|

시장보고서

상품코드

2063579

로봇 개 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Robot Dog - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

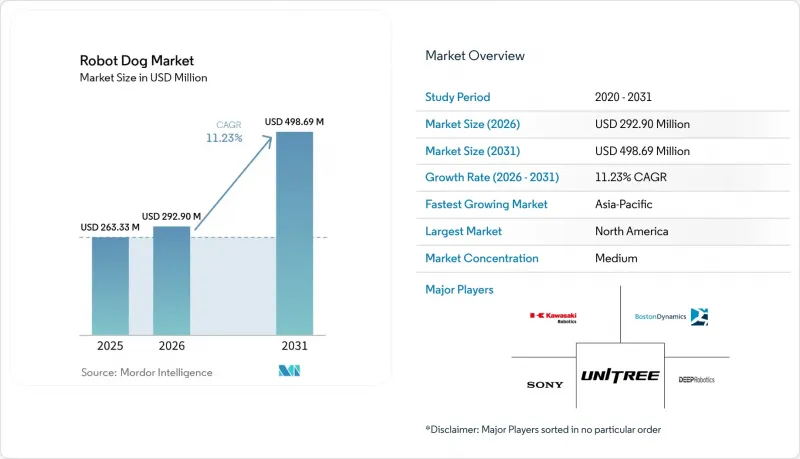

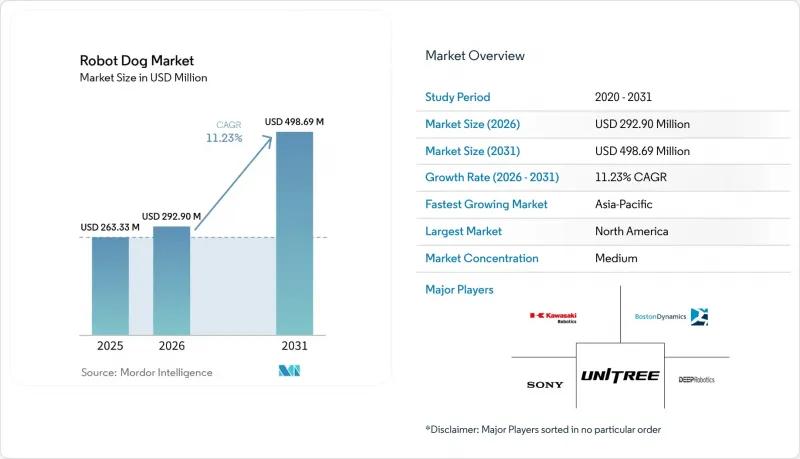

Mordor Intelligence에 의하면, 로봇 개 시장 규모는 2025년 2억 6,333만 달러, 2026년 2억 9,290만 달러에서 2031년까지 4억 9,869만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 11.23%를 나타낼 것으로 예측됩니다.

본 보고서는 의료 용도(시설 검사 및 규정 준수 모니터링 등), 의료 환경(3차 및 4차 병원 및 IDN 등), 자율 수준(원격 조작 및 텔레오퍼레이션, 반자율형, 완전 자율형), 그리고 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 로봇 개 시장 동향과 인사이트

의료 인력 부족과 인건비 급등이 비임상 업무의 자동화를 촉진하고 있습니다.

병원에서는 임상 업무와 비임상 업무의 역할 분담을 재검토하는 움직임이 계속되고 있으며, 검체 운반, 물자 배송, 일상적인 순찰을 수행하는 이동 플랫폼에 대한 수요가 증가하고 있습니다. 로봇 개 시장은 이러한 업무상의 변화에 적합합니다. 왜냐하면, 4족 보행 로봇은 바퀴가 달린 카트로는 이동이 제한되는 계단이나 요철이 있는 노면도 이동할 수 있기 때문에 그 활동 범위는 지하실, 경사로, 실외 연결 통로까지 미치기 때문입니다. 의료기관은 반복적인 물류 및 점검 업무에 있어 24시간 365일 가동을 보장하는 기종을 표준화하고 있으며, 이를 통해 간호사와 기술자는 직접적인 환자 돌봄에 할애할 시간을 확보할 수 있게 됩니다. 로봇 군이 작업 관리 시스템 및 전자 로그와 통합되면, 규정 준수 팀을 위한 감사 가능한 기록이 생성되고 인적 자원 절감 효과를 측정할 수 있으므로 가치 실현이 향상됩니다. 또한, 구독형 및 관리형 서비스 모델은 초기 비용을 절감하고 예산 편성을 원활하게 함으로써, 대규모 자본 투자 프로그램이 없는 지역 의료 현장에서의 도입을 가속화할 것입니다. 고성능 4족 보행 로봇이나 검증된 적재량에 대한 공개 가격표 등, 주요 플랫폼의 가격 투명성은 수년에 걸친 사업 계획을 수립해야 하는 구매자에게 있어 평가의 장벽을 한층 더 낮춰줍니다.

격리 환경 및 중요 환경에서의 감염 관리와 직원 안전 확보의 필요성

의료시설에서는 엄격한 감염 예방 절차를 준수하며, 오염된 공간에 사람이 출입하는 것을 최소화하기 위해 노력하고 있습니다. UV-C, 열 센서, 공기질 센서를 탑재한 4족 보행 로봇은 위생 관리 업무를 지원하는 동시에, 격리 구역에 대한 직원의 출입을 제한할 수 있습니다. 병원 환경에서의 자율적 소독 및 UV-C 시스템 시험 결과, 미생물 수가 대폭 감소한 것으로 입증되었으며, 이는 처리 능력을 유지하면서 의료 관련 감염 위험을 줄이겠다는 목표와 부합합니다. 로봇 개 시장은 클린룸 기준이나 감사 요건이 적용되는 분야에서도 발전하고 있습니다. 검증된 오염 제거 워크플로우와 추적 가능한 유지보수 기록은 약국 및 검사실의 거버넌스 요건을 충족하는 데 도움이 됩니다. 플랫폼이 일관된 환경 모니터링을 지원하면, 안전 관리 담당자는 지속적인 가시성을 확보하여 수동 점검 사이의 사각지대를 줄일 수 있습니다. 진화하는 의료기기 품질 프레임워크 및 클린룸에 관한 지침을 통해 로봇이 충족해야 할 요건이 명확해졌으며, 이를 통해 공급업체와 병원 간에 문서화, 감사 가능성, 품질 시스템 통합에 관한 인식이 일치하고 있습니다.

높은 TCO, IT/OT 통합 및 병원 사이버 보안 승인

총 소유 비용(TCO)에는 하드웨어, 페이로드, 소프트웨어, 연결성 및 변경 관리가 포함되며, 이러한 요소들이 초기 도입을 지연시킬 수 있습니다. 구매자는 플랫폼 가격 외에도 센서, 매니퓰레이터 암, 안전 옵션, 도킹 기능을 평가한 후, 네트워크 업그레이드, 역할 기반 접근 제어, 감사 로그 기능을 추가하여 검토합니다. 검증이 완료된 페이로드를 탑재한 고성능 사족 보행 로봇은 가격이 비싸기 때문에 병원 측은 단일 시설에서의 투자 수익률(ROI)과, 서비스 및 예비 부품 풀을 통해 장기적으로 단위당 비용이 낮아지는 다중 시설로의 대규모 확장을 비교 검토합니다. 로봇이 환자 구역에서 영상을 촬영할 가능성이 있으므로 기밀 데이터를 보호해야 하며, 보안 및 개인정보 보호 심사로 인해 도입 일정이 지연될 것입니다. 이로 인해 벤더들은 암호화, 엣지 처리, 엄격한 접근 제어의 도입을 요구받고 있습니다. 영상을 시설 내에 저장하고 완벽한 감사 추적을 기록하는 이 플랫폼은 HIPAA 규정을 준수하며, 사고 조사 시 발생하는 위험을 줄여줍니다. 상호 운용성은 여전히 걸림돌로 남아 있으며, 로봇 군이 독자적인 스택과 ROS 기반 시스템을 혼용하고 있기 때문에 의료 기관은 엘리베이터 호출이나 출입문 접근 제어와 관련해 일관된 API와 워크플로우 이관을 제공하는 인증된 통합 업체에 의존하는 경우가 많습니다. 또한, 컴플라이언스 팀은 로봇이 약국이나 검사실 환경에서 가동될 경우, 의료기기의 품질 요건 및 클린룸 기준에 관한 명확한 문서를 요구하고 있으며, 병원의 거버넌스에 부합하는 지침을 공개한 공급업체가 유리합니다.

부문별 분석

2025년 도입 현황을 기준으로 볼 때, 시설 점검과 규정 준수 감시가 가장 큰 비중을 차지했습니다. 이는 병원이 예측 가능한 ROI와 지속적인 자산 가시성을 우선시했기 때문이며, 오케스트레이션 도구가 성숙해짐에 따라 이러한 핵심적인 역할은 앞으로도 지속될 것으로 예측됩니다. 이러한 상황에서 로봇 개 시장은 빈번한 순찰 시 재현성 있는 품질로 HVAC, 의료용 가스, 패널을 스캔하는 열화상, 음향 감지, LiDAR 등의 점검용 페이로드에 적합합니다. 병원에서는 이상 감지 및 자동 보고 기능을 활용하여 시설 관리 팀과 인증 심사 팀을 위한 감사 추적을 구축하고 있으며, 이를 통해 수동 순회만으로는 완료하기 어려운 장비 점검이 철저히 이루어지고 있습니다. 주목할 만한 검사 사례로, 4족 보행 로봇이 규제 대상 시설에서 누출을 확인하여 정제된 공기의 손실을 방지한 사례가 있으며, 이는 간헐적인 인력 순찰에 비해 지속적인 감시가 가져다주는 성능상의 우위를 보여줍니다. 보안 및 캠퍼스 순찰 분야는 현재 점유율이 낮지만, 서비스 제공업체들이 통합된 로봇 경비 워크플로를 활용해 경계선, 주차장, 로비를 강화함에 따라 빠르게 확대될 전망입니다. 로봇 개 시장은 VMS(영상 관리 시스템) 및 출입 통제에 정보를 제공하는 순찰 기능을 통해 이러한 프로그램을 지원하고 있으며, 훈련을 받은 조련사가 우선순위가 지정된 경보에 대응함으로써 상시 카메라 감시로 인한 피로를 덜어주고 있습니다.

시설 점검은 2025년 용도 구성의 42.19%를 차지하며, 멀티 페이로드 활용의 도입 기반을 뒷받침하고 있습니다. 반면, 보안 및 캠퍼스 순찰은 자율적인 순찰 범위가 야간 대응 능력과 사건 기록을 강화하기 때문에 2031년까지 연평균 성장률(CAGR) 12.89%를 기록하며 가장 빠르게 성장하는 분야입니다. 이 두 가지 이용 사례 모두에서 성장을 지속하기 위해, 각 벤더사는 보다 안전한 공동 운영과 사람을 고려한 내비게이션을 중시하고 있습니다. 이를 통해 교육 기간이 단축되고, 직원 및 방문객의 수용도가 높아집니다. 시설 점검용 로봇 개 시장 규모는 2025년 도입에서 큰 비중을 차지하고 있으며, 이는 가동 중단 시간 단축과 에너지 절약에 따른 지속적인 이익을 반영한 것입니다. 한편, 보안 분야에서의 도입은 병원 네트워크가 거점 간 조달을 통합하는 추세를 따르는 형태를 띠고 있습니다. 로봇, 영상 분석, On-Premise 데이터 처리를 통합하는 파트너십을 통해 병원의 개인정보 보호 요건을 충족하면서도 사건에 대한 즉각적인 검증이 가능해집니다. 이러한 기반이 안정화됨에 따라, 긴급 훈련 및 재해 평가 분야로의 확대 적용 시 동일한 자율 기능과 센싱 스택이 활용되어, 새로운 하드웨어 클래스를 도입하지 않고도 사족 보행 로봇의 유용성이 확대될 것입니다.

지역별 분석

2025년, 북미는 로봇 개 시장 점유율의 45.44%를 차지했습니다. 이는 초기 도입 기업들이 점검, 물류, 캠퍼스 보안 등 각 분야에서 도입을 확대했기 때문입니다. 이 지역의 병원들은 성숙한 품질 관리 체계와 명확한 문서화 프로세스의 혜택을 누리고 있으며, 이는 시스템 도입, 변경 관리 및 운영 중 감사를 지원하고 있습니다. 자사의 품질 관리 관행을 공인된 기준에 부합하도록 하는 공급업체는 병원이 심사 주기를 단축하고 갱신을 통해 규정 준수를 유지할 수 있도록 지원합니다. 학술의료센터, 통합의료네트워크, 제약 관련 시설은 사족 보행 로봇이 계단이나 다양한 지형을 이동할 수 있도록 하는 복잡한 인프라를 관리하고 있기 때문에 주요 구매처로 자리 잡고 있습니다. 병원 네트워크가 로봇을 접근 제어 및 영상 시스템과 통합하여 지속적인 모니터링과 신속한 사고 에스컬레이션을 실현함에 따라, 보안 활용 사례가 확대되고 있습니다. 또한, 의료 기관들은 경비팀을 보완하는 보안 로봇 계약을 늘리고 있으며, 이는 대규모 하이브리드 순찰 모델에 대한 신뢰를 보여주는 것입니다.

아시아태평양은 국내 제조업체와 대학 병원이 실증 시험을 진행하며 단가를 낮춤으로써, 2031년까지 연평균 성장률(CAGR) 13.42%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 공개된 보고서에 따르면, 2025년에 국내 4족 보행 로봇의 출하 대수가 증가하고 있으며, 이는 여러 도시에서 진행 중인 노인 돌봄 및 시설 업무 분야의 시범 프로그램을 뒷받침하고 있습니다. 일본의 대학병원에서는 2026년에 개념 검증(PoC)을 실시하여, 유동 인구가 많은 복도나 입구 구역에서의 자율 주행이 검증되었습니다. 이로 인해, 직원의 감독 하에 실제 환경에서 시스템을 운영하는 것에 대한 신뢰도가 높아지고 있습니다. 또한, 현지의 워크플로우와 언어 인터페이스에 맞추어 로봇을 맞춤 설정해 주는 통합 업체와 소프트웨어 파트너의 존재도 이러한 추세를 뒷받침하고 있습니다. 검사 로봇과 관련된 산업계의 협력은 규제가 엄격한 의료 인프라 분야로 지속적으로 확대되고 있으며, 이에 따라 안전성 입증 및 문서화 관행이 강화되고 있습니다. 이러한 사례가 축적됨에 따라, 해당 지역의 구매자들은 공용 공간의 관리, 청소 절차 및 사고 대응에 관한 보다 명확한 지침을 얻을 수 있게 될 것입니다.

유럽에서는 산업용 등급의 검사 기술에 대한 꾸준한 관심이 나타나고 있으며, 이는 병원 시설 및 제약 제조 현장으로 확대되고 있습니다. 이 지역의 로봇 개 시장은 검증된 검사 실적과 탄탄한 규정 준수 실적을 갖춘 공급업체의 혜택을 받고 있습니다. 에너지 및 인프라 분야의 로봇 OEM과 서비스 제공업체간의 제휴는 병원 환경에서도 요구되는 신뢰성, 안전성, 그리고 재현성 있는 문서화를 중시한다는 점에서 높은 관련성을 가지고 있다고 할 수 있습니다. 유럽의 병원에서는 엄격한 환자 권리 및 데이터 보호 규정이 적용되고 있기 때문에 엣지 측에서 영상을 처리하고 세밀한 접근 제어를 제공하는 플랫폼이 조달 요구 사항에 더 부합합니다. 성장은 EU의 의료기기 품질 시스템 하에서 신기술을 도입할 수 있는 거버넌스 역량을 갖춘 대학병원이나 대규모 의료 네트워크를 중심으로 이루어질 가능성이 높을 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the robot dog market size is projected to expand from USD 263.33 million in 2025 and USD 292.90 million in 2026 to USD 498.69 million by 2031, registering a CAGR of 11.23% between 2026 to 2031.

This report is Segmented by Healthcare Application (Facilities Inspection & Compliance Monitoring, and More), Care Setting (Tertiary/Quaternary Hospitals & IDNs, and More), Autonomy Level (Remote-controlled/Teleoperated, Semi-Autonomous, Fully Autonomous), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Robot Dog Market Trends and Insights

Healthcare Staffing Shortages and Rising Labor Costs Push Automation for Non Clinical Tasks

Hospitals continue to rebalance work across clinical and non clinical roles, which elevates demand for mobile platforms that move specimens, deliver supplies, and perform routine rounds. The robot dog market fits this operational shift because quadrupeds can traverse stairs and uneven surfaces that limit wheeled carts, so coverage extends to basements, ramps, and outdoor connectors. Providers are standardizing on units that deliver 24/7 uptime for repetitive logistics and inspection, so nurses and technicians reclaim time for direct care. Value realization improves when fleets integrate with tasking systems and electronic logs, since this creates auditable trails for compliance teams and measures diverted human hours. Subscription and managed service models also reduce upfront spending and smooth budgeting, which speeds adoption in community settings that lack large capital programs. Price transparency for core platforms, such as published list pricing for high end quadrupeds and validated payloads, further lowers evaluation friction for buyers that must build multi year business cases.

Infection Control and Staff Safety Needs in Isolation and Critical Environments

Healthcare facilities maintain stringent infection prevention routines and seek to reduce human exposure in contaminated spaces. Quadrupeds equipped with UV C, thermal sensors, and air quality payloads can support hygiene workflows while limiting staff entries into isolation areas. Trials with autonomous wiping and UV C systems in hospital environments have demonstrated strong microbial load reduction, which aligns with goals to reduce healthcare associated infection risk while maintaining throughput. The robot dog market is also advancing where cleanroom standards and audit requirements apply, since validated decontamination workflows and traceable maintenance logs help satisfy pharmacy and lab governance. When the platform supports consistent environmental monitoring, safety officers gain continuous visibility and fewer blind spots between manual checks. Evolving device quality frameworks and cleanroom guidance have clarified expectations that robots must meet, which aligns vendors and hospitals on documentation, auditability, and quality system integration.

High TCO, IT/OT Integration, and Hospital Cybersecurity Approvals

Total ownership costs encompass hardware, payloads, software, connectivity, and change management, which can delay first deployments. Buyers evaluate platform price along with sensors, manipulator arms, safety options, and docking, and then add network upgrades, role based access, and audit logging. High spec quadrupeds with validated payloads command premium pricing, so hospitals weigh single site ROI against multi site scale where service and spare pools lower unit economics over time. Security and privacy reviews extend timelines because robots can capture video in patient areas and must protect sensitive data, which pushes vendors to implement encryption, edge processing, and strict access control. Platforms that keep video on premises and record complete audit trails align better with HIPAA obligations and reduce risk in incident investigations. Interoperability remains a hurdle where fleets mix proprietary stacks and ROS based systems, so providers often lean on certified integrators that expose consistent APIs and workflow handoffs for elevator calls and door access. Compliance teams also look for clear documentation to medical device quality expectations and cleanroom norms when robots operate in pharmacy or lab environments, which favors vendors that publish guidance aligned to hospital governance.

Other drivers and restraints analyzed in the detailed report include:

- Hospital Campus Security and Emergency Readiness Require 24/7 Autonomous Patrols

- AI Navigation and Sensor Fusion Enable Reliable Indoor-Outdoor Hospital Operations

- Clinical Workflow Fit, Infection Control Cleaning, and Safety Validation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Facilities inspection and compliance monitoring held the largest share in 2025 deployment base as hospitals prioritized predictable ROI and continuous asset visibility, and this anchor role is expected to persist as orchestration tools mature. Within this context, the robot dog market has aligned to inspection payloads such as thermal imaging, acoustic sensing, and LiDAR that scan HVAC, medical gases, and panels with repeatable quality across frequent rounds. Hospitals use anomaly detection and automated reports to build audit trails for facilities and accreditation teams, which tighten equipment checks that are difficult to complete during manual walkthroughs. A notable inspection reference showed how quadrupeds validated leaks and prevented loss of purified air at a regulated site, which illustrates the performance gains of persistent monitoring over episodic human rounds. Security and campus patrol are currently a smaller share, yet they are set to expand faster as providers reinforce perimeters, parking structures, and lobbies with integrated robot guard workflows. The robot dog market supports these programs with patrols that feed VMS and access control, while trained handlers respond to prioritized alerts that reduce fatigue from constant camera monitoring.

Facilities inspection commanded 42.19% of the 2025 application mix, which anchors the deployment base for multi payload use. In contrast, security and campus patrol is the fastest growing application at a 12.89% CAGR through 2031 as autonomous coverage strengthens nighttime readiness and incident documentation. To sustain growth across both use cases, vendors emphasize safer shared operation and human aware navigation, which shortens training and increases acceptance around staff and visitors. The robot dog market size for facilities inspection accounted for significant share in 2025 deployments, reflecting repeatable returns tied to downtime reduction and energy savings, while security adoption follows where hospital networks consolidate procurement across sites. Partnerships that bring together robots, video analytics, and on premises data processing address hospital privacy needs while enabling immediate incident review. As this foundation stabilizes, extensions to emergency drills and disaster assessment leverage the same autonomy and sensing stack, which expands quadruped utility without new hardware classes.

Geography Analysis

North America held 45.44% of robot dog market share in 2025 as early adopters scaled deployments across inspection, logistics, and campus security. Hospitals in the region benefit from mature quality management frameworks and clear documentation pathways, which supports commissioning, change control, and in service audits. Vendors that align device quality practices with recognized standards help hospitals shorten review cycles and sustain compliance through updates. Academic medical centers, integrated delivery networks, and pharma adjacent facilities are key buyers because they manage complex infrastructures where quadrupeds can traverse stairs and varied terrain. Security use cases expand as hospital networks integrate robots with access control and video systems for continuous coverage and faster incident escalation. Providers have also increased contracts for security robots that supplement guard teams, which indicates confidence in hybrid patrol models at scale.

Asia Pacific is projected to be the fastest growing region at a 13.42% CAGR through 2031 as domestic manufacturers and university hospitals advance trials and lower unit costs. Public reporting indicates that domestic shipments of quadrupeds rose in 2025, which supports pilot programs in elder care and facility tasks across multiple cities. Japanese university hospitals ran proofs of concept in 2026 that validated autonomous navigation through active corridors and entry areas, which builds confidence for real world use with staff oversight. This is also supported by integrators and software partners that tailor robots to local workflows and language interfaces. Industrial collaborations involving inspection robots continue to cross over into regulated healthcare infrastructure, which strengthens safety cases and documentation practices. As these examples accumulate, buyers in the region will have clearer playbooks on governance, cleaning protocols, and incident response in shared spaces.

Europe shows steady interest centered on industrial grade inspection that transfers into hospital facilities and pharma manufacturing sites. The robot dog market in the region benefits from vendors with validated inspection references and strong compliance credentials. Partnerships between robot OEMs and service providers in energy and infrastructure are relevant because they stress reliability, safety, and repeatable documentation that hospital environments also require. Hospitals in Europe apply strict patient rights and data protection rules, so platforms that process video at the edge and provide granular access controls align better with procurement needs. Growth is likely to cluster around academic medical centers and large networks with the governance capacity to onboard new technologies under EU medical device quality systems.

- ANYbotics

- Boston Dynamics

- DEEP Robotics

- Ghost Robotics

- Hiwonder

- Kawasaki Heavy Industries (BEX)

- Keybotic

- LimX Dynamics

- MAB Robotics

- MangDang

- Petoi

- RIVR (formerly Swiss-Mile)

- Sony (aibo)

- Tencent Robotics X (Max)

- Tombot

- Unitree Robotics

- WEILAN (AlphaDog)

- WowWee (CHiP)

- Xiaomi Robotics (CyberDog)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Healthcare staffing shortages and rising labor costs push automation for non-clinical tasks

- 4.2.2 Infection control and staff safety needs in isolation and critical environments

- 4.2.3 Hospital campus security and emergency readiness require 24/7 autonomous patrols

- 4.2.4 AI navigation and sensor fusion enable reliable indoor-outdoor hospital operations

- 4.2.5 Cleanroom/Bio-safety routines and audit trails for labs and pharmacies (under-the-radar)

- 4.2.6 Therapeutic engagement in pediatrics/geriatrics reduces sitter burden (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 High TCO, IT/OT integration, and hospital cybersecurity approvals

- 4.3.2 Clinical workflow fit, infection-control cleaning, and safety validation

- 4.3.3 Patient/visitor acceptance and noise in sensitive wards (under-the-radar)

- 4.3.4 Legacy buildings limit elevator/door/EMC compatibility near imaging suites (under-the-radar)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Healthcare Application

- 5.1.1 Facilities inspection & compliance monitoring (HVAC, med gas, plant rooms)

- 5.1.2 Security and campus patrol

- 5.1.3 Telepresence and virtual rounds in isolation wards

- 5.1.4 Patient engagement and therapy (pediatric, geriatric, behavioral)

- 5.1.5 Emergency response and disaster drills

- 5.1.6 Materials couriering & logistics (lab samples, pharmacy)

- 5.1.7 Training and simulation for medical education

- 5.1.8 Environmental and infectious-disease surveillance

- 5.2 By Care Setting

- 5.2.1 Tertiary/Quaternary Hospitals & IDNs

- 5.2.2 Community Hospitals

- 5.2.3 Pediatric Hospitals

- 5.2.4 Rehabilitation Centers

- 5.2.5 Long-term Care & Nursing Homes

- 5.2.6 Behavioral Health Facilities

- 5.2.7 Outpatient Clinics & ASCs

- 5.2.8 Hospital-based Laboratories & Cleanrooms

- 5.2.9 University Medical Centers & Teaching Hospitals

- 5.2.10 Field Hospitals & Public Health Sites

- 5.3 By Autonomy Level

- 5.3.1 Remote-controlled / Teleoperated

- 5.3.2 Semi-autonomous

- 5.3.3 Fully autonomous

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 ANYbotics

- 6.3.2 Boston Dynamics

- 6.3.3 DEEP Robotics

- 6.3.4 Ghost Robotics

- 6.3.5 Hiwonder

- 6.3.6 Kawasaki Heavy Industries (BEX)

- 6.3.7 Keybotic

- 6.3.8 LimX Dynamics

- 6.3.9 MAB Robotics

- 6.3.10 MangDang

- 6.3.11 Petoi

- 6.3.12 RIVR (formerly Swiss-Mile)

- 6.3.13 Sony (aibo)

- 6.3.14 Tencent Robotics X (Max)

- 6.3.15 Tombot

- 6.3.16 Unitree Robotics

- 6.3.17 WEILAN (AlphaDog)

- 6.3.18 WowWee (CHiP)

- 6.3.19 Xiaomi Robotics (CyberDog)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment