|

시장보고서

상품코드

2063443

헬스케어 웨어러블 로봇 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Healthcare Wearable Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

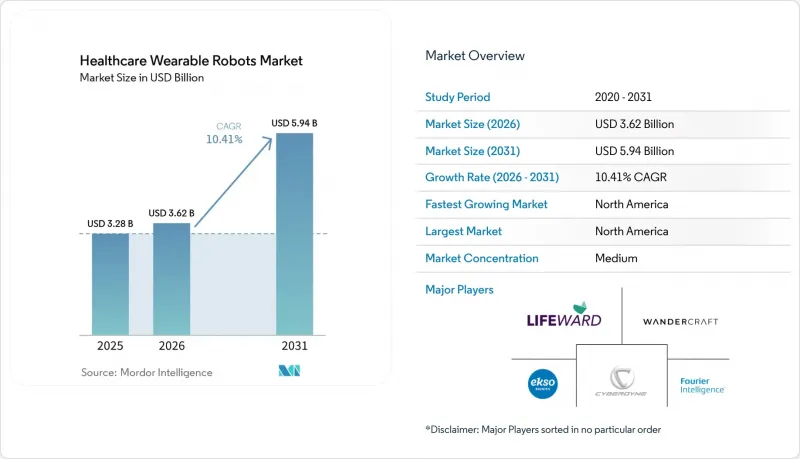

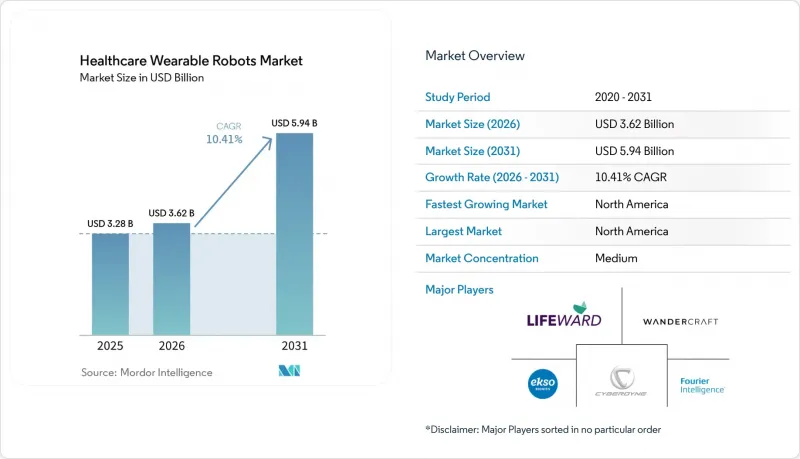

Mordor Intelligence에 의하면, 헬스케어 웨어러블 로봇 시장 규모는 2025년 32억 8,000만 달러, 2026년 36억 2,000만 달러에서 2031년까지 59억 4,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.41%를 나타낼 것으로 예측됩니다.

본 보고서는 신체 부위(하지 등), 프레임 유형(경성 외골격, 연성 외골격), 임상 용도(뇌졸중, 척수 손상 등), 최종 사용자(병원 등), 구동 방식(전기 모터 등) 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 헬스케어 웨어러블 로봇 시장 동향과 인사이트

노화에 따른 신경근골격계 장애의 유병률

세계보건기구(WHO)의 기록에 따르면, 2024년에는 17억 1,000만 명이 신경근골격계 질환을 앓으며 생활하고 있으며, 이는 2019년 대비 12% 증가한 수치입니다. 일본에서는 노인 요양 시설에 대한 외골격 장치 비용 지원이 이루어지고 있으며, 2024년 12월까지 400대의 CYBERDYNE HAL이 도입되었습니다. 독일도 2024년에 이에 발맞추어 법정 보험을 통한 로봇 보행 치료 적용이 시작되면서, Ottobock C-Brace의 수주가 전년 대비 크게 증가했습니다. 유병률은 75세 이후 비선형적으로 증가하며, 일본, 이탈리아, 독일 등 초고령 사회에서 수요가 집중되고 있습니다. 미국 요양 시설의 연간 비용은 8만-12만 달러이므로, 10만 달러짜리 외골격 장치는 1.2년 만에 투자 비용을 회수할 수 있는 셈이며, 설령 장치 가격이 하락하더라도 장기적인 수요는 확보될 것입니다.

규제 당국의 승인 및 임상 적응증 확대

FDA는 2024년 5월부터 2025년 10월까지 CYBERDYNE사의 HAL 소형 모델, ReWalk 7, 그리고 Wandercraft사의 Atalante X에 대해 510(k) 승인을 부여했습니다. 이는 해당 기관이 외골격의 안전성 프로파일에 대해 점점 더 큰 신뢰를 가지고 있음을 보여줍니다. 2024년 5월 CYBERDYNE의 승인 과정에서 소아 및 희귀질환에 대한 적응증이 추가되어, 치료 대상이 되는 환자층이 확대되었습니다. 강화된 EU MDR 규정 이후에도, 충분한 임상 데이터가 있다면 여전히 약 18개월 만에 유럽에서 CE 마크 승인을 받을 수 있음이 입증되었습니다. 중국은 2024년에 승인까지 소요되는 기간을 18개월로 단축함으로써, 유럽과 미국의 기존 기업들이 등록을 확보하기 전에 현지 공급업체들이 아시아 전역에서 시장 점유율을 확보할 수 있게 되었습니다. 승인이 잇따를 때마다 시판 후 데이터가 축적되고, 이후 신청 시 심사 주기가 단축되므로 선순환이 강화됩니다.

기기, 서비스, 교육에 드는 높은 비용

외골격 장치의 가격은 7만-15만 달러에 달하며, 연간 서비스 계약비로 8,000-1만 2,000달러가 추가되므로, 5년간의 총 소유 비용은 최대 18만 달러에 이릅니다. 2024년 APTA 조사에 따르면, 미국 재활 병원의 대다수가 높은 비용을 가장 큰 장벽으로 꼽았으며, 41%는 40시간의 치료사 연수 요건을 꼽았습니다. 리스 계약은 설비 투자 부담을 줄여줍니다. CYBERDYNE가 2024년에 미쓰비시 UFJ 리스와 체결한 계약에 따르면, HAL의월이용료는 15만 엔(1,000달러)으로 책정되어 있으며, 이 모델은 현재 ReWalk와 Wandercraft에도 채택되어 있습니다. 인도에서는 현지에서 조립된 기기가 3만-5만 달러에 판매되고 있지만, 대상 환자의 대다수에게 있어 본인 부담금이 평균 가구 소득을 초과하기 때문에 보급이 더딘 실정입니다. 미국에서는 메디케어의 80% 급여 덕분에 경제적 장벽의 대부분이 해소되었지만, 2024년 현재 유럽의 민간 보험사 중 외골격 치료 비용을 보상하는 곳은 고작 30%에 불과하여 투자 회수 기간이 길어지고 있습니다.

부문별 분석

2025년 기준으로, 하체용 시스템이 헬스케어 웨어러블 로봇 시장 점유율의 58.9%를 차지하고 있으며, 이는 척수 손상 재활 분야에서 해당 시스템이 널리 보급된 데 기인합니다. 상지용 웨어러블 헬스케어 로봇 시장 규모는 2031년까지 연평균 성장률(CAGR) 10.96%로 확대될 것으로 전망됩니다. 이는 로봇 팔 치료를 통해 8주 만에 푸글-마이어 점수가 12점 향상된다는 증거가 점점 더 많아지고 있기 때문입니다. 체간 및 전신용 모델은 고령자의 자세 안정성이라는 또 다른 요구를 충족시키고 있으며, 혼다는 2024년에 일본의 요양 시설에 보행 보조 기기 50대를 도입했습니다.

하지 치료가 지역사회에서의 보행에 이르기까지 획기적인 성과를 가져오는 한편, 상지 플랫폼은 미세 운동 기능 회복에 주력함으로써 지속적인 부가가치를 제공하며, 환자 1인당 수익 창출 기간을 연장하고 있습니다. CYBERDYNE사의 소형 HAL이 승인을 받으면서 소아 적응증이 확대됨에 따라, 특히 뇌성마비 환자를 대상으로 한 시장 규모가 커지고 있습니다. 현재 병원에서는 진단 내용에 맞추어 기기의 형태를 조정할 수 있도록 다양한 제품 포트폴리오를 도입하고 있으며, 모듈식 아키텍처를 확립한 공급업체는 핵심 전자 기기를 재설계하지 않고도 여러 신체 부위에 대응할 수 있게 되었습니다.

강성 아키텍처는 40 Nm의 무릎 토크를 통해 운동 기능을 완전히 상실한 사용자도 지원할 수 있기 때문에 2025년 매출의 58.96%를 차지하고 있습니다. 그러나 소프트형 외골격 로봇의 헬스케어 웨어러블 로봇 시장 규모는 공압식 근육과 보덴 케이블을 통해 프레임 무게가 대폭 줄어들고 8시간 동안 착용할 수 있게 됨에 따라 연평균 성장률(CAGR) 11.13%로 성장을 지속하고, 있습니다.

기능적인 측면에서 경질 프레임은 여전히 입원 환자를 대상으로 한 척수 손상(SCI) 치료의 표준으로 여겨지지만, 재택 간호 분야에서는 착용 편의성과 빠른 착용 속도가 순수한 힘보다 더 중요하게 여겨지기 때문에 소프트 엑소슈트가 주류를 이루고 있습니다. 오토복(Ottobock)사의 하이브리드형 ‘Paexo’는 두 부문이 융합되어 가고 있음을 입증하고 있습니다. 이 25 Nm의 출력은 양측 간의 격차를 좁혔으며, 2024년에는 유럽의 재활센터로부터의 수주가 28% 증가했습니다. ISO 13482 인증은 마케팅상의 필수 요건으로 자리 잡고 있으며, 이 관문을 조기에 통과한 소프트 엑소슈트 제조업체들은 가속화되는 D2C(소비자 직접 판매) 채널을 주도하게 될 것입니다.

지역별 분석

북미는 2025년 매출의 41.6%를 차지하며, 연평균 성장률(CAGR) 10.81%로 성장하고 있습니다. 이는 CMS(미국 의료보험서비스센터)의 일괄 지급 제도에 따라 메디케어 수급자의 본인 부담금이 10만 달러에서 약 2만 달러로 대폭 감소했기 때문입니다. 재향군인부 프로그램은 2024년에 재택 치료용으로 500대를 도입했으며, 로봇 보행 지원 서비스를 제공하는 미국의 병원은 2022년 200곳에서 340곳으로 증가했습니다. 캐나다와 멕시코는 2024년부터 2025년까지 주 및 연방 차원의 시범 사업을 시작했으며, 이는 북미 전역에서 보상 제도로의 전환을 향한 기세가 고조되고 있음을 보여줍니다.

유럽은 2025년 매출에서 큰 비중을 차지하고 있으며, 결제 기관의 정책이 제각각임에도 불구하고 상당한 연평균 성장률(CAGR)을 기록하며 성장하고 있습니다. 독일에서 2024년에 로봇 보행 치료법이 승인됨에 따라 오토복사의 수주가 크게 증가했습니다. 한편, 사이버다인사와 리워크사는 더욱 엄격해진 EU 의료기기 규정(MDR)을 준수하여 CE 마크 획득에 성공했습니다. 영국의 원격 재활 시범 사업에서는 높은 완료율을 달성했으나, 프랑스의 보험 급여 제도가 미비하고 남유럽 국가들의 자금 조달이 분산되어 있어 시장에 널리 보급되는 데 걸림돌이 되고 있습니다.

아시아태평양은 예측 기간 동안 상당한 성장을 기록할 것으로 전망됩니다. 일본의 초고령화 사회와 보조금 제도 덕분에 2024년 말까지 400대의 HAL이 도입되었습니다. 중국은 승인 기간을 절반으로 단축하고 20억 달러 규모의 기금을 통해 국내 생산을 지원한 덕분에, Angel Robotics와 Fourier Intelligence는 유럽 및 미국 가격보다 훨씬 낮은 가격을 책정할 수 있게 되었습니다. 호주의 NDIS(국가장애인보험제도)와 한국의 뇌졸중 시범 사업을 통해 오세아니아 지역에서의 접근성은 확대되고 있지만, 인도에서는 국가보험제도가 구체화될 때까지 가격 측면의 제약이 계속되고 있습니다.

중동 및 아프리카 및 남미는 2025년 소비에서 차지하는 비중은 미미했으나, 눈부신 성장을 기록했습니다. UAE와 남아프리카공화국에서는 제한적인 시범 사업이 시작되었지만, 공공 예산은 여전히 1차 의료에 중점을 두고 있어 보급 확대는 민간 보험사의 참여나 자선 단체의 지원금에 달려 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the healthcare wearable robots market size is projected to expand from USD 3.28 billion in 2025 and USD 3.62 billion in 2026 to USD 5.94 billion by 2031, registering a CAGR of 10.41% between 2026 to 2031.

This report is Segmented by Body Region (Lower-Limb, and More), Frame Type (Rigid Exoskeletons, Soft Exosuits), Clinical Application (Stroke, Spinal Cord Injury, and More), End User (Hospitals, and More), Actuation Type (Electric Motor, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare Wearable Robots Market Trends and Insights

Aging-Related Neuro-Musculoskeletal Impairment Prevalence

The World Health Organization recorded 1.71 billion people living with neuro-musculoskeletal disorders in 2024, a 12% rise since 2019. Japan subsidizes exoskeleton costs for elder-care facilities, spurring 400 CYBERDYNE HAL deployments by December 2024 . Germany followed suit in 2024 when statutory insurance began covering robotic gait therapy, driving Ottobock C-Brace orders up significantly year over year. Prevalence climbs non-linearly after age 75, concentrating demand in super-aged societies such as Japan, Italy, and Germany. Because U.S. skilled-nursing care costs USD 80,000-120,000 annually, a USD 100,000 exoskeleton has a 1.2-year payback, locking in long-run demand even if device prices soften.

Expanding Regulatory Clearances and Clinical Indications

The FDA granted 510(k) clearances to CYBERDYNE's HAL small model, ReWalk 7, and Wandercraft's Atalante X between May 2024 and October 2025, showing the agency's growing comfort with exoskeleton safety profiles. CYBERDYNE's May 2024 clearance added pediatric and rare-disease indications, expanding the treatable addressable population. CE-mark approvals after the tougher EU MDR rules prove that robust clinical files can still move through Europe in roughly 18 months . China sliced its approval timeline to 18 months in 2024, allowing local vendors to win share across Asia before Western incumbents secure registration. Each successive approval supplies post-market data that shortens review cycles for follow-on submissions, reinforcing the positive loop.

High Device, Service, and Training Costs

Exoskeleton price tags span USD 70,000-150,000, while annual service contracts add USD 8,000-12,000, pushing the five-year total cost of ownership to as much as USD 180,000. The majority of U.S. rehab hospitals flagged sticker shock as the top hurdle in a 2024 APTA poll, and 41% cited 40-hour therapist training requirements. Leasing eases capex pressure; CYBERDYNE's 2024 pact with Mitsubishi UFJ Lease prices HAL access at JPY 150,000 (USD 1,000) per month, a model now mirrored by ReWalk and Wandercraft. In India, locally assembled devices sell for USD 30,000-50,000, yet adoption lags because out-of-pocket costs exceed average household income for the majority of candidates. Medicare's 80% coverage erases most financial friction in the United States, but only 30% of European private insurers reimbursed exoskeleton therapy as of 2024, prolonging payback horizons.

Other drivers and restraints analyzed in the detailed report include:

- Strengthening Clinical Evidence for Functional Recovery & ADL Gains

- Emerging Reimbursement Pathways and Coverage Pilots

- Safety, Supervision, and Liability Constraints in Real-World Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lower-limb systems accounted for 58.9% of the healthcare wearable robots market share in 2025, owing to their entrenched use in spinal cord injury rehabilitation. The healthcare wearable robots market size for upper-limb devices is projected to expand at a 10.96% CAGR through 2031, as evidence mounts that robotic arm therapy increases Fugl-Meyer scores by 12 points in eight weeks. Trunk and full-body variants meet a separate need for postural stability for elderly users, and Honda placed 50 Walking Assist devices in Japanese care homes in 2024.

While lower-limb therapy delivers milestone gains up to community ambulation, upper-limb platforms continue adding value by tackling fine-motor recovery, extending the revenue window per patient. Pediatric indications opened by CYBERDYNE's small HAL clearances enlarge the addressable base, especially for cerebral palsy. Hospitals now procure mixed portfolios to align device geometry with diagnosis, and vendors that master modular architectures can address multiple body regions without redesigning core electronics.

Rigid architectures held 58.96% of 2025 revenue because their 40 Nm knee torque accommodates users with complete motor loss. However, the healthcare wearable robots market size for soft exosuits is tracking an 11.13% CAGR as pneumatic muscles and Bowden cables slash frame weight significantly and enable 8-hour wear periods.

Functionally, rigid frames remain the gold standard for inpatient SCI therapy, yet soft exosuits dominate home-care adoption where comfort and fast donning beat raw power. Ottobock's hybrid Paexo proves the segments will blend: its 25 Nm output bridges the gap and drew 28% higher 2024 orders from European rehab centers. ISO 13482 certification is becoming a marketing prerequisite, and soft-exuit makers that clear the bar early will ride accelerated direct-to-consumer channels.

Geography Analysis

North America generated 41.6% of 2025 sales and is advancing at a 10.81% CAGR because CMS's lump-sum payment slashed out-of-pocket costs from USD 100,000 to roughly USD 20,000 for Medicare beneficiaries. The Veterans Affairs program placed 500 units for home therapy in 2024, and 340 U.S. hospitals now offer robotic gait services, up from 200 in 2022. Canada and Mexico launched provincial and federal pilots in 2024-2025, signaling continent-wide momentum for reimbursement.

Europe held a significant share of 2025 revenue and is rising at a notable CAGR despite heterogeneous payer policies. Germany's 2024 green light for robotic gait therapy lifted Ottobock orders significantly, while CYBERDYNE and ReWalk both navigated the stricter EU MDR to secure CE marks. U.K. tele-rehab pilots achieved better completion rates, but the lack of French reimbursement and fragmented Southern European funding are restraining broader penetration.

Asia-Pacific is expected to register significant growth over the forecasted period. Japan's super-aged demographics and subsidy scheme drove 400 HAL installs by late 2024. China cut approval times in half and backed local manufacturing with a USD 2 billion fund, allowing Angel Robotics and Fourier Intelligence to notably undercut Western pricing. Australia's NDIS and South Korea's stroke pilots widen Oceania access, while India remains price-constrained until a national payer plan materializes.

The Middle East & Africa and South America accounted for a modest share of 2025 consumption and posted notable growth. The UAE and South Africa launched limited pilots, but widespread uptake hinges on private insurance participation and philanthropic grants, as public budgets remain focused on primary care.

- Able Human Motion S.L.

- Angel Robotics Co., Ltd.

- Biomotum, Inc.

- B-Temia

- Cyberdyne

- Daiya Industry Co., Ltd.

- Ekso Bionics Holdings, Inc.

- ExoAtlet Global SA

- Exosystems Inc.

- Fourier Intelligence Co., Ltd.

- Gogoa Mobility Robots S.L.

- Hangzhou RoboCT Technology Development Co., Ltd

- Honda Motor Co., Ltd.

- Lifeward Ltd

- Marsi Bionics S.L.

- Myomo, Inc.

- MyoSwiss AG

- Ottobock

- Roam Robotics, Inc.

- Technaid S.L.

- Wandercraft SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging-Related Neuro-Musculoskeletal Impairment Prevalence

- 4.2.2 Expanding Regulatory Clearances and Clinical Indications

- 4.2.3 Strengthening Clinical Evidence for Functional Recovery & ADL Gains

- 4.2.4 Emerging Reimbursement Pathways and Coverage Pilots

- 4.2.5 Miniaturized Soft Exosuits Enabling Home Use and Continuous Therapy

- 4.2.6 Tele-Rehab Integration and Outcomes-Linked Contracting

- 4.3 Market Restraints

- 4.3.1 High Device, Service, and Training Costs

- 4.3.2 Safety, Supervision, and Liability Constraints in Real-World Use

- 4.3.3 Lack of Standardized Outcomes Hindering Broad Reimbursement

- 4.3.4 Precision Component Supply Constraints

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Body Region

- 5.1.1 Lower-limb

- 5.1.2 Upper-limb

- 5.1.3 Trunk/Full-body

- 5.2 By Frame Type

- 5.2.1 Rigid exoskeletons

- 5.2.2 Soft exosuits

- 5.3 By Clinical Application

- 5.3.1 Stroke

- 5.3.2 Spinal cord injury

- 5.3.3 Multiple sclerosis

- 5.3.4 Cerebral palsy & pediatrics

- 5.3.5 Orthopedic & post-surgical rehab

- 5.3.6 Elderly mobility assistance

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Rehabilitation centers

- 5.4.3 Homecare

- 5.5 By Actuation Type

- 5.5.1 Electric motor

- 5.5.2 Pneumatic

- 5.5.3 Hybrid/cable-driven

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Able Human Motion S.L.

- 6.3.2 Angel Robotics Co., Ltd.

- 6.3.3 Biomotum, Inc.

- 6.3.4 B-Temia Inc.

- 6.3.5 Cyberdyne Inc.

- 6.3.6 Daiya Industry Co., Ltd.

- 6.3.7 Ekso Bionics Holdings, Inc.

- 6.3.8 ExoAtlet Global SA

- 6.3.9 Exosystems Inc.

- 6.3.10 Fourier Intelligence Co., Ltd.

- 6.3.11 Gogoa Mobility Robots S.L.

- 6.3.12 Hangzhou RoboCT Technology Development Co., Ltd

- 6.3.13 Honda Motor Co., Ltd.

- 6.3.14 Lifeward Ltd

- 6.3.15 Marsi Bionics S.L.

- 6.3.16 Myomo, Inc.

- 6.3.17 MyoSwiss AG

- 6.3.18 Ottobock SE & Co. KGaA

- 6.3.19 Roam Robotics, Inc.

- 6.3.20 Technaid S.L.

- 6.3.21 Wandercraft SAS

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment