|

시장보고서

상품코드

2063512

아유르베다 센터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Ayurveda Centers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

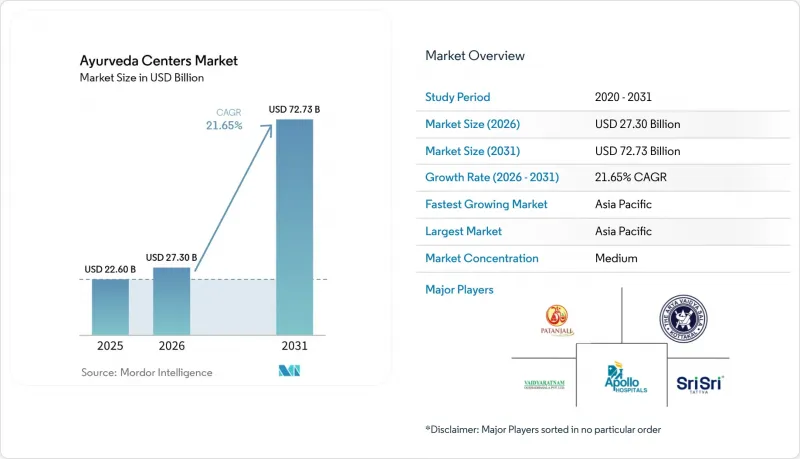

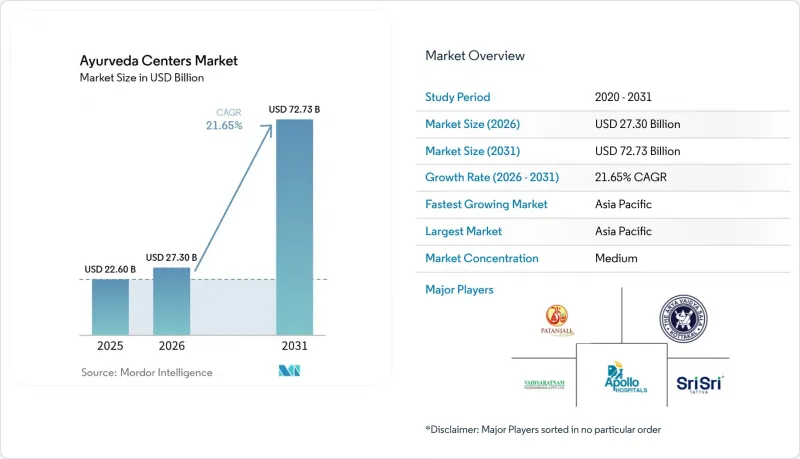

Mordor Intelligence에 의하면, 아유르베다 센터 시장 규모는 2025년 226억 달러로 평가되었습니다. 2026년 273억 달러에서 2031년까지 727억 3,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 21.65%를 나타낼 것으로 예측됩니다.

본 보고서는 시설 유형(독립형 외래 클리닉, 아유르베다 병원(입원), 판차카르마 데이케어 센터 등), 서비스 라인(외래 진료·의약품, 판차카르마 디톡스/회춘 프로그램, 만성 질환 관리·재활 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 아유르베다 센터 시장 동향 및 인사이트

IRDAI의 보험 적용 확대가 보험 수요를 촉진

2024년 1월 인도 정부의 지침에 따라 아유르베다, 요가, 우나니, 시다, 동종요법에 대한 보험 적용이 의무화되었으며, 기존에 무현금 환급 대상에서 제외되었던 상황이 해소되었습니다. 27개 보험사가 AYUSH(아유르베다, 요가, 우나니, 시드다, 동종요법)를 포함한 상품을 출시하고 있지만, 대다수의 병원에서 표준화된 진료 코드나 전자 차트가 정비되어 있지 않아 보험금 청구 거부가 여전히 빈번하게 발생하고 있습니다. 체계적인 문서 관리에 투자하고 있는 NABH 인증 센터는 이미 신속한 승인 절차와 환자 수 증가를 확보하고 있습니다. 아유슈부는 NABH의 지원을 받아 전국적으로 청구 내용을 표준화할 통일된 분류 체계를 마련하고 있습니다. 중기적으로는 이 지침에 따라 본인 부담 디톡스 비용이 보험 적용 의료비로 전환됨에 따라, 도시 지역 소비자들의 가격에 대한 거부감이 줄어들 것으로 예측됩니다.

AYUSH 비자 및 의료 관광 촉진

인도는 2024년에 411건의 전용 아유르베다 비자를 발급했으며, 2025년 초까지 누적 발급 건수는 1,600건을 넘어섰습니다. 이에 따라 케랄라 주에서만 월 3억-4억 루피(317만-423만 달러)의 아유르베다 관광 수입이 예상됩니다. 스리랑카의 리조트 시설에 따르면, 외국인 관광객의 80%가 일반 관광 비자로 허용되는 기간보다 더 긴 체류를 필요로 하고 있어, 이 제도의 중요성이 부각되고 있습니다. 단기적인 성장은 케랄라주와 카르나타카주에 집중되어 있으며, 영어에 능통한 임상의들과 유서 깊은 리조트들이 문화적 마찰을 완화하고 있습니다. 중기적으로는 항공사 및 호텔 체인과의 마케팅 제휴를 통해 인바운드 관광객 수가 3배로 늘어날 것으로 예측됩니다. 또한, 이 비자는 해외 규제 당국의 관점에서 아유르베다를 정당화하는 것이며, 양국 간의 인증 협상을 원활하게 하는 역할을 합니다.

지극히 세분화된 의료 제공 체계와 표준화의 부족

인도의 3,844개 병원과 36,848개 진료소는 그 계보, 치료 철학, 기록 관리 관행 면에서 크게 다릅니다. 2025년 시점에서 정부 지원을 받는 통합병원 167곳 중 운영 중이던 곳은 고작 52곳에 불과했으며, 이로 인해 공급 병목 현상이 더욱 심화되고 있습니다. 통일된 임상 프로토콜이 없기 때문에 보험사는 예측 불가능한 비용에 직면해 있으며, 규제가 미흡한 진료소에서 발생하는 유해 사건은 평판이 연쇄적으로 악화될 위험을 초래할 수 있습니다. 인증 제도는 통합을 촉진하지만, 프로토콜화에 대한 인식론적 저항이 표준화의 진전을 늦추고 있습니다. 이러한 분할 현상은 복잡한 증례가 소수의 고급 의료 센터에 집중됨으로써 성장을 저해하고, 소규모 의료 기관에는 수익성이 낮은 급성기 의료만 남게 됩니다.

부문별 분석

2025년, 판차카르마 당일 치료 센터는 시설 수익의 45.12%를 차지했습니다. 이는 90분에서 120분 정도의 치료가 보험 규정에 부합하며, 도심 지역 환자들의 바쁜 일정에도 잘 맞출 수 있기 때문입니다. 그럼에도 불구하고, 가장 빠른 성장이 예상되는 분야는 웰니스 리트리트와 리조트입니다. 부유층 여행객들이 디톡스 치료와 요가, 명상, 사트빅 식단을 결합한 2주짜리 패키지에 6,000-1만 2,000달러를 지불함에 따라, 2031년까지의 연평균 성장률(CAGR)은 23.14%를 나타낼 것으로 예측됩니다. 이 분류에서 두 가지 명확한 전략이 드러납니다. 아폴로 아유르베이드(Apollo AyurVAID)가 2024년 285병상에서 2028년까지 1,000병상으로 규모를 확대한 데일리케어 센터는 퇴행성 관절염이나 대사증후군 등의 질환에 대해, 장기 입원과 동등한 임상 성과를 유지하면서도, 많은 환자 수와 1회당 낮은 비용에 중점을 두고 있습니다.

풀서비스 아유르베다 병원은 수익의 상당 부분을 차지하고 있으며, 주로 14일에서 28일간의 경과 관찰이 필요한 복잡한 증례를 다루고 있습니다. 파탄잘리 요그피트에 새로 설립된 250병상 규모의 종합병원은 중환자실과 아유르베다가 급성기 치료 후 재활 과정에서 어떻게 협력할 수 있는지를 보여주고 있습니다. 독립 외래 클리닉 시장 점유율은 낮은 편이며, 보험사가 환자를 지정 네트워크로 유도함에 따라 압박을 받고 있습니다. 이로 인해 소규모 사업자들은 안과 등 틈새 분야로 밀려나고 있으며, 이것이 Sreedhareeyam의 22개 지점으로 구성된 안과 진료 체인의 핵심 사업 분야가 되고 있습니다.

지역별 분석

아시아태평양은 2025년에 아유르베다 센터 시장 매출의 79.02%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 22.13%를 나타낼 전망입니다. 인도는 2026년도 예산에서 3개의 새로운 전국 아유르베다 연구소와 5개의 지역 허브에 450억 루피(4억 7,550만 달러)를 배정하여 공급 체계를 강화하고 있는 반면, 케랄라주에는 250개 이상의 NABH 인증 기관이 있어 의료 관광객을 끌어모으는 자석 역할을 하고 있습니다. 스리랑카에는 40개국 이상에 수출하는 GMP 인증 리조트가 조성되어 있으며, 외국인 관광객이 받는 판차카르마 시술의 대부분을 차지하고 있습니다. 현재 중국과 일본에서는 아유르베다가 도시 지역의 스파로 한정되어 있지만, 양국 간의 상호 인정 협상이 진전된다면 2027년 이후 대규모 성장이 기대됩니다. 호주에서는 엄격한 의료 제품 규제가 급속한 확장을 저해하고 있지만, 과학적 근거가 풍부한 제조업체에게는 독자적인 사업 기회가 열리고 있습니다.

북미는 전 세계 매출에서 차지하는 비중이 적습니다. 미국의 웰니스 관련 지출은 2019년 이후, 매년 대폭 증가하고 있지만, 대부분의 아유르베다 센터는 노스캐롤라이나주의 ‘더 라지’처럼 7박 판차카르마 패키지를 5,500-1만 2,843달러에 제공하는 소규모 자비 진료 클리닉 수준에 머물러 있습니다. 주별 면허 제도가 분절되어 있어 보험 적용이 제한되고 있으며, 이는 시장 침투율의 상한선이 되고 있습니다. 캐나다도 비슷한 상황이지만, 멕시코에서는 막 시작된 서비스가 주재원들 수요를 충족시키고 있습니다.

유럽에서는 독일이 ISO 9001 인증을 획득한 ‘유럽 아유르베다 아카데미’를 통해 성장을 주도하고 있으며, 이학 석사 과정과 외래형 디톡스 클리닉을 제공합니다. 영국에서는 국민보건서비스(NHS) 내에서 만성 통증에 대한 아유르베다 치료의 시범 도입이 진행되고 있지만, 보험 급여에 대해서는 여전히 조사 단계에 머물러 있습니다. 남유럽에서는 아유르베다를 스파 시설의 부가 서비스로 자리매김하고 있으며, 동유럽은 가처분 소득 증가에 따라 개척 가능성이 있는 미개척 시장입니다.

중동 및 아프리카에서는 아랍에미리트가 이미 2002년에 아유르베다를 승인했으며, 두바이에서는 현재 무현금 결제가 가능한 여러 클리닉이 인가를 받았습니다. 지나 시코 라이프케어가 153만 AED(42만 달러)에 ‘백 투 루츠 아유르베다’를 인수한 것은 해외 거주자들 수요에 대응함으로써 2025년까지 매출을 223% 성장시켰습니다. 남아프리카와 동아프리카에는 디아스포라(해외 거주자) 커뮤니티가 주도하는 규모는 작지만 성장 중인 네트워크가 존재합니다. 남미에서는 브라질과 아르헨티나가 엄격한 의약품 규제 하에 웰빙을 최우선으로 하는 센터를 운영하고 있습니다. 시장 확대는 현재 협상 중인 양자 간 인정 협정에 달려 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the ayurveda centers market size is projected to expand from USD 22.60 billion in 2025 and USD 27.30 billion in 2026 to USD 72.73 billion by 2031, registering a CAGR of 21.65% between 2026 to 2031.

This report is Segmented by Facility Type (Standalone OP Clinics, Ayurveda Hospitals (IPD), Panchakarma Day-Care Centers, and More), Service Line (OPD Consultations & Medicines, Panchakarma Detox/Rejuvenation Programs, Chronic Disease Management & Rehabilitation, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Ayurveda Centers Market Trends and Insights

IRDAI Parity Unlocking Insurance-Backed Demand

India's January 2024 directive mandates equal insurance coverage for Ayurveda, Yoga, Unani, Siddha, and Homeopathy, removing historical exclusion from cashless reimbursement. Twenty-seven insurers have launched AYUSH-inclusive products, yet claim rejection remains common because most hospitals lack standardized procedure codes and digital records. NABH-accredited centers that invest in structured documentation already secure faster approvals and higher patient inflows. The Ministry of Ayush, with NABH support, is drafting a unified taxonomy that will standardize claims nationwide. Over the medium term the directive is expected to convert out-of-pocket detox spending into insured medical expenditure, shrinking price resistance among urban consumers.

AYUSH Visa and Medical Value Travel Promotion

India issued 411 dedicated Ayush visas in 2024, and cumulative issuances topped 1,600 by early 2025, funneling an estimated INR 300-400 million (USD 3.17-4.23 million) in monthly Ayurveda tourism revenue to Kerala alone. Resorts in Sri Lanka report that 80% of international guests need stays longer than typical tourist visas allow, underscoring the scheme's importance. Short-term growth concentrates in Kerala and Karnataka, where English-proficient clinicians and heritage resorts reduce cultural friction. In the medium term, marketing alliances with airline and hotel chains are expected to triple inbound volumes. The visa also legitimizes Ayurveda in the eyes of regulators abroad, smoothing bilateral accreditation talks.

Highly Fragmented Provider Base and Limited Standardization

India's 3,844 hospitals and 36,848 dispensaries vary widely in lineage, therapeutic philosophy, and record-keeping practices. Just 52 of 167 government-supported integrated hospitals were operational in 2025, amplifying supply bottlenecks. Without uniform clinical protocols, insurers face unpredictable costs, and adverse events at poorly regulated clinics risk reputational contagion. Although accreditation drives consolidation, epistemological resistance to protocolization slows harmonization. The fragmentation trims growth by steering complex cases to a handful of premium centers, leaving smaller outlets with low-margin acute care.

Other drivers and restraints analyzed in the detailed report include:

- WHO Global Centre for Traditional Medicine Elevates Standards

- Rapid Growth in Global Wellness Tourism

- Sparse High-Quality Clinical Evidence for Many Indications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Panchakarma day-care centers generated 45.12% of facility revenue because their 90- to 120-minute therapies fit neatly into insurance rules and the busy schedules of urban patients. Still, the fastest growth is expected from wellness retreats and resorts, which are projected to expand at a 23.14% CAGR through 2031 as affluent travelers pay USD 6,000-12,000 for two-week packages that blend detox treatments with yoga, meditation, and sattvic meals. This split shows two clear strategies. Day-care centers, typified by Apollo AyurVAID's plan to scale from 285 beds in 2024 to 1,000 beds by 2028, focus on high patient volumes and low per-visit costs while maintaining clinical outcomes for conditions such as osteoarthritis and metabolic syndrome on par with those of longer stays.

Full-service Ayurveda hospitals account for a notable share of revenue, mainly treating complex cases that need 14- to 28-day supervision; Patanjali Yogpeeth's new 250-bed integrated hospital shows how critical-care units and Ayurveda can work together in post-acute rehabilitation. Stand-alone outpatient clinics hold a modest share and feel pressure as insurers steer patients toward accredited networks, pushing smaller operators toward niches such as ophthalmology-the focus of Sreedhareeyam's 22-center eye-care chain.

Geography Analysis

Asia-Pacific generated 79.02% of the Ayurveda centers market revenue in 2025 and will compound at 22.13% through 2031. India's 2026 budget allocation of INR 45,000 million (USD 475.5 million) for three new All India Institutes of Ayurveda and five regional hubs bolsters supply, while Kerala hosts more than 250 NABH-accredited institutions that act as magnets for medical tourists. Sri Lanka complements GMP-certified resorts that export to 40+ countries and report the majority of Panchakarma uptake among foreign guests. China and Japan currently restrict Ayurveda to urban spas, but bilateral recognition talks could unlock scaled growth post-2027. Australia's stringent therapeutic-goods rules hinder rapid expansion yet open differentiated opportunities for evidence-rich manufacturers.

North America delivers a modest share of global revenue. U.S. wellness spending has climbed significantly each year since 2019, but most Ayurveda centers remain boutique cash-pay clinics, such as The Raj in North Carolina, offering seven-night Panchakarma packages priced at USD 5,500-12,843. Fragmented state licensing limits insurance reimbursement, capping penetration. Canada mirrors this landscape, while Mexico's nascent offerings serve expatriate demand.

In Europe Germany anchors growth via the ISO 9001-certified European Academy of Ayurveda, providing Master of Science programs and ambulatory detox clinics. The United Kingdom pilots Ayurveda inside the National Health Service for chronic pain, though reimbursement remains research-bound. Southern Europe positions Ayurveda as a spa amenity, and Eastern Europe is an untapped frontier contingent on disposable-income gains.

In Middle East & Africa United Arab Emirates recognized Ayurveda as early as 2002, and Dubai now licenses multiple cashless-enabled clinics. Jeena Sikho Lifecare's AED 1.53 million (USD 0.42 million) acquisition of Back to Roots Ayurveda targets 223% revenue growth in 2025 by addressing expatriate demand. South Africa and East Africa house small but growing networks driven by diaspora communities. In South America, Brazil and Argentina operate wellness-first centers within tight pharmaceutical regulations. Market expansion depends on bilateral accreditation treaties that are still under negotiation.

- Amala Ayurvedic Hospital & Research Centre

- Apollo AyurVAID Hospitals

- Arya Vaidya Pharmacy

- Arya Vaidya Sala

- Ayushakti Ayurveda

- Barberyn Ayurveda Resorts

- CGH Earth Ayurveda

- Jeena Sikho Lifecare

- Jiva Ayurveda

- JSS Ayurveda Hospital

- Kairali Ayurvedic Group

- Kerala Ayurveda Ltd.

- Niraamaya Wellness Retreats

- Patanjali Yogpeeth

- Sanjeevanam Ayurveda Hospital

- Shathayu Ayurveda

- Siddhalepa Ayurveda

- Sitaram Ayurveda

- Somatheeram Group

- Sreedhareeyam Ayurvedic Eye Hospital & Research Centre

- Sri Sri Tattva Panchakarma / Sri Sri Wellbeing

- The Raj - Maharishi Ayurveda (USA)

- Vaidyaratnam Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IRDAI Parity for AYUSH Unlocking Insurance-Backed Demand

- 4.2.2 AYUSH Visa And Medical Value Travel Promotion

- 4.2.3 WHO Global Centre for Traditional Medicine Elevates Standards

- 4.2.4 Rapid Growth in Global Wellness Tourism

- 4.2.5 Rising NABH/Quality Accreditation Enabling Cashless/IP Referrals

- 4.2.6 ICD-11 Coding for Ayurveda/Siddha/Unani Improves Reimbursement

- 4.3 Market Restraints

- 4.3.1 Highly Fragmented Provider Base; Limited Standardization

- 4.3.2 Sparse High-Quality Clinical Evidence for Many Indications

- 4.3.3 Insurance Coverage Outside India Remains Limited

- 4.3.4 Accreditation Costs and Compliance Burden for Small Centers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Facility Type

- 5.1.1 Standalone OP Clinics

- 5.1.2 Ayurveda Hospitals (IPD)

- 5.1.3 Panchakarma Day-Care Centres

- 5.1.4 Wellness Retreats/Resorts

- 5.1.5 Other Facilities

- 5.2 By Service Line

- 5.2.1 OPD Consultations & Medicines

- 5.2.2 Panchakarma Detox/Rejuvenation Programs

- 5.2.3 Chronic Disease Management & Rehabilitation

- 5.2.4 Wellness/Aesthetic Programs

- 5.2.5 Other Service Lines

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Amala Ayurvedic Hospital & Research Centre

- 6.3.2 Apollo AyurVAID Hospitals

- 6.3.3 Arya Vaidya Pharmacy

- 6.3.4 Arya Vaidya Sala

- 6.3.5 Ayushakti Ayurveda

- 6.3.6 Barberyn Ayurveda Resorts

- 6.3.7 CGH Earth Ayurveda

- 6.3.8 Jeena Sikho Lifecare

- 6.3.9 Jiva Ayurveda

- 6.3.10 JSS Ayurveda Hospital

- 6.3.11 Kairali Ayurvedic Group

- 6.3.12 Kerala Ayurveda Ltd.

- 6.3.13 Niraamaya Wellness Retreats

- 6.3.14 Patanjali Yogpeeth

- 6.3.15 Sanjeevanam Ayurveda Hospital

- 6.3.16 Shathayu Ayurveda

- 6.3.17 Siddhalepa Ayurveda

- 6.3.18 Sitaram Ayurveda

- 6.3.19 Somatheeram Group

- 6.3.20 Sreedhareeyam Ayurvedic Eye Hospital & Research Centre

- 6.3.21 Sri Sri Tattva Panchakarma / Sri Sri Wellbeing

- 6.3.22 The Raj - Maharishi Ayurveda (USA)

- 6.3.23 Vaidyaratnam Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment