|

시장보고서

상품코드

2063441

폴리에틸렌 테레프탈레이트(PET) 섬유 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Polyethylene Terephthalate (PET) Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

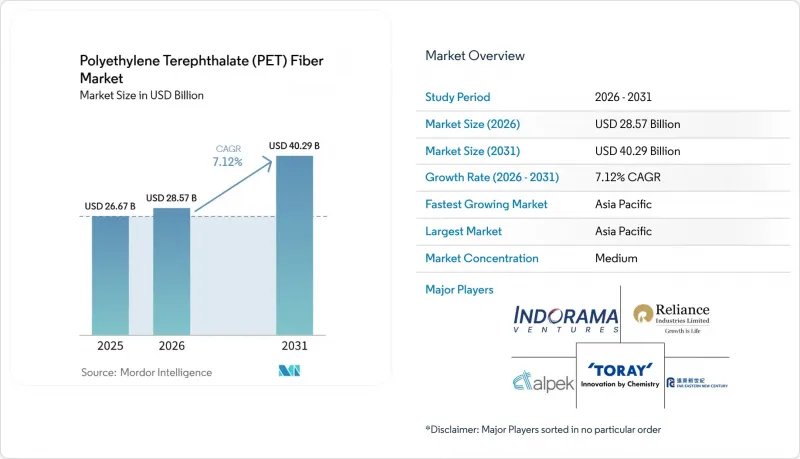

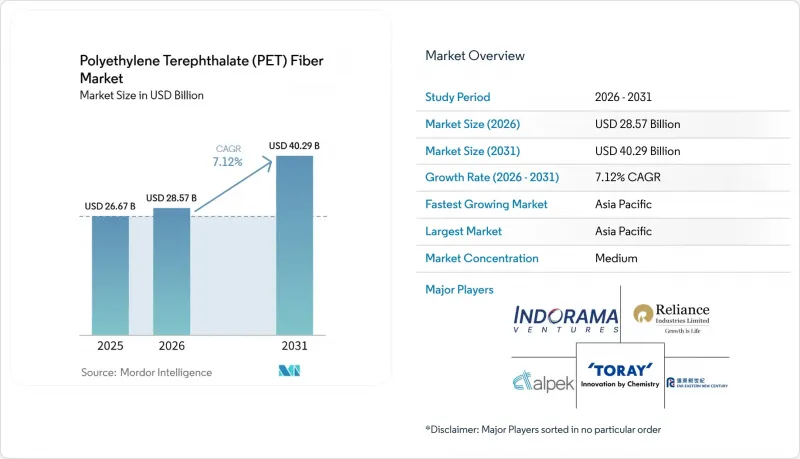

Mordor Intelligence에 의하면, 폴리에틸렌 테레프탈레이트(PET) 섬유 시장 규모는 2025년 266억 7,000만 달러로 평가되었고, 2026년에는 285억 7,000만 달러로 추정되고, 2031년까지 402억 9,000만 달러에 이를 것으로 예측됩니다. 2026-2031년 CAGR 7.12%로 성장할 전망입니다.

본 보고서는 제품 유형별(스테이플 섬유 및 필라멘트 섬유), 용도별(섬유, 병, 필름, 자동차, 전자, 기타), 최종 사용자별(의류, 가정용 직물, 산업용, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 폴리에틸렌 테레프탈레이트(PET) 섬유 시장 동향 및 분석

PET 섬유의 비용 경쟁력 및 범용성

PET 용융 방사 공정은 물을 대량으로 소비하는 면의 탈면 및 빗질 공정을 생략할 수 있어, 면 시스템에 비해 설비 투자 비용을 약 40% 절감할 수 있습니다. 경쟁력 있는 공급 비용 덕분에, 가공업체는 인테리어 및 산업용 직물 분야에서 면 및 폴리에스터 혼방 제품보다 저렴한 가격에 스테이플 섬유를 판매할 수 있습니다. 또한, 화학적 안정성과 자외선 저항성 덕분에 지오텍스타일 및 여과재로 사용되는 분야가 확대되고 있습니다. 이소프탈산이나 디에틸렌글리콜을 첨가한 공중합체를 조절함으로써, 새로운 설비를 도입하지 않고도 유리전이온도나 염색 친화성을 변화시킬 수 있어, 다양한 시장을 겨냥한 신속한 등급 변경이 가능해집니다. 동일한 압출기로 스테이플과 필라멘트를 모두 생산할 수 있기 때문에 공장은 더 높은 수익률을 기대할 수 있는 등급에 맞추어 생산 능력을 유연하게 조정할 수 있어, PET의 비용 경쟁력을 한층 더 공고히 하고 있습니다.

기능성 섬유 및 액티브웨어에 대한 수요 증가

현재 각 브랜드는 엘라스탄과 혼방하여 부드러운 촉감과 4방향 신축성을 구현하는 마이크로 데니어 필라멘트(1가닥당 1.0-1.5 데니어(dpf))를 필수로 사용하고 있습니다. COOLMAX 유형의 원사에서 볼 수 있는 중공 또는 홈 모양의 단면은 무게를 늘리지 않으면서도 흡습 발산성을 제공하여, 아웃도어 및 군사 분야에서 높은 평가를 받고 있습니다. 기계적 재생 섬유인 REPREVE 원사는 이미 유니피(Unifi)사의 2025년 매출의 31%를 차지하고 있으며, 2030년까지 50% 이상을 목표로 하고 있습니다. 2028년에 발효될 EU의 에코디자인 규정은 추적 가능한 재생 소재의 사용을 의무화함으로써 추가적인 수요를 창출하고, 방적 업체들이 재생 PET(rPET)공급을 확보하도록 압박하게 될 것입니다.

원유 연동형 원자재 가격의 변동

정제 테레프탈산(PTA)과 모노에틸렌글리콜(MEG)은 원유 가격에 뒤이어 움직이기 때문에 2025년 초 브렌트유 가격의 상승으로 인해 중국의 필라멘트 마진은 수년 만에 최저 수준으로 떨어졌습니다. 아시아의 신규 생산 능력이 수요를 초과함에 따라, 2025년 중반에는 PTA-파라자일렌 스프레드가 톤당 80달러까지 급락했고, 이로 인해 고비용 방적 업체들은 생산 중단을 피할 수 없게 되었습니다. 선물 헤지는 효과적이지만, 브렌트유와 PTA의 베이시스(가격 차이)가 톤당 30달러나 변동하기 때문에 완전한 헤지는 어렵고, 기업들은 더 깊은 수직 통합을 추진할 수밖에 없는 상황입니다.

부문별 분석

2025년, 단섬유는 시장 점유율의 57.84%를 차지했으며, 압도적인 입지를 확립했습니다. 한편, 필라멘트 섬유는 에어백, 안전벨트, 타이어 코드 등의 용도로 인해 2026-2031년 연평균 성장률(CAGR) 7.62%로 성장할 것으로 전망됩니다. 이러한 용도들은 모두 100만 분의 1(ppm) 미만의 고장 허용도를 요구하는 것입니다. 2025년, 중국은 연간 183만 톤(Mt/y)의 추가 생산 능력을 갖춘 부분 연신사(POY)를 도입하여, 주로 실내 장식용 및 산업용 직물용 드로우 텍스처드 원사에 활용했습니다. 이와 동시에, Filatex India는 2026년을 목표로 부분연사(POY), 완전연사(FDY), 드로우 텍스처드사(DTY) 각 라인에서 연간 62킬로톤의 생산 계획을 수립하고 준비를 진행하고 있습니다. 필라멘트 섬유는 스테이플 섬유에 비해 가공 비용이 저렴하고, 재단 폐기물을 최소화할 수 있어 수익성 향상에 기여합니다. 하류 부문에서는 연속 장섬유 직물 제조업체가 OEM(원청 브랜드 제조) 인증을 획득하여, 3년에서 5년의 계약 기간 동안 경쟁사를 사실상 배제함으로써 성장 궤도를 공고히 하고 있습니다.

의류용 혼방 및 홈퍼니싱 분야에서는 특정 컷에 맞추어 미세 조정된 링 및 로터 시스템 덕분에 스테이플 섬유가 여전히 주류로 자리 잡고 있지만, 그 성장률은 필라멘트 섬유에 뒤처지고 있습니다. 이는 레저 의류 분야에서 면 소재가 다시 주목받고 있는 상황에서 특히 두드러집니다. 양이온성 염색 가능 섬유, 난연성 섬유, 중공 섬유 등의 특수 스테이플 섬유는 더 높은 부가가치를 창출할 뿐만 아니라, 유럽과 미국에서 제한된 신규 생산 능력의 기반이 되고 있습니다. 2028년 이후, EU의 '디지털 제품 여권' 규정에 따라, 특히 다중 혼방 스테이플 원사와 비교하여 필라멘트 섬유의 추적 가능성이 강화될 것입니다. 이러한 추세는 연속 방적 설비에 대한 투자를 더욱 촉진할 것으로 예측됩니다.

지역별 분석

아시아태평양은 2025년 매출의 62.58%를 차지했으며, 2026-2031년 연평균 성장률(CAGR) 7.94%로 성장할 전망입니다. 전 세계 필라멘트 생산 능력의 대부분을 차지하는 중국이 주요 주자로 군림하고 있습니다. 주목할 만한 움직임으로, 통쿤(Tongkun)은 친환경 차별화 섬유의 생산 확대를 위해 막대한 투자를 진행하고 있습니다. 한편, 인도에서는 릴라이언스(Reliance)의 폴리에스터 섬유 라인 가동 개시와 필라텍스(Filatex)의 부분연신사(POY) 생산 확대 계획이 진행 중이며, 두 프로젝트 모두 2026년에 가동을 시작할 것으로 예측됩니다. 2029년을 내다보면, 브루나이의 2단계 프로젝트에서는 저비용 가스 원료라는 강점을 살려, 정제 테레프탈산(PTA) 및 폴리에틸렌 테레프탈레이트(PET)의 생산 확대를 목표로 하고 있습니다.

에너지 가격 급등과 규제 비용이라는 어려움에 직면해 있음에도 불구하고, 유럽과 북미는 틈새 투자를 계속해서 유치하고 있습니다. 2025년 초, 알펙은 생산 능력을 강화하기 위해 영국의 PET 시설을 재가동했습니다. 미국 걸프 연안 지역에서는 '인플레이션 억제법'에 따른 세액 공제가 생산 능력에 미미하지만 긍정적인 영향을 미치고 있습니다. 유럽의 제조업체들은 사업 방침을 전환하여, 현재는 재생 필라멘트 생산에 주력하는 한편, 버진 등급 제품의 생산은 태국에 외주하고 있습니다. 테이진(Teijin)은 전략적 확장의 일환으로 2025년에 태국 내 고강도 재생섬유 생산 능력을 증강했습니다. 남미, 중동 및 아프리카는 현재 비교적 작은 역할만을 수행하고 있지만, PET 지오텍스타일 및 컨베이어 벨트에 대한 수요가 매우 높은 사우디아라비아의 인프라 프로젝트와 브라질의 광업 활동으로부터 혜택을 볼 수 있는 기반이 마련되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the polyethylene terephthalate fiber market size is expected to increase from USD 26.67 billion in 2025 to USD 28.57 billion in 2026 and reach USD 40.29 billion by 2031, growing at a CAGR of 7.12% over 2026-2031.

This report is Segmented by Product Type (Staple Fiber and Filament Fiber), Application (Textiles, Bottles, Films, Automotive, Electronics, and Others), End-User (Apparel, Home Furnishing, Industrial, and Others), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Polyethylene Terephthalate (PET) Fiber Market Trends and Insights

Cost Advantage and Versatility of PET Fibers

PET's melt-spinning route circumvents water-intensive ginning and carding, lowering installed-capacity capex by roughly 40% versus cotton systems. Competitive delivered costs let converters price staple below cotton-polyester blends in furnishings and industrial cloth, while chemical inertness and UV stability widen use in geotextiles and filtration. Copolymer tweaks, adding isophthalic acid or diethylene glycol, shift glass-transition temperature and dye affinity without new hardware, enabling quick grade changes for diverse markets. Because the same extruders produce both staple and filament, plants flex capacity toward whichever grade commands better margins, further reinforcing PET's cost moat.

Rising Demand for Performance Textiles and Activewear

Brands now mandate micro-denier filaments (1.0-1.5 denier per filament [dpf]) that create a softer hand and four-way stretch when co-knit with elastane. Hollow or channeled cross-sections in COOLMAX-type yarns supply moisture management with no weight penalty, prized by outdoor and military programs. Mechanically recycled REPREVE yarn already represented 31% of Unifi's FY 2025 sales and targeted more than 50% by 2030. EU Ecodesign rules entering into force in 2028 add further pull by requiring traceable recycled content, compelling mills to lock in recycled PET (rPET) supply.

Crude-Linked Feedstock Price Volatility

Purified Terephthalic Acid (PTA) and Monoethylene Glycol (MEG) track with a lag, so Brent's early-2025 rally squeezed Chinese filament margins to multi-year lows. PTA-paraxylene spreads collapsed to USD 80 per ton mid-2025 as new Asian capacity outpaced demand, forcing high-cost spinners into turnarounds. Futures hedges help, yet Brent-PTA basis swings of USD 30 per ton undermine perfect cover, pressing firms toward deeper integration.

Other drivers and restraints analyzed in the detailed report include:

- Recycled-Content Mandates Boost Fiber Uptake

- Expansion of Technical and Industrial Applications

- Competition from Cotton and Bio-based Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, staple fiber held a commanding 57.84% share of the market. Meanwhile, filament fiber is projected to grow at a 7.62% compound annual growth rate (CAGR) from 2026 to 2031, driven by its applications in airbags, seatbelts, and tire cords, all of which demand a failure tolerance of less than 1 part per million (ppm). In 2025, China introduced an additional 1.83 million tons per year (Mt/y) of partially oriented yarn (POY), primarily channeling it into draw-textured yarns for upholstery and technical fabrics. Concurrently, Filatex India is gearing up for 2026 with plans for 62 kilotons per year across its partially oriented yarn (POY), fully drawn yarn (FDY), and draw-textured yarn (DTY) lines. Filament fiber boasts lower conversion costs compared to staple fiber and minimizes cutting waste, enhancing its profit margins. On the downstream side, continuous-filament weavers are securing original equipment manufacturer (OEM) certifications, effectively sidelining competitors for contract durations of three to five years, bolstering their growth trajectory.

While staple fiber remains the go-to choice for apparel blends and home furnishings, thanks to ring and rotor systems fine-tuned for specific cuts, its growth rate is trailing behind that of filament fiber. This is particularly evident as cotton makes a comeback in leisurewear. Specialty staple varieties, including cationic-dyeable, flame-retardant, and hollow fibers, not only command a higher value but also underpin the limited new capacities emerging in the West. Beginning in 2028, the EU's Digital Product Passports mandate will enhance traceability for filament fibers, especially in contrast to multi-fiber staple yarns. Such a development is poised to channel more investments into continuous assets.

Geography Analysis

Asia-Pacific, accounting for 62.58% of 2025 revenue, is set to grow at a 7.94% CAGR from 2026 to 2031. China, with a significant share of the global filament capacity, stands as the dominant player. In a notable development, Tongkun is making a substantial investment to expand its production of green differentiated fiber. Meanwhile, India is advancing with Reliance's upcoming polyester-fiber line and Filatex's planned expansion of partially oriented yarn (POY), both expected to commence operations in 2026. Looking ahead to 2029, Brunei's Phase II aims to enhance its production of purified terephthalic acid (PTA) and polyethylene terephthalate (PET), leveraging its advantage of low-cost gas feedstock.

Despite facing high energy prices and regulatory costs, Europe and North America continue to attract niche investments. In early 2025, Alpek restarted a PET facility in the UK to enhance production capacity. On the Gulf Coast, credits from the Inflation Reduction Act are providing a modest boost to capacity. European mills are pivoting, now focusing on recycled filament and outsourcing virgin grades to Thailand. In a strategic expansion, Teijin increased its high-tenacity recycled capacity in Thailand in 2025. While South America and the Middle-East and Africa play minor roles currently, they are poised to benefit from Saudi infrastructure projects and Brazilian mining activities, both of which have a significant demand for PET geotextiles and conveyor belts.

- Alpek S.A.B. de C.V.

- Barnet

- China Petroleum & Chemical Corporation.

- DAK Americas LLC

- Far Eastern New Century Corporation

- HYOSUNG

- Indorama Ventures Public Company Limited

- Kolon Industries, Inc.

- Lotte Chemical Corporation

- NAN YA PLASTICS CORPORATION

- Reliance Industries Limited

- SHINKONG SYNTHETIC FIBERS CORP.

- TEIJIN LIMITED.

- Tongkun Group Co., Ltd.

- Toray Advanced Composites (Toray Industries, Inc.)

- UNIFI, Inc.,

- Wellman International

- Zhejiang Hengyi Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost Advantage and Versatility of PET Fibers

- 4.2.2 Rising Demand for Performance Textiles and Activewear

- 4.2.3 Recycled-Content Mandates Boost Fiber Uptake

- 4.2.4 Expansion of Technical and Industrial Applications

- 4.2.5 AI-Enabled Spinning Control Enhancing Yield and Quality

- 4.3 Market Restraints

- 4.3.1 Crude-Linked Feedstock Price Volatility

- 4.3.2 Competition from Cotton and Bio-based Alternatives

- 4.3.3 rPET Bottle-to-Bottle Demand Squeezing Fiber Feedstock

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of Substitution

- 4.5.4 Threat of New Entrants

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Staple Fiber

- 5.1.2 Filament Fiber

- 5.2 By Application

- 5.2.1 Textiles

- 5.2.2 Bottles

- 5.2.3 Films

- 5.2.4 Automotive

- 5.2.5 Electronics

- 5.2.6 Others

- 5.3 By End-User

- 5.3.1 Apparel

- 5.3.2 Home Furnishing

- 5.3.3 Industrial

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Alpek S.A.B. de C.V.

- 6.4.2 Barnet

- 6.4.3 China Petroleum & Chemical Corporation.

- 6.4.4 DAK Americas LLC

- 6.4.5 Far Eastern New Century Corporation

- 6.4.6 HYOSUNG

- 6.4.7 Indorama Ventures Public Company Limited

- 6.4.8 Kolon Industries, Inc.

- 6.4.9 Lotte Chemical Corporation

- 6.4.10 NAN YA PLASTICS CORPORATION

- 6.4.11 Reliance Industries Limited

- 6.4.12 SHINKONG SYNTHETIC FIBERS CORP.

- 6.4.13 TEIJIN LIMITED.

- 6.4.14 Tongkun Group Co., Ltd.

- 6.4.15 Toray Advanced Composites (Toray Industries, Inc.)

- 6.4.16 UNIFI, Inc.,

- 6.4.17 Wellman International

- 6.4.18 Zhejiang Hengyi Group Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment