|

시장보고서

상품코드

2063440

분산형 임상시험 수탁기관(CRO) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Decentralized Clinical Trials Contract Research Organization (CRO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

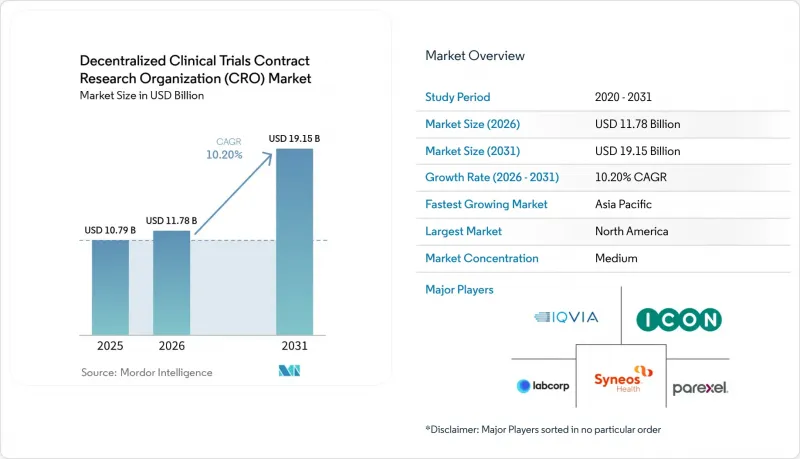

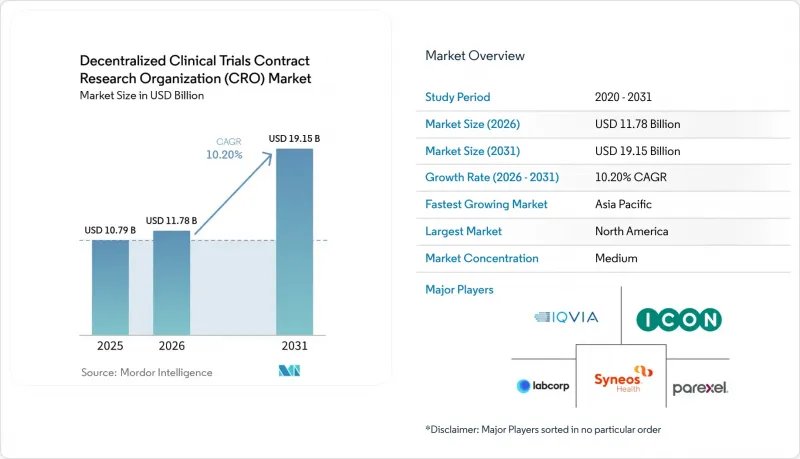

Mordor Intelligence에 의하면, 분산형 임상시험 수탁기관(CRO) 시장 규모는 2025년 107억 9,000만 달러로 평가되었고, 2026년 117억 8,000만 달러로 추정되고, 2031년까지 191억 5,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 10.20%를 나타낼 것으로 예측됩니다.

본 보고서는 서비스 유형별(풀서비스 CRO, 기능별 서비스 제공업체 등), 임상시험 단계별(1상, 2상, 3상 등), 치료 분야별(종양학, 순환기학 등), 최종 사용자별(제약 및 바이오기술 기업 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 분산형 임상시험 수탁기관(CRO) 시장 동향 및 분석

환자 중심의 신속한 피험자 모집 모델을 위한 후원사의 추진

시설 방문에 따른 부담은 선별 검사 실패나 시험 도중 중도의 주된 원인이기 때문에 후원사는 참가자의 편의성을 고려하여 프로토콜을 재설계하고 있습니다. 2024년에 발표된 FDA 지침서에 따르면, 환자 중심 접근 방식은 기존 설계에 비해 피험자 모집 기간을 30-40% 단축할 수 있는 것으로 나타났습니다.

현재 제약 기업들은 프로토콜 작성 단계부터 환자 자문위원회를 구성하고, 모집 예산의 20-25%를 재택 채혈 등의 컨시어지 서비스에 배정하며, CRO의 모바일 간호사 네트워크를 활용해 임상시험용 의약품을 참가자에게 직접 전달하고 있습니다. 이러한 전략은 약물 복용 순응도가 통계적 유의성의 기반이 되는 만성 질환 연구에서 특히 효과를 발휘하며, 확립된 재택치료 자원을 보유한 CRO에 확고한 우위를 제공합니다. 사내에 직원 참여 체계가 갖춰지지 않은 벤처 자본 기반 바이오테크 기업들이 가장 빠르게 도입을 추진하고 있으며, 이것이 중소규모 스폰서의 연평균 성장률(CAGR) 11.25%라는 예측의 배경이 되고 있습니다.

클라우드 eClinical 플랫폼의 급속한 확산

스폰서들이 실시간 데이터 가시성과 적응형 프로토콜 관리를 요구함에 따라, 통합 클라우드 환경은 '선택 사항'에서 '필수 사항'으로 자리 잡았습니다. Veeva Systems는 2025 회계연도 3분기 R&D 클라우드 매출로 6억 7,620만 달러를 기록했습니다. 이는 온프레미스형 도구에서 해당 회사의 Vault Clinical 제품군으로의 전환에 힘입어 전년 동기 대비 15% 증가했습니다. Medidata, Oracle 및 기타 공급업체들은 현재 웨어러블 데이터, ePRO, 원격 진료 기록을 단일 감사 추적으로 통합하여 대조 작업에 소요되는 노력을 40-50% 줄이고 있습니다. 스폰서들은 이러한 플랫폼에 직접 라이선스를 부여하고, 틈새 업무에 대해서는 기능별 제공업체를 활용하는 경향이 강해지고 있으며, 이로 인해 플랫폼의 매출 성장률은 연평균 복합 성장률(CAGR) 12.00%로 가속화되고 있어, 풀서비스 CRO에게는 화이트라벨 제휴 체결이나 기술 자산 인수를 강요하는 압박 요인으로 작용하고 있습니다.

국경을 초월한 데이터 개인정보 보호 및 사이버 보안 격차

2024년 1분기에는 헬스케어 데이터 유출 사고가 급증하여, 145건의 사고로 9,000만 건 이상의 기록이 유출되었고, 임상시험 일정이 최대 6개월 지연되었습니다. 유럽의 GDPR(EU 개인정보보호규정)에 따르면, 동등한 보호 조치가 입증되지 않는 한 데이터를 EU 역내에 보관해야 할 의무가 있어, 스폰서는 별도의 클라우드 인스턴스를 운영할 수밖에 없게 되었고, 이로 인해 IT 예산이 10-15% 증가했습니다. 미국에서는 CCPA와 같은 주법이 제각각 존재하여, 여러 주에 걸친 동의 획득 절차를 복잡하게 만들고 있습니다. 현재 스폰서들은 CRO와의 계약에서 침투 테스트, 사이버 보험 및 데이터 소재지 조항을 의무화하고 있지만, 잔존 위험으로 인해 정신과나 소아과 분야의 보수적인 임상시험은 기존의 시설 기반 설계로 회귀할 가능성이 있습니다.

부문별 분석

2025년 기준으로 풀서비스 벤더는 분산형 임상시험 CRO 시장의 38.23%를 차지했으며, 이는 단일 벤더에 의한 책임 체제를 중시하는 기존의 경향을 반영하고 있습니다. eClinical 플랫폼 제공과 연계된 분산형 임상시험 CRO 시장 규모는 제약사의 IT 팀과의 직접 라이선싱 계약에 힘입어, 연평균 성장률(CAGR) 12.00%를 기록하는 이 틈새 시장에서 급속히 확대될 것으로 전망됩니다. 이와 동시에, 피험자 모집 및 데이터 분석에 특화된 기능별 전문 업체들은 개별 업무 패키지에서 풀서비스형 경쟁사보다 20-30% 낮은 가격을 제시하고 있어, 비용을 중시하는 후원사들 사이에서 지지를 넓혀가고 있습니다. 따라서 플랫폼 제공업체는 밸류체인의 핵심에 위치하며, 높은 수익률을 자랑하는 구독료를 확보하는 동시에 스폰서가 업무 파트너를 자유롭게 선정할 수 있도록 하고 있습니다.

현재 피험자 모집 서비스는 임상시험 예산 전체에서 상당한 비중을 차지하고 있으며, 경쟁이 치열한 파이프라인에서 '첫 피험자 확보 및 첫 방문까지의 속도'가 핵심 요소로 부상함에 따라 그 비중은 더욱 확대될 것으로 예측됩니다. 데이터 관리 기업들은 AI를 도입해 안전성 신호를 자동화하고 있으며, 이에 따라 의뢰사는 피험자 등록을 중단하지 않고도 임상시험 도중에 적격 기준을 수정할 수 있게 되었습니다. 이에 대응하기 위해 풀서비스 CRO들은 독자적인 기술을 확보하기 위해 잇달아 인수를 진행하고 있지만, 통합에 따른 리스크가 단기적인 수익률을 위협하고 있습니다. 한편, 독립 소프트웨어 공급업체들도 그들만의 과제에 직면해 있습니다. 즉, 임상시험이 복잡해질 때 정교한 코드가 오랜 기간 축적된 운영 노하우를 대체할 수 있다고 후원사를 설득하는 것입니다.

2025년, 3상 임상시험은 분산형 임상시험 CRO 시장 매출의 55.23%를 차지한 것으로 평가되었으며, 그 배경에는 예산이 5,000만 달러를 초과하는 경우가 많은 고비용의 종양학 및 희귀질환 임상시험 프로토콜이 있습니다. 그러나 리얼 월드 에비던스(RWE) 요건에 따라 성장 동력은 4상 감시 연구로 이동하고 있으며, 해당 분야는 연평균 성장률(CAGR) 11.50%로 확대되고 있습니다. 대서양 양안의 규제 당국은 전자건강기록(EHR) 및 보험 청구 데이터를 유효한 종점 지표로 인정하고 있으며, 이를 통해 연구 후원사는 비용이 많이 드는 대면 방문을 지속적인 원격 모니터링으로 대체할 수 있게 되었습니다. 이러한 변화는 승인 후 조사와 관련된 분산형 임상시험 CRO 시장 규모를 확대시키고 있으며, 종단적 안전성 데이터에 관심을 갖는 지불 주체들의 주목을 받고 있습니다.

초기 단계 임상시험은 용량 증량 과정에서 집중적인 현장 안전성 모니터링이 필요하기 때문에 분산화의 영향을 어느 정도 피하고 있습니다. 그럼에도 불구하고, 웨어러블 기기의 발전과 함께 시설 내 진료 절차와 원격 진료를 결합한 하이브리드형 2단계 모델이 점차 보급되고 있습니다. 대면 생검과 클라우드 기반 ePRO 업로드를 동기화하는 운영 체계를 확립한 CRO는 고부가가치 적응형 프로그램 입찰에서 확실한 우위를 점하게 될 것입니다.

지역별 분석

2025년, FDA 지침에 따라 규제 불확실성이 해소되고 클라우드 인프라가 견조한 성장세를 보임에 따라, 북미는 분산형 임상시험 CRO 시장 매출의 40.00%를 차지했습니다. 미국의 후원사들은 전 세계 연구개발(R&D) 예산을 주도하고 있으며, 많은 경우 세계 확장에 앞서 국내에서 하이브리드 프로토콜의 시범 시험을 실시했습니다. 한편, 캐나다는 지리적 근접성의 이점을 누리고 있으며, 멕시코는 비용 절감 효과 덕분에 히스패닉계를 대상으로 한 연구를 유치하고 있습니다. 해당 지역의 분산형 임상시험 CRO 시장 규모는 꾸준히 확대되고 있지만, 사이버 보안 보험료와 HIPAA 감사로 인해 운영 비용이 증가하고 있습니다.

아시아태평양은 확실한 성장 동력이며, 2031년까지 연평균 성장률(CAGR) 10.80%를 나타낼 것으로 전망됩니다. 중국은 2024년에 분산형 프로토콜의 심사 기간을 60일로 단축하고, 2023년에는 1,476건의 시험 등록을 촉진했으며, 2025년에는 그 수가 더욱 늘어날 것으로 예측됩니다. 인도는 미국 수준보다 50-60% 낮은 인건비를 활용하고, 원격의료 관련 규정을 개정하여 2·3선 도시에서도 원격 임상시험을 실시할 수 있도록 했습니다. 일본과 호주는 여전히 신중한 태도를 유지하고 있지만, 제한적인 원격 모니터링 체계를 시범적으로 도입하고 있습니다. WuXi AppTec이나 Novotech와 같은 지역 CRO들은 지리적 근접성과 현지 언어 운영 능력을 강점으로 삼고 있지만, BIOSECURE 법안과 같이 미국에서 제안되고 있는 법안들로 인해 향후 미중 협력의 향방은 불투명해지고 있습니다.

유럽에서는 EMA(유럽의약품청)의 지침이 통일되어 있으며, 원격의료 도입도 정착되어 있습니다. 그러나 GDPR(EU 개인정보보호규정)에 따라 스폰서는 유럽 전용 클라우드 환경을 운영할 수밖에 없어, IT 예산이 10-15% 증가하고 있습니다. 독일, 영국, 프랑스가 도입을 주도하고 있으며, 독일의 BfArM(연방의약품의료제품청)은 디지털 헬스 용도에 대해 보험 적용을 실시했습니다. 라틴아메리카와 중동 및 아프리카은 여전히 개발도상 단계에 있습니다. 브라질에서는 ANVISA의 180일 심사 주기와 불안정한 통신 환경이 지역 진출의 걸림돌이 되고 있습니다. 한편, 걸프 연안 국가들의 시범 프로그램은 주로 당뇨병과 종양학에 초점을 맞추고 있어 잠재력은 있지만, 완전히 정착되기까지는 시간이 걸릴 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the decentralized clinical trials contract research organization market size is projected to expand from USD 10.79 billion in 2025 and USD 11.78 billion in 2026 to USD 19.15 billion by 2031, registering a CAGR of 10.20% between 2026 to 2031.

This report is Segmented by Service Type (Full-Service CRO, Functional Service Provider, and More), Trial Phase (Phase I, Phase II, Phase III, and More), Therapeutic Area (Oncology, Cardiology, and More), End-User (Pharmaceutical & Biotechnology Companies, and More), and Geography and More. The Market Forecasts are Provided in Terms of Value (USD).

Global Decentralized Clinical Trials Contract Research Organization (CRO) Market Trends and Insights

Sponsor Push for Patient-Centric, Faster Recruitment Models

Site-visit burden is the leading cause of screen failure and mid-study dropout, so sponsors are redesigning protocols around participant convenience. FDA guidance documents published in 2024 indicate that patient-centric approaches cut enrollment timelines by 30-40% versus traditional designs .

Pharmaceutical companies now embed patient advisory boards during protocol drafting, allocate 20-25% of recruitment budgets to concierge services such as home phlebotomy, and rely on CRO networks of mobile nurses to deliver investigational products directly to participants. These tactics resonate most in chronic-disease studies where adherence underpins statistical power, giving CROs with established home-health resources a defensible edge. Venture-backed biotechs lacking in-house engagement infrastructure are the fastest adopters, underpinning the 11.25% CAGR forecast for small and mid-sized sponsors.

Rapid Cloud eClinical Platform Adoption

Unified cloud environments have moved from optional to essential as sponsors demand real-time data visibility and adaptive protocol control. Veeva Systems logged USD 676.2 million in R&D cloud revenue for Q3 FY 2025, a 15% year-over-year increase fueled by migrations from on-premise tools to its Vault Clinical suite . Medidata, Oracle, and other vendors now integrate wearable streams, ePROs, and tele-visit archives into single audit trails, trimming reconciliation labor by 40-50%. Sponsors increasingly license these platforms directly, then tap functional providers for niche tasks, accelerating platform revenue growth at a 12.00% CAGR and pressuring full-service CROs to form white-label partnerships or acquire technology assets.

Cross-Border Data-Privacy & Cyber-Security Gaps

Healthcare data breaches surged in Q1 2024, with 145 incidents exposing over 90 million records and stalling trial timelines by up to six months. Europe's GDPR requires data to stay within EU borders unless equivalent protections are proven, forcing sponsors to run separate cloud instances and adding 10-15% to IT budgets. The United States operates under a patchwork of state laws, such as CCPA, complicating multi-state consent workflows. Sponsors now mandate penetration tests, cyber-insurance, and data-residency clauses within CRO contracts, but residual risk could push conservative studies psychiatric and pediatric trials back toward traditional, site-based designs.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Green-Lights for Hybrid / Decentralized Designs

- CRO Investment in AI-Driven RWD Recruitment Engines

- Fragmented Asia-Pacific / LATAM Regulatory Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full-service vendors commanded 38.23% of the decentralized clinical trials CRO market share in 2025, reflecting the historical bias for single-vendor accountability. The decentralized clinical trials CRO market size tied to eClinical platform provision is projected to widen quickly as this niche records a 12.00% CAGR, powered by direct licensing deals with pharmaceutical IT teams. In parallel, functional specialists in recruitment or data analytics underbid full-service rivals by 20-30% on discrete work packages, gaining traction among cost-sensitive sponsors. Platform providers, therefore, sit at the fulcrum of the value chain, capturing high-margin subscription fees while allowing sponsors to cherry-pick operational partners.

Patient-recruitment services now hold a significant portion of total study budgets, a share expected to climb as competitive pipelines hinge on speed to first-patient-first-visit. Data-management houses embed AI to automate safety signals, letting sponsors amend eligibility mid-stream without halting enrollment. As a defensive move, full-service CROs have launched acquisition sprees to secure proprietary tech, yet integration risks threaten near-term margins. Stand-alone software vendors face their own challenge: convincing sponsors that elegant code can substitute for years of operational know-how when trials turn complex.

Phase III trials collected 55.23% of the decentralized clinical trials CRO market revenue in 2025, underpinned by big-ticket oncology and rare-disease protocols often budgeted above USD 50 million. Real-world evidence mandates are, however, tilting growth toward Phase IV surveillance, which is advancing at an 11.50% CAGR. Regulators on both sides of the Atlantic accept electronic health records and insurance claims as valid endpoints, letting sponsors replace high-cost observational visits with continuous remote monitoring. This shift lifts the decentralized clinical trials CRO market size tied to post-approval studies and draws interest from payers keen on longitudinal safety data.

Early-phase studies remain partly sheltered from decentralization because dose escalation demands intensive, onsite safety surveillance. Even so, hybrid Phase II models that blend site-based procedures with tele-visits are gaining ground as wearable devices mature. CROs that master the operational choreography of synchronizing in-person biopsies with cloud-based ePRO uploads will hold clear leverage in bids for high-value adaptive programs.

Geography Analysis

North America contributed 40.00% of decentralized clinical trials CRO market revenue in 2025 as FDA guidance resolved regulatory uncertainty and cloud infrastructure remained robust. U.S. sponsors dominate global R&D budgets and often pilot hybrid protocols domestically before global rollout, while Canada benefits from geographic proximity and Mexico attracts Hispanic-focused studies with cost relief. The decentralized clinical trials CRO market size in the region grows steadily, though cybersecurity insurance premiums and HIPAA audits inflate operating costs.

Asia-Pacific is the clear growth engine, set for a 10.80% CAGR through 2031. China shortened decentralized-protocol review timelines to 60 days in 2024, spurring 1,476 trial registrations in 2023 and an even higher tally in 2025. India leveraged labor costs 50-60% below U.S. levels and updated telemedicine rules to open its tier-2 and tier-3 cities to remote trials. Japan and Australia remain cautious but are piloting limited remote-monitoring frameworks. Regional CROs such as WuXi AppTec and Novotech thrive on proximity and local-language operations, although proposed U.S. legislation like the BIOSECURE Act clouds future U.S.-China collaboration.

Europe enjoys harmonized EMA guidance and established tele-health adoption, yet GDPR forces sponsors to operate Europe-only cloud instances, adding 10-15% to IT budgets. Germany, the United Kingdom, and France lead uptake, with Germany's BfArM reimbursing digital-health applications. Latin America and the Middle East & Africa remain nascent. Brazil's 180-day ANVISA review cycle and inconsistent connectivity hold back regional expansion, while Gulf states' pilot programs focus mainly on diabetes and oncology, indicating potential but slow maturation.

- IQVIA

- Laboratory Corporation

- ICON

- Parexel International Corp.

- Syneos Health

- MedPace

- Thermo Fisher Scientific (PPD)

- Charles River

- WuXi App Tec

- Tigermed Co. Ltd.

- PSI CRO

- Premier Research

- Worldwide Clinical Trials

- Novotech

- KCR S.A.

- CMIC Group

- Advanced Clinical

- Frontage Laboratories

- Science 37 Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sponsor Push for Patient-Centric, Faster Recruitment Models

- 4.2.2 Rapid Cloud E Clinical Platform Adoption

- 4.2.3 Regulatory Green-Lights for Hybrid / Decentralized Designs

- 4.2.4 CRO Investment In AI-Driven RWD Recruitment Engines

- 4.2.5 Home-Health Nursing Networks for Last-Mile Procedures

- 4.2.6 LEO-Satellite Connectivity for Rural Data Streaming

- 4.3 Market Restraints

- 4.3.1 Cross-Border Data-Privacy & Cyber-Security Gaps

- 4.3.2 Fragmented Asia-Pacific / LATAM Regulatory Pathways

- 4.3.3 Digital-Skill Shortage at Trial Sites

- 4.3.4 Wearable-Sensor Kit Price Inflation

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Full-Service CRO

- 5.1.2 Functional Service Provider (FSP)

- 5.1.3 Patient Recruitment & Retention

- 5.1.4 Data Management & Analytics

- 5.1.5 eClinical Platform Provision

- 5.2 By Trial Phase

- 5.2.1 Phase I

- 5.2.2 Phase II

- 5.2.3 Phase III

- 5.2.4 Phase IV / Post-Marketing

- 5.3 By Therapeutic Area

- 5.3.1 Oncology

- 5.3.2 Cardiology

- 5.3.3 CNS Disorders

- 5.3.4 Rare Diseases

- 5.3.5 Others

- 5.4 By End-User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Medical Device Companies

- 5.4.3 Academic & Research Institutes

- 5.4.4 Small & Mid-Sized Sponsors

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 IQVIA Holdings Inc.

- 6.3.2 Laboratory Corporation

- 6.3.3 ICON plc

- 6.3.4 Parexel International Corp.

- 6.3.5 Syneos Health

- 6.3.6 Medpace Holdings Inc.

- 6.3.7 Thermo Fisher Scientific (PPD)

- 6.3.8 Charles River Laboratories

- 6.3.9 WuXi AppTec

- 6.3.10 Tigermed Co. Ltd.

- 6.3.11 PSI CRO AG

- 6.3.12 Premier Research

- 6.3.13 Worldwide Clinical Trials

- 6.3.14 Novotech

- 6.3.15 KCR S.A.

- 6.3.16 CMIC Group

- 6.3.17 Advanced Clinical

- 6.3.18 Frontage Laboratories

- 6.3.19 Science 37 Holdings Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment