|

시장보고서

상품코드

2063467

진단용 피부과 기기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Diagnostic Dermatology Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

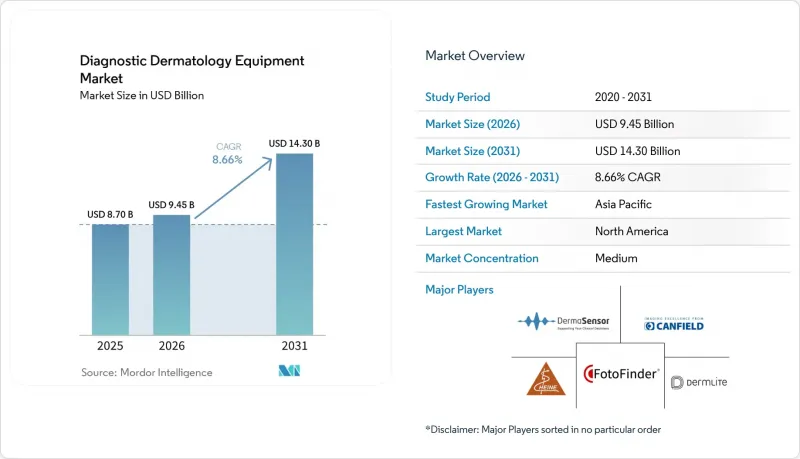

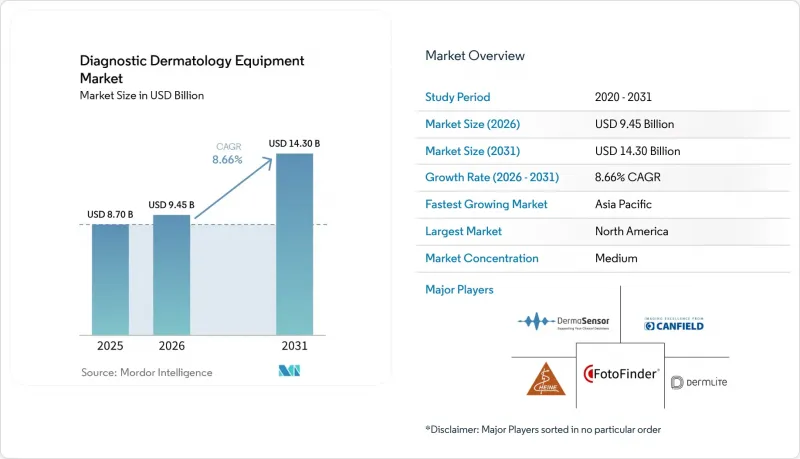

Mordor Intelligence에 의하면, 진단용 피부과 기기 시장 규모는 2025년 87억 달러로 평가되었습니다. 2026년에는 94억 5,000만 달러로 확대되어 2031년까지 143억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 8.66%를 나타낼 것으로 전망됩니다.

본 보고서는 기기별(피부현미경 등), 휴대성별(휴대용/포켓형 피부현미경, 고정형 피부현미경 등), 용도별(피부암 등), 최종 사용자별(병원, 피부과 클리닉·센터 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 진단용 피부과 기기 시장 동향 및 인사이트

피부암 발병률 증가와 선별검진 프로그램 확대

피부암 유병률이 증가함에 따라 조기 발견이 의료 서비스의 핵심으로 자리 잡고 있으며, 이로 인해 영상 진단 분야에 대한 지속적인 투자가 촉진되고 있습니다. 미국에서는 2025년에 침윤성 흑색종 및 국소성 흑색종의 신규 환자가 약 10만 4,960건 발생했으며, 이들의 5년 생존율은 99%입니다. 이러한 상황은 1차 진료 현장으로도 확대 적용 가능한 시스템 차원의 선별 검사 방안과 영상 유도 기반 분류 경로의 추진을 뒷받침하고 있습니다. 호주는 여전히 세계에서 가장 높은 흑색종 발병률 중 하나를 기록하고 있으며, 국내 이해관계자들은 적시 개입을 위한 표적 선별 검사 및 진단 도구에 대한 접근성 향상에 계속해서 큰 중점을 두고 있습니다. 이러한 임상적 현실은 스토어 앤 포워드(저장 및 전송) 방식을 통한 상담을 가능하게 하고, 피부과로의 의뢰를 효율화함으로써, 연결 가능한 피부경 및 상호 운용 가능한 이미지 플랫폼에 대한 꾸준한 수요를 뒷받침하고 있습니다. 보건 기관과 전문 단체들도 예방 및 선별 검사 활동을 추진하고 있으며, 이는 간접적으로 진단용 피부과 기기 시장 전반의 기기 활용을 촉진하고 있습니다. 의료 시스템의 프로토콜이 표준화됨에 따라, 진단용 피부과 기기 시장에서는 독립형 광학 기기에서 통합된 영상 관리 및 AI 기반 진단 지원으로의 꾸준한 업그레이드가 진행되고 있습니다.

비침습적 영상 진단으로의 전환

비침습적 영상 검사는 생검 전 병변을 계층화하는 데 도움이 되며, 고해상도의 구조적 정보를 바탕으로 치료 방침을 결정하는 데 기여하기 때문에 임상 현장에서의 활용이 확대되고 있습니다. LC-OCT 및 OCT 플랫폼은 뛰어난 임상 성능과 운영 효율성을 발휘하고 있으며, LC-OCT는 세포 수준에 가까운 해상도와 깊은 침투 깊이를 제공하여 한 번의 검사로 표피 및 진피의 구조를 시각화합니다. 2025년 3월 LC-OCT 시스템의 FDA 승인으로, 이 하이브리드 모달리티의 미국 시장 진출이 공식적으로 확정되었습니다. 이를 통해 불필요한 절제를 줄이고, 수술 전 절제 경계를 평가하는 데 도움이 되는 광학 워크플로우에 대한 임상의들의 신뢰가 높아지고 있습니다. 상관 연구에서는 기저세포암의 주요 특징에 대해 조직병리학과의 높은 일치율이 지속적으로 나타나고 있으며, 이는 침습적인 생검 전 진단 과정에 OCT 및 LC-OCT를 정착시키는 데 기여하고 있습니다. 비침습적 영상 기술이 신속한 임상 판단과 연계됨에 따라, 진단용 피부과 기기 시장은 고해상도 기기와 상호 운용 가능한 소프트웨어를 우선시하는 업데이트 주기의 혜택을 누리고 있습니다. AI 기반 진단 도구 및 원격 피부과 진료 도입

첨단 시스템의 높은 도입 및 유지 비용

자본 집약성은 여전히 제약 요인으로 작용하고 있으며, 특히 영업이익률이 낮은 개인 개업의나 소규모 클리닉의 경우 그 현상이 두드러집니다. 고급 영상 진단 제품군이나 전신 3D 시스템의 경우, 시설 준비, 훈련을 받은 직원, 그리고 안전한 보관을 위한 IT 인프라가 필요하며, 이러한 요소들은 장비 가격을 넘어서는 초기 비용을 더욱 증가시킵니다. 임상 사진 및 AI 소프트웨어와의 통합에는 지속적인 라이선스 비용과 업그레이드가 수반되므로, 의료기관은 수년에 걸쳐 지속적인 비용 부담을 감수해야 합니다. 이러한 현실을 감안하여, 우선 연결형 피부경이나 영상 관리 소프트웨어부터 도입을 시작하고, 증례 수가 증가함에 따라 비침습적 영상 진단 모듈로 단계적으로 전환하는 경향이 나타나고 있습니다. 병원 시스템이 설비 투자를 주도하는 경우에는 연구 및 교육이라는 사명을 맡은 학술 기관에 도입이 집중되는 반면, 지역 의료 기관에서는 공유 서비스 모델이나 원격 피부과 진료 제휴를 통해 도입이 진행되고 있습니다. 이러한 단계적 접근 방식에 따라 단기적인 구매 수요는 억제되지만, 진단용 피부과 기기 시장에서 상호 운용 가능한 플랫폼에 대한 수요는 유지되고 있습니다.

부문별 분석

2025년, 피부경(dermatoscope)은 진단용 피부과 기기 시장 규모의 32.10%를 차지하며, 1차 진료 및 피부과에서 환자 선별 첫 단계로서 입지를 확고히 다졌습니다. 연결형 피부현미경을 일상적으로 사용하면 영상 촬영의 표준화에 기여하며, 저장 및 전송 워크플로우를 지원합니다. 이를 통해 환자의 접근성이 확대되고, 필요에 따라 전문의에게의 의뢰가 신속해집니다. OCT 플랫폼은 표재성 및 비표재성 기저세포암에 대한 병변의 계층화 및 치료 계획 수립과 같은 활용 사례에 힘입어, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.90%로 가장 높은 성장률을 나타낼 것으로 전망됩니다. 임상 상관 연구를 통해 조직병리학적 소견과 일치하는 기저세포암(BCC)의 특징에 대해 하이브리드 LC-OCT의 유효성이 지속적으로 입증됨에 따라, 생검 전 단계에서 비침습적 영상 진단에 대한 임상의들의 신뢰가 높아지고 있습니다. 소프트웨어가 이미지 관리 및 원격 검토의 기반이 됨에 따라, 진단용 피부과 기기 시장은 광학 촬영, AI 기반 의사결정 지원 및 아카이브 기능을 결합한 통합 생태계로 전환되고 있습니다.

2025년에는 휴대용 또는 포켓 사이즈의 피부경이 36.10%의 시장 점유율을 차지했으며, 2031년까지 연평균 성장률(CAGR) 8.60%를 나타낼 것으로 전망됩니다. 이는 피부 병변 평가 및 원격 분류의 최전선에서 이러한 기기들이 수행하는 역할을 반영한 것입니다. 스마트폰용 액세서리 및 연동 워크플로우를 통해 이미지 품질의 일관성이 향상되어, 1차 진료 담당자가 고위험 사례를 효율적으로 의뢰할 수 있게 됩니다. 고정형 피부현미경 및 고정 광학 시스템은 환자 수가 많은 진료소에서 여전히 필수적이며, 안정적인 광학 시스템과 통합된 촬영 장치를 통해 움직임으로 인한 아티팩트를 줄이고 표준화된 검사를 지원합니다. 바디 매핑을 자동화하는 트롤리 탑재형 이미징 시스템은 특히 AI를 활용한 변화 감지 기능과 결합함으로써 경과 시간에 따른 모니터링과 데이터 수집을 가속화합니다. 이러한 기기 유형들은 1차 진료 단계에서의 신속한 촬영부터 전문 의료 센터에서의 보다 종합적인 영상 진단에 이르기까지를 아우르며, 진단용 피부과 기기 시장을 확대되고 있습니다. RCM(공명 광산란법) 및 OCT(광간섭 단층촬영)용 벤치탑형 또는 콘솔형 시스템은 치료 방침을 결정하는 데 조직학적 수준의 상세한 정보와 더 깊은 구조적 시각화가 필요한 전문의의 업무 흐름을 지원합니다. 병원이나 학술 기관에서는 일반적으로 팀이 기술, 영상 판독 능력 및 표준화된 보고서 작성 능력을 유지할 수 있도록 이러한 시스템을 도입하고 있습니다. 진단용 피부과 기기 시장에서는 영상 보관, 주석 달기, 원격 판독을 위한 상호 운용 가능한 소프트웨어가 점점 더 중요해지고 있으며, 이를 통해 여러 거점에 걸친 네트워크 간의 마찰이 완화됩니다. 휴대용, 고정형, 콘솔형 등 폭넓은 제품 라인업은 의료 서비스 제공업체가 치료 과정 전반에 걸친 다양한 이용 사례에 맞추어 제품을 구매할 때, 공급업체의 입지를 강화합니다.

지역별 분석

2025년, 북미는 진단용 피부과 기기 시장 규모의 39.60%를 차지했습니다. 이는 공초점 이미징에 대한 명확한 보상 체계와 비침습적 진단에 대한 기관의 투자에 힘입은 결과입니다. 메디케어는 특정 전국 통일 지급액을 정한 RCM(수익 관리)용 CPT(진료 행위 분류) 경로를 유지하고 있으며, 이는 청구의 기반이 되어 선정된 시설에서 더 광범위한 임상 활용의 길을 열어주고 있습니다. 피부암 예방과 조기 발견에 대한 관심이 높아짐에 따라, 선별검사 및 종양학 프로그램 전반에 걸쳐 장비 사용의 일관성이 강화되고 있습니다. FDA의 의료기기용 AI 및 머신러닝 프레임워크는 알고리즘 업데이트를 위한 예측 가능한 절차를 도입하고 있으며, 이를 통해 진단 및 피부과용 기기 시장에서 AI 기반 영상 솔루션의 혁신 주기가 단축되고 있습니다.

유럽에서는 독일, 프랑스, 영국에서 이 기술이 현저하게 보급되고 있으며, 탄탄한 임상 인프라와 공적 보험의 지원이 고도의 영상 진단을 뒷받침하고 있습니다. LC-OCT 분야의 EU 중심 혁신은 최근 미국 FDA의 승인으로 가속화되고 있으며, 이는 대서양을 가로지르는 임상 검증과 모범 사례의 교류를 촉진하고 있습니다. 의료 제공업체 네트워크는 품질과 규정 준수를 중시하며, 명확한 임상적 근거와 명확한 시판 후 계획을 갖춘 영상 진단 플랫폼을 선호합니다. 병원 시스템이 시간 경과에 따른 모니터링을 확대하고 AI를 활용한 변화 분석을 통합함에 따라, 그 활용 사례는 종양학을 넘어 염증성 피부 질환의 특성 평가로 확대되고 있습니다. 이러한 환경은 진단용 피부과 기기 시장에서 피부경검, OCT 및 LC-OCT를 통합한 워크플로우를 갖춘 플랫폼의 지속적인 도입을 촉진하고 있습니다.

아시아태평양은 피부과 서비스의 지속적인 확대와 의료 서비스가 미치지 못하는 지역에서의 원격 피부과 진료 보급에 힘입어, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.90%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 지역입니다. 호주는 연령 조정 발병률이 세계 최고 수준이며, 대상자를 선별한 검진 및 지방 지역의 영상 진단 접근성 확보에 국가 차원에서 지속적으로 주력하고 있어, 이 지역의 높은 위험 프로파일을 상징하고 있습니다. 의료 시스템이 원격 의료와 표준화된 선별 검사를 추진하는 가운데, 영상 관리 소프트웨어와 원격 판독의 지원을 받아 지역 의료 현장에서 휴대용 피부경(dermatoscope)이 점차 보급되고 있습니다. 주요 도시권 외의 지역 사회에서 3D 바디 매핑에 대한 접근성을 확대하려는 기업 주도의 노력은 APAC 지역의 성장 궤적에서 모바일 영상 진단이 차지하는 역할을 더욱 부각시키고 있습니다. 이러한 추세는 상호 운용이 가능한 영상 진단 기술과 AI 분류 워크플로우를 통해 1차 진료 기관과 전문 의료 센터를 연결함으로써, 진단용 피부과 기기 시장을 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the diagnostic dermatology equipment market size is expected to increase from USD 8.70 billion in 2025 to USD 9.45 billion in 2026 and reach USD 14.30 billion by 2031, growing at a CAGR of 8.66% over 2026-2031.

This report is Segmented by Device (Dermatoscopes, and More), Portability (Handheld/Pocket Dermatoscopes, Stationary/Fixed Dermatoscope, and More), Application (Skin Cancer, and More), End-User (Hospitals, Dermatology Clinics & Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Diagnostic Dermatology Equipment Market Trends and Insights

Rising Skin Cancer Incidence and Screening Program Expansion

Skin cancer prevalence keeps early detection at the center of care delivery, which prompts sustained investment in diagnostic imaging. In the United States, in 2025, an estimated 104,960 new cases of invasive melanoma and localized melanoma carry a 99% five-year survival rate, which motivates system-level screening initiatives and image-guided triage pathways that can be scaled into primary care settings. Australia continues to face one of the world's highest melanoma incidence rates, and national stakeholders maintain a strong emphasis on targeted screening and enhanced access to diagnostic tools for timely intervention. This clinical reality supports steady demand for connected dermatoscopes and interoperable imaging platforms that enable store-and-forward consultations and streamline referrals to dermatology. Health agencies and professional associations also promote prevention and screening activities, which indirectly sustain device utilization across the diagnostic dermatology equipment market. As health systems standardize protocols, the Diagnostics dermatology equipment market tracks consistent upgrades from standalone optical tools to integrated image-management and AI-supported review.

Shift to Non-Invasive Imaging

Non-invasive imaging is expanding clinical use because it helps stratify lesions before biopsy and supports treatment decisions with high-resolution structural information. LC-OCT and OCT platforms demonstrate strong clinical performance and operating efficiency, with LC-OCT providing near-cellular resolution and deeper penetration to visualize epidermal and dermal architecture in one session. The FDA clearance of an LC-OCT system in March 2025 formalized U.S. entry for this hybrid modality, which strengthens clinician confidence in optical workflows that can reduce unnecessary excisions and guide pre-surgical margin assessment. Correlation studies continue to show high agreement with histopathology for key basal cell carcinoma features, which helps embed OCT and LC-OCT in diagnostic pathways before invasive sampling. As non-invasive imaging aligns with faster clinical decisions, the Diagnostics dermatology equipment market benefits from replacement cycles that prioritize higher-resolution devices and interoperable software. AI-Enabled Diagnostic Tools and Teledermatology Adoption

High Acquisition and Ownership Costs for Advanced Systems

Capital intensity remains a constraint, especially for private practices and smaller clinics that face tight operating margins. Advanced imaging suites and total-body 3D systems require facility readiness, trained staff, and IT infrastructure for secure storage, which compounds initial outlays beyond device price. Integration with clinical photography and AI software also involves ongoing licensing and upgrades, which commits providers to recurring expenses over multi-year periods. These realities encourage phased adoption that starts with connected dermatoscopes and image-management software, then proceeds to non-invasive imaging modules as case volumes grow. Where hospital systems lead capital programs, deployments cluster in academic centers with research and training mandates, while community facilities progress through shared-service models and teledermatology alliances. This staged approach moderates near-term purchasing, yet it preserves demand for interoperable platforms in the diagnostics dermatology equipment market.

Other drivers and restraints analyzed in the detailed report include:

- RCM Reimbursement Momentum (Category-1 CPT Codes)

- Emergent LC-OCT Hybrid Modality Expands Use-Cases

- Shortage of Trained Operators; Workflow Time Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dermatoscopes commanded 32.10% share of the diagnostics dermatology equipment market size in 2025, affirming their position as the entry point for triage across primary care and dermatology. Routine use of connected dermatoscopes helps standardize image capture and supports store-and-forward workflows, which expands access for patients and accelerates referrals to specialists when needed. OCT platforms are projected to post the highest growth at an 8.90% CAGR during 2026-2031, driven by use cases that include lesion stratification and treatment planning for superficial versus non-superficial basal cell carcinoma. Clinical correlation continues to validate hybrid LC-OCT for BCC features that align with histopathology, which strengthens clinician trust in non-invasive imaging as a pre-biopsy step. As software becomes the organizing layer for image management and remote review, the diagnostics dermatology equipment market tilts toward integrated ecosystems that combine optical capture, AI decision support, and archival.

Handheld or pocket dermatoscopes held a 36.10% share in 2025 and are projected to grow at an 8.60% CAGR through 2031, reflecting their role at the front line of skin lesion evaluation and remote triage. Smartphone-compatible accessories and connected workflows improve image quality consistency and enable primary-care users to refer higher-risk cases efficiently. Stationary dermatoscopes and fixed optical systems remain critical in high-volume clinics, where stable optics and integrated capture rigs reduce motion artifacts and support standardized examinations. Trolley-mounted imaging suites that automate body mapping accelerate longitudinal monitoring and data capture, especially when paired with AI-enabled change detection. These device formats expand the diagnostics dermatology equipment market by covering both quick capture in primary care and more comprehensive imaging in specialty centers. Benchtop or console systems for RCM and OCT anchor specialist workflows that need near-histologic detail or deeper structural views to guide management. Hospitals and academic centers typically deploy these systems to help teams maintain technique, interpretation skills, and standardized reporting. The diagnostics dermatology equipment market increasingly favors interoperable software for image archiving, annotations, and remote reads, which reduces friction across multi-site networks. Portfolio breadth across handheld, stationary, and console formats strengthens vendor positioning as providers align purchases with diverse clinical use cases across the care continuum.

Geography Analysis

North America accounted for 39.60% share of the diagnostics dermatology equipment market size in 2025, supported by defined reimbursement frameworks for confocal imaging and institutional investment in non-invasive diagnostics. Medicare has maintained CPT pathways for RCM with specified national payment amounts, which anchor billing and pave the way for broader clinical use in select centers. Rising emphasis on skin cancer prevention and early detection also reinforces consistent device utilization across screening and oncology programs. The FDA's AI and machine learning framework for medical devices introduces a predictable route for algorithm updates, which shortens innovation cycles for AI-enabled imaging solutions in the diagnostics and dermatology equipment market.

Europe maintains significant adoption across Germany, France, and the United Kingdom, where robust clinical infrastructure and public coverage support advanced imaging. EU-centered innovation in LC-OCT has accelerated with recent United States FDA clearance, which encourages transatlantic clinical validation and best-practice exchange. Provider networks emphasize quality and compliance, which favors imaging platforms with clear clinical evidence and defined postmarket plans. As hospital systems scale longitudinal monitoring and integrate AI-assisted change analysis, use cases broaden beyond oncology toward inflammatory dermatoses characterization. This environment supports continued platform adoption that integrates dermoscopy, OCT, and LC-OCT into unified workflows in the diagnostics dermatology equipment market.

Asia Pacific is the fastest-growing region with an 8.90% projected CAGR during 2026-2031, led by the continued expansion of dermatology services and the diffusion of teledermatology in underserved areas. Australia illustrates the region's high-risk profile, with age-standardized incidence among the highest worldwide and a sustained national focus on targeted screening and rural access to imaging. As health systems promote remote care and standardized screening, handheld dermatoscopes gain traction in community settings supported by image-management software and remote reading. Company-led initiatives to extend 3D body-mapping access in communities outside major metro areas further underline the role of mobile imaging in APAC's growth trajectory. These developments expand the diagnostic dermatology equipment market by connecting primary care to specialist centers through interoperable imaging and AI triage workflows.

- Canfield Scientific

- Cortex Technology (DermaLab)

- Damae Medical (deepLive LC-OCT)

- DermaSensor Inc.

- DermLite

- DermoScan GmbH

- FotoFinder Systems

- HEINE Optotechnik

- ILLUCO Corpo

- Kirchner & Wilhelm GmbH + Co. KG

- MedX Health Corp.

- MetaOptima Technology (DermEngine)

- Michelson Diagnostics Ltd. (VivoSight)

- Optilia Instruments

- SciBase

- VivaScope GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Skin Cancer Incidence and Screening Program Expansion

- 4.2.2 Shift to Non-Invasive Imaging

- 4.2.3 AI-Enabled Diagnostic Tools and Teledermatology Adoption

- 4.2.4 RCM Reimbursement Momentum (Category-1 CPT Codes)

- 4.2.5 Emergent LC-OCT Hybrid Modality Expands Use-Cases

- 4.3 Market Restraints

- 4.3.1 High Acquisition and Ownership Costs for Advanced Systems

- 4.3.2 Shortage of Trained Operators; Workflow Time Constraints

- 4.3.3 Regulatory/Data-Governance Hurdles for AI/ML (Samd)

- 4.3.4 Inconsistent Reimbursement for Imaging/Teledermatology

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device

- 5.1.1 Dermatoscopes

- 5.1.2 Digital Photographic Imaging Systems

- 5.1.3 Reflectance Confocal Microscopy (RCM)

- 5.1.4 Optical Coherence Tomography (OCT)

- 5.1.5 High-Frequency Ultrasound (HFUS)

- 5.1.6 Electrical Impedance Spectroscopy (EIS)

- 5.1.7 Total Body 3D Imaging Systems

- 5.1.8 Microscopes And Trichoscopes

- 5.1.9 Skin Biopsy Diagnostics Instruments

- 5.1.10 Others

- 5.2 By Portability

- 5.2.1 Handheld/Pocket Dermatoscopes

- 5.2.2 Stationary/Fixed Dermatoscope

- 5.2.3 Trolley-Mounted/Tabletop Imaging Systems

- 5.2.4 Benchtop/Console RCM And OCT Systems

- 5.2.5 Others

- 5.3 By Application

- 5.3.1 Skin Cancer Diagnosis

- 5.3.1.1 Melanoma

- 5.3.1.2 Non-melanoma Skin Cancers

- 5.3.2 Pigmented Lesion Mapping & Longitudinal Monitoring

- 5.3.3 Inflammatory Skin Diseases

- 5.3.4 Hair & Scalp Disorders

- 5.3.5 Aesthetic & Dermatologic Surgery Planning/Documentation

- 5.3.6 Other Applications

- 5.3.1 Skin Cancer Diagnosis

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Dermatology Clinics & Centers

- 5.4.3 Primary Care & Ambulatory Care Centers

- 5.4.4 Academic & Research Institutes

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Canfield Scientific, Inc.

- 6.3.2 Cortex Technology (DermaLab)

- 6.3.3 Damae Medical (deepLive LC-OCT)

- 6.3.4 DermaSensor Inc.

- 6.3.5 DermLite

- 6.3.6 DermoScan GmbH

- 6.3.7 FotoFinder Systems GmbH

- 6.3.8 HEINE Optotechnik GmbH & Co. KG

- 6.3.9 ILLUCO Corporation Ltd.

- 6.3.10 Kirchner & Wilhelm GmbH + Co. KG

- 6.3.11 MedX Health Corp.

- 6.3.12 MetaOptima Technology (DermEngine)

- 6.3.13 Michelson Diagnostics Ltd. (VivoSight)

- 6.3.14 Optilia Instruments AB

- 6.3.15 SciBase

- 6.3.16 VivaScope GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment