|

시장보고서

상품코드

2063451

나노입자 위탁제조 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Nanoparticle Contract Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

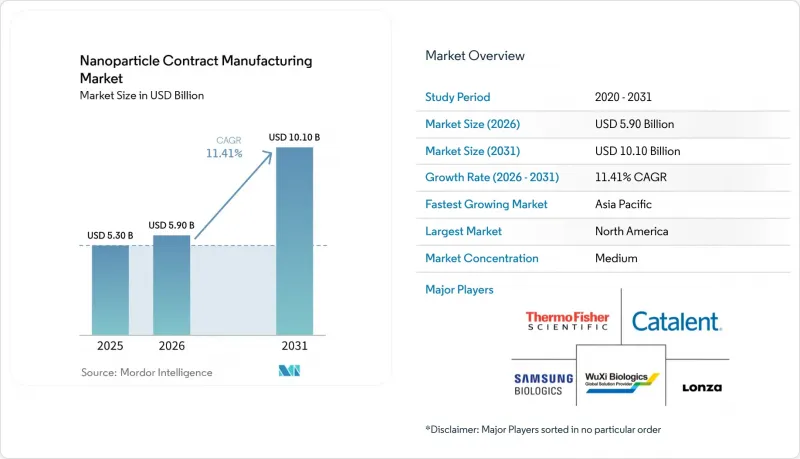

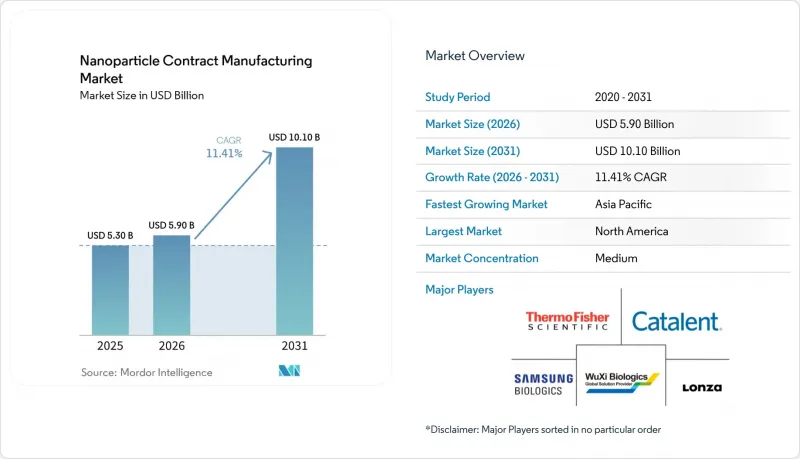

Mordor Intelligence에 의하면, 나노입자 위탁제조 시장 규모는 2025년 53억 달러에서 2026년에는 59억 달러로 확대되어 2031년까지 101억 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 11.41%로 성장할 전망입니다.

본 보고서는 입자(지질 나노입자, 고분자 나노입자 등), 모달리티(mRNA, 저분자 화합물 등), 서비스 유형(제형화 전 스크리닝 등), 용도(종양학 등), 고객 유형(제약·바이오기술 기업 등), 투여 경로(경구 등) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계 나노입자 위탁제조 시장 동향과 인사이트

LNP 생산 능력이 필요한 mRNA/siRNA 파이프라인의 확대

모더나는 2025년 10-K 보고서에서 15개의 임상 프로그램 중 8개가 외부에서 공급받는 지질 나노입자 제제에 의존하고 있음을 밝혔습니다. 이는 사내 시설이 코로나19 부스터 접종용으로 확보되어 있기 때문입니다. BioNTech와 Arbutus의 이러한 아웃소싱 사례는 GMP 기준을 충족하는 물리적 시설에 대한 투자보다 연구 개발(R&D)에 자본을 투입하는 것을 우선시하는 명확한 경향을 보여주고 있습니다. 새로운 FDA 지침에서는 80% 이상의 봉입 효율과 0.2 이하의 다분산 지수가 요구됨에 따라 분석 기준이 높아졌기 때문에 이미 AF4-MALS나 저온 TEM 분석을 수행하고 있는 CDMO가 유리한 입장에 서게 되었습니다. 플랫폼화된 이온화성 지질 덕분에 제제 개발 리드타임이 절반으로 단축됨에 따라, 스폰서는 여러 파이프라인 자산을 동시에 진행할 수 있게 됩니다.

종양학 분야에서 나노의료 기술의 도입이 복잡한 입자에 대한 수요를 뒷받침하고 있습니다.

전신 독성을 완화하는 PEG화 리포솜 및 고분자 운반체를 바탕으로, 2025년 매출의 34.87%를 종양학 분야가 차지했습니다. 머크 KGaA는 나노입자에 캡슐화된 항체-약물 복합체(ADC)에 대한 CDMO 의뢰가 크게 증가했다고 보고했으며, 이는 임상의들이 표적 전달 방식을 선호한다는 사실을 뒷받침합니다. NCI의 연구에 따르면, 고체 지질 나노입자(SLN)는 크레모폴 제제와 비교하여 파클리탁셀의 종양 내 축적량을 3배로 증가시켜, 그 임상적 이점을 강조하고 있습니다. TLR 작용제의 종양 내 주사는 사이토카인 폭풍을 유발하지 않으면서 전신적인 면역 활성화를 유도한다는 사실이 추가로 입증됨에 따라, 나노입자의 활용 범위가 확대되고 있습니다.

복잡한 나노 CMC의 특성 평가 및 비교 가능성과 관련된 위험

FDA가 Translate Bio사에 발송한 2024년 완전 답변서(CRL)에서는 지질 산화 프로파일링이 불충분하다는 지적이 제기되어, 9개월간의 재제출을 강요받았을 뿐만 아니라 규제상 위험도 부각되었습니다. 전 세계적으로 검증된 AF4-MALS 분석을 수행하고 있는 CDMO는 20곳 미만이며, 이로 인해 의뢰사의 선택지가 좁아지고 기술 이전이 지연되고 있습니다. 저온 전자현미경(Cryo-EM)의 비용은 시료당 5,000-1만 달러로, 시드 단계의 벤처 기업에게는 큰 부담이 됩니다. 프로그램 도중에 공급업체를 변경하면 입자 직경이 10-20 nm 정도 변동할 가능성이 있으며, 그 결과 12-18개월이 소요되는 브리징 시험이 필요해질 수 있습니다.

부문별 분석

2025년에는 지질 나노입자가 매출의 32.16%를 차지하며, 나노입자 위탁제조 시장 전체에서 RNA 치료제의 주력 제품으로서 계속해서 중요한 역할을 수행하고 있습니다. 폴리머 기반 시스템은 PLGA나 키토산 캐리어를 통해 지질 기반 시스템으로는 실현하기 어려운 경구 투여 및 서방형 방출을 가능하게 하므로, 연평균 성장률(CAGR) 11.98%로 성장할 전망입니다. 리포솜은 반감기 연장과 심장 독성 감소를 실현하여, 저분자 항암제 분야에서 확고한 틈새 시장을 유지하고 있습니다. 덴드리머는 합성 비용이 높기 때문에 여전히 시제품 단계에 머물러 있습니다. 나노 구조 지질 운반체나 고체 지질 나노입자 등 다른 형태는 피부과 및 안과 분야에서 활용되고 있지만, 무기 입자는 주로 영상 연구에 한정되어 있습니다.

고분자 플랫폼은 FDA 승인을 받은 첨가제를 활용함으로써 독성 시험의 진입 장벽을 낮추고, IND 심사 기간을 단축하고 있습니다. 에보닉(Evonik)사의 유드라지트(Eudragit) 나노입자는 제1상 임상시험에서 경구용 인슐린의 생체이용률을 4배 향상시켜, 고분자 화학이 첫 통과 대사의 문제를 어떻게 해결할 수 있는지 입증했습니다. 삼성바이오로직스는 현재 당뇨병 및 염증성 장질환(IBD)을 대상으로 한 6개의 2상 폴리머 기반 프로그램을 보유하고 있으며, 이 분야의 신뢰도를 높이고 있습니다. 지질계와 고분자계 제품 라인을 모두 제공하는 CDMO는 수요 변동을 조정하고 설비의 가동 중단 시간을 줄일 수 있으며, 나노입자 위탁제조 시장이 다양화되는 가운데 이는 전략적 우위가 됩니다.

2025년 매출액에서 저분자 약물이 차지하는 비중은 28.13%로, 이는 나노입자를 통해 용해된 항암제가 주도한 결과입니다. 그러나 mRNA 프로젝트는 감염병 백신과 저용량 투여를 가능하게 하는 새로운 자가증폭형 구조체의 등장으로 인해 2031년까지 연평균 성장률(CAGR) 11.89%를 나타낼 것으로 전망됩니다. CRISPR-Cas9 리보핵산단백질 등의 유전자 편집 페이로드에는 엔도좀에서 탈출하는 데 최적화된 초고순도 LNP가 필요하며, 이로 인해 분석 요건이 더욱 까다로워지고 있습니다. 펩타이드 및 단백질 치료법에서는 효소에 의한 분해를 방지하기 위해 pH 감응성 고분자 입자를 활용하고 있습니다. 실온에서 6개월간 안정적으로 유지되는 고리형 RNA는 나노입자 위탁제조 시장에 새로운 물류상의 이점을 제공합니다.

이러한 치료법의 다양화로 인해, 현재는 더욱 폭넓은 후원자층이 참여하고 있습니다. 모더나(Moderna)는 심혈관 및 종양학 분야에 걸쳐 15개의 비코로나19용 mRNA 프로그램을 제시하고 있으며, 이들 각각은 외부 제형 솔루션에 의존하고 있습니다. BioNTech사의 흑색종 신항원에 관한 데이터에 따르면, 맞춤형 LNP를 통해 투여했을 때 객관적 반응이 확인되어 효능 향상이 시사되었을 뿐만 아니라, 아웃소싱 파이프라인도 강화되었습니다.

지역별 분석

2025년, 북미는 매출의 39.16%를 차지하며 나노 입자 위탁제조 시장을 독점했습니다. 이는 보스턴, 샌프란시스코, 리서치 트라이앵글에 30개 이상의 GMP 인증 지질 나노입자 제조 시설이 존재한다는 점이 뒷받침하고 있습니다. 모든 IND 신청에 대해 극저온 TEM 및 AF4-MALS 사용을 의무화하는 FDA의 최종 지침은 미국의 첨단 제조 역량에 대한 수요를 더욱 공고히 하고 있습니다. 캐나다는 NRC 몬트리올을 통해 국내 아웃소싱을 지원하고 있는 반면, 멕시코의 톨카 클러스터는 초기 단계의 미국 후원사들에게 니어쇼어 방식의 비용 차익 거래를 제공합니다.

아시아태평양은 중국의 NMPA가 2024년부터 2025년까지 8개의 LNP 제품을 승인하고, 인도의 CDMO가 새로운 혼합 라인에 5억 달러를 투자함에 따라 연평균 성장률(CAGR) 11.84%를 기록하며, 지역별로는 가장 빠른 성장이 예상됩니다. 삼성바이오로직스의 3억 달러 규모 확장으로, 한국은 이 지역의 거점으로서의 입지를 공고히 하고 있습니다. 호주는 통합된 1상 임상시험 시설을 활용하여 현지 생명공학 기업의 임상시험을 유치하고 있으며, 한편 일본 PMDA의 지침 조화를 통해 수출 장벽이 낮아지고 있습니다.

유럽은 이 두 극단 사이의 중간에 위치하며, Polymun Scientific이나 Evonik과 같은 기업을 통해 특수 이온화 지질 화학 분야에서 강점을 발휘하고 있습니다. EMA의 검토 문서는 CMC 요건의 조화를 도모하고 있지만, 영국의 MHRA가 독자적으로 마련한 절차는 일부 신청사에게 더 신속한 대안이 되고 있습니다. 스페인의 Rovi 시설은 Moderna의 유럽 내 공급을 확보하고 있으며, 스위스에 본사를 둔 Lonza는 후기 임상시험 프로그램에서 주요 공급업체로서의 입지를 유지하고 있습니다. 중동 및 아프리카 및 남미 지역의 신흥 수요는 콜드체인 부족으로 인해 제약을 받고 있지만, 브라질의 Fiocruz와 남아프리카공화국의 Biovac은 나노입자 백신 생산 라인에 대한 투자를 추진하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the nanoparticle contract manufacturing market size is expected to increase from USD 5.30 billion in 2025 to USD 5.90 billion in 2026 and reach USD 10.10 billion by 2031, growing at a CAGR of 11.41% over 2026-2031.

This report is Segmented by Particle (Lipid Nanoparticles, Polymeric Nanoparticles, and More), Modality (mRNA, Small Molecules, and More), Service Type (Pre-Formulation Screening and More), Application (Oncology and More), Client Type (Pharmaceutical and Biotechnology Companies and More), Delivery Route (Oral and More), and Geography. Market Forecasts are Provided in Value (USD).

Global Nanoparticle Contract Manufacturing Market Trends and Insights

Expansion of mRNA/siRNA Pipelines Requiring LNP Capacity

Moderna disclosed in its 2025 10-K that eight of fifteen clinical programs rely on external lipid-nanoparticle formulation because in-house suites are reserved for COVID-19 boosters. Similar outsourcing by BioNTech and Arbutus shows a clear preference to deploy capital toward R&D rather than toward GMP bricks-and-mortar. New FDA guidance now requires ≥80% encapsulation efficiency and a polydispersity index ≤0.2, elevating the analytical bar and favoring CDMOs that already run AF4-MALS and cryo-TEM assays . With platformized ionizable lipids cutting formulation timelines in half, sponsors can progress multiple pipeline assets concurrently.

Oncology Nanomedicine Adoption Sustaining Complex Particle Demand

Oncology held 34.87% revenue in 2025 on the back of PEGylated liposomes and polymeric carriers that temper systemic toxicity. Merck KGaA logged a significant jump in CDMO requests for antibody-drug conjugate cargos encapsulated in nanoparticles, confirming clinician preference for targeted delivery . NCI studies show solid-lipid nanoparticles triple tumor accumulation for paclitaxel versus Cremophor formulations, underlining the clinical upside. Intratumoral injections of TLR agonists further show systemic immune activation without cytokine storms, broadening nanoparticle use cases.

Complex Nano-CMC Characterization and Comparability Risk

FDA's 2024 Complete Response Letter to Translate Bio cited inadequate lipid-oxidation profiling, forcing a nine-month refile and underscoring regulatory stakes. Less than 20 CDMOs worldwide run validated AF4-MALS assays, narrowing sponsor choice and slowing tech transfer . Cryo-EM costs USD 5,000-10,000 per sample, a heavy burden for seed-stage ventures. Switching vendors mid-program can shift particle size by 10-20 nm, triggering bridging studies that add 12-18 months.

Other drivers and restraints analyzed in the detailed report include:

- Outsourcing Acceleration Tied to Capex and Analytics Barriers

- Regulatory Clarity Around Nano-CMC Expectations

- High Cost, Scale-Up Risk, and Batch-Failure Sensitivity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lipid nanoparticles secured 32.16% revenue in 2025 and remain the primary workhorse for RNA therapeutics across the Nanoparticle Contract Manufacturing Market. Polymeric systems will grow at an 11.98% CAGR because PLGA and chitosan carriers enable oral dosing and sustained release that lipids struggle to match. Liposomes retain a solid niche in small-molecule oncology, delivering extended half-life and reduced cardiotoxicity. Dendrimers stay in prototype status due to high synthesis cost. Other formats, such as nanostructured lipid carriers and solid lipid nanoparticles, serve dermatology and ophthalmology, while inorganic particles are largely confined to imaging studies.

Polymeric platforms capitalize on FDA-approved excipients, lowering toxicology hurdles and shortening IND review. Evonik's Eudragit nanoparticles improved oral insulin bioavailability fourfold in Phase I, demonstrating how polymer chemistry can solve first-pass metabolism challenges. Samsung Biologics now lists six Phase II polymeric programs for diabetes and IBD, giving credibility to the segment. CDMOs offering both lipid and polymer lines can arbitrage demand swings and reduce capacity downtime, a tactical edge as the Nanoparticle Contract Manufacturing Market diversifies.

Small-molecule cargos held 28.13% of 2025 revenue, powered by nanoparticle-solubilized oncology agents. mRNA projects, however, will post an 11.89% CAGR on the way to 2031, propelled by infectious-disease vaccines and emerging self-amplifying constructs that permit lower dosing. Gene-editing payloads such as CRISPR-Cas9 ribonucleoproteins require ultra-pure LNPs optimized for endosomal escape, pushing analytical demands higher. Peptide and protein therapies leverage pH-sensitive polymeric particles to prevent enzymatic degradation. Circular RNA, stable at room temperature for six months, offers new logistical advantages for the Nanoparticle Contract Manufacturing Market.

The modality mix now attracts a wider sponsor base. Moderna lists fifteen non-COVID mRNA programs spanning cardiology and oncology, each depending on external formulation suites. BioNTech's melanoma neoantigen data showed objective response when delivered via customized LNPs, underscoring efficacy upside and fortifying outsourcing pipelines.

Geography Analysis

North America dominated the Nanoparticle Contract Manufacturing Market with 39.16% revenue in 2025, supported by more than 30 GMP-certified lipid-nanoparticle suites across Boston, San Francisco, and the Research Triangle. FDA final guidance that now mandates cryo-TEM and AF4-MALS for all IND submissions further entrenches demand for advanced U.S. capacity. Canada subsidizes domestic outsourcing through NRC Montreal, while Mexico's Toluca cluster offers near-shore cost arbitrage for early-stage U.S. sponsors.

Asia-Pacific is forecast to record an 11.84% CAGR, the fastest regional climb, as China's NMPA cleared eight LNP products in 2024-2025 and Indian CDMOs invested USD 500 million in new mixing lines. Samsung Biologics' USD 300 million expansion cements South Korea as a regional anchor. Australia leverages integrated Phase I units to woo local biotech trials, while Japan's PMDA guidance convergence reduces export hurdles.

Europe sits between these poles, strong in specialized ionizable-lipid chemistry through players like Polymun Scientific and Evonik. EMA's reflection paper harmonizes CMC demands, but the UK's separate MHRA pathway offers a faster alternative for some sponsors. Spain's Rovi facility secured Moderna's European supply, and Swiss-based Lonza remains the go-to vendor for late-stage programs. Emerging demand in Middle East & Africa and South America is limited by cold-chain gaps, though Brazil's Fiocruz and South Africa's Biovac are investing in nanoparticle vaccine lines.

- AGC Biologics

- Ardena

- Catalent Biologics

- CordenPharma

- Curia

- Danaher

- Evonik Health Care

- Fortis Life Sciences

- Laboratorios Farmaceuticos Rovi

- Lonza Group

- Merck

- Nanoform Finland

- PCI Pharma Services

- Polymun Scientific

- Recipharm

- Rentschler Biopharma

- Samsung Group

- ST Pharm

- Thermo Fisher Scientific

- Vernal Biosciences

- Wuxi Biologics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of mRNA/siRNA pipelines requiring LNP-enabled CDMO capacity

- 4.2.2 Oncology nanomedicine adoption sustaining complex nanoparticle demand

- 4.2.3 Outsourcing acceleration due to capex, GMP, and analytics barriers

- 4.2.4 Regulatory clarity and evolving CMC expectations for nanomedicines

- 4.2.5 Platformization of LNP/analytical toolkits reducing time-to-clinic

- 4.2.6 saRNA/circRNA programs creating novel formulation demand

- 4.3 Market Restraints

- 4.3.1 Complex, evolving nano-CMC characterization and comparability risk

- 4.3.2 High cost, scale-up risk, and batch failure sensitivity

- 4.3.3 Lipid IP/licensing constraints and freedom-to-operate hurdles

- 4.3.4 Cold-chain and aseptic constraints for nano-DP/fill-finish

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Particle

- 5.1.1 Lipid nanoparticles

- 5.1.2 Nanostructured lipid carriers

- 5.1.3 Dendrimers

- 5.1.4 Liposomes

- 5.1.5 Polymeric nanoparticles

- 5.1.6 Nanoemulsions

- 5.1.7 Solid lipid nanoparticles

- 5.1.8 Polymeric micelles

- 5.1.9 Inorganic nanoparticles

- 5.2 By Modality / Payload

- 5.2.1 mRNA

- 5.2.2 Small molecules

- 5.2.3 Gene editing cargos

- 5.2.4 siRNA / ASO

- 5.2.5 Peptides

- 5.2.6 Vaccines

- 5.2.7 DNA

- 5.2.8 Proteins

- 5.2.9 Therapeutic vaccines

- 5.3 By Service Type

- 5.3.1 Pre-formulation screening

- 5.3.2 Analytical & characterization

- 5.3.3 Aseptic fill-finish & lyophilization

- 5.3.4 Formulation development

- 5.3.5 GMP clinical manufacturing (DP)

- 5.3.6 Tech transfer & comparability

- 5.3.7 Process development & scale-up

- 5.3.8 GMP commercial manufacturing (DP)

- 5.3.9 Stability & method validation

- 5.4 By Application

- 5.4.1 Oncology

- 5.4.2 Infectious diseases

- 5.4.3 Genetic & metabolic disorders

- 5.4.4 Cardiovascular & metabolic

- 5.4.5 CNS

- 5.4.6 Ophthalmology

- 5.4.7 Respiratory

- 5.4.8 Immunology/Inflammation

- 5.5 By Client Type

- 5.5.1 Pharmaceutical and Biotechnology Companies

- 5.5.2 Academic and Research Institutes

- 5.5.3 Contract Research Organizations

- 5.6 By Delivery Route

- 5.6.1 Intravenous (IV)

- 5.6.2 Intramuscular (IM)

- 5.6.3 Subcutaneous (SC)

- 5.6.4 Inhalation

- 5.6.5 Intratumoral

- 5.6.6 Intrathecal

- 5.6.7 Ocular

- 5.6.8 Oral

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AGC Biologics

- 6.3.2 Ardena

- 6.3.3 Catalent Biologics

- 6.3.4 CordenPharma

- 6.3.5 Curia

- 6.3.6 Danaher Corporation

- 6.3.7 Evonik Health Care

- 6.3.8 Fortis Life Sciences

- 6.3.9 Laboratorios Farmaceuticos Rovi

- 6.3.10 Lonza

- 6.3.11 Merck KGaA

- 6.3.12 Nanoform Finland

- 6.3.13 PCI Pharma Services

- 6.3.14 Polymun Scientific

- 6.3.15 Recipharm

- 6.3.16 Rentschler Biopharma

- 6.3.17 Samsung Biologics

- 6.3.18 ST Pharm

- 6.3.19 Thermo Fisher Scientific

- 6.3.20 Vernal Biosciences

- 6.3.21 WuXi Biologics

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment