|

시장보고서

상품코드

2063669

마이크로 LED 칩 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Micro LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

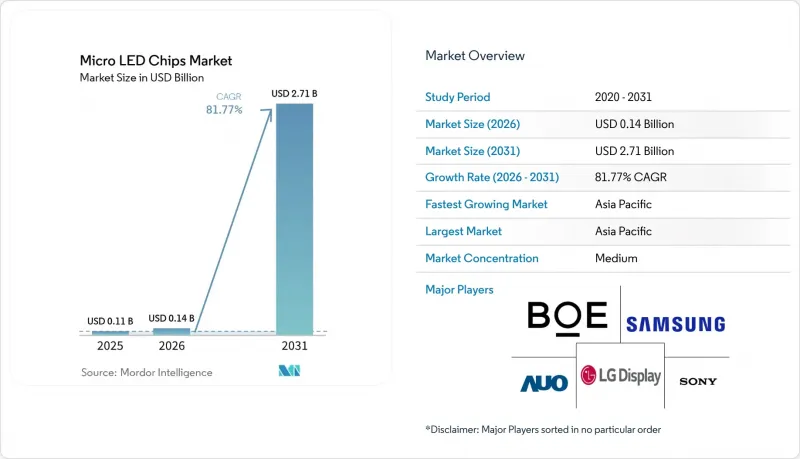

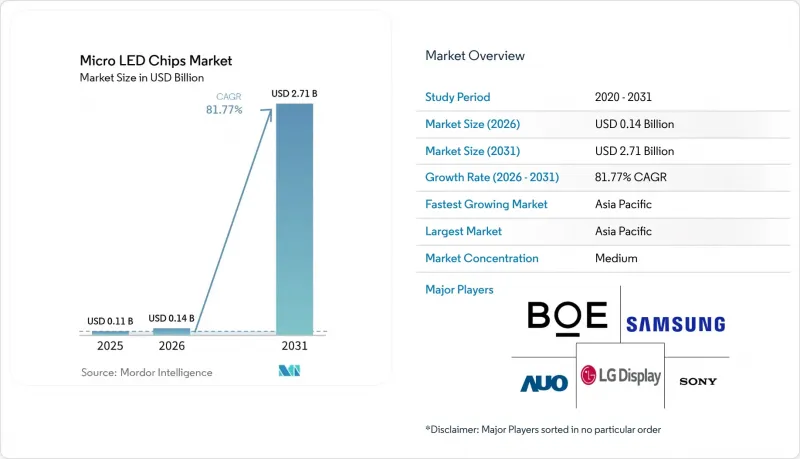

Mordor Intelligence에 의하면, 마이크로 LED 칩 시장 규모는 2025년 1억 800만 달러로 평가되었습니다. 2026년 1억 3,700만 달러에서 2031년까지 27억 1,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 81.77%에 이를 것으로 예측됩니다.

본 보고서는 칩 크기(1-20mm, 20-50mm 및 그 이상), 반도체 소재(GaN/InGaN 및 AlGaInP), 용도(스마트 워치 및 웨어러블, AR/VR 근안 디스플레이, TV, 스마트폰 및 태블릿, 자동차용 디스플레이, 디지털 사이니지/대형 디스플레이, 기타), 지역(북미, 유럽, 아시아태평양, 기타)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 마이크로 LED 칩 시장 동향 및 인사이트

애플과 삼성, 자체 개발 마이크로 LED 통합 로드맵 가속화

CES 2026에서 삼성의 TV 로드맵이 55-130인치 Micro RGB 모델로 확대되었으며, 블루라이트 위험성에 대한 인증 없이 BT.2020 색상 범위를 100% 구현한다는 사실이 확인되었습니다. LG는 이에 대응해 Micro RGB Evo 시리즈를 발표하며, OLED에 대한 의존에서 벗어나 수직 통합형 공급망으로 전략을 전환하겠다는 의지를 보였습니다. 소니는 Crystal LED S 시리즈를 위해 ‘True RGB’ 상표 등록을 진행하며, 프리미엄 브랜드가 얼리 어답터를 확보하기 위한 수단으로서 브랜딩을 중시하고 있음을 강조했습니다. 애플은 공식적으로는 침묵을 지키고 있지만, 이 회사의 워치 프로토타입을 통해 삼성의 적극적인 규모 확대와는 대조적으로, 아직 모색 단계에 있는 듯한 자세가 엿보입니다. 이러한 차이로 인해, TV 사업의 수익이 웨어러블 및 AR 단말기용 다이 크기의 학습 곡선을 상쇄하는 양극화된 생태계가 형성되고 있습니다.

6인치 GaN-on-Si 웨이퍼의 생산 규모 확대를 통한 비용 절감

BOE HC Semitek의 7억 달러 규모의 주하이 프로젝트는 연간 5만 8,000장의 6인치 웨이퍼를 생산할 예정이며, 기존의 4인치 라인에 비해 유효 다이 면적을 4배로 확대하고, 칩 1장당 에피택셜 비용을 약 50% 절감할 것입니다. PlayNitride의 예측에 따르면, 이러한 학습 곡선으로 인해 고휘도 이용 사례 분야에서 마이크로 LED 칩 시장은 2028년까지 OLED 시장과 같은 규모에 도달할 것으로 전망됩니다. 호난 대학이 개발한 1,000만 니트를 초과하는 6인치 GaN-on-Si 웨이퍼는 더 큰 직경에서도 광학적 무결성이 확보됨을 입증하고 있습니다. 15억 달러 규모의 CHIPS법에 따른 보조금을 통해 GlobalFoundries는 서반구에 GaN-on-Si 공급 거점을 구축할 수 있게 되었으며, 이를 통해 자동차 및 방위 분야에서의 지정학적 위험을 줄이고 있습니다. 이러한 움직임들이 맞물리면서 OLED와의 비용 격차가 줄어들고, 공급망의 지리적 재편이 진행되고 있습니다.

4인치 미만의 웨이퍼를 사용한 10µm 미만의 적색 LED의 수율은 60% 미만입니다.

10µm 미만의 AlGaInP 적색 칩의 외부 양자 효율은 알루미늄 질화물을 이용한 패시베이션을 통해 22.3%까지 향상되었으나, 상업적 수율은 여전히 녹색 및 청색 칩에 비해 현저히 낮은 수준에 머물러 있습니다. 사이드월의 산화 처리를 통해 비방사 재결합은 감소하지만, 수율을 60% 이상으로 끌어올리지는 못하고 있어 폐기 비용이 발생하여 이익률을 압박하고 있습니다. Samsung Electronics와 LG는 패널당 다이 수가 적은 TV의 경우, 더 큰 크기의 적색 다이를 채택함으로써 이 문제를 해결하고 있습니다. 한편, 웨어러블 기기나 AR 디바이스에서는 양자점을 이용한 다운컨버전 방식을 적용한 청색 GaN 어레이가 채택되고 있어, 비용과 제조 공정이 증가하고 있습니다. 업계에서는 6인치 AlGaInP 웨이퍼를 사용하면 에지 제거 및 온도 구배를 줄일 수 있다는 견해가 일반적이지만, 현재로서는 해당 직경에 대한 공식적인 수율 데이터는 아직 존재하지 않습니다.

부문별 분석

1-20µm 부문은 연평균 성장률(CAGR) 83.21%를 나타낼 것으로 예측되며, 이는 모든 크기 등급 중에서 가장 높은 성장률입니다. 이는 가민의 1,999.99달러짜리 ‘Fenix 8 Pro MicroLED’가 4,500니트의 야외 가시성을 위해 소비자들이 기꺼이 비용을 지불할 의향이 있음을 입증하기 때문입니다. Jade Bird Display사의 1만 0,160 PPI ‘Roadrunner’ 마이크로 패널은 근시용 디스플레이의 보급 곡선을 결정짓는 요소가 다이 비용이 아니라 화소 밀도임을 보여주고 있습니다. 그러나 배터리 사용 시간은 여전히 AMOLED에 미치지 못하며, 전력 차이를 줄이기 위해서는 드라이버 IC의 집적화를 더욱 추진해야 합니다.

대형 디스플레이는 수율이 높고 대량 전사 시 허용 오차가 넉넉한 50-100µm 크기의 다이로 전환되고 있습니다. 삼성의 130인치 모델과 LG의 100인치 모델은 100µm 미만의 RGB LED를 채택하여, 벽 한 면을 가득 채울 듯한 대형 화면 크기를 자랑하면서도 비용 관리를 유지하며 BT.2020 색역을 100% 커버하고 있습니다. 자동차용 HUD 유닛은 그 중간에 위치하며, 20-50µm 크기의 다이(die)를 사용하여 밀도와 처리량의 균형을 맞추고 있습니다. BOE의 HERO 2.0과 Tianma의 모듈은 이러한 최적의 균형을 구현하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 62.30%를 차지했으며, 연평균 성장률(CAGR) 84.36%를 나타낼 것으로 전망되어 마이크로 LED 칩 시장의 중심이 되고 있습니다. 중국의 ‘속도와 규모’ 모델은 BOE의 5만 8,000 웨이퍼 규모 주하이 공장과 삼안광전의 5,000만 개 규모 미니 LED 생산 확대에 잘 드러나 있으며, 이 지역에 타의 추종을 불허하는 칩 공급 역량을 제공합니다. 대만은 초고해상도 틈새 시장을 주도하고 있습니다. AUO가 가민용 패널 수주를 확보한 것과 ASE가 가오슝에 5억 7,900만 달러 규모의 백엔드 공장을 건설하는 것은 생태계 전략을 반영하고 있습니다. 한국은 TV 통합 조립 분야에서 선두를 달리고 있지만, 여전히 많은 칩을 수입하고 있어 업스트림 공정에 대한 투자 여지가 있음을 보여주고 있습니다.

북미의 전망은 CHIPS법의 시행에 달려 있습니다. 전 세계 파운드리 업체들의 GaN-on-Si 생산 라인에 15억 달러가 투자되고 있는 반면, 인텔과 TSMC는 마이크로 LED 및 드라이버 부품을 생산할 가능성이 있는 첨단 노드 팹 건설을 위해 총 255억 달러를 조달하고 있습니다. 2026년 1월부터 발효된 수입 첨단 칩에 대한 25% 관세는 OEM 각사가 국내 조달로 전환하도록 유도할 가능성이 있지만, 단기적인 비용 상승을 초래할 것입니다. 유럽에는 이에 상응하는 인센티브가 없어 에피택시 및 패널은 수입에 의존하고 있지만, 푸조를 통한 자동차 OEM 업체들의 관심은 잠재적인 수요를 시사하고 있습니다.

남미와 중동은 초기 단계 시장이며, 고급 옥외 간판과 자동차 개조가 보급의 계기가 될 것입니다. 현지 생산은 이루어지지 않지만, 마이크로 LED의 긴 수명과 높은 밝기는 플래그십 매장의 외관이나 고급 전기차의 대시보드에 이를 도입하는 것을 정당화해 줍니다. 규제의 미비, 특히 자동차 안전 기준과 관련된 문제는 전 세계적인 과제이며, 기술적 준비가 갖춰진 경우에도 도입을 지연시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the micro LED chips market size is projected to expand from USD 0.108 billion in 2025 and USD 0.137 billion in 2026 to USD 2.71 billion by 2031, registering a CAGR of 81.77% between 2026 and 2031.

This report is Segmented by Chip Size (1-20 Mm, 20-50 Mm, and More), Semiconductor Material (GaN/InGaN and AlGaInP), Application (Smartwatches and Wearables, AR/VR Near-Eye Displays, Television, Smartphones and Tablets, Automotive Displays, Digital Signage/Large Displays, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Micro LED Chips Market Trends and Insights

Accelerating Apple and Samsung In-house Micro LED Integration Roadmaps

CES 2026 confirmed that Samsung's television roadmap now spans 55-130-inch Micro RGB models, achieving 100% BT.2020 color without blue-light hazard certification. LG countered with its Micro RGB Evo series, signaling a strategic pivot away from reliance on OLEDs and toward vertically integrated supply chains. Sony trademarked "True RGB" for its Crystal LED S Series, underscoring that premium brands see branding as a lever to capture early adopters. Apple remains publicly silent, but its watch prototypes suggest an exploratory posture that contrasts with Samsung's aggressive scale-up. This divergence creates a two-speed ecosystem where television economics may subsidize die-size learning curves for wearable and AR form factors.

Cost Declines from Six-Inch GaN-on-Si Wafer Scale-Up

BOE HC Semitek's USD 700 million Zhuhai project will deliver 58,000 six-inch wafers annually, quadrupling usable die area relative to legacy four-inch lines and slashing per-chip epitaxial cost by roughly 50%. PlayNitride projects that the learning curve will push the micro LED chip market to market size parity with OLED by 2028 for high-brightness use cases. Hunan University's six-inch GaN-on-Si wafers exceeding 10 million nits confirm optical integrity at larger diameters. A USD 1.5 billion CHIPS Act award is enabling GlobalFoundries to build a Western Hemisphere GaN-on-Si source, reducing geopolitical risk for automotive and defense applications. Together, these moves compress the cost gap with OLED and reposition supply chains geographically.

Yield < 60% for Sub-10 µm Red LEDs Below 4-Inch Wafers

The external quantum efficiency of sub-10 µm AlGaInP red dies rose to 22.3% with aluminum-nitride passivation, yet commercial yields still trail those of green and blue counterparts by a wide margin. Side-wall oxidation reduces non-radiative recombination but has not lifted yields above 60%, creating scrap costs that erode margins. Samsung and LG navigate this by using larger red dies for televisions, where die counts per panel are lower. Wearable and AR devices instead deploy blue GaN arrays with quantum-dot down-conversion, adding cost and process steps. Industry consensus holds that six-inch AlGaInP wafers could reduce edge exclusion and thermal gradients, but no public yield data yet exist for that diameter.

Other drivers and restraints analyzed in the detailed report include:

- Laser-Based Mass-Transfer Throughput Gains > 400 Chips/Sec

- Automotive OEM Demand for Sun-Readable HUDs in EV Platforms

- > USD 600 M CapEx Barrier for Greenfield High-Volume Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 1-20 µm segment is forecast to post an 83.21% CAGR, the fastest among all size classes, as Garmin's USD 1,999.99 Fenix 8 Pro MicroLED proves consumer readiness to pay for 4,500-nit daylight performance. Jade Bird Display's 10,160 PPI Roadrunner micro panel showcases that density, not die cost, defines near-eye adoption curves. However, battery life still trails AMOLED, and driver IC integration must improve to close the power gap.

Large-format displays gravitate toward 50-100 µm dies, where yields are higher, and mass-transfer tolerances are looser. Samsung's 130-inch set and LG's 100-inch model rely on sub-100 µm RGB LEDs to hit 100% BT.2020 color while maintaining cost discipline at wall-scale diagonals. Automotive HUD units sit between, using 20-50 µm dies to balance density with throughput; BOE's HERO 2.0 and Tianma's modules exemplify this sweet spot.

Geography Analysis

Asia Pacific generated 62.30% of 2025 revenue and is projected to grow at an 84.36% CAGR, making it the anchor of the micro LED chips market. China's "speed-and-scale" model is epitomized by BOE's 58,000-wafer Zhuhai fab and San'an's 5,000 kk-unit mini-LED ramp, giving the region unmatched die supply depth. Taiwan champions ultra-high-resolution niches; AUO's Garmin panel win, and ASE's USD 579 million backend plant in Kaohsiung reflect an ecosystem strategy. South Korea leads in integrated TV assembly but still imports many chips, indicating room for upstream investment.

North America's outlook hinges on the execution of the CHIPS Act. USD 1.5 billion is funding GlobalFoundries' GaN-on-Si line, while Intel and TSMC are collecting a combined USD 25.5 billion for advanced-node fabs that may house micro LED and driver components. A 25% tariff on imported advanced chips, effective January 2026, could nudge OEMs toward domestic sourcing but raises near-term costs. Europe lacks comparable incentives, relying on imports for epitaxy and panels, though automotive OEM interest via Peugeot indicates latent demand.

South America and the Middle East are early-stage markets where premium outdoor signage and automotive upgrades will seed adoption. Local manufacturing is absent, but micro LEDs' longevity and brightness can justify imports for flagship retail facades and luxury EV dashboards. Regulatory gaps, especially around automotive safety standards, are global, slowing deployment even where technical readiness is proven.

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- Sony Group Corporation

- AUO Corporation

- PlayNitride Inc.

- Epistar Corporation

- Jade Bird Display Inc.

- Plessey Semiconductors Ltd.

- Aledia S.A.

- VueReal Inc.

- San'an Optoelectronics Co., Ltd.

- Innolux Corporation

- Leyard Optoelectronic Co., Ltd.

- Unilumin Group Co., Ltd.

- Kyocera Corporation

- Cree LED, a Smart Global Holdings Company

- OSRAM Opto Semiconductors GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Apple and Samsung In-house Micro LED Integration Roadmaps

- 4.2.2 Cost Declines from Six-Inch GaN-on-Si Wafer Scale-Up

- 4.2.3 Laser-Based Mass-Transfer Throughput Gains >400 Chips/Sec

- 4.2.4 Automotive OEM Demand for Sun-Readable HUDs in EV Platforms

- 4.2.5 Government CHIPS-style Incentives for Domestic Micro-Display Fabs

- 4.2.6 Quantum-Dot Color Conversion Surpassing 80 % Efficiency

- 4.3 Market Restraints

- 4.3.1 Yield <60 % for Sub-10 µm Red LEDs Below 4-inch Wafers

- 4.3.2 >USD 600 M CapEx Barrier for Greenfield High-Volume Lines

- 4.3.3 Lack of Automotive Qualification Standards for Micro LED HUDs

- 4.3.4 Concentrated Supply of GaN-on-Si Wafers in East Asia

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Chip Size

- 5.1.1 1-20 µm

- 5.1.2 20-50 µm

- 5.1.3 50-100 µm

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.3 By Application

- 5.3.1 Smartwatches & Wearables

- 5.3.2 AR/VR Near-Eye Displays

- 5.3.3 Television

- 5.3.4 Smartphones & Tablets

- 5.3.5 Automotive Displays

- 5.3.6 Digital Signage / Large Displays

- 5.3.7 Other Applications (Industrial, Medical)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 LG Display Co., Ltd.

- 6.4.3 Sony Group Corporation

- 6.4.4 AUO Corporation

- 6.4.5 PlayNitride Inc.

- 6.4.6 Epistar Corporation

- 6.4.7 Jade Bird Display Inc.

- 6.4.8 Plessey Semiconductors Ltd.

- 6.4.9 Aledia S.A.

- 6.4.10 VueReal Inc.

- 6.4.11 San'an Optoelectronics Co., Ltd.

- 6.4.12 Innolux Corporation

- 6.4.13 Leyard Optoelectronic Co., Ltd.

- 6.4.14 Unilumin Group Co., Ltd.

- 6.4.15 Kyocera Corporation

- 6.4.16 Cree LED, a Smart Global Holdings Company

- 6.4.17 OSRAM Opto Semiconductors GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment