|

시장보고서

상품코드

2063481

재생 실험실 장비 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Refurbished Laboratory Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

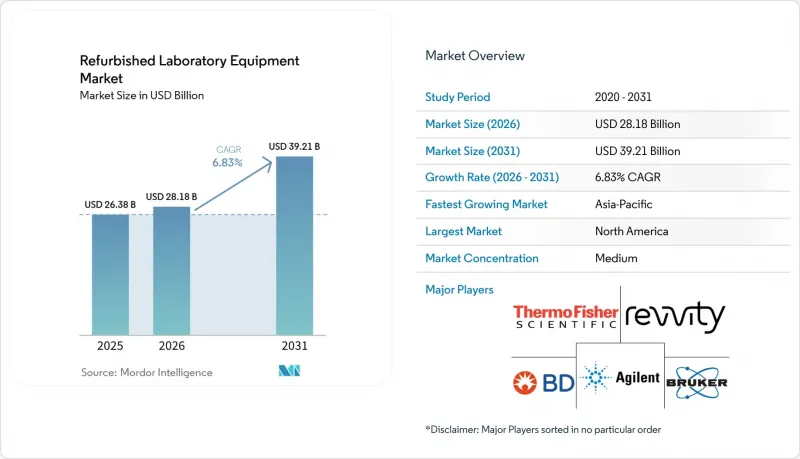

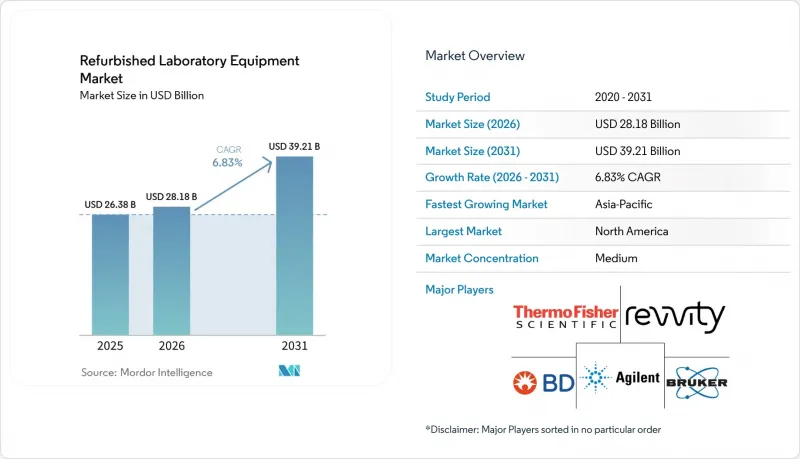

Mordor Intelligence에 의하면, 재생 실험실 장비 시장 규모는 2025년 263억 8,000만 달러로 평가되었습니다. 2026년에는 281억 8,000만 달러로 확대되어 2026-2031년 CAGR은 6.83%를 나타내, 2031년에는 392억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(분석 기기, 일반 실험실 기기 등), 최종 사용자(제약·바이오기술 기업 등), 판매 채널(OEM 인증 중고 프로그램 등), 재생 등급(OEM 공장 인증 등) 및 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계의 재생 실험실 장비 시장 동향 및 인사이트

예산에 제약이 있는 연구소나 스타트업 기업을 위한 비용 대비 효과가 높은 조달

학술 기관, 진단 기관, 수탁 조사 기관 등 예산에 민감한 구매자들은 신규 구매 대신, 더 낮은 도입 비용으로 처리 용량 요구 사항을 충족시키는 인증된 리퍼비시 장비로 자금을 전환하고 있으며, 이를 통해 소모품, 인력, 검증에 대한 자금 재분배가 가능해집니다. 공공 기관 및 NGO의 구매 담당자들은 자산의 유휴화나 특정 공급업체에 대한 종속을 피하기 위해, 다년간의 관점에서 교정, 부품의 입수 가능성, 시약의 물류, 서비스 이용 편의성을 중시하는 총소유비용(TCO)의 관점에서 의사결정을 내리고 있습니다. 구매자들이 예측 가능한 가동 시간과 감사 가능한 기록을 요구하는 가운데, 교정 추적성 및 출하 전 검증 정보를 공개하는 공급업체가 우선적으로 선정되고 있습니다. 공급 측면에서는 공장에서의 검사와 신제품과 동등한 보증을 제공하는 인증 재생 프로그램을 통해 신제품 시스템과의 성능 차이에 대한 인식이 줄어들고 있습니다. 문서화된 환경 부하 저감 실적과 미리 구성된 스타트업 번들을 제공하는 마켓플레이스의 전문 업체들은 신속한 가동을 원하는 인큐베이터나 초기 단계의 연구소에 대한 매력을 높이고 있습니다. 그 대표적인 예로, 규제 대상 워크플로우에서 규정 준수에 부합하는 가동을 지원하기 위해 순정 부품을 사용한 다항목 검사, 완전 보증, 현장 설치를 명시하는 공급업체의 프로그램을 들 수 있습니다. 또한, 예산에 민감한 연구소에서는 감사에 대응할 수 있는 기록을 유지하기 위해, 국가 계량 기관에 추적 가능한 교정 증명서를 활용하여 공급업체의 주장을 검증하고 있습니다.

제약·바이오기술 분야의 연구개발 확대 : 장비 수요 증가

바이오의약품 분야의 연구 개발이 활발해짐에 따라 LC-MS, 크로마토그래피 시스템, 하이컨텐츠 이미징 플랫폼의 도입이 증가하고 있으며, 이러한 장비들은 향후 포트폴리오 갱신 시 트레이드인 또는 인증 재판매 대상이 됩니다. M&A 및 포트폴리오 재편으로 인해 폐기 주기가 늘어나면서, 고가치가 있는 장비들이 재생·재판매 파이프라인으로 유입되고 있습니다. 대부분의 경우, 구매자의 부담을 덜어주기 위해 철거 및 물류 서비스가 패키지로 제공됩니다. 주요 OEM 기업들은 고객 관계를 강화하고, 자산 수명 주기 전반에 걸쳐 설치된 장비군에 대한 접근성을 확대하기 위해 엔드투엔드 역량과 파트너십에 대한 투자를 지속하고 있습니다. 인도의 Vigyan Dhara는 2025-26 회계연도에 연구개발(R&D) 예산을 확대하고 장비 보조금을 지원함으로써 지역 내 설치 기반을 확대하고, 향후 자금 조달 기간 동안의 갱신 주기를 확립하고 있습니다. 바이오의약품 업계 수요에 부응하는 OEM을 통한 인수 및 생산 능력 확대는 장비 사용이 지속되고 있음을 시사하며, 고객이 보유 장비를 최신 모델로 교체함에 따라 중고 유통 채널을 활성화시키고 있습니다. ISO 13485 및 FDA의 QMSR 요건을 둘러싼 규제 조화를 통해 교정 및 문서화가 더욱 체계화되었으며, 이에 따라 재생업체에 대한 요구 수준이 높아지는 한편, 적절하게 문서화된 제품 및 서비스에 대한 구매자의 신뢰도 높아지고 있습니다.

일관되지 않은 재생 기준으로 인한 정확도, 신뢰성 및 보정에 대한 우려

교정 기준이 제각각인 경우, 특히 엄격한 측정 관리에 의존하는 FDA, ISO 및 CLIA의 요건을 충족해야 하는 실험실에서는 교정의 품질이 여전히 가장 큰 우려 사항으로 남아 있습니다. 최근 연방 정부가 발송한 부적합 통지서에서는 교정상의 미비 사항이 빈번히 지적되고 있으며, 이로 인해 공급업체의 프로세스에 통합된 추적성, 불확실성의 허용 범위 및 환경 관리에 대한 구매자의 심사가 더욱 엄격해지고 있습니다. ISO 13485 및 ISO/IEC 17025의 틀에서는 제품 수명 주기 전반에 걸쳐 제품 품질을 유지하기 위해, 국가 계량 기관에 대한 문서화된 교정 체인, 정의된 허용 오차 및 허용 오차 초과 사례에 대한 조사가 요구됩니다. FDA의 품질 시스템 요건 역시 정의된 교정 주기와, 장비 상태를 검사된 배치나 시료와 연계하는 기록을 중시하고 있으며, 이에 따라 재생업체는 도입 첫날부터 감사 가능한 문서를 제공해야 합니다. CLIA 및 관련 지침은 시약 로트 변경이나 유지보수 등 정기적인 검증을 유발하는 요인을 강화하고 있으며, 이에 따라 임상 워크플로우에 도입되는 리퍼비시 기기에 대한 신뢰할 수 있는 서비스 접근의 중요성이 커지고 있습니다. 검사실은 NIST 또는 BIPM에 추적 가능한 교정 증명서, 검증된 소프트웨어 버전, 그리고 교정 시의 환경 조건이 문서화되어 있는 공급업체를 표준화함으로써 이러한 제약을 완화하고 있습니다.

부문별 분석

2025년, 재생 실험실 장비 시장에서 분석 장비는 매출의 42.17%를 차지했습니다. 이는 신약 개발 및 품질 관리(QC) 워크플로우 전반에 걸쳐 사용되는 LC-MS, GC, 분광 분석 시스템에 대한 지속적인 수요를 반영하고 있습니다. 조달 팀은 최신 세대의 장비를 트레이드인 프로그램에 포함시키는 경향을 점점 더 강화하고 있으며, 이를 통해 공장 검사 기록, 펌웨어 업데이트 및 동등한 보증이 적용된 인증된 LC-MS 플랫폼이 제공됩니다. 이로 인해 규제 대상 용도 분야에서 이 카테고리에 대한 신뢰도가 높아지고 있습니다. 판매업체가 수개월간의 보증, 추적 가능한 교정 및 설치 서비스를 제공함으로써 잔존 가치가 강화되는 한편, 구매자는 서비스 수준 및 예방 정비 계획을 통해 가동 시간에 대한 기대치를 명확히 하고 있습니다. ISO 13485 및 ISO/IEC 17025를 준수하는 교정 문서는 제약 품질 관리(QC) 및 CLIA 환경에 재생 분석 시스템을 도입하는 데 있어 여전히 핵심적인 역할을 수행하고 있으며, 이는 OEM 인증 장치와 비인증 대체품 간의 가격 차이에 영향을 미치고 있습니다. 연구소에서 구형 운영 체제나 소프트웨어 버전을 단종할 경우, 출하 시 검증된 소프트웨어 상태를 제공하는 공급업체는 도입 과정의 마찰을 줄이고 규정 준수 승인을 신속하게 처리할 수 있습니다. 이러한 요인들이 복합적으로 작용하여, 재생 실험실 장비 시장에서 분석 장비 부문의 선도적 입지를 공고히 하고 있습니다.

일반 실험 기기는 학술, 병원, 산업 분야의 각 연구소에서 폭넓게 활용되고 있다는 점을 바탕으로, 2031년까지 연평균 성장률(CAGR) 7.43%로 시장이 확대되어 가장 빠르게 성장하는 제품 카테고리가 될 것으로 전망됩니다. 이 부문과 관련된 리퍼비시 실험실용 장비 시장 규모는 실험실 인증 요건을 충족할 수 있는 원심분리기, 인큐베이터, 생물안전 캐비닛, 저울 및 액체 처리 시스템을 신속하게 확보할 수 있다는 점에서 혜택을 보고 있습니다. 수요는 에너지 및 소모품 사용량을 줄여주는 모듈식 자동화 장비와 지속가능성 대응 장비에 힘입어 증가하고 있으며, 이러한 장비들은 순환형 조달 목표와 부합합니다. 판매업체들은 보증 범위가 넓다는 점과, 감사 대상 환경에서 신속하게 가동을 시작할 수 있도록 하는 문서화된 IQ/OQ/PQ 시험 기록을 첨부하여 출하할 수 있는 역량을 바탕으로 차별화를 꾀하고 있습니다. 구매자들은 제한된 예산 내에서 새로운 실험실을 구축하거나 기존 시설을 확장하기 위해, 재생 일반 장비에 스타트업 키트나 교육을 세트로 제공하는 경우가 늘고 있습니다. 선정의 주요 기준은 여전히 문서의 품질과 일관성이지만, 교정 과정의 추적 가능성과 명확한 서비스 경로가 의사 결정의 속도와 확신을 높여주고 있습니다. 이러한 추세가 재생 실험실 장비 시장에서 일반 장비의 지속적인 성장을 뒷받침하고 있습니다.

제약 및 생명공학 기업들은 연구개발 투자를 통해 개발 및 품질 관리(QC)의 모든 단계에서 LC-MS, 크로마토그래피, 하이컨텐츠 이미징 플랫폼의 활용도가 높아짐에 따라, 2025년 매출의 32.28%를 차지했습니다. 새로운 분석 기법이 신약 개발 및 분석 분야의 장비 수요를 확대하는 가운데, 활발한 중고 장비 임베디드 및 업그레이드 주기로 인해 유지보수가 잘 된 자산이 유통 시장에 공급되고 있습니다. 의약품 제조 및 서비스에 부합하는 OEM 파트너십과 생산 능력 확충은 1차 판매부터 최종 인증 재판매에 이르는 장비 수명 주기를 강화하고 있습니다. 바이오프로세스 및 분석 워크플로우에 대한 투자는 계속해서 도입 기반을 형성하고 있으며, 이러한 장비들은 이후 품질이 검증된 제품으로 중고 실험 장비 시장에 공급됩니다. 제약 기업 구매처와 연계된 재생 실험실 장비 시장 점유율은 감사 및 인증 요건을 충족한다는 보증의 동등성과 공장 내 검증 절차를 통해 지속적으로 뒷받침되고 있습니다. 이러한 요소들로 인해, 문서화, 교정 추적성 및 서비스 대응 시간이 입증된 비 GxP 환경이나 특정 GxP 환경에서 리퍼비시 장비의 도입이 현실적인 선택지가 되고 있습니다.

학술·연구 기관은 공공 프로그램을 통한 실험실 규모 확대와 실무 중심 인프라 구축에 우선순위를 두면서, 2031년까지 연평균 성장률(CAGR) 8.56%로 가장 빠르게 성장할 것으로 전망됩니다. 인도의 ‘Vigyan Dhara’ 기금은 각 기관의 장비 도입을 지원하고 있으며, 이를 통해 인증된 재생 시스템에 대한 단기적인 수요가 증가하고, 향후 2차 공급을 위한 다년간의 교체 주기가 확립됩니다. 새로 설립된 국립계측센터와 산학협력 허브에서는 대사체학, 분자생물학, 특성 평가 기능이 도입되어 있으며, 대부분의 경우 도입 및 교육을 신속하게 진행할 수 있는 재생 키트가 활용되고 있습니다. 학술 기관의 조달 팀은 인증 기준 및 보조금 보고 요건을 준수하는 동시에 장비의 가동 시간을 극대화하기 위해 교정 문서, 설치 및 교육 서비스를 중시하고 있습니다. 보증 범위, 스타트업 번들, 서비스 계약을 결합한 공급업체는 교육 및 연구 실험실에서의 신속한 도입과 장기적인 활용을 지원합니다. 이러한 요인들이 재생 실험실 장비 시장의 급성장 중인 학술 부문을 뒷받침하고 있습니다.

지역별 분석

북미는 2025년 재생 실험실 장비 시장의 매출의 36.74%를 차지했습니다. 이는 제약 및 생명공학 산업이 밀집해 있다는 점과 중고 장비 유통 채널이 성숙해 있다는 점에 힘입은 것입니다. 연방 정부 및 인증 체계는 ISO/IEC 17025를 준수하는 교정 서비스 제공업체를 권장하고 있으며, 이는 문서화된 재현 프로세스와 추적성 기준에 대한 수요를 촉진하고 있습니다. 각 OEM 업체들은 라이프사이클 지원을 강화하고, 장비 교체 시 인증된 재판매 경로를 명확히 제시하기 위해 미국 내 제조 및 서비스 파트너십을 지속적으로 심화하고 있습니다. 엄격한 규제와 보증 내용의 동등성을 요구하는 구매자들의意向에 따라, 이 지역에서는 여전히 트레이드인 프로그램이나 제조업체 인증 중고 기기 제공이 주류를 이루고 있습니다. 브로커와 딜러는 폭넓은 재고와 유연한 보증을 통해 OEM 유통 채널을 보완하고 있는 반면, 학술 컨소시엄은 실험실을 신속하게 구축하기 위해 미리 구성된 키트를 조달하고 있습니다. 이러한 요소들이 재생 실험실 장비 시장에서 해당 지역의 선도적 지위와 꾸준한 보급을 뒷받침하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.90%를 나타낼 것으로 예측되며, 이는 재생 실험실 장비 시장에서 각 지역 중 가장 높은 성장률입니다. 대학 및 국립 연구소의 확장에 따라 중점 분야의 처리 능력이 강화되고 있으며, 주요 국가의 공공 프로그램에서는 연구 인프라 및 인재 양성을 위해 자금이 투입되고 있습니다. 인도의 ‘Vigyan Dhara’ 프로그램에 대한 예산 배정은 이러한 추세를 상징하며, 대학 및 연구 기관 전반에 걸쳐 신제품과 리퍼비시 제품 모두에 대한 수요 파이프라인을 창출하고 있습니다. 또한, 각 지역의 허브에는 향후 2차 공급 채널에 대응할 수 있는 도입 기반을 구축하는 첨단 계측 기기 센터가 마련되어 있습니다. 장비의 도입 세대가 성숙기에 접어들고 교체 주기가 시작됨에 따라, OEM을 통한 중고 제품 임베디드 및 공인 리퍼비시 제품 프로그램은 아시아태평양에서 더욱 확대될 것으로 예측됩니다. 해당 지역의 구매자들은 인증 및 데이터 무결성 요건을 준수하기 위해 서류 준비 현황, 서비스 이용 편의성, 그리고 소프트웨어 검증 지원을 중요하게 여기고 있습니다. 이러한 추세는 재생 실험실 장비 시장에서 해당 지역의 지속적인 호조를 뒷받침하고 있습니다.

유럽에서는 엄격한 품질 및 안전 규제로 인해 리퍼비시 기기에 대한 문서화 요건이 표준화되어 있어, 리퍼비시 연구소용 기기 시장에서 여전히 큰 점유율을 유지하고 있습니다. 규제 대상 기기의 대대적인 재생과 관련된 CE 마킹 요건은 규정 준수 장벽을 높이는 한편, 회원국 간 품질 표준화를 통해 구매자의 불확실성을 줄여주고 있습니다. 주요 OEM 기업들은 유럽 내 제조 및 서비스 거점에 대한 투자를 지속하고 있으며, 이를 통해 사용 수명이 끝난 장비의 수명 주기 관리와 인증된 재판매 경로가 뒷받침되고 있습니다. 보다 광범위한 지속가능성 노력을 통해 기관들은 자산의 수명을 연장하고, 환경적 이점이 입증 가능한 재생 및 회수 옵션을 중시하는 순환형 조달 규정을 채택하도록 장려받고 있습니다. 이러한 동향들이 맞물려, 유럽의 규제 대상 워크플로우 및 ESG 방침에 부합하는 문서화된 재생 시스템에 대한 지속적인 수요를 뒷받침하고 있습니다.

중동 및 아프리카 및 남미에서는 정부와 대학이 연구·시험 역량을 확충함에 따라 리퍼비시드 실험실용 장비 시장이 확대되고 있습니다. 수천 개의 기관을 연결하는 국경을 초월한 디지털 인프라가 과학 프로그램용 장비 수요를 촉진하고 있으며, 이로 인해 도입 규모가 확대되고, 향후 중고 유통 채널로 재활용될 것입니다. 연구 지원 역량을 강화하고 장비 이용을 촉진하는 민관 협력 프로그램은 장비 접근성을 개선하고 자원 공유 모델을 지원하고 있습니다. 이 지역의 구매자들은 현지에서 이용할 수 있는 서비스 옵션이 제한적인 상황에서 가동 시간을 유지하기 위해 신뢰성, 교정 추적성 및 교체 부품의 확보 가능성을 최우선으로 고려하고 있습니다. 원격 지원, 문서화된 설치 절차, 명확한 보증 조건을 제공하는 브로커나 OEM은 도입을 가속화할 수 있는 유리한 입장에 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the refurbished laboratory equipment market size is expected to grow from USD 26.38 billion in 2025 to USD 28.18 billion in 2026 and is forecast to reach USD 39.21 billion by 2031 at 6.83% CAGR over 2026-2031.

This report is Segmented by Product Type (Analytical Instruments, General Laboratory Equipment, and More), End User (Pharmaceutical & Biotechnology Companies, and More), Sales Channel (OEM Certified Pre-Owned Programs, and More), Refurbishment Grade (OEM Factory-Certified, and More), and Geography (North America, Europe, and More). The Market and Forecasted in Terms of Value (USD).

Global Refurbished Laboratory Equipment Market Trends and Insights

Cost-Effective Procurement for Budget-Constrained Labs and Startups

Budget-sensitive buyers spanning academia, diagnostics, and contract research redirect capital from new purchases to certified refurbished instruments that meet throughput needs at lower acquisition cost, which allows funds to be reallocated to consumables, personnel, and validation. Public buyers and NGOs frame decisions through total cost of ownership lenses that weigh calibration, parts availability, reagent logistics, and service access over multi-year horizons to avoid idle assets and procurement lock-ins. Vendors that publish calibration traceability and pre-shipment validation gain preference as buyers seek predictable uptime and auditable records. On the supply side, certified refurbishment programs with factory inspection and warranty parity narrow the perceived performance gap compared with new systems. Marketplace specialists that provide documented environmental savings and configured startup bundles strengthen appeal to incubators and early-stage labs seeking rapid commissioning. Case-in-point examples include vendor programs that disclose multi-point inspections with genuine parts, full warranty, and on-site installation to support compliant go-live in regulated workflows. Budget-conscious labs also validate supplier claims against calibration certificates traceable to national metrology bodies to maintain audit-ready records.

Expansion of Pharma and Biotech R&D Increasing Instrument Demand

Rising biopharma R&D intensity increases deployments of LC-MS, chromatography systems, and high-content imaging platforms, which later become candidates for trade-in or certified resale during portfolio upgrades. M&A and portfolio shifts add to decommissioning cycles that release high-value instruments into refurbishment pipelines, often bundled with removal and logistics services to reduce buyer friction. Large OEMs continue to invest in end-to-end capabilities and partnerships that reinforce customer relationships and expand access to installed equipment fleets over the asset lifecycle. India's Vigyan Dhara expanded R&D allocations in 2025-26, supporting equipment grants that add to regional installed bases and set up refresh cycles over subsequent funding windows. OEM acquisitions and capacity expansions that align with biopharma demands signal sustained instrument utilization and repower secondary channels as customers modernize fleets. Regulatory convergence around ISO 13485 and FDA QMSR expectations further codifies calibration and documentation, which raises the bar for refurbishers and increases buyer trust in well-documented offerings.

Accuracy, Reliability, and Calibration Concerns from Non-Uniform Refurb Standards

Calibration quality remains a top concern when refurbishment standards vary, especially where labs must meet FDA, ISO, and CLIA requirements that depend on tight measurement control. Federal letters of nonconformance in recent years have frequently referenced calibration gaps, which elevates buyer scrutiny of traceability, uncertainty budgets, and environmental controls embedded in vendor processes. ISO 13485 and ISO/IEC 17025 frameworks expect documented calibration chains to national metrology bodies, defined tolerances, and investigation of out-of-tolerance events to maintain product quality across the lifecycle. FDA quality system requirements also emphasize defined calibration intervals and records that link instrument status to batches or samples tested, which pushes refurbishers to provide auditable documentation from day one. CLIA and related guidance reinforce periodic verification triggers such as reagent-lot changes and maintenance events, which increase the importance of reliable service access for refurbished units placed in clinical workflows. Labs mitigate this restraint by standardizing on vendors that provide calibration certificates traceable to NIST or BIPM, validated software versions, and environmental conditions documented at the time of calibration.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability and Circular Economy Policies Accelerating Reuse

- Growth of Academic and Research Capacity in Emerging Economies

- Limited Warranty/After-Sales Support and Lack of Process Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Analytical Instruments captured 42.17% of revenue in 2025 within the refurbished laboratory equipment market, reflecting sustained demand for LC-MS, GC, and spectroscopy systems used across discovery and QC workflows. Procurement teams increasingly channel late-generation instruments into trade-in programs that return certified LC-MS platforms with documented factory inspection, firmware updates, and parity warranties, which strengthens trust in this category for regulated uses. Residual value is reinforced by sellers that provide multi-month warranties, traceable calibration, and installation services, while buyers formalize uptime expectations through service tiers and preventive maintenance plans. Calibration documentation aligned to ISO 13485 and ISO/IEC 17025 remains central to placing refurbished analytical systems in pharma QC and CLIA environments, which influences price premiums for OEM-certified units over non-certified alternatives. Where labs retire legacy operating systems or software versions, sellers that provide validated software states at shipment reduce commissioning friction and speed compliance sign-offs. These factors collectively reinforce category leadership for analytical instruments in the refurbished laboratory equipment market.

General Laboratory Equipment is forecast to be the fastest-growing product category at a 7.43% CAGR through 2031, supported by broad applicability across academic, hospital, and industrial labs. The refurbished laboratory equipment market size tied to this segment benefits from quick-turn availability of centrifuges, incubators, biosafety cabinets, balances, and liquid handling systems that can be certified to lab accreditation requirements. Demand is reinforced by modular automation and sustainability-aligned equipment that reduces energy or consumables usage, which aligns with circular procurement objectives. Sellers differentiate through warranty breadth and ability to ship with documented IQ/OQ/PQ test records for rapid go-live in audited environments. Buyers increasingly bundle refurbished general equipment with startup kits and training to stand up new labs or expand existing facilities on constrained budgets. Documentation quality and consistency remain the primary selection criteria, with calibration traceability and defined service routes improving decision speed and confidence. These dynamics support sustained expansion for general equipment in the refurbished laboratory equipment market.

Pharmaceutical & Biotechnology Companies represented 32.28% of 2025 revenue as R&D investment supported high utilization of LC-MS, chromatography, and high-content imaging platforms across development and QC. Active trade-in and upgrade cycles supply secondary channels with well-maintained assets as new modalities expand instrumentation needs in discovery and analytics. OEM partnerships and capacity additions that align to drug-product manufacturing and services strengthen the equipment lifecycle, from primary sale through eventual certified resale. Bioprocess and analytical workflow investments continue to shape installed bases, which later feed the refurbished laboratory equipment market with quality-documented units. The refurbished laboratory equipment market share tied to pharma buyers remains supported by warranty parity and factory validation that satisfy audit and accreditation requirements. These elements keep refurbished placements viable for non-GxP and selected GxP contexts where documentation, calibration traceability, and service response times are proven.

Academic & Research Institutes are projected to grow the fastest at an 8.56% CAGR through 2031 as public programs expand laboratory capacity and prioritize hands-on infrastructure. India's Vigyan Dhara funding supports instrumentation grants across institutions, which increases near-term demand for certified refurbished systems and sets multi-year refresh cycles for future secondary supply. New national instrumentation centers and university-industry hubs bring metabolomics, molecular, and characterization capabilities online, often with refurbished kits that speed commissioning and training. Procurement teams in academia weigh calibration documentation, installation, and training services to comply with accreditation and grant reporting while maximizing instrument uptime. Suppliers that combine warranty coverage, startup bundles, and service agreements support rapid adoption and long-term utilization in teaching and research labs. These drivers sustain the fast-growing academic cohort in the refurbished laboratory equipment market.

Geography Analysis

North America held 36.74% of 2025 revenue for the refurbished laboratory equipment market, supported by dense pharma and biotech clusters and mature secondary-equipment channels. Federal and accreditation frameworks favor ISO/IEC 17025-aligned calibration providers, which reinforces demand for documented refurbishment and traceability standards. OEMs continue to deepen U.S. manufacturing and services partnerships that strengthen lifecycle support and provide clear pathways to certified resale when fleets refresh. Trade-in programs and factory-certified refurbished offerings remain prominent in this region due to regulatory rigor and buyer preferences for warranty parity. Brokers and dealers complement OEM channels through inventory breadth and flexible warranties, while academic consortia source configured kits for rapid lab setups. These elements underpin regional leadership and steady adoption in the refurbished laboratory equipment market.

Asia-Pacific is projected to grow at an 8.90% CAGR through 2031, the fastest among regions in the refurbished laboratory equipment market. University and national lab expansions are adding capacity in priority fields, and public programs in major countries are directing funds toward research infrastructure and training. India's Vigyan Dhara allocation exemplifies this trend, creating a pipeline for both new and refurbished instruments across universities and institutes. Regional hubs are also building advanced instrumentation centers that will generate installed bases aligned to future secondary supply channels. As cohorts mature and upgrade cycles begin, OEM trade-in and certified refurbished programs are expected to scale further into Asia-Pacific. Buyers in the region focus on documentation readiness, service access, and software validation support to align with accreditation and data-integrity requirements. These developments support sustained regional outperformance in the refurbished laboratory equipment market.

Europe maintains a significant share in the refurbished laboratory equipment market as stringent quality and safety regulations normalize documentation expectations for refurbished units. CE marking requirements for substantial refurbishment of regulated devices raise compliance thresholds but also reduce uncertainty for buyers by standardizing quality across member states. Leading OEMs continue to invest in European manufacturing and service footprints, which supports lifecycle management and certified resale pathways for instruments that exit primary service. Broader sustainability initiatives motivate institutions to extend asset life and adopt circular procurement rules that value refurbishment and take-back options with provable environmental benefits. Collectively, these dynamics support durable demand for documented refurbished systems that fit regulated workflows and ESG policies in Europe.

In the Middle East and Africa and in South America, the refurbished laboratory equipment market advances as governments and universities build out research and testing capacity. Cross-border digital infrastructure that connects thousands of institutions is catalyzing equipment demand for scientific programs, which expands installed bases that later recycle into secondary channels. Public-private programs that strengthen research-granting capacity and promote equipment utilization are improving access to instruments and supporting shared resource models. Buyers in these regions prioritize reliability, calibration traceability, and access to replacement parts to sustain uptime with limited local service options. Brokers and OEMs that provide remote support, documented installation, and clear warranty terms are positioned to accelerate adoption.

- Agilent Technologies

- American Laboratory Trading (ALT)

- Beckton Dickinson

- Bruker

- Cambridge Scientific Products

- Carl Zeiss

- Copia Scientific

- EquipNet, Inc.

- GenTech Scientific LLC

- International Equipment Trading Ltd. (IET)

- IRIS Industries

- Marshall Scientific LLC

- Mettler Toledo

- Revvity, Inc.

- Richmond Scientific (UK)

- Sartorius

- Siemens Healthineers

- Surplus Solutions LLC

- Thermo Fisher Scientific

- Waters Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-Effective Procurement for Budget-Constrained Labs and Startups

- 4.2.2 Expansion of Pharma and Biotech R&D Increasing Instrument Demand

- 4.2.3 Sustainability and Circular Economy Policies Accelerating Reuse

- 4.2.4 Growth of Academic and Research Capacity in Emerging Economies

- 4.2.5 OEM Certified Pre-Owned and Trade-In Programs De-Risk Purchases

- 4.2.6 Lab Closures, M&A, and Decommissioning Fueling High-Quality Secondary Supply

- 4.3 Market Restraints

- 4.3.1 Accuracy, Reliability, and Calibration Concerns from Non-Uniform Refurb Standards

- 4.3.2 Limited Warranty/After-Sales Support and Lack of Process Standardization

- 4.3.3 OEM Software Licensing/EoL Support Restrictions Limiting Redeployment

- 4.3.4 Parts Obsolescence and Validation Costs for Regulated Workflows

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 Product Type

- 5.1.1 Analytical Instruments

- 5.1.2 General Laboratory Equipment

- 5.1.3 Life Science Equipment

- 5.1.4 Clinical Diagnostic Equipment

- 5.2 By End User

- 5.2.1 Pharmaceutical & Biotechnology Companies

- 5.2.2 Academic & Research Institutes

- 5.2.3 Clinical & Diagnostic Laboratories

- 5.2.4 Contract Research Organizations (CROs)

- 5.2.5 Hospitals & Healthcare Facilities

- 5.3 By Sales Channel

- 5.3.1 OEM Certified Pre-Owned Programs

- 5.3.2 Independent Refurbishers/Dealers

- 5.3.3 Online Marketplaces & Auctions

- 5.4 By Refurbishment Grade

- 5.4.1 OEM Factory-Certified

- 5.4.2 Third-Party Reconditioned

- 5.4.3 As-Is/Lightly Used with Warranty

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Agilent Technologies, Inc.

- 6.3.2 American Laboratory Trading (ALT)

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Bruker Corporation

- 6.3.5 Cambridge Scientific Products

- 6.3.6 Carl Zeiss AG

- 6.3.7 Copia Scientific

- 6.3.8 EquipNet, Inc.

- 6.3.9 GenTech Scientific LLC

- 6.3.10 International Equipment Trading Ltd. (IET)

- 6.3.11 IRIS Industries

- 6.3.12 Marshall Scientific LLC

- 6.3.13 Mettler-Toledo International Inc.

- 6.3.14 Revvity, Inc.

- 6.3.15 Richmond Scientific (UK)

- 6.3.16 Sartorius AG

- 6.3.17 Siemens Healthineers AG

- 6.3.18 Surplus Solutions LLC

- 6.3.19 Thermo Fisher Scientific, Inc.

- 6.3.20 Waters Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment