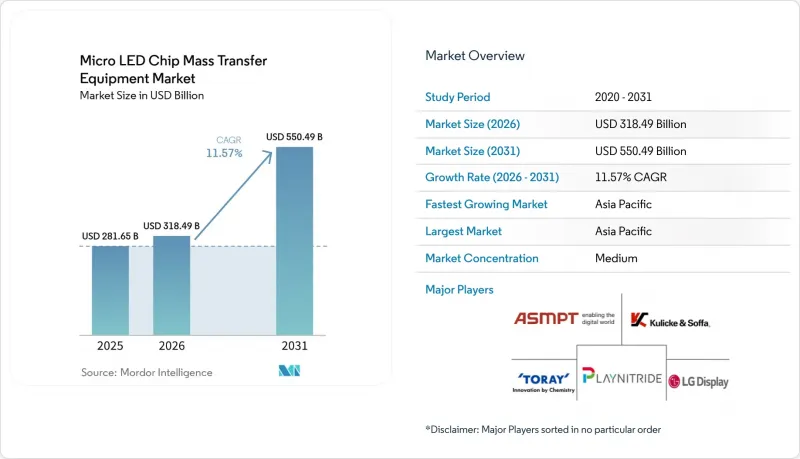

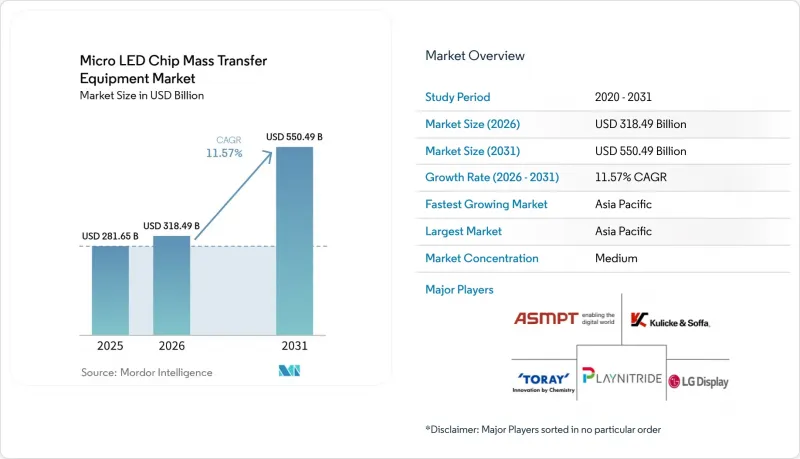

Mordor Intelligence에 의하면, 마이크로 LED 칩 매스 트랜스퍼 장비 시장 규모는 2025년 2,816억 5,000만 달러로 평가되었습니다. 2026년 3,184억 9,000만 달러에서 2031년까지 5,504억 9,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 11.57%를 나타낼 것으로 예측됩니다.

본 보고서는 전사 기술(엘라스토머 스탬프 전사, 레이저 전사, 정전기 전사, 유체 전사 등), 장치 아키텍처(웨이퍼 간 전사, 웨이퍼에서 패널로의 전사, 칩에서 패널로의 전사 등), 용도(소비자용 전자기기, AR/VR 디스플레이 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 마이크로 LED 칩 매스 트랜스퍼 장비 시장 동향 및 인사이트

고급 가전제품 시장에서 마이크로 LED 디스플레이 수요 증가

현재 MicroLED는 플래그십 스마트폰, 스마트 워치, 그리고 대형 TV 분야에서 OLED의 사실상 후속 기술로 자리 잡고 있습니다. 삼성은 2026년에 마이크로 RGB TV 라인업을 55-115인치 크기로 확대하고, 패널당 수백만 개의 마이크로LED 다이를 표준화하는 한편, 주요 외주 조립 파트너사의 연간 설비 가동률을 높였습니다. PlayNitride는 AUO와 협력하여 스마트 워치 및 자동차용 주문에 대응하기 위해 6인치 GaN-on-silicon 웨이퍼의 생산 규모를 확대하고, 2026년 생산 능력 계획을 20% 상향 조정했습니다. 각 디스플레이 제조업체들은 블루칩과 양자점을 활용한 색상 변환 방식에서 진정한 RGB 전사 방식으로의 전환을 가속화하고 있습니다. 이 방식에서는 3회의 연속적인 배치 주기가 필요하지만, 발광 효율을 최대 40%까지 향상시킬 수 있습니다. LG 디스플레이는 2024년에 22.3인치 액티브 매트릭스 방식 마이크로 LED 타일을 전시했습니다. 이는 136인치 4K 월에 통합되는 것으로, 상용 수준의 처리량을 바탕으로 50마이크로미터 미만의 스탬프 전사에 의존하는 모듈식 전략입니다. 시장 연구기관 Omdia는 2025년부터 2026년에 걸쳐 마이크로 LED 디스플레이 매출이 두 배로 증가할 것으로 전망하고 있으며, 이는 설비 수주의 단기적인 증가를 뒷받침하는 것입니다(omdia.tech.informa.com).

차세대 디스플레이 생산 라인에 대한 지속적인 투자

아시아태평양의 패널 제조업체들은 기존의 LTPS 및 a-Si 생산 공장을 마이크로 LED 시범 생산 라인으로 전환하고 있으며, 2024년부터 2025년에 걸쳐 10억 달러 이상을 웨이퍼-투-패널 및 하이브리드 제조 장비에 투자하고 있습니다. 충칭에 위치한 BOE의 6세대 생산라인은 2025년 초에 생산을 시작하며,월5만 장의 생산 능력을 바탕으로 LTPO 백플레인과 독립형 마이크로LED 파일럿 구역을 모두 지원하고 있습니다. 천마(Tianma)는 2024년 12월, 11억 위안(1억 5,500만 달러)을 투자해 공장을 완공했습니다. 이 공장에는 시간당 4,000만 칩을 처리할 수 있는 3.5세대 풀 레이저 전사 시스템이 도입되어 있습니다. AUO의 4.5세대 캠퍼스는 2025년에 양산을 시작했으며, 2026년 ‘AFEELA’ 출시를 앞두고 소니 모빌리티에 콕핏 모듈을 공급하고 있습니다. 2024년 11월부터 가동을 시작한 HC SemiTek의 주하이 에피웨이퍼 라인은 중국의 수입 의존도를 낮추고, 다운스트림 공정의 전사 인증을 위한 웨이퍼 공급 안정성을 높이고 있습니다. 투자의 대부분은 중국, 대만, 한국에 집중되어 있지만, 미국 기업들은 CHIPS법의 세액 공제를 활용하여 첨단 패키징 거점에 시범 생산 라인을 함께 설치하고 있습니다.

OLED 대체 기술에 비해 높은 설비 투자 비용과 공정의 복잡성

새로운 마이크로 LED 생산 라인을 건설하는 데는 2억-3억 달러가 필요하며, 이는 OLED의 증착 및 봉합 능력을 확장하는 데 드는 추가 비용의 약 2배에 해당합니다. LG디스플레이가 2025년부터 2027년에 걸쳐 편성된 1조 원(7억 5,000만 달러) 규모의 예산 중 대부분은 OLED에 배정되었으며, 마이크로 LED는 AMOLED 백플레인에 통합되는 파일럿 모듈 수준에 그치고 있습니다(lgdisplay.com). AUO의 4.5세대 공장 건설비는 20억 대만 달러(6,670만 달러)였으나,월6인치 웨이퍼 1만 장밖에 생산할 수 없어 규모의 경제 효과가 제한적임을 보여줍니다(auo.com). MicroLED 제조에는 최대 12개의 공정이 필요하며, 각 공정에서 수율이 떨어지기 때문에 초기 단계의 수율은 약 60-70%에 그칩니다. 이에 비해 OLED의 수율은 85-90%입니다(onlinelibrary.wiley.com). 삼성은 제품 라인을 세분화함으로써 이러한 부담을 줄이고 있습니다. 초고급 110-140인치 자체 발광형 벽면 디스플레이는 높은 비용을 감수하는 반면, 비용이 최적화된 Micro RGB TV는 픽셀별 제어 기능을 희생함으로써 합리적인 가격을 실현하고 있습니다(news.samsung.com). 장비 제조업체들은 단계적인 투자가 가능한 모듈식 도구로 이에 대응하고 있지만, 이로 인해 보수적인 패널 제조업체의 경우 투자 회수 기간이 6-8년으로 늘어날 것입니다.

부문별 분석

2025년에는 엘라스토머 스탬프 방식의 공구가 마이크로 LED 칩 마스터 전사 장비 시장 규모의 41.68%를 차지하며 시장을 주도했습니다. 이는 수십 년에 걸친 프린트 전자 기술 노하우를 활용하여, 대형 사이니지 기판 위에 10-20 마이크로미터 크기의 다이를 초당 1만-2만 개씩 배치할 수 있기 때문입니다. 이러한 간편함, 소모품의 저렴한 가격, 그리고 곡면형 자동차 계기판과의 호환성이 수요를 뒷받침하고 있습니다. 그러나 망막 해상도의 AR 광학계 등 5 마이크로미터 미만의 미세화를 추구하는 용도에서는 스탬핑으로 인한 가장자리 손상이나 접착 위치의 어긋남이 두드러지게 나타납니다. 그 결과, 레이저 지원형 포워드 전사가 매출의 약 3분의 1을 차지했습니다. 이는 Coherent사의 UVtransfer 및 이와 유사한 엑시머 레이저 솔루션이 10배 빠른 속도로 서브마이크로미터 수준의 공차를 실현한 데서 비롯된 것입니다. 유체식이나 정전기식 접근 방식은 여전히 틈새 시장 수준에 머물러 있지만, 기존 기업들이 무시할 수 없는 특허의 씨앗이 되고 있습니다.

하이브리드 설계는 레이저 박리의 압도적인 속도와 정전기식 또는 진공식 픽 앤 플레이스를 통한 부드러운 착지 제어를 결합하여, 단일 장비로 3-100 마이크로미터 범위의 다이를 처리할 수 있게 해줍니다. 이러한 조합을 통해 순차 처리형 장치에 비해 사이클 타임을 약 40% 단축할 수 있으며, 이는 하이브리드 플랫폼의 예상 연평균 성장률(CAGR) 12.33%를 뒷받침하는 기반이 되고 있습니다. VueReal의 카트리지 시스템은 제조 공정 간에 미리 충전된 다이 카세트를 교체할 수 있어, 다품종 생산에서 민첩성을 상징한다고 할 수 있습니다. 한편, ASMPT는 0.01% 미만의 위치 편차를 즉시 보정하는 자동 복구 헤드를 통합하고 있으며, 패널의 다이 수가 2,000만 개를 초과하는 경우 이는 필수적인 기능이 됩니다. 이러한 성능의 융합으로 인해, 계획 기간 동안 칩 크기의 변화에 대비해야 하는 신규 팹에서 하이브리드 시스템은 기본 선택지로 자리 잡고 있습니다.

지역별 분석

2025년 마이크로 LED 칩 전사 장비 시장 매출의 62.83%를 아시아태평양이 차지했으며, 에피택셜 성장, 전사, 백플레인 조립 과정을 클러스터 캠퍼스 내에 집약한 중국 및 대만의 대기업들이 시장을 주도했습니다. 천마(Tianma), BOE, Visionox 등 3개사는 2024년부터 2025년에 걸쳐 시범 생산 라인 및 4.5세대 생산 라인에 총 15억 달러 이상을 투자하여 개발 주기를 단축하는 한편, 지역 공급업체들에게 선점 우위를 안겨주었습니다. 한국 정부가 수립한 4,840억 원(3억 5,000만 달러) 규모의 인센티브 계획은 국내 웨이퍼 및 본딩 기술의 격차를 해소함으로써 전략적 깊이를 더하고 있으며, 인증 마일스톤이 달성되면 현지 장비 구매를 촉진할 가능성이 높습니다.

연평균 성장률(CAGR) 12.16%의 성장이 예상되는 북미에서는 ‘CHIPS법’에 따른 세액 공제 및 보조금이 에피택셜 성장에서 이종 통합에 이르는 그린필드 투자로 전환되고 있습니다. 초기 지원 대상에는 Amkor, GlobalFoundries, Intel, SK Hynix의 첨단 패키징 거점이 포함되어 있으며, 이들 거점은 레이저 전사 플랫폼을 칩렛과 마이크로 LED 모두에 활용할 수 있습니다. 뉴욕주에 위치한 Meta의 Haylo 팹은 5마이크로미터 미만의 청색 및 녹색 다이 공급망의 핵심을 담당하고 있는 반면, Rocket Lab에 대한 Veeco의 Lumina+ MOCVD 출하량은 대량 전사 수요로 이어지는 상·하류 분야의 파급 효과를 보여주고 있습니다.

유럽 시장 점유율은 약 8%에 그치고 있으며, 대량 생산을 하는 디스플레이 제조업체는 적지만, EU 칩법의 감가상각 우대 조치의 혜택을 받고 있습니다. 이에 따라 자동차 내장재 및 항공우주용 HUD를 목표로 하는 연구개발 실험실과 파일럿 모듈 개발이 활발히 진행되고 있습니다. 세계의 그 밖의 지역(주로 동남아시아와 중동)은 중국 및 대만 브랜드에게 지정학적 리스크를 헤지할 수 있는 틈새 조립 거점으로 남아 있지만, 현재로서는 대규모 설비 발주까지는 이르지 못하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the micro lED chip mass transfer equipment market size is projected to expand from USD 281.65 billion in 2025 and USD 318.49 billion in 2026 to USD 550.49 billion by 2031, registering a CAGR of 11.57% between 2026 to 2031.

This report is Segmented by Transfer Technology (Elastomer Stamp Transfer, Laser Transfer, Electrostatic Transfer, Fluidic Transfer, and More), Equipment Architecture (Wafer-To-Wafer, Wafer-To-Panel, Chip-To-Panel, and More), Application (Consumer Electronics, AR/VR Displays, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Micro LED Chip Mass Transfer Equipment Market Trends and Insights

Growing Demand for Micro LED Displays in Premium Consumer Electronics

MicroLED is now the de facto successor to OLED in flagship smartphones, watches, and large-screen televisions. Samsung expanded its Micro RGB television line in 2026 to 55-115-inch sizes, normalizing millions of microLED dies per panel and boosting annual tool utilization at key outsourced assembly partners. PlayNitride, working with AUO, scaled six-inch GaN-on-silicon wafer output for smartwatch and automotive orders, driving a 20% boost in capacity plans for 2026. Display makers are accelerating the shift from blue-chip plus quantum-dot color conversion to true RGB transfer, which demands three sequential placement cycles but increases luminous efficiency by up to 40%. LG Display demonstrated a 22.3-inch active-matrix microLED tile in 2024 that stitches into 136-inch 4K walls, a modular strategy that relies on sub-50 micrometer stamp transfer at commercial throughputs. Research firm Omdia expects microLED display revenue to double between 2025 and 2026, confirming the near-term uptick in equipment orders omdia.tech.informa.com.

Ongoing Investments in Next-Gen Display Manufacturing Lines

Asia-Pacific panel makers are repurposing legacy LTPS and a-Si fabs for microLED pilot lines, funneling more than USD 1 billion between 2024 and 2025 into wafer-to-panel and hybrid tools. BOE's sixth-generation line in Chongqing entered production in early 2025, with 50,000 sheets per month supporting both LTPO backplanes and a separate microLED pilot zone. Tianma completed a RMB 1.1 billion (USD 155 million) plant in December 2024 featuring a G3.5 full-laser transfer system rated at 40 million chips per hour. AUO's 4.5-generation campus reached mass production in 2025, supplying Sony Mobility with cockpit modules for the 2026 AFEELA launch. HC SemiTek's Zhuhai epi-wafer line, live since November 2024, reduces China's import dependency and enhances wafer availability for downstream transfer qualification. While the bulk of spending centers on China, Taiwan, and South Korea, U.S. firms leverage CHIPS Act credits to co-locate pilot lines with advanced-packaging hubs.

High Capital Expenditure and Process Complexity vs. OLED Alternatives

A greenfield microLED line requires USD 200-300 million, roughly double the incremental cost of extending OLED evaporation and encapsulation capacity. LG Display's W 1 trillion (USD 750 million) budget for 2025-2027 earmarks a majority for OLED, keeping microLED in pilot modules that piggyback on AMOLED backplanes lgdisplay.com. AUO's 4.5-generation plant cost NTD 2 billion (USD 66.7 million) yet supports only 10,000 six-inch wafers per month, illustrating the constrained economies of scale auo.com. MicroLED production involves up to twelve process steps, each compounding yield loss to roughly 60-70% at early maturity, compared with OLED's 85-90% onlinelibrary.wiley.com. Samsung mitigates the burden by segmenting its product line: ultra-luxury 110-140 inch self-emissive walls absorb higher costs, whereas cost-optimized Micro RGB televisions trade off per-pixel control for attainable price points news.samsung.com. Equipment builders respond with modular tools that allow staged investments, but this elongates payback to six-eight years for conservative panel makers.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Mass-Transfer Throughput and Yield Metrics

- Government Incentives for Domestic Semiconductor-Equipment Production

- Limited Supply Chain for High-Uniformity MicroLED Epitaxial Wafers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Elastomer-stamp tools dominated 2025 with 41.68% of the Micro LED chip mass transfer equipment market size, leveraging decades of printed-electronics know-how to place 10-20 micrometer dies across large signage substrates at 10,000-20,000 dies per second. Their simplicity, low consumable cost, and compatibility with curved automotive clusters sustain demand. Yet applications that push below 5 micrometers, such as retinal-resolution AR optics, expose stamp-induced edge damage and adhesion drift. Laser-assisted forward transfer therefore captured almost one-third of revenue, propelled by Coherent's UVtransfer and similar excimer solutions that hit sub-micrometer tolerances at tenfold higher speeds. Fluidic and electrostatic approaches remain niche, but they seed patents that incumbents cannot ignore.

Hybrid designs marry the raw speed of laser release with the gentle landing control of electrostatic or vacuum pick-and-place, enabling a single frame to process die ranges from 3 to 100 micrometers. The combination lowers cycle time by roughly 40% compared with sequential tools and underpins the 12.33% CAGR expected for hybrid platforms. VueReal's cartridge system, capable of swapping pre-filled die cassettes between builds, epitomizes high-mix agility. Meanwhile, ASMPT integrates auto-repair heads that rework sub-0.01% mismatches in-situ, an essential feature once panel die counts exceed 20 million. The performance blend positions hybrid systems as default selections for new fabs that must hedge against die-size evolution over the planning horizon.

Geography Analysis

Asia-Pacific dominated with 62.83% of Micro LED chip mass transfer equipment market revenue in 2025, anchored by Chinese and Taiwanese conglomerates that co-locate epi-growth, transfer, and backplane assembly within cluster campuses. Tianma, BOE, and Visionox collectively deployed more than USD 1.5 billion on pilot and Gen 4.5 lines between 2024 and 2025, compressing development loops and giving regional vendors first-mover runway. South Korea's KRW 484 billion (USD 350 million) incentive blueprint adds strategic depth by plugging domestic wafer and bonding gaps, a move likely to lift local tool purchases once qualification milestones are met.

North America, forecast to expand at a 12.16% CAGR, is translating CHIPS Act tax credits and grants into green-field investments that span epi-growth through heterogeneous integration. Early awards cover Amkor, GlobalFoundries, Intel, and SK Hynix advanced-packaging hubs that can repurpose laser-transfer platforms for chiplets and microLEDs alike. Meta's Haylo fab in New York State anchors the supply chain for sub-5 micrometer blue and green dies, while Veeco's Lumina+ MOCVD shipments to Rocket Lab illustrate upstream-downstream pull effects that ripple into mass-transfer demand.

Europe, at roughly 8% share, lacks high-volume display makers yet benefits from EU Chips Act depreciation perks that spur R&D labs and pilot modules aimed at automotive interiors and aerospace HUDs. Rest-of-World regions, mainly Southeast Asia and the Middle East, remain niche assembly hubs that hedge geopolitical risk for Chinese and Taiwanese brands but have not yet placed substantial tool orders.

- ASMPT Ltd.

- Kulicke & Soffa Industries Inc.

- Toray Engineering Co. Ltd.

- PlayNitride Inc.

- LG Display Co. Ltd.

- K&S NeoLight (Rohinni-K&S JV)

- Rohinni LLC

- TDK Corporation

- Coherent Corp.

- Aixtron SE

- Veeco Instruments Inc.

- QMAT Inc.

- Samsung Electronics Co. Ltd.

- BOE Technology Group Co. Ltd.

- Visionox Technology Inc.

- AUO Corporation

- Innolux Corporation

- Saphlux Inc.

- Plessey Semiconductors Ltd.

- Tianma Microelectronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand For Micro LED Displays In Premium Consumer Electronics

- 4.2.2 Ongoing Investments In Next-Gen Display Manufacturing Lines

- 4.2.3 Advancements In Mass Transfer Throughput And Yield Metrics

- 4.2.4 Government Incentives For Domestic Semiconductor Equipment Production

- 4.2.5 Adoption Of Chiplet-Ready Transfer Platforms For Modular AR/VR Optics

- 4.2.6 Integration Of AI-Based Vision Systems For In-Process Defect Detection

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure And Process Complexity Vs. OLED Alternatives

- 4.3.2 Limited Supply Chain For High-Uniformity Micro LED Epitaxial Wafers

- 4.3.3 Thermal Stress-Induced Warpage During Wafer-to-Panel Transfer Cycles

- 4.3.4 IP Litigation Risks Around Elastomer Stamp Patents In China

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Transfer Technology

- 5.1.1 Elastomer Stamp Transfer

- 5.1.2 Laser Transfer

- 5.1.3 Electrostatic Transfer

- 5.1.4 Fluidic Transfer

- 5.1.5 Hybrid Transfer

- 5.2 By Equipment Architecture

- 5.2.1 Wafer-to-Wafer

- 5.2.2 Wafer-to-Panel

- 5.2.3 Chip-to-Panel

- 5.2.4 Repair Transfer Systems

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 AR/VR Displays

- 5.3.3 Automotive Displays

- 5.3.4 Commercial Displays

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.2 North America

- 5.4.3 Europe

- 5.4.4 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASMPT Ltd.

- 6.4.2 Kulicke & Soffa Industries Inc.

- 6.4.3 Toray Engineering Co. Ltd.

- 6.4.4 PlayNitride Inc.

- 6.4.5 LG Display Co. Ltd.

- 6.4.6 K&S NeoLight (Rohinni-K&S JV)

- 6.4.7 Rohinni LLC

- 6.4.8 TDK Corporation

- 6.4.9 Coherent Corp.

- 6.4.10 Aixtron SE

- 6.4.11 Veeco Instruments Inc.

- 6.4.12 QMAT Inc.

- 6.4.13 Samsung Electronics Co. Ltd.

- 6.4.14 BOE Technology Group Co. Ltd.

- 6.4.15 Visionox Technology Inc.

- 6.4.16 AUO Corporation

- 6.4.17 Innolux Corporation

- 6.4.18 Saphlux Inc.

- 6.4.19 Plessey Semiconductors Ltd.

- 6.4.20 Tianma Microelectronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment