|

시장보고서

상품코드

2063437

CLV 및 이탈 예측 AI 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)CLV And Churn Prediction AI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

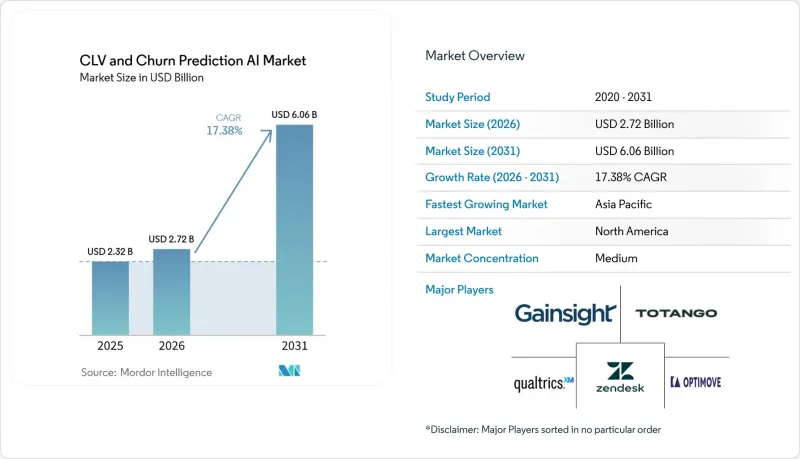

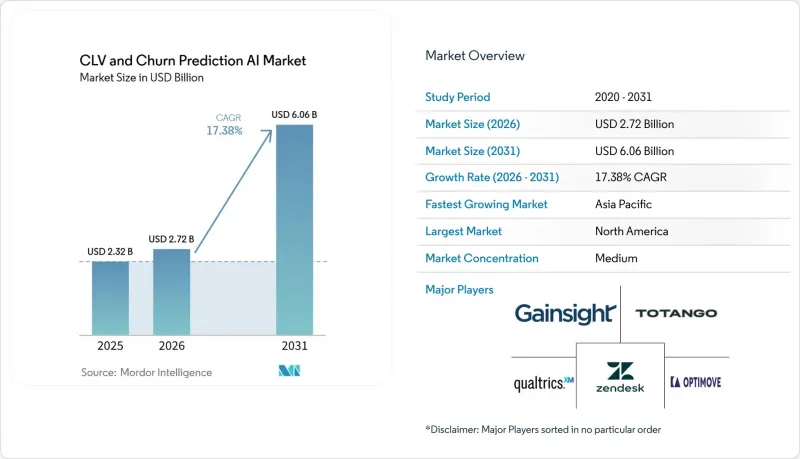

Mordor Intelligence에 의하면, CLV 및 이탈 예측 AI시장 규모는 2025년에 23억 2,000만 달러, 2026년에 27억 2,000만 달러, 2031년까지 60억 6,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 17.38%로 성장할 것으로 전망됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 기업 규모(대기업 및 중소기업), 최종 사용자 산업(소매 및 전자상거래, 은행, 금융서비스 및 보험(BFSI), 통신, 헬스케어, 기타 최종 사용자 산업) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

전 세계 CLV 및 이탈 예측 AI 시장 동향과 인사이트

소매 및 BFSI 업계에서의 예측 분석 도구 도입 확대

소매업체와 은행은 생성형 AI 덕분에 구매를 미루는 참여도가 높은 고객들이 디지털 매장으로 몰려들고 있기 때문에 수익 관리에 실시간 트렌드 스코어링을 도입하고 있습니다. 2024년 연말 연휴 기간 동안, 미국 소매업체로 유입된 생성형 AI를 통한 트래픽은 1,300% 급증했으나, 전환율은 기존 채널보다 9% 낮았습니다. 금융기관 역시 이와 같은 시급성을 안고 있습니다. 180억 달러 규모의 자산을 운용하는 한 자산운용사는 AI 기반 고객 유지 모델을 도입한 결과, 해지율을 15% 낮추고 연간 750만 달러의 비용 절감을 달성했습니다. Klaviyo와 같이 하루에 수십억 건의 상호작용을 처리하는 플랫폼은 예측 인사이트를 스토어프론트 워크플로우에 반영함으로써, 중견 브랜드가 1년 이내에 총상품가치(GMV)를 62% 향상시킬 수 있도록 돕고 있습니다. 아시아태평양의 개인 소비는 2035년까지 36조 달러에 달할 것으로 예상되며, 이미 소비자의 39%가 쇼핑에 생성형 AI를 활용하고 있어 예측 도구의 대상 고객층이 확대되고 있습니다.

고객 유지 전략을 통한 고객 확보 비용 절감의 필요성 증가

디지털 광고 시장의 포화 상태와 검색 행태의 변화로 인해 고객 확보 비용이 증가하고 있으며, 이익을 창출하는 성장을 위한 최단 경로는 고객 유지가 되었습니다. 4조 4,000억 달러 규모의 장기적인 AI 시장 기회 중 영업, 마케팅, 서비스 분야의 활용 사례가 40% 가까이 차지하고 있지만, 현재 시점에서 생성형 AI를 통해 1% 이상의 매출 증가를 달성했다고 보고한 경영진은 절반에도 미치지 못하는 상황입니다. Pecan의 Predictive AI Agent와 같은 노코드 에이전트를 활용하면, 기획자는 단 몇 분 만에 실제 운영 수준의 이탈 예측 모델을 구축할 수 있으며, 수동 예측에 소요되는 시간을 60% 단축할 수 있습니다. 통신 업계의 조사에 따르면, 설명 가능한 앙상블 모델을 활용하여 위험도가 높고 계약 기간이 짧은 고객을 우선적으로 관리함으로써 해지율을 최대 25%까지 낮추고, 고객 유지를 위한 마케팅 비용을 45% 절감할 수 있는 것으로 나타났습니다. 개인화와 공급 탄력성 사이의 균형을 맞추고 있는 소매업체의 경우, 고객 생애 가치가 37% 증가한 반면 재고 부족은 29% 증가하여, 운영상의 제약 조건과 부합하는 예측 모델의 필요성이 다시 한번 부각되었습니다.

데이터의 사일로화와 낮은 데이터 품질이 모델의 정확도를 제한합니다.

기업의 약 3분의 1이 데이터 품질을 AI 도입의 가장 큰 과제로 꼽고 있으며, 시스템 전체에 걸쳐 일관된 데이터 구조를 갖추고 있다고 보고한 기업은 고작 43%에 불과합니다. 이러한 데이터 구조의 불일치는 AI를 효과적으로 도입하려는 조직에게 큰 걸림돌이 되고 있습니다. 의료 분야는 이 과제의 전형적인 예입니다. ClosedLoop와 같은 기업은 설명 가능하고 실용적인 예측을 도출하기 전에, 전자 건강 기록, 비정형 임상 기록, 보험 청구 데이터, 검사 결과, 건강의 사회적 결정 요인 등 다양한 유형의 데이터를 처리해야 합니다. 이러한 데이터 관련 과제를 해결하기 위해, 60%의 기업이 데이터 정리를 전문으로 하는 새로운 서비스 제공업체를 활용하거나, 다양한 분야에 걸친 전문 지식을 갖춘 인재를 채용할 계획을 세우고 있습니다. 이러한 전략적 움직임에 따라 아웃소싱 서비스에 대한 평균 지출이 7% 증가할 것으로 예상되며, 이는 AI 도입에 있어 데이터 관리의 중요성이 커지고 있음을 반영하고 있습니다.

부문별 분석

2025년 시점에서 서비스 부문 시장 규모는 소프트웨어 부문보다 작았으나, 데이터 조화, 모델 검증, EU AI법 준수 여부 점검을 외부에 위탁하는 기업이 늘어남에 따라 2026년부터 2031년까지 연평균 성장률(CAGR) 18.91%로 확대될 것으로 예측됩니다. 기업들은 아웃소싱된 데이터 서비스에 대한 지출을 7% 늘릴 것으로 예상되며, 60%는 데이터 정리 및 다양한 분야의 인재 확보를 목적으로 새로운 파트너와 제휴할 계획입니다. Totango의 ‘Unison’ 솔루션은 전문 서비스와 계약 갱신 몇 달 전에 전화, 이메일, 티켓을 분석하는 맞춤형 모델을 결합한 것으로, 전문적인 인사이트이 도입을 어떻게 뒷받침하고 있는지 보여줍니다. 이러한 변화는 금융 서비스 및 헬스케어 분야로도 확산되고 있으며, 설명 가능성과 편향성 감사에 대해서는 각 분야의 규제 당국이 이를 인식해야 합니다.

소프트웨어는 사용자에게 기술적 장벽을 낮추는 에이전트형 플랫폼의 역량에 힘입어, 2025년 고객 생애 가치(CLV) 및 이탈 예측 AI 시장에서 67.98%의 점유율을 유지할 것으로 전망됩니다. 예를 들어, Pecan의 예측형 AI 에이전트는 모델 배포에 소요되는 시간을 대폭 단축하여 불과 몇 분으로 줄여줍니다. 마찬가지로, ChurnZero의 크레딧 기반 AI 마켓플레이스를 통해 기업은 인력을 늘리지 않고도 사업을 확장할 수 있습니다. 그러나 거버넌스 비용이 계속 상승하는 가운데, 하이브리드형 참여 모델이 주목을 받고 있습니다. 이러한 모델에서는 공급업체가 소프트웨어 라이선스와 관리형 서비스를 결합하여 제공하고 있으며, 이로 인해 순수한 소프트웨어 판매를 통한 수익과 수수료 기반의 구현 서비스를 통한 수익 간의 격차가 점차 좁혀지고 있습니다.

2025년, 클라우드 부문은 CLV 및 이탈률 예측 AI 시장 점유율의 71.78%를 차지했습니다. 이는 Warehouse Native 데이터 플랫폼의 도입과 탄력적인 GPU 용량 확장성에 힘입은 결과입니다. 그러나 유럽 및 중동의 기업들이 투명성 요건을 충족하면서 동시에 데이터 소재지 규정을 준수해야 하는 이중 과제에 직면함에 따라, 하이브리드 방식의 도입은 연평균 성장률(CAGR) 22.54%라는 견실한 성장세를 보일 것으로 전망됩니다. 레노버가 의사결정권자 800명을 대상으로 실시한 최근 조사에 따르면, 58%가 하이브리드 AI 솔루션을 선호하는 것으로 나타났습니다. 이러한 선호의 주된 이유로 꼽힌 것은 강화된 개인정보 보호 제어 기능과, 특정 조직의 요구에 맞추어 솔루션을 맞춤 설정할 수 있다는 점이었습니다. Teradata AI Factory는 확정적인 비용과 GDPR(EU 개인정보보호규정) 준수가 필요한 은행 및 병원을 대상으로 NVIDIA의 AI 스택을 On-Premise 방식으로 제공합니다.

퍼블릭 클라우드는 버스트 트레이닝 지원은 물론, Klaviyo와 Shopify의 실시간 동기화와 같은 생태계 통합을 실현하는 데 있어 계속해서 중요한 역할을 하고 있습니다. 그러나 아웃바운드 통신 비용의 상승과 추론 지연 시간에 대한 우려로 인해, 기업들은 정기적인 스코어링 워크로드를 고객 데이터 근처로 이동시키고 있습니다. On-Premise 솔루션은 국방 및 공공 부문 용도에서 틈새 시장을 유지하고 있는 한편, 관리형 업데이트 스트림과의 통합이 진행되고 있습니다. 이러한 추세에 따라 도입 모델 간의 기존 경계가 점차 모호해지면서, 다양한 인프라 프레임워크 전반에 걸쳐 고객 생애 가치(CLV) 및 이탈 예측 AI 시장 규모가 확대되고 있습니다.

지역별 분석

2025년에도 SaaS 생태계가 영업, 서비스, 마케팅 각 분야에서 AI를 주류로 자리매김시킨 결과, 북미는 CLV 및 이탈률 예측 AI 시장에서 가장 큰 기여를 한 지역으로 남아 있었습니다. 그 예로, Gainsight가 Slack 및 Zendesk 내에 인사이트 기능을 통합한 점과, Forethought와의 제휴를 통해 자율형 에이전트를 추가한 점을 들 수 있습니다. 이 지역은 풍부한 벤처 자금, 견고한 SaaS 생태계, 그리고 풍부한 기술 인력의 혜택을 누리고 있으며, 이 모든 요소가 하나로 어우러져 주도적인 입지를 확고히 하고 있습니다. 그러나 API 비용의 상승은 고객 데이터의 소유권과 관리권을 둘러싼 논쟁을 불러일으키고 있으며, 시장의 성장 궤도에 있어 과제로 대두되고 있습니다.

유럽 및 중동은 하이브리드 모델에 대한 선호도와 규제 준수 기한에 대응해야 할 필요성에 힘입어 급속히 발전하고 있습니다. 지역 조사에 따르면, AI 시범 프로젝트의 46%가本番 환경으로의 전환에 성공했으며, 기업들은 AI 이니셔티브에 1달러를 투자할 때마다 2.78달러의 수익을 올릴 것으로 예상된다고 보고하고 있습니다. 이러한 진전에도 불구하고, 해당 지역의 조직 중 종합적인 거버넌스 체계를 도입한 곳은 고작 27%에 불과합니다. 그 결과, 데이터 통합, 편향 감사, 문서 수집을 전문으로 하는 파트너 기업들이 시장에서 높은 인지도와 경쟁 우위를 확보해 가고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 22.42%를 나타낼 것으로 예측되며, 이는 다른 어떤 지역보다 높은 성장률입니다. 이 지역의 개인 소비는 크게 확대될 것으로 예상되며, 부유층의 소비 증가율은 2025년에 3배에 달하고, 신규 소비의 75%를 차지할 것으로 전망됩니다. 크로스보더 전자상거래와 관광은 국내 시장보다 빠른 속도로 성장하고 있으며, 이로 인해 라이프타임 밸류(LTV) 모델에 여행 빈도나 환율 변동과 같은 복잡한 요소가 더해지고 있습니다. 중국, 인도, 인도네시아, 태국 등 주요 시장의 현지 브랜드들은 AI를 활용해 다국적 기업보다 더 신속하게 개선과 혁신을 추진하고 있습니다. 이러한 추세는 체인 예측 도구에 대한 수요를 가속화하며, 해당 지역 시장 전체의 성장을 견인하는 혁신의 선순환을 반영하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the cLV and Churn Prediction AI market size is projected to be USD 2.32 billion in 2025, USD 2.72 billion in 2026, and reach USD 6.06 billion by 2031, growing at a CAGR of 17.38% from 2026 to 2031.

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (Retail and E-Commerce, BFSI, Telecommunications, Healthcare, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global CLV And Churn Prediction AI Market Trends and Insights

Growing Adoption of Predictive Analytics Tools Across Retail and BFSI

Retailers and banks are embedding real-time propensity scoring into revenue operations because generative AI has flooded digital storefronts with high-engagement shoppers who postpone purchases. During the 2024 holiday season, generative-AI referrals to United States retailers surged 1,300%, yet conversion rates trailed traditional channels by 9%. Financial institutions mirror this urgency; a wealth-management firm with USD 18 billion in assets cut churn by 15% and saved USD 7.5 million annually after deploying an AI-driven retention model. Platforms processing billions of daily interactions, such as Klaviyo, now enable midsize brands to lift gross merchandise value 62% within a year by pushing predictive insights back into storefront workflows. Asia-Pacific's private consumption is on track to reach USD 36 trillion by 2035, with 39% of consumers already using generative AI for shopping, expanding the addressable base for predictive tools.

Rising Need to Reduce Customer Acquisition Costs Through Retention Strategies

Digital advertising saturation and shifting search behaviors have inflated customer acquisition costs, making retention the fastest route to profitable growth. Sales, marketing, and service use cases account for nearly 40% of the USD 4.4 trillion long-term AI opportunity, yet fewer than half of executives report a revenue lift of more than 1% from generative AI so far. No-code agents such as Pecan's Predictive AI Agent let planners build production-grade churn models in minutes, reducing manual forecasting time by 60%. Telecom research shows that explainable ensembles can slash churn by up to 25% and reduce retention marketing costs by 45% by prioritizing high-risk, short-tenure customers. Retailers balancing personalization with supply resilience also saw a 37% increase in customer lifetime value, though stockouts rose 29%, reinforcing the need for predictive models to align with operational constraints.

Data Silos and Poor Data Quality Limiting Model Accuracy

Nearly one-third of enterprises cite data quality as a top AI challenge, with only 43% reporting a consistent data structure across their systems. This inconsistency in data structure poses significant hurdles for organizations aiming to implement AI effectively. The healthcare sector serves as a prime example of this challenge. Companies like ClosedLoop must process a wide range of data types, including electronic health records, unstructured clinical notes, insurance claims, lab results, and social determinants of health, before they can generate explainable, actionable predictions. To address these data-related challenges, 60% of firms are planning to hire new providers specializing in data organization and multidisciplinary talent. This strategic move is expected to increase the average spending on outsourced services by 7%, reflecting the growing importance of data management in AI adoption.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Cloud-Native Customer Data Platforms Enabling Real-Time Churn Scoring

- Increasing Integration of AI in Customer Success Workflows Among SaaS Enterprises

- Shortage of Skilled Data Scientists Constraining Implementation in SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services captured a smaller base than Software in 2025, yet they are forecast to expand at an 18.91% CAGR between 2026 and 2031 as buyers outsource data harmonization, model validation, and EU AI Act conformity checks. Enterprises expect to increase spending on outsourced data services by 7%, and 60% will engage new partners for data organization and access to multidisciplinary talent. Totango's Unison offering bundles professional services with custom models that analyze calls, emails, and tickets months before renewal, illustrating how specialized expertise underpins adoption. The shift extends across financial services and healthcare, where explainability and bias audits demand that domain regulators recognize.

Software is projected to maintain a 67.98% share of the Customer Lifetime Value (CLV) and Churn Prediction AI market in 2025, driven by the ability of agentic platforms to lower technical barriers for users. For instance, Pecan's Predictive AI Agent significantly reduces the time required for model deployment, compressing it to just minutes. Similarly, ChurnZero's credit-based AI marketplace enables businesses to scale operations without adding headcount. However, as governance costs continue to rise, hybrid engagement models are gaining traction. These models involve vendors offering a combination of software licenses and managed services, which is gradually narrowing the gap between revenue generated from pure software sales and fee-based implementation services.

Cloud held 71.78% of the CLV and Churn Prediction AI market share in 2025, driven by the adoption of warehouse-native data platforms and the scalability of elastic GPU capacity. However, hybrid deployments are projected to grow at a robust CAGR of 22.54%, as enterprises in Europe and the Middle East navigate the dual challenges of meeting transparency mandates while adhering to data-residency regulations. A recent Lenovo survey of 800 decision-makers found that 58% prefer hybrid AI solutions. The primary reasons cited for this preference were enhanced privacy controls and the ability to customize solutions to meet specific organizational needs. Teradata AI Factory brings NVIDIA's AI stack on-premises for banks and hospitals that need deterministic costs and GDPR compliance.

Public cloud continues to play a critical role in supporting burst training and enabling ecosystem integrations, such as Klaviyo's real-time synchronization with Shopify. However, rising egress costs and concerns about inference latency are driving organizations to move recurrent scoring workloads closer to customer data. While on-premises solutions maintain a niche presence in defense and public-sector applications, they are increasingly integrating with managed update streams. This trend is gradually blurring the traditional lines between deployment models and expanding the CLV and Churn Prediction AI market size across diverse infrastructure frameworks.

Geography Analysis

North America remained the largest contributor to the CLV and Churn Prediction AI market in 2025, as SaaS ecosystems mainstreamed AI across sales, service, and marketing. Examples include Gainsight embedding insights inside Slack and Zendesk, adding autonomous agents through the Forethought deal. The region benefits from deep venture funding, a robust SaaS ecosystem, and an abundance of technical talent, which collectively cement its leadership position. However, rising API costs have sparked debates over ownership and control of customer data, posing a challenge to the market's growth trajectory.

Europe and the Middle East are advancing rapidly, driven by a preference for hybrid deployment models and the need to meet compliance deadlines. A regional survey revealed that 46% of AI pilots successfully transitioned to production, with companies reporting an anticipated return of USD 2.78 for every USD 1 invested in AI initiatives. Despite this progress, only 27% of organizations in the region have implemented comprehensive governance frameworks. As a result, partners that specialize in data integration, bias audits, and documentation capture are gaining significant mindshare and competitive advantage in the market.

Asia-Pacific is forecast to record a 22.42% CAGR, outpacing every other region. The region's private consumption is expected to grow significantly, with affluent consumers generating three times the spending growth in 2025 and accounting for 75% of new spending. Cross-border e-commerce and tourism are growing at a faster pace than domestic markets, adding complexities such as travel frequency and foreign-exchange variables to lifetime-value models. Local brands in key markets like China, India, Indonesia, and Thailand are leveraging AI to iterate and innovate faster than multinational competitors. This dynamic reflects an innovation loop that is accelerating demand for churn prediction tools and driving the overall growth of the market in the region.

- Gainsight, Inc.

- Qualtrics International Inc.

- Zendesk, Inc.

- Totango Inc.

- ChurnZero Inc.

- Pecan AI Ltd.

- Baremetrics Inc.

- Optimove Ltd.

- Blushift Labs, Inc.

- Klaviyo, Inc.

- HubSpot, Inc.

- ChurnKey, Inc.

- MoEngage, Inc.

- NGDATA NV

- Amperity, Inc.

- BlueConic, Inc.

- Custora, Inc.

- Twilio Inc.

- Alteryx, Inc.

- Express Analytics LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Predictive Analytics Tools Across Retail and BFSI

- 4.2.2 Rising Need to Reduce Customer Acquisition Costs Through Retention Strategies

- 4.2.3 Proliferation of Cloud-Native Customer Data Platforms Enabling Real-Time Churn Scoring

- 4.2.4 Increasing Integration of AI in Customer Success Workflows Among SaaS Enterprises

- 4.2.5 Emergence of Federated Learning Frameworks Addressing Data-Privacy Barriers in Cross-Industry CLV Modeling

- 4.2.6 Demand for Explainable AI to Meet Upcoming EU AI Act Requirements Driving Platform Upgrades

- 4.3 Market Restraints

- 4.3.1 Data Silos and Poor Data Quality Limiting Model Accuracy

- 4.3.2 Shortage of Skilled Data Scientists Constraining Implementation in SMEs

- 4.3.3 Rising API Access Fees from Third-Party Data Vendors Inflating Total Cost of Ownership

- 4.3.4 Model Performance Degradation from Rapidly Shifting Customer Behavior Post-Generative AI Adoption

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-User Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 BFSI

- 5.4.3 Telecommunications

- 5.4.4 Healthcare

- 5.4.5 Other End-User Indutries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Gainsight, Inc.

- 6.4.2 Qualtrics International Inc.

- 6.4.3 Zendesk, Inc.

- 6.4.4 Totango Inc.

- 6.4.5 ChurnZero Inc.

- 6.4.6 Pecan AI Ltd.

- 6.4.7 Baremetrics Inc.

- 6.4.8 Optimove Ltd.

- 6.4.9 Blushift Labs, Inc.

- 6.4.10 Klaviyo, Inc.

- 6.4.11 HubSpot, Inc.

- 6.4.12 ChurnKey, Inc.

- 6.4.13 MoEngage, Inc.

- 6.4.14 NGDATA NV

- 6.4.15 Amperity, Inc.

- 6.4.16 BlueConic, Inc.

- 6.4.17 Custora, Inc.

- 6.4.18 Twilio Inc.

- 6.4.19 Alteryx, Inc.

- 6.4.20 Express Analytics LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment